Download as pdf or txt

You might also like

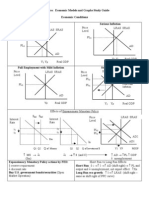

- AP Macroeconomic Models and Graphs Study GuideDocument23 pagesAP Macroeconomic Models and Graphs Study GuideAznAlexT90% (21)

- BBA-1st Sem Micro Economics NotesDocument126 pagesBBA-1st Sem Micro Economics Notesrajvinder deol83% (83)

- The General Theory of Employment, Interest and Money. IllustratedFrom EverandThe General Theory of Employment, Interest and Money. IllustratedRating: 3.5 out of 5 stars3.5/5 (18)

- Chapter 24. Epilogue: The Story of Macroeconomics: I. Motivating QuestionDocument4 pagesChapter 24. Epilogue: The Story of Macroeconomics: I. Motivating QuestionAhmad Alatas100% (1)

- Keynesian RevolutionDocument4 pagesKeynesian RevolutionRakesh KumarNo ratings yet

- Permasalahan Ekonomi Dalam Sistem EkonomiDocument25 pagesPermasalahan Ekonomi Dalam Sistem EkonomiHiskia SinagaNo ratings yet

- Lesson 3 - Time Value of MoneyDocument122 pagesLesson 3 - Time Value of MoneyJannine Joyce Bergonio33% (3)

- Cooperative Banking ProjectDocument53 pagesCooperative Banking ProjectselvamNo ratings yet

- Negotiating by HarwardDocument42 pagesNegotiating by HarwardzapshaNo ratings yet

- Assignment 2Document25 pagesAssignment 2Jiaxi WNo ratings yet

- Block 4Document41 pagesBlock 4Binita SherpaNo ratings yet

- LET MacroeconomicsMicroeconomicsDocument7 pagesLET MacroeconomicsMicroeconomicsMay-Ann S. CahiligNo ratings yet

- Block 4Document42 pagesBlock 4harshjindal941No ratings yet

- Edem ClassicalDocument7 pagesEdem ClassicalMarcus BansahNo ratings yet

- The Relevance of The Classical Theory Under Modern ConditionsDocument10 pagesThe Relevance of The Classical Theory Under Modern ConditionsPawa12No ratings yet

- Published in 1936 The Interpretations of Keynes Are Contentious, andDocument14 pagesPublished in 1936 The Interpretations of Keynes Are Contentious, andPratik PatelNo ratings yet

- Notes On Macro Economics With Keynes Theory PDFDocument46 pagesNotes On Macro Economics With Keynes Theory PDFShalini Singh IPSANo ratings yet

- Economics and EconomistsDocument94 pagesEconomics and EconomistsbrokenwingsfairyNo ratings yet

- Unit 4 Classical and Keynesian Systems: 4.0 ObjectivesDocument28 pagesUnit 4 Classical and Keynesian Systems: 4.0 ObjectivesHemant KumarNo ratings yet

- 11 Types of Economic TheoryDocument6 pages11 Types of Economic Theorydinesh kumarNo ratings yet

- New Classical MacroeconomicsDocument3 pagesNew Classical Macroeconomicslutfunnessabegum66No ratings yet

- Macro Economics: DR Jyotishree PandeyDocument12 pagesMacro Economics: DR Jyotishree PandeyJyotishree PandeyNo ratings yet

- Economics Module - I-1Document66 pagesEconomics Module - I-1Neet 720No ratings yet

- Neoclassical EconomicsDocument8 pagesNeoclassical EconomicsYob YnnosNo ratings yet

- Micro and Macro: The Economic Divide: Economics Is Split Into Two Realms: The Overall Economy and Individual MarketsDocument2 pagesMicro and Macro: The Economic Divide: Economics Is Split Into Two Realms: The Overall Economy and Individual Markets--No ratings yet

- Understanding Economics and The Overwiew of The EconomyDocument7 pagesUnderstanding Economics and The Overwiew of The EconomyKathkath PlacenteNo ratings yet

- Notes On ME (2) Unit 1Document16 pagesNotes On ME (2) Unit 1Shashwat SinhaNo ratings yet

- Neo Classical EconomicsDocument5 pagesNeo Classical EconomicsLadiaBagrasNo ratings yet

- Keynesian Schools of ThoughtDocument3 pagesKeynesian Schools of ThoughtSanskaar SharmaNo ratings yet

- Classical vs. Keynesian EconomicsDocument7 pagesClassical vs. Keynesian EconomicsRamon VillarealNo ratings yet

- CHAPTER-1 EconDocument16 pagesCHAPTER-1 EconRonah SabanalNo ratings yet

- Branches of EconomicsDocument3 pagesBranches of EconomicsJezreeljeanne Largo CaparosoNo ratings yet

- Field of EconomicsDocument5 pagesField of EconomicsVinod JoshiNo ratings yet

- Unit-5 Macro EconomicsDocument16 pagesUnit-5 Macro EconomicsYash JainNo ratings yet

- Microeconimics Handout Chapter 1Document8 pagesMicroeconimics Handout Chapter 1John Henry ParungaoNo ratings yet

- Report On Economic Development 1Document93 pagesReport On Economic Development 1Crizzia Oblepias SantillaNo ratings yet

- Lesson 1Document46 pagesLesson 1Maurice ZorillaNo ratings yet

- (9781786439857 - Money, Method and Contemporary Post-Keynesian Economics) IntroductionDocument14 pages(9781786439857 - Money, Method and Contemporary Post-Keynesian Economics) IntroductionCaio CésarNo ratings yet

- Ipe Working Paper 32Document43 pagesIpe Working Paper 32Krezel kaye BarbadilloNo ratings yet

- Ch2 Macro ThoughtDocument32 pagesCh2 Macro ThoughtLewoye BantieNo ratings yet

- Macroeconomics: Sana BashirDocument13 pagesMacroeconomics: Sana BashirAbdullah AliNo ratings yet

- 20th CenturyDocument6 pages20th Centuryagapitodimagiba021No ratings yet

- Using MINITAB's Graph MenuDocument21 pagesUsing MINITAB's Graph MenuAli PopiNo ratings yet

- Keynesian ThesisDocument4 pagesKeynesian Thesismichellespragueplano100% (2)

- Eigna QueenDocument12 pagesEigna QueenAngie May Castroverde CañoneroNo ratings yet

- Keynesian EconomicsDocument12 pagesKeynesian EconomicsSheilaNo ratings yet

- Development of Economic ThinkingDocument30 pagesDevelopment of Economic ThinkingPeris WanjikuNo ratings yet

- Economics CHPTDocument7 pagesEconomics CHPTDarshit BhovarNo ratings yet

- Ch2 Macro ThoughtDocument25 pagesCh2 Macro ThoughtProveedor Iptv EspañaNo ratings yet

- Economic Way of ThinkingDocument32 pagesEconomic Way of Thinkingailyn eleginoNo ratings yet

- Marxian Critique of Classical EconomicsDocument11 pagesMarxian Critique of Classical EconomicsPravin Dhas100% (1)

- Lecture 1, NijhuDocument9 pagesLecture 1, NijhuNizhum FarzanaNo ratings yet

- Economic TheoryDocument9 pagesEconomic TheoryAlano S. LimgasNo ratings yet

- Economics and Its NatureDocument4 pagesEconomics and Its NatureElrey IncisoNo ratings yet

- Module 1 MicroEconomicsDocument29 pagesModule 1 MicroEconomicsjustin vasquezNo ratings yet

- Lesson 1-8 Economic DevelopmentDocument43 pagesLesson 1-8 Economic DevelopmentRachelleNo ratings yet

- Ballb 118Document52 pagesBallb 118justforworkmail.eduNo ratings yet

- MA I Short Note For Extit TutorDocument43 pagesMA I Short Note For Extit TutorTesfaye GutaNo ratings yet

- Economic 1Document21 pagesEconomic 1abaye2013No ratings yet

- History: DiscoveringDocument20 pagesHistory: DiscoveringDaniel Gabriel PunoNo ratings yet

- BBA 1st Sem Micro Economics NotesDocument128 pagesBBA 1st Sem Micro Economics NotesJEMALYN TURINGAN0% (1)

- Chapter 1Document6 pagesChapter 1othmane.hamidiNo ratings yet

- Micro and MacroeconomicsDocument4 pagesMicro and MacroeconomicsAlice Dalina100% (1)

- Economic Schools of ThoughtDocument14 pagesEconomic Schools of ThoughtSOUMYA BABYNo ratings yet

- Maths Pamphlet Kyawama-1 PDFDocument25 pagesMaths Pamphlet Kyawama-1 PDFJoseph MayelanoNo ratings yet

- Project WorkDocument65 pagesProject WorkTikendra BhandariNo ratings yet

- Revised GR 01 04 2017 08112017Document13 pagesRevised GR 01 04 2017 08112017jimbarotNo ratings yet

- Project Profile On The Establishment of Palm Beach Resort at BatticoloaDocument33 pagesProject Profile On The Establishment of Palm Beach Resort at BatticoloaCyril PathiranaNo ratings yet

- Computation of Simple InterestDocument14 pagesComputation of Simple InterestMartin De VillaNo ratings yet

- Applied Economics: Module No. 1: Week 1: First QuarterDocument8 pagesApplied Economics: Module No. 1: Week 1: First QuarterGellegani, Julius100% (1)

- EXIM Bank Internship ReportDocument32 pagesEXIM Bank Internship ReportOdhora ShiponNo ratings yet

- Ross 12e PPT Ch06 CalculatorDocument71 pagesRoss 12e PPT Ch06 CalculatorKirthagan SelvamNo ratings yet

- Loan Agreement: I. Terms of Repayment A. PaymentsDocument3 pagesLoan Agreement: I. Terms of Repayment A. PaymentsKennedy Willson IboboNo ratings yet

- Currency WarDocument20 pagesCurrency WarBhumiNo ratings yet

- DlptypesofweedsDocument23 pagesDlptypesofweedsKathlen Aiyanna Salvan BuhatNo ratings yet

- HBS Introduction To Bonds and Bond Math 5170-PDF-ENG (1) (01-30) (16-30)Document15 pagesHBS Introduction To Bonds and Bond Math 5170-PDF-ENG (1) (01-30) (16-30)LorennarNo ratings yet

- Pilipinas Bank Vs CADocument2 pagesPilipinas Bank Vs CA001noone100% (1)

- 12 Acc 1 ModelDocument11 pages12 Acc 1 ModeljessNo ratings yet

- Universal Partnership of ProfitsDocument4 pagesUniversal Partnership of ProfitsSambile Clint LloydNo ratings yet

- Tally - ERP 9 at A Glance - Book6 PDFDocument10 pagesTally - ERP 9 at A Glance - Book6 PDFAyush BishtNo ratings yet

- Statement 36823447Document7 pagesStatement 36823447Robert SchumannNo ratings yet

- Loan Management System Project Documentation PDFDocument14 pagesLoan Management System Project Documentation PDFAbhishek Dangol0% (1)

- Yeow Guang Cheng V Tang Lee Hiok & Ors (2020) 1 LNS 1696Document67 pagesYeow Guang Cheng V Tang Lee Hiok & Ors (2020) 1 LNS 1696Nurshaura AzrinNo ratings yet

- Foundation Program 2021-22 Case Study and Report Generation CASE - 1 (Extra) Hindustan Housing CompanyDocument5 pagesFoundation Program 2021-22 Case Study and Report Generation CASE - 1 (Extra) Hindustan Housing CompanyRaj ThakurNo ratings yet

- Las AllDocument14 pagesLas AllDovylle Nazareth AndalesNo ratings yet

- Winfield RefuseDocument5 pagesWinfield RefuseAbhishek BaratamNo ratings yet

- STD IX, Economics, Unit 1, NotesDocument7 pagesSTD IX, Economics, Unit 1, NoteswhoeverNo ratings yet

- Problem Set EconDocument22 pagesProblem Set EconDaniel Viterbo RodriguezNo ratings yet

- ACN002 Midterm Exam PDFDocument5 pagesACN002 Midterm Exam PDFjennie kyutiNo ratings yet