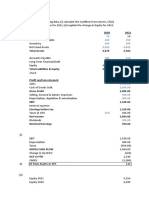

IAS7-Q4

IAS7-Q4

You might also like

- MMZ Accountancy School PH 09 453197062: 15 Mark Questions: Preparing Simple Consolidated Financial StatementsDocument7 pagesMMZ Accountancy School PH 09 453197062: 15 Mark Questions: Preparing Simple Consolidated Financial StatementsSerena100% (1)

- Segregation of Duties MatrixDocument13 pagesSegregation of Duties MatrixForumnoj100% (1)

- Contoh Soal Pelaporan KorporatDocument4 pagesContoh Soal Pelaporan Korporatirma cahyani kawi0% (1)

- CR Inter QuestionsDocument22 pagesCR Inter QuestionsRichie BoomaNo ratings yet

- Question 5: Ias 7 Statements of Cash FlowsDocument4 pagesQuestion 5: Ias 7 Statements of Cash FlowsShiza ArifNo ratings yet

- Statement of Cash Flow - Thorstved CoDocument5 pagesStatement of Cash Flow - Thorstved Cotun ibrahimNo ratings yet

- Income Statements For The November: @Chapter7AnalyslngandlnterpretlngflnanclalstatementsDocument1 pageIncome Statements For The November: @Chapter7AnalyslngandlnterpretlngflnanclalstatementsAik Luen LimNo ratings yet

- Thegodfather CF Student CdADocument8 pagesThegodfather CF Student CdAPablo MichavilaNo ratings yet

- SCF With DODocument3 pagesSCF With DOMuhammad Asif KhanNo ratings yet

- 2021 Seminar Paper Marking SchemeDocument12 pages2021 Seminar Paper Marking Schemesayuru423geenethNo ratings yet

- Statement of Financial Position As at 31st March 2015Document52 pagesStatement of Financial Position As at 31st March 2015Shameel IrshadNo ratings yet

- CORPORATE REPORTING Icag PDFDocument31 pagesCORPORATE REPORTING Icag PDFmohedNo ratings yet

- Notes Before UTSDocument20 pagesNotes Before UTSdevina utamiNo ratings yet

- Cash Flows Tutorial QuestionsDocument6 pagesCash Flows Tutorial Questionssmlingwa100% (1)

- Test 1Document3 pagesTest 1tshepomoejanejrNo ratings yet

- ACCT 4200 Project Solution - Final Posting 2022Document14 pagesACCT 4200 Project Solution - Final Posting 2022Jaspal SinghNo ratings yet

- Mock Exam FRPM SolutionDocument45 pagesMock Exam FRPM SolutionangelitayosecasetiawanNo ratings yet

- Anandam Case AnalysisDocument5 pagesAnandam Case AnalysisVini ShethNo ratings yet

- 91406-res-2021Document4 pages91406-res-2021grace.padfield2006No ratings yet

- ACCT 4200 Project Solution - Final Posting 2022Document15 pagesACCT 4200 Project Solution - Final Posting 2022Jaspal SinghNo ratings yet

- AccntsDocument10 pagesAccntsLav RamgopalNo ratings yet

- Qantas DataDocument31 pagesQantas DataChip choiNo ratings yet

- Acct 401 Tutorial Set FiveDocument13 pagesAcct 401 Tutorial Set FiveStudy GirlNo ratings yet

- 7001 Assignment #3Document9 pages7001 Assignment #3南玖No ratings yet

- Class Discussion On Ratios 28022023Document2 pagesClass Discussion On Ratios 28022023lil telNo ratings yet

- Class Day Test BSC Finance Year 2Document5 pagesClass Day Test BSC Finance Year 2Revatee HurilNo ratings yet

- Hartalega Holdings Berhad (Malaysia) : Source: - WVB - Financial Standard For Industrial CompaniesDocument6 pagesHartalega Holdings Berhad (Malaysia) : Source: - WVB - Financial Standard For Industrial CompaniesJUWAIRIA BINTI SADIKNo ratings yet

- Osborne Answers - Work Book Year 2Document44 pagesOsborne Answers - Work Book Year 2deshawnosae12No ratings yet

- W2D2C1&2 Interpretation FS ActivitiesDocument13 pagesW2D2C1&2 Interpretation FS ActivitiesMaximillian GleichmannNo ratings yet

- Finacial Accounting Ii FA260US ASSIGNMENT 1 (5 Group Member Only) Faculty Department Course Course Code Due Date Possible Marks Examiner (S) Moderator InstructionsDocument5 pagesFinacial Accounting Ii FA260US ASSIGNMENT 1 (5 Group Member Only) Faculty Department Course Course Code Due Date Possible Marks Examiner (S) Moderator InstructionsJohanna AseliNo ratings yet

- Workshop 5 QsDocument7 pagesWorkshop 5 QsNaresh SehdevNo ratings yet

- Fa 6 Ans Key Q.P Code 75847 PDFDocument16 pagesFa 6 Ans Key Q.P Code 75847 PDFAmar ChapniyaNo ratings yet

- JengaCashFlowExercise 1546983290168Document3 pagesJengaCashFlowExercise 1546983290168rex100% (1)

- ITAE Financial Datasheet Summer 2024 Final (15084)Document4 pagesITAE Financial Datasheet Summer 2024 Final (15084)sahil95867No ratings yet

- Ratio AnalysisDocument17 pagesRatio Analysisdora76pataNo ratings yet

- Jenga Cashflow ExerciseDocument2 pagesJenga Cashflow ExerciseHue PhamNo ratings yet

- CILO 4 - Prepare The Financial Statements.: Profit or Loss)Document5 pagesCILO 4 - Prepare The Financial Statements.: Profit or Loss)Neama1 RadhiNo ratings yet

- E TranspharmaDocument7 pagesE TranspharmaLucas Moraes Teixeira SalgadoNo ratings yet

- Corporate Financial Reporting PDFDocument3 pagesCorporate Financial Reporting PDFIshan SharmaNo ratings yet

- C 20: C C F: Hapter Onsolidation ASH LowsDocument1 pageC 20: C C F: Hapter Onsolidation ASH Lows.No ratings yet

- Financial Statement ACIFL 31 March 2015 ConsolidatedDocument16 pagesFinancial Statement ACIFL 31 March 2015 ConsolidatedNurhan JaigirdarNo ratings yet

- Assignment 7 SolutionsDocument10 pagesAssignment 7 SolutionsjoanNo ratings yet

- Statement of Cash FlowsDocument12 pagesStatement of Cash FlowsDaniel PeterNo ratings yet

- Rivera and Santos PartnershipDocument31 pagesRivera and Santos PartnershipDaneca GallardoNo ratings yet

- Хариу HW2 ACC732Document6 pagesХариу HW2 ACC732ZayaNo ratings yet

- AMARILODocument8 pagesAMARILOIngrid Molina GarciaNo ratings yet

- Lecture 1 & 2 ExamplesDocument5 pagesLecture 1 & 2 ExamplesAbubakari Abdul MananNo ratings yet

- Cash Flow (Exercise)Document5 pagesCash Flow (Exercise)abhishekvora7598752100% (1)

- Mo Hinh Ky Thuat Phan Tich Tai ChinhDocument39 pagesMo Hinh Ky Thuat Phan Tich Tai ChinhĐào Mạnh Quân Pete'rNo ratings yet

- Act 3602. Chapter 3. Prob.3-39 HomeworkDocument3 pagesAct 3602. Chapter 3. Prob.3-39 HomeworkphanupongnineNo ratings yet

- Ratio AnlysDocument5 pagesRatio AnlysVi PhuongNo ratings yet

- JengaCashFlowExercise 1546983290168Document2 pagesJengaCashFlowExercise 1546983290168Vibhuti BatraNo ratings yet

- Chapter 7 Up StreamDocument14 pagesChapter 7 Up StreamAditya Agung SatrioNo ratings yet

- FAWCM - Cash Flow 2Document29 pagesFAWCM - Cash Flow 2Jake RoosenbloomNo ratings yet

- Accounting IAS (Malaysia) Model Answers Series 2 2007 Old SyllabusDocument18 pagesAccounting IAS (Malaysia) Model Answers Series 2 2007 Old SyllabusAung Zaw HtweNo ratings yet

- Evaluating Financial PerformanceDocument31 pagesEvaluating Financial PerformanceShahruk AnwarNo ratings yet

- MR D.I.Y. Group (M) Berhad: Interim Financial Report For The Third Quarter Ended 30 September 2020Document15 pagesMR D.I.Y. Group (M) Berhad: Interim Financial Report For The Third Quarter Ended 30 September 2020Mzm Zahir MzmNo ratings yet

- FRS 107 Ie 2016BBDocument10 pagesFRS 107 Ie 2016BBAmelia RahmawatiNo ratings yet

- Tutorial 8Document6 pagesTutorial 8WEI QUAN LEENo ratings yet

- OLC Chap 5Document6 pagesOLC Chap 5Isha SinghNo ratings yet

- Equity Valuation: Models from Leading Investment BanksFrom EverandEquity Valuation: Models from Leading Investment BanksJan ViebigNo ratings yet

- XdfdhfheDocument2 pagesXdfdhfheKrishna 11No ratings yet

- ZOHO TrainingDocument4 pagesZOHO TrainingKrishna 11No ratings yet

- If Mr. Paul Resided in The UK For ADocument1 pageIf Mr. Paul Resided in The UK For AKrishna 11No ratings yet

- General LedgerDocument3 pagesGeneral LedgerKrishna 11No ratings yet

- Abc FR129Document3 pagesAbc FR129Krishna 11No ratings yet

- Abc FR264Document1 pageAbc FR264Krishna 11No ratings yet

- Analysing Institutional and Government Support ForDocument3 pagesAnalysing Institutional and Government Support ForKrishna 11No ratings yet

- ACA 2022 Syllabus Handbook Advanced Corporate ReportingDocument35 pagesACA 2022 Syllabus Handbook Advanced Corporate ReportingNishhhhiiiNo ratings yet

- Prakash Jhunjhunwala & Co LLP: Chartered AccountantsDocument9 pagesPrakash Jhunjhunwala & Co LLP: Chartered AccountantsKinshuk SinghNo ratings yet

- Citi Bank Statement Feb 2022Document6 pagesCiti Bank Statement Feb 2022Akshay SinghNo ratings yet

- EB - Romney - AIS13wm 405 440 16 20Document5 pagesEB - Romney - AIS13wm 405 440 16 20Mayang SariNo ratings yet

- AIS ch09Document151 pagesAIS ch09Syarief HuseinNo ratings yet

- Dokumen - Tips 6018 p3 SPK Lembar Kerja Menyelesaikan Siklus AkuntansiDocument22 pagesDokumen - Tips 6018 p3 SPK Lembar Kerja Menyelesaikan Siklus AkuntansiM IkhsanNo ratings yet

- Financial ManagementDocument88 pagesFinancial ManagementSomevi Bright KodjoNo ratings yet

- Break-Even Point and Cost-Volume-Profit AnalysisDocument44 pagesBreak-Even Point and Cost-Volume-Profit AnalysisKhánh Đoan NgôNo ratings yet

- Business CombinationDocument7 pagesBusiness CombinationJae DenNo ratings yet

- Material Cost 01 - Class Notes - Udesh Regular - Group 1Document8 pagesMaterial Cost 01 - Class Notes - Udesh Regular - Group 1Shubham KumarNo ratings yet

- Pre - Board Examination - Accountancy - Class XII - (2022-23)Document12 pagesPre - Board Examination - Accountancy - Class XII - (2022-23)Shipra GumberNo ratings yet

- Occupied 500: Area FT.) Light PointsDocument10 pagesOccupied 500: Area FT.) Light PointsAbhijit HoroNo ratings yet

- Financial Accounting Objectives Sem V PDFDocument14 pagesFinancial Accounting Objectives Sem V PDFAyman MalikNo ratings yet

- Limitations of Conceptual Framework PDFDocument20 pagesLimitations of Conceptual Framework PDFGeorge Buliki100% (25)

- Ross Fundamentals of Corporate Finance 13e CH10 PPT AccessibleDocument38 pagesRoss Fundamentals of Corporate Finance 13e CH10 PPT AccessibleAdriana RisiNo ratings yet

- Siklus CahayaDocument27 pagesSiklus CahayaBangYonnNo ratings yet

- Midterm - Chapter 4Document78 pagesMidterm - Chapter 4JoshrylNo ratings yet

- Daftar PustakaDocument5 pagesDaftar PustakaWinda AyuNo ratings yet

- Course OutlineDocument4 pagesCourse Outlinetacamp daNo ratings yet

- Understanding Financial StatementDocument14 pagesUnderstanding Financial StatementNHELBY VERAFLORNo ratings yet

- 3512 Chapter 23 Cash Flows HW Exercises ProblemsDocument12 pages3512 Chapter 23 Cash Flows HW Exercises ProblemsM MustafaNo ratings yet

- Answer-Key Acco-201 Intacc2 Mte 1say2324Document8 pagesAnswer-Key Acco-201 Intacc2 Mte 1say2324John cookNo ratings yet

- Financial Accounting Class 11 NotesDocument7 pagesFinancial Accounting Class 11 NotesAnkush ThakurNo ratings yet

- Chapter 26 Marginal Costing and Cost Volume Profit AnalysisDocument25 pagesChapter 26 Marginal Costing and Cost Volume Profit Analysisorkuting84% (73)

- Solution Manual For Accounting Information Systems 3rd Edition Vernon Richardson Chengyee Chang Rod SmithDocument13 pagesSolution Manual For Accounting Information Systems 3rd Edition Vernon Richardson Chengyee Chang Rod SmithJessica Wyke100% (38)

- Basic Accounting T AccountsDocument1 pageBasic Accounting T Accountsbae joohyunNo ratings yet

- Questionnaire For Microfinance Institution-Risk Management and Internal Control System (Recovered)Document113 pagesQuestionnaire For Microfinance Institution-Risk Management and Internal Control System (Recovered)Shilpi KumariNo ratings yet

- 12 Acc. QB Ch. 2Document27 pages12 Acc. QB Ch. 2Himanshu K. SinghNo ratings yet

- Accounting Entries of Procurement Process SAPDocument4 pagesAccounting Entries of Procurement Process SAPhardik kachhadiyaNo ratings yet

Download as pdf or txt

You might also like

- MMZ Accountancy School PH 09 453197062: 15 Mark Questions: Preparing Simple Consolidated Financial StatementsDocument7 pagesMMZ Accountancy School PH 09 453197062: 15 Mark Questions: Preparing Simple Consolidated Financial StatementsSerena100% (1)

- Segregation of Duties MatrixDocument13 pagesSegregation of Duties MatrixForumnoj100% (1)

- Contoh Soal Pelaporan KorporatDocument4 pagesContoh Soal Pelaporan Korporatirma cahyani kawi0% (1)

- CR Inter QuestionsDocument22 pagesCR Inter QuestionsRichie BoomaNo ratings yet

- Question 5: Ias 7 Statements of Cash FlowsDocument4 pagesQuestion 5: Ias 7 Statements of Cash FlowsShiza ArifNo ratings yet

- Statement of Cash Flow - Thorstved CoDocument5 pagesStatement of Cash Flow - Thorstved Cotun ibrahimNo ratings yet

- Income Statements For The November: @Chapter7AnalyslngandlnterpretlngflnanclalstatementsDocument1 pageIncome Statements For The November: @Chapter7AnalyslngandlnterpretlngflnanclalstatementsAik Luen LimNo ratings yet

- Thegodfather CF Student CdADocument8 pagesThegodfather CF Student CdAPablo MichavilaNo ratings yet

- SCF With DODocument3 pagesSCF With DOMuhammad Asif KhanNo ratings yet

- 2021 Seminar Paper Marking SchemeDocument12 pages2021 Seminar Paper Marking Schemesayuru423geenethNo ratings yet

- Statement of Financial Position As at 31st March 2015Document52 pagesStatement of Financial Position As at 31st March 2015Shameel IrshadNo ratings yet

- CORPORATE REPORTING Icag PDFDocument31 pagesCORPORATE REPORTING Icag PDFmohedNo ratings yet

- Notes Before UTSDocument20 pagesNotes Before UTSdevina utamiNo ratings yet

- Cash Flows Tutorial QuestionsDocument6 pagesCash Flows Tutorial Questionssmlingwa100% (1)

- Test 1Document3 pagesTest 1tshepomoejanejrNo ratings yet

- ACCT 4200 Project Solution - Final Posting 2022Document14 pagesACCT 4200 Project Solution - Final Posting 2022Jaspal SinghNo ratings yet

- Mock Exam FRPM SolutionDocument45 pagesMock Exam FRPM SolutionangelitayosecasetiawanNo ratings yet

- Anandam Case AnalysisDocument5 pagesAnandam Case AnalysisVini ShethNo ratings yet

- 91406-res-2021Document4 pages91406-res-2021grace.padfield2006No ratings yet

- ACCT 4200 Project Solution - Final Posting 2022Document15 pagesACCT 4200 Project Solution - Final Posting 2022Jaspal SinghNo ratings yet

- AccntsDocument10 pagesAccntsLav RamgopalNo ratings yet

- Qantas DataDocument31 pagesQantas DataChip choiNo ratings yet

- Acct 401 Tutorial Set FiveDocument13 pagesAcct 401 Tutorial Set FiveStudy GirlNo ratings yet

- 7001 Assignment #3Document9 pages7001 Assignment #3南玖No ratings yet

- Class Discussion On Ratios 28022023Document2 pagesClass Discussion On Ratios 28022023lil telNo ratings yet

- Class Day Test BSC Finance Year 2Document5 pagesClass Day Test BSC Finance Year 2Revatee HurilNo ratings yet

- Hartalega Holdings Berhad (Malaysia) : Source: - WVB - Financial Standard For Industrial CompaniesDocument6 pagesHartalega Holdings Berhad (Malaysia) : Source: - WVB - Financial Standard For Industrial CompaniesJUWAIRIA BINTI SADIKNo ratings yet

- Osborne Answers - Work Book Year 2Document44 pagesOsborne Answers - Work Book Year 2deshawnosae12No ratings yet

- W2D2C1&2 Interpretation FS ActivitiesDocument13 pagesW2D2C1&2 Interpretation FS ActivitiesMaximillian GleichmannNo ratings yet

- Finacial Accounting Ii FA260US ASSIGNMENT 1 (5 Group Member Only) Faculty Department Course Course Code Due Date Possible Marks Examiner (S) Moderator InstructionsDocument5 pagesFinacial Accounting Ii FA260US ASSIGNMENT 1 (5 Group Member Only) Faculty Department Course Course Code Due Date Possible Marks Examiner (S) Moderator InstructionsJohanna AseliNo ratings yet

- Workshop 5 QsDocument7 pagesWorkshop 5 QsNaresh SehdevNo ratings yet

- Fa 6 Ans Key Q.P Code 75847 PDFDocument16 pagesFa 6 Ans Key Q.P Code 75847 PDFAmar ChapniyaNo ratings yet

- JengaCashFlowExercise 1546983290168Document3 pagesJengaCashFlowExercise 1546983290168rex100% (1)

- ITAE Financial Datasheet Summer 2024 Final (15084)Document4 pagesITAE Financial Datasheet Summer 2024 Final (15084)sahil95867No ratings yet

- Ratio AnalysisDocument17 pagesRatio Analysisdora76pataNo ratings yet

- Jenga Cashflow ExerciseDocument2 pagesJenga Cashflow ExerciseHue PhamNo ratings yet

- CILO 4 - Prepare The Financial Statements.: Profit or Loss)Document5 pagesCILO 4 - Prepare The Financial Statements.: Profit or Loss)Neama1 RadhiNo ratings yet

- E TranspharmaDocument7 pagesE TranspharmaLucas Moraes Teixeira SalgadoNo ratings yet

- Corporate Financial Reporting PDFDocument3 pagesCorporate Financial Reporting PDFIshan SharmaNo ratings yet

- C 20: C C F: Hapter Onsolidation ASH LowsDocument1 pageC 20: C C F: Hapter Onsolidation ASH Lows.No ratings yet

- Financial Statement ACIFL 31 March 2015 ConsolidatedDocument16 pagesFinancial Statement ACIFL 31 March 2015 ConsolidatedNurhan JaigirdarNo ratings yet

- Assignment 7 SolutionsDocument10 pagesAssignment 7 SolutionsjoanNo ratings yet

- Statement of Cash FlowsDocument12 pagesStatement of Cash FlowsDaniel PeterNo ratings yet

- Rivera and Santos PartnershipDocument31 pagesRivera and Santos PartnershipDaneca GallardoNo ratings yet

- Хариу HW2 ACC732Document6 pagesХариу HW2 ACC732ZayaNo ratings yet

- AMARILODocument8 pagesAMARILOIngrid Molina GarciaNo ratings yet

- Lecture 1 & 2 ExamplesDocument5 pagesLecture 1 & 2 ExamplesAbubakari Abdul MananNo ratings yet

- Cash Flow (Exercise)Document5 pagesCash Flow (Exercise)abhishekvora7598752100% (1)

- Mo Hinh Ky Thuat Phan Tich Tai ChinhDocument39 pagesMo Hinh Ky Thuat Phan Tich Tai ChinhĐào Mạnh Quân Pete'rNo ratings yet

- Act 3602. Chapter 3. Prob.3-39 HomeworkDocument3 pagesAct 3602. Chapter 3. Prob.3-39 HomeworkphanupongnineNo ratings yet

- Ratio AnlysDocument5 pagesRatio AnlysVi PhuongNo ratings yet

- JengaCashFlowExercise 1546983290168Document2 pagesJengaCashFlowExercise 1546983290168Vibhuti BatraNo ratings yet

- Chapter 7 Up StreamDocument14 pagesChapter 7 Up StreamAditya Agung SatrioNo ratings yet

- FAWCM - Cash Flow 2Document29 pagesFAWCM - Cash Flow 2Jake RoosenbloomNo ratings yet

- Accounting IAS (Malaysia) Model Answers Series 2 2007 Old SyllabusDocument18 pagesAccounting IAS (Malaysia) Model Answers Series 2 2007 Old SyllabusAung Zaw HtweNo ratings yet

- Evaluating Financial PerformanceDocument31 pagesEvaluating Financial PerformanceShahruk AnwarNo ratings yet

- MR D.I.Y. Group (M) Berhad: Interim Financial Report For The Third Quarter Ended 30 September 2020Document15 pagesMR D.I.Y. Group (M) Berhad: Interim Financial Report For The Third Quarter Ended 30 September 2020Mzm Zahir MzmNo ratings yet

- FRS 107 Ie 2016BBDocument10 pagesFRS 107 Ie 2016BBAmelia RahmawatiNo ratings yet

- Tutorial 8Document6 pagesTutorial 8WEI QUAN LEENo ratings yet

- OLC Chap 5Document6 pagesOLC Chap 5Isha SinghNo ratings yet

- Equity Valuation: Models from Leading Investment BanksFrom EverandEquity Valuation: Models from Leading Investment BanksJan ViebigNo ratings yet

- XdfdhfheDocument2 pagesXdfdhfheKrishna 11No ratings yet

- ZOHO TrainingDocument4 pagesZOHO TrainingKrishna 11No ratings yet

- If Mr. Paul Resided in The UK For ADocument1 pageIf Mr. Paul Resided in The UK For AKrishna 11No ratings yet

- General LedgerDocument3 pagesGeneral LedgerKrishna 11No ratings yet

- Abc FR129Document3 pagesAbc FR129Krishna 11No ratings yet

- Abc FR264Document1 pageAbc FR264Krishna 11No ratings yet

- Analysing Institutional and Government Support ForDocument3 pagesAnalysing Institutional and Government Support ForKrishna 11No ratings yet

- ACA 2022 Syllabus Handbook Advanced Corporate ReportingDocument35 pagesACA 2022 Syllabus Handbook Advanced Corporate ReportingNishhhhiiiNo ratings yet

- Prakash Jhunjhunwala & Co LLP: Chartered AccountantsDocument9 pagesPrakash Jhunjhunwala & Co LLP: Chartered AccountantsKinshuk SinghNo ratings yet

- Citi Bank Statement Feb 2022Document6 pagesCiti Bank Statement Feb 2022Akshay SinghNo ratings yet

- EB - Romney - AIS13wm 405 440 16 20Document5 pagesEB - Romney - AIS13wm 405 440 16 20Mayang SariNo ratings yet

- AIS ch09Document151 pagesAIS ch09Syarief HuseinNo ratings yet

- Dokumen - Tips 6018 p3 SPK Lembar Kerja Menyelesaikan Siklus AkuntansiDocument22 pagesDokumen - Tips 6018 p3 SPK Lembar Kerja Menyelesaikan Siklus AkuntansiM IkhsanNo ratings yet

- Financial ManagementDocument88 pagesFinancial ManagementSomevi Bright KodjoNo ratings yet

- Break-Even Point and Cost-Volume-Profit AnalysisDocument44 pagesBreak-Even Point and Cost-Volume-Profit AnalysisKhánh Đoan NgôNo ratings yet

- Business CombinationDocument7 pagesBusiness CombinationJae DenNo ratings yet

- Material Cost 01 - Class Notes - Udesh Regular - Group 1Document8 pagesMaterial Cost 01 - Class Notes - Udesh Regular - Group 1Shubham KumarNo ratings yet

- Pre - Board Examination - Accountancy - Class XII - (2022-23)Document12 pagesPre - Board Examination - Accountancy - Class XII - (2022-23)Shipra GumberNo ratings yet

- Occupied 500: Area FT.) Light PointsDocument10 pagesOccupied 500: Area FT.) Light PointsAbhijit HoroNo ratings yet

- Financial Accounting Objectives Sem V PDFDocument14 pagesFinancial Accounting Objectives Sem V PDFAyman MalikNo ratings yet

- Limitations of Conceptual Framework PDFDocument20 pagesLimitations of Conceptual Framework PDFGeorge Buliki100% (25)

- Ross Fundamentals of Corporate Finance 13e CH10 PPT AccessibleDocument38 pagesRoss Fundamentals of Corporate Finance 13e CH10 PPT AccessibleAdriana RisiNo ratings yet

- Siklus CahayaDocument27 pagesSiklus CahayaBangYonnNo ratings yet

- Midterm - Chapter 4Document78 pagesMidterm - Chapter 4JoshrylNo ratings yet

- Daftar PustakaDocument5 pagesDaftar PustakaWinda AyuNo ratings yet

- Course OutlineDocument4 pagesCourse Outlinetacamp daNo ratings yet

- Understanding Financial StatementDocument14 pagesUnderstanding Financial StatementNHELBY VERAFLORNo ratings yet

- 3512 Chapter 23 Cash Flows HW Exercises ProblemsDocument12 pages3512 Chapter 23 Cash Flows HW Exercises ProblemsM MustafaNo ratings yet

- Answer-Key Acco-201 Intacc2 Mte 1say2324Document8 pagesAnswer-Key Acco-201 Intacc2 Mte 1say2324John cookNo ratings yet

- Financial Accounting Class 11 NotesDocument7 pagesFinancial Accounting Class 11 NotesAnkush ThakurNo ratings yet

- Chapter 26 Marginal Costing and Cost Volume Profit AnalysisDocument25 pagesChapter 26 Marginal Costing and Cost Volume Profit Analysisorkuting84% (73)

- Solution Manual For Accounting Information Systems 3rd Edition Vernon Richardson Chengyee Chang Rod SmithDocument13 pagesSolution Manual For Accounting Information Systems 3rd Edition Vernon Richardson Chengyee Chang Rod SmithJessica Wyke100% (38)

- Basic Accounting T AccountsDocument1 pageBasic Accounting T Accountsbae joohyunNo ratings yet

- Questionnaire For Microfinance Institution-Risk Management and Internal Control System (Recovered)Document113 pagesQuestionnaire For Microfinance Institution-Risk Management and Internal Control System (Recovered)Shilpi KumariNo ratings yet

- 12 Acc. QB Ch. 2Document27 pages12 Acc. QB Ch. 2Himanshu K. SinghNo ratings yet

- Accounting Entries of Procurement Process SAPDocument4 pagesAccounting Entries of Procurement Process SAPhardik kachhadiyaNo ratings yet