Download as pdf or txt

You might also like

- Lengo Savings Plan PremierDocument9 pagesLengo Savings Plan PremierPado DjochieNo ratings yet

- Boost Fitness Marketing Bootcamp Financial Projection Excel SpreadsheetDocument10 pagesBoost Fitness Marketing Bootcamp Financial Projection Excel SpreadsheetJason BrownNo ratings yet

- Be There For Your Family. Always.: Assure PlusDocument10 pagesBe There For Your Family. Always.: Assure PlusSidhant kumarNo ratings yet

- QC-3654 Guaranteed Wealth Plan Brochure - V5a - 1Document19 pagesQC-3654 Guaranteed Wealth Plan Brochure - V5a - 1202032053 imtnagNo ratings yet

- Contract MahalifegoldDocument6 pagesContract MahalifegoldLohitRamakrishnaKotapatiNo ratings yet

- Wealth Ultima - EnglishDocument2 pagesWealth Ultima - EnglishJagdeesh ShettyNo ratings yet

- PP06201811428 HDFC Life Sanchay (Standard) Retail - Brochure PDFDocument8 pagesPP06201811428 HDFC Life Sanchay (Standard) Retail - Brochure PDFDjddhNo ratings yet

- IndiaFirst Smart Save Plan BrochureDocument16 pagesIndiaFirst Smart Save Plan BrochureVishal SharmaNo ratings yet

- 302 InsuranceDocument15 pages302 InsuranceManoj PundirNo ratings yet

- Super Cash PlanDocument4 pagesSuper Cash PlanShivam RustagiNo ratings yet

- HDFC Life Classic Assure Plus PlanDocument6 pagesHDFC Life Classic Assure Plus PlanPrashant ChaudharyNo ratings yet

- Terms and Conditions Sampoorna Raksha Plus PDFDocument11 pagesTerms and Conditions Sampoorna Raksha Plus PDFSanthi Swetha PudhotaNo ratings yet

- Product Brochure 2Document17 pagesProduct Brochure 2Wajid MohdNo ratings yet

- BSLI Vision LifeSecure Plan Policy ContractDocument6 pagesBSLI Vision LifeSecure Plan Policy ContractCitizen ReporterNo ratings yet

- HDFC Life Click 2 InvestDocument7 pagesHDFC Life Click 2 InvestShaik BademiyaNo ratings yet

- FAMILY INCOME SECURITY - by ENTERPRISE LIFEDocument10 pagesFAMILY INCOME SECURITY - by ENTERPRISE LIFEemmanuelNo ratings yet

- 5032-Sanchay Broucher PDFDocument8 pages5032-Sanchay Broucher PDFChandanNo ratings yet

- Future PerfectDocument11 pagesFuture PerfectAditi SinghNo ratings yet

- Guaranteed Savings Insurance PlanDocument5 pagesGuaranteed Savings Insurance PlanAnoop MannadathilNo ratings yet

- IPru Sarv Jana Suraksha BrochureDocument6 pagesIPru Sarv Jana Suraksha BrochureyesindiacanngoNo ratings yet

- ICICI Future Perfect - BrochureDocument11 pagesICICI Future Perfect - BrochureChandan Kumar SatyanarayanaNo ratings yet

- Meaning of Life Insurance and It Types of PoliciesDocument2 pagesMeaning of Life Insurance and It Types of Policiesshakti ranjan mohanty100% (1)

- IDBI Federal Lifesurance Savings Insurance PlanDocument16 pagesIDBI Federal Lifesurance Savings Insurance PlanKumarniksNo ratings yet

- Samjho Ho Gaya.: Goal AssureDocument21 pagesSamjho Ho Gaya.: Goal AssureshanmugamNo ratings yet

- Guaranteed Income Plan-PD V 3 0 - 20102020Document22 pagesGuaranteed Income Plan-PD V 3 0 - 20102020Sudarshan DeshmukhNo ratings yet

- Diamond Savings Plan-BrochureDocument7 pagesDiamond Savings Plan-BrochureneerajishanNo ratings yet

- Max Life Monthly Income Advantage Plan ProspectusDocument11 pagesMax Life Monthly Income Advantage Plan Prospectushemantchawla89No ratings yet

- Active Income Plan - English PDFDocument2 pagesActive Income Plan - English PDFJagdeesh ShettyNo ratings yet

- Wealth Gain Insurance Plan Brochure V03Document30 pagesWealth Gain Insurance Plan Brochure V03rajlal88No ratings yet

- Ace LeafletDocument24 pagesAce LeafletShyamNo ratings yet

- Term Life Insurance FinalDocument10 pagesTerm Life Insurance FinalsearchingnobodyNo ratings yet

- Secure Income PlanDocument15 pagesSecure Income PlanSuyash PrasadNo ratings yet

- 60002147373Document5 pages60002147373rajputbhupendra787No ratings yet

- Jeevan - Sathi Eng BH PDFDocument2 pagesJeevan - Sathi Eng BH PDFNaygarp IhtapirtNo ratings yet

- IPru Signature LeafletDocument4 pagesIPru Signature LeafletSanju KumavatNo ratings yet

- Future Generali Long Term Income Plan (UIN - 133N090V01) Individual, Non-Linked, Non-Participating (Without Profits), Savings, Life Insurance PlanDocument8 pagesFuture Generali Long Term Income Plan (UIN - 133N090V01) Individual, Non-Linked, Non-Participating (Without Profits), Savings, Life Insurance PlanHSNo ratings yet

- ICICI Pru Signature Online Brochure 230331 150752Document30 pagesICICI Pru Signature Online Brochure 230331 150752Tamil PokkishamNo ratings yet

- Savings Advantage Plan LeafletDocument2 pagesSavings Advantage Plan LeafletNishanthNo ratings yet

- The M. S.University of Baroda - Faculty of Commerce Personal Finance & Investment Unit III - Insurance and Retirement PlanningDocument16 pagesThe M. S.University of Baroda - Faculty of Commerce Personal Finance & Investment Unit III - Insurance and Retirement PlanningSocio Fact'sNo ratings yet

- Smart Growth Brochure Fina 0Document24 pagesSmart Growth Brochure Fina 0Sooraj KuruvathNo ratings yet

- 2149 - ABSLI Nishchit Aayush Plan V04 - One PagerDocument1 page2149 - ABSLI Nishchit Aayush Plan V04 - One PagervamsipalagummiNo ratings yet

- Shriram Life Golden Premier Saver - Website VersionDocument21 pagesShriram Life Golden Premier Saver - Website VersionG YkNo ratings yet

- Edelweiss Tokio Life Wealth Accumulation AcceleratedCover V01 BrochureDocument10 pagesEdelweiss Tokio Life Wealth Accumulation AcceleratedCover V01 BrochureavisekgNo ratings yet

- Term Ins v. Endowment Insurance - PPT (Insurance)Document10 pagesTerm Ins v. Endowment Insurance - PPT (Insurance)Diya MirajNo ratings yet

- Secure Income Plan BrochureDocument18 pagesSecure Income Plan Brochuremantoo kumarNo ratings yet

- Dhan Varsha BrochureDocument16 pagesDhan Varsha BrochureJanagiramanNo ratings yet

- Flexi Care Product BrochureDocument10 pagesFlexi Care Product Brochuremantoo kumarNo ratings yet

- Life BrochureDocument8 pagesLife BrochureHar DonNo ratings yet

- Future Wealth GainDocument23 pagesFuture Wealth GainSudhirGajareNo ratings yet

- Life Insurance SavitaDocument10 pagesLife Insurance Savitasavitashrivastava123No ratings yet

- Tata AIA Life Insurance MoneyBackPlus BrochureDocument6 pagesTata AIA Life Insurance MoneyBackPlus BrochureasfakpaliwalaNo ratings yet

- MGFP BrochureDocument26 pagesMGFP BrochureAbhinesh KumarNo ratings yet

- Brochure Shriram Assured Income Plan Offline PDFDocument12 pagesBrochure Shriram Assured Income Plan Offline PDFVSNo ratings yet

- Brochure DSPDocument8 pagesBrochure DSPCHANDRAKANT RANANo ratings yet

- Company Profile BirlaDocument31 pagesCompany Profile BirlaShivayu VaidNo ratings yet

- ICICI Pru Savings SurakshaDocument8 pagesICICI Pru Savings SurakshaRojan G JosephNo ratings yet

- ICICI Pru Signature Online BrochureDocument30 pagesICICI Pru Signature Online Brochuremyhomemitv2uNo ratings yet

- Tax Free Wealth: Learn the strategies and loopholes of the wealthy on lowering taxes by leveraging Cash Value Life Insurance, 1031 Real Estate Exchanges, 401k & IRA InvestingFrom EverandTax Free Wealth: Learn the strategies and loopholes of the wealthy on lowering taxes by leveraging Cash Value Life Insurance, 1031 Real Estate Exchanges, 401k & IRA InvestingNo ratings yet

- Textbook of Urgent Care Management: Chapter 9, Insurance Requirements for the Urgent Care CenterFrom EverandTextbook of Urgent Care Management: Chapter 9, Insurance Requirements for the Urgent Care CenterNo ratings yet

- VCFGCCDocument9 pagesVCFGCCKyla de SilvaNo ratings yet

- Invoice Shipment ARIH101442 Order PROJECT 224 ADocument1 pageInvoice Shipment ARIH101442 Order PROJECT 224 ASuitable SinghNo ratings yet

- Budget2 FC To FRBMDocument37 pagesBudget2 FC To FRBMbhavyaNo ratings yet

- R. K. Marble Private Limited-12!30!2020Document6 pagesR. K. Marble Private Limited-12!30!2020Brajpal JhalaNo ratings yet

- Macro Economics 10 YearsDocument97 pagesMacro Economics 10 YearsManish Jha 2086No ratings yet

- Demo Account - Simulated Trading: Activity StatementDocument5 pagesDemo Account - Simulated Trading: Activity StatementVIPUL GARGNo ratings yet

- A Project Report On HDFC BankDocument45 pagesA Project Report On HDFC BankMukesh LalNo ratings yet

- Smartprotect Essential 3 BrochureDocument9 pagesSmartprotect Essential 3 BrochureMisc RegisNo ratings yet

- Stock Phoenix - Tweezer TopDocument20 pagesStock Phoenix - Tweezer Toppagis31861No ratings yet

- DerivativesProducts PosterDocument1 pageDerivativesProducts PosterchoubixNo ratings yet

- 3.1. Present WDocument32 pages3.1. Present WAbdulselam AbdurahmanNo ratings yet

- 2022 Property Tax Exemption FormDocument5 pages2022 Property Tax Exemption FormsplouffevachonNo ratings yet

- Manvi PuriDocument2 pagesManvi PuriGaurav GaggarNo ratings yet

- Quiz 1Document10 pagesQuiz 1Raja Ghufran ArifNo ratings yet

- Cost Volume Profit Analysis - Chapter 6Document39 pagesCost Volume Profit Analysis - Chapter 6Maria Maganda MalditaNo ratings yet

- OverviewDocument13 pagesOverviewJimmy KodyNo ratings yet

- RATIO ANALYSIS MbaDocument23 pagesRATIO ANALYSIS MbaManoj KumawatNo ratings yet

- PFF108 LoyaltyCardPlusApplicationForm V07 UPDATEDDocument2 pagesPFF108 LoyaltyCardPlusApplicationForm V07 UPDATEDjane deloviarNo ratings yet

- Bahria University Karachi Campus: Management Sciences Department Class Monday TuesdayDocument6 pagesBahria University Karachi Campus: Management Sciences Department Class Monday TuesdayHabib EjazNo ratings yet

- Index 1. Frequently Asked Question Page 2 2Document11 pagesIndex 1. Frequently Asked Question Page 2 2SnehasreeNo ratings yet

- DocxDocument14 pagesDocxMutiara MahuletteNo ratings yet

- CPChap 2Document79 pagesCPChap 2K59 Hoang Gia HuyNo ratings yet

- Reliance-Communications Urvashi & AmishaDocument27 pagesReliance-Communications Urvashi & Amishakeval soniNo ratings yet

- AME-Chap17-Economic Analysis of Agricultural MachinesDocument5 pagesAME-Chap17-Economic Analysis of Agricultural MachinesJordan YapNo ratings yet

- Audit Mtp2 DoneDocument11 pagesAudit Mtp2 Donegaurav gargNo ratings yet

- 2015 Annual Report v1Document92 pages2015 Annual Report v1Erman CevikkalpNo ratings yet

- Adjustment of Goodwill-Admission PDFDocument2 pagesAdjustment of Goodwill-Admission PDFarnav trivediNo ratings yet

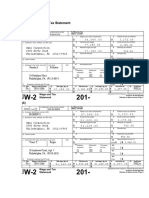

- 4-13B. Wage and Tax Statement: Omni Corporation 4800 River Road Philadelphia, PA 19113-5548Document4 pages4-13B. Wage and Tax Statement: Omni Corporation 4800 River Road Philadelphia, PA 19113-5548KrisnaNo ratings yet