Download as doc, pdf, or txt

You might also like

- Project Management Casebook: Instructor's ManualFrom EverandProject Management Casebook: Instructor's ManualNo ratings yet

- Wembley Project ManagementDocument7 pagesWembley Project ManagementSunny GoyalNo ratings yet

- 6012SSL - Project Management For Business Coursework 1Document19 pages6012SSL - Project Management For Business Coursework 1Thảo My Trương100% (2)

- Project Management Bathroom RemodelDocument25 pagesProject Management Bathroom RemodelAijaz Shaikh67% (3)

- GCU Technical Approach and MethodologyDocument13 pagesGCU Technical Approach and Methodologyqsultan100% (2)

- Assignment-7BU504-100601249 - 1Document14 pagesAssignment-7BU504-100601249 - 1Jayeola Aborode100% (1)

- Project Management PlanDocument30 pagesProject Management PlanSumann Ballaa100% (1)

- Project Turnover and CloseoutDocument31 pagesProject Turnover and Closeoutking jeremiah100% (1)

- Theories and Practice in Project SchedulingDocument67 pagesTheories and Practice in Project SchedulingStephen Kamau100% (2)

- Statement of Management Responsibility (Not Personally Owned)Document1 pageStatement of Management Responsibility (Not Personally Owned)Mabz Buan0% (2)

- APSR-17.7Annual Verification CertificateDocument2 pagesAPSR-17.7Annual Verification CertificatekkkothaNo ratings yet

- Method Statement For An EPC Construction Project - Method Statement HQDocument31 pagesMethod Statement For An EPC Construction Project - Method Statement HQgpjegatheeshNo ratings yet

- Two Construction Supervision & Quality ControlDocument52 pagesTwo Construction Supervision & Quality ControlbolinagNo ratings yet

- Project Brief:: Site Plan (Diagram No. 1)Document14 pagesProject Brief:: Site Plan (Diagram No. 1)KarthikNo ratings yet

- Project AuditDocument37 pagesProject Auditakanksha.guptaNo ratings yet

- Official Assignment PDFDocument23 pagesOfficial Assignment PDFAnt PhweNo ratings yet

- Construction Engineering Ce 332-Lecture Notes 2014Document135 pagesConstruction Engineering Ce 332-Lecture Notes 2014Tosin Opawole100% (4)

- Project Management - Kumar AnimeshDocument7 pagesProject Management - Kumar Animeshkumaranimesh2606No ratings yet

- TTCL Vietnam Corporation LimitedDocument4 pagesTTCL Vietnam Corporation LimitedLinh GiangNo ratings yet

- BEN 610 Assignment 1: Post Project Review Report On "Remodelling of Terminal 1 at The Heathrow Airport, UK"Document8 pagesBEN 610 Assignment 1: Post Project Review Report On "Remodelling of Terminal 1 at The Heathrow Airport, UK"Quel Domingo EspinNo ratings yet

- Scheduling and Financial Analysis of A High Rise Building: E. Suresh Kumar S.KrishnamoorthiDocument6 pagesScheduling and Financial Analysis of A High Rise Building: E. Suresh Kumar S.KrishnamoorthiIOSRjournalNo ratings yet

- Saep 14 PDFDocument48 pagesSaep 14 PDFRami Elloumi100% (1)

- uc-8 Presentation UPADATEDocument36 pagesuc-8 Presentation UPADATEDaniel tesfayNo ratings yet

- Project Management Civil EngineersDocument32 pagesProject Management Civil EngineersJenifer JosephNo ratings yet

- Project Execution Plan: For Archetype For Client Reviewed by Approved by Reviewed byDocument35 pagesProject Execution Plan: For Archetype For Client Reviewed by Approved by Reviewed byGia Vinh Bui TranNo ratings yet

- Ara 1Document48 pagesAra 1Anonymous 4IpmN7On0% (1)

- 6 S 7 o FZ47 Lhyir Ne JQFEEqd CT89 ZLML 8 Zls VKAwp EDocument7 pages6 S 7 o FZ47 Lhyir Ne JQFEEqd CT89 ZLML 8 Zls VKAwp Ejing qiangNo ratings yet

- CHAPTER 2 (Introduction To The Construction Industry)Document16 pagesCHAPTER 2 (Introduction To The Construction Industry)Saidatul SazwaNo ratings yet

- 4.0. Management PlanDocument6 pages4.0. Management Plannormchuma87No ratings yet

- Assignments-Mba Sem-Ii: Subject Code: MB0033Document32 pagesAssignments-Mba Sem-Ii: Subject Code: MB0033Mithesh KumarNo ratings yet

- Construction 1Document3 pagesConstruction 1T N Roland BourgeNo ratings yet

- Reclamation Manual: Subject: PurposeDocument11 pagesReclamation Manual: Subject: PurposealfonsxxxNo ratings yet

- 93 Lansdowne Road: Prepared in Accordance With The Site Waste Management Plans Regulations 2008Document11 pages93 Lansdowne Road: Prepared in Accordance With The Site Waste Management Plans Regulations 2008Asif HussainNo ratings yet

- Section 5. Terms of Reference: Annexure - ADocument26 pagesSection 5. Terms of Reference: Annexure - AsalemmanojNo ratings yet

- Five (5) Storey AMH Office Building: Project Management Plan For The Design of The ProposedDocument11 pagesFive (5) Storey AMH Office Building: Project Management Plan For The Design of The ProposedJenna PallarcaNo ratings yet

- MobilizationDocument46 pagesMobilizationarsaban50% (2)

- MoM Meeting PSG - ADC - LJHC-TH - ETBDocument3 pagesMoM Meeting PSG - ADC - LJHC-TH - ETBJoseph NguyenNo ratings yet

- BRT-Peshawer-Package-I-Reach-I - METHOD STATEMENTDocument66 pagesBRT-Peshawer-Package-I-Reach-I - METHOD STATEMENTRizwanNo ratings yet

- PM Handbook (Full PDFDocument88 pagesPM Handbook (Full PDFGary LoNo ratings yet

- Macaraig, Ryan M., 2016-02810-MN-0, CM600 Assignment No. 3Document12 pagesMacaraig, Ryan M., 2016-02810-MN-0, CM600 Assignment No. 3RyanNo ratings yet

- 21 10 06 Impact of Adverse Weather Conditions On Completion Time of Offshore Construction ProjectsDocument131 pages21 10 06 Impact of Adverse Weather Conditions On Completion Time of Offshore Construction ProjectsJuan Carlos PiñeiroNo ratings yet

- Assignment Nicmar / Code Office: Site Organization & Management Reg. No. - 217-09-11-51049-2194Document15 pagesAssignment Nicmar / Code Office: Site Organization & Management Reg. No. - 217-09-11-51049-2194Manvendra singhNo ratings yet

- Introduction To Project Management: Subject Code - PM0010Document10 pagesIntroduction To Project Management: Subject Code - PM0010Umesh BabuNo ratings yet

- PMT 30103Document41 pagesPMT 30103Yousef Adel HassanenNo ratings yet

- Mom Commitment Meeting PSG - Adc - LJHC-TH - EtbDocument6 pagesMom Commitment Meeting PSG - Adc - LJHC-TH - EtbJoseph NguyenNo ratings yet

- Construction of MRT Feeder Bus Depot and Related Supporting Buildings and Facilities For The KVMRT Project, SBK LineDocument5 pagesConstruction of MRT Feeder Bus Depot and Related Supporting Buildings and Facilities For The KVMRT Project, SBK LineIkhwan HishamNo ratings yet

- 2023 PM (3-Con-Cá)Document30 pages2023 PM (3-Con-Cá)Hoàng KhangNo ratings yet

- Latest ReportDocument45 pagesLatest ReportFaizal AbdullahNo ratings yet

- Mb0033 Project Management Set 1Document20 pagesMb0033 Project Management Set 1Mohd ShahidNo ratings yet

- Project ControlDocument4 pagesProject ControlVishal TiwariNo ratings yet

- Method StatemntDocument123 pagesMethod StatemntAhmed BadawyNo ratings yet

- CRS Project-Management-PlanDocument12 pagesCRS Project-Management-PlanGervie Cabang PalattaoNo ratings yet

- Assignment No 4 - Site Organization and ManagmentDocument15 pagesAssignment No 4 - Site Organization and Managmentchettriranjan75% (4)

- Project ManagementDocument23 pagesProject ManagementabhisonaliNo ratings yet

- ToR - Qaisar-Laman PDFDocument22 pagesToR - Qaisar-Laman PDFGolam MasudNo ratings yet

- BTQS3042 Tutorial Notes 1Document3 pagesBTQS3042 Tutorial Notes 1WEI LI NEOHNo ratings yet

- Basic Fundamental of Construction ManagementDocument13 pagesBasic Fundamental of Construction ManagementMANTHANKUMAR VAGHANINo ratings yet

- Chap 3c Project ManagementDocument9 pagesChap 3c Project ManagementArianNo ratings yet

- Execution PlanDocument21 pagesExecution PlanTariq KhanNo ratings yet

- Career Change From Real Estate to Oil and Gas ProjectsFrom EverandCareer Change From Real Estate to Oil and Gas ProjectsRating: 5 out of 5 stars5/5 (1)

- Integrated Project Planning and Construction Based on ResultsFrom EverandIntegrated Project Planning and Construction Based on ResultsNo ratings yet

- Guidelines for Estimating Greenhouse Gas Emissions of ADB Projects: Additional Guidance for Clean Energy ProjectsFrom EverandGuidelines for Estimating Greenhouse Gas Emissions of ADB Projects: Additional Guidance for Clean Energy ProjectsNo ratings yet

- 033&117-Sergio F. Naguiat vs. NLRC 269 Scra 564 (1997)Document11 pages033&117-Sergio F. Naguiat vs. NLRC 269 Scra 564 (1997)wewNo ratings yet

- The History of Romanian CoinsDocument139 pagesThe History of Romanian CoinsDoru Sicoe100% (2)

- Chapter 7 Financial Statments AnalysisDocument44 pagesChapter 7 Financial Statments AnalysisAddisalem MesfinNo ratings yet

- Accounting Assignment & CATDocument14 pagesAccounting Assignment & CATMargaret IrunguNo ratings yet

- Ultiple Choice QuestionsDocument10 pagesUltiple Choice QuestionssakfeeNo ratings yet

- LESSON-19 Central Excise Laws: StructureDocument21 pagesLESSON-19 Central Excise Laws: Structuresudhir.kochhar3530No ratings yet

- MW STJ 08252016Document34 pagesMW STJ 08252016medtechyNo ratings yet

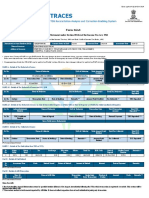

- Form 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961Document3 pagesForm 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961Vikas VidhurNo ratings yet

- Land Law: Session Three Easements, Profits and MortgagesDocument39 pagesLand Law: Session Three Easements, Profits and MortgagesAngel MoongaNo ratings yet

- CF 2Document2 pagesCF 2shahidameen2No ratings yet

- AFM Cash Flow StatementDocument13 pagesAFM Cash Flow StatementSusheel KumarNo ratings yet

- 185cf432 The Role of NGOs SHGS Development Processes WWW - Visionias.inDocument13 pages185cf432 The Role of NGOs SHGS Development Processes WWW - Visionias.inSuresh RVNo ratings yet

- Harley Davidson Strategic Management Changed NewDocument33 pagesHarley Davidson Strategic Management Changed NewDevina GuptaNo ratings yet

- Performance ManagementDocument100 pagesPerformance ManagementBasavanagowda GowdaNo ratings yet

- Chapter 1 PresentationDocument39 pagesChapter 1 PresentationSagni Oo ChambNo ratings yet

- Electrical Machinery - Make in IndiaDocument3 pagesElectrical Machinery - Make in IndiaBitan GhoshNo ratings yet

- Book - Kentanddang 2020en PDFDocument186 pagesBook - Kentanddang 2020en PDFAbeMatNo ratings yet

- Npa Vivek Sip 123456Document52 pagesNpa Vivek Sip 123456Vivek rathodNo ratings yet

- Midterms Sa2 FARDocument6 pagesMidterms Sa2 FAREloiNo ratings yet

- Warren SM CH 02 Final PDFDocument66 pagesWarren SM CH 02 Final PDFSandra0% (1)

- Infrastructure Sector 230720 JM Fin Initiating Coverage Riding ADocument159 pagesInfrastructure Sector 230720 JM Fin Initiating Coverage Riding AAbhishek KatkamNo ratings yet

- Month Day Month Day: 526-1212, Extension 2403 / 8231-10-73 (Temporary)Document209 pagesMonth Day Month Day: 526-1212, Extension 2403 / 8231-10-73 (Temporary)Ivan ChiuNo ratings yet

- Investasi Sementara Pada ObligasiDocument34 pagesInvestasi Sementara Pada ObligasiAli-ImronNo ratings yet

- Financial Management - Eugene F. Brigham and Michael C. Ehrhardt - 20086Document5 pagesFinancial Management - Eugene F. Brigham and Michael C. Ehrhardt - 20086Oronno Afridi0% (2)

- Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument65 pagesDate Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalancePardeep KumarNo ratings yet

- Beams12ge Im12Document4 pagesBeams12ge Im12ElaNo ratings yet

- Few Successful Entrepreneurship Stories For RecruitmentDocument15 pagesFew Successful Entrepreneurship Stories For RecruitmentpallavcNo ratings yet

- SICHOTS240114220Document1 pageSICHOTS240114220Sandu MonicaNo ratings yet