Download as pdf or txt

You might also like

- Assessment Tool: Assessment Task 1: Knowledge QuestionsDocument59 pagesAssessment Tool: Assessment Task 1: Knowledge QuestionsTaniya100% (1)

- Consummation Order and Final Decree Penn Central BankruptcyDocument52 pagesConsummation Order and Final Decree Penn Central BankruptcyJanetLindenmuthNo ratings yet

- Final and Capital Gains TaxDocument7 pagesFinal and Capital Gains TaxElla Marie LopezNo ratings yet

- IndAS8 Accounting Policies, Changes in Accounting Estimates and ErrorsDocument19 pagesIndAS8 Accounting Policies, Changes in Accounting Estimates and Errorsajayaju005No ratings yet

- Accounting Policies, Changes in Accounting Estimates and ErrorsDocument25 pagesAccounting Policies, Changes in Accounting Estimates and ErrorsAshish agrawalNo ratings yet

- Exp Posure D Draft: A Accounti Ing Stan Ndard (A AS) 5 (Re Evised)Document15 pagesExp Posure D Draft: A Accounti Ing Stan Ndard (A AS) 5 (Re Evised)ratiNo ratings yet

- Accounting Policies, Changes in Accounting Estimates and ErrorsDocument14 pagesAccounting Policies, Changes in Accounting Estimates and ErrorsSuresh Reddy SannapureddyNo ratings yet

- Accounting Policies, Changes in Accounting Estimates and ErrorsDocument15 pagesAccounting Policies, Changes in Accounting Estimates and ErrorsPriya JandialNo ratings yet

- Accounting Policies, Changes in Accounting Estimates and ErrorsDocument9 pagesAccounting Policies, Changes in Accounting Estimates and ErrorsMaruf HossainNo ratings yet

- 8 Policy, Estimate, ErrorDocument16 pages8 Policy, Estimate, ErrorChelsea Anne VidalloNo ratings yet

- Ias 8 EnglezaDocument9 pagesIas 8 EnglezaTatiana LupuNo ratings yet

- 21.0 NAS 8 - SetPasswordDocument9 pages21.0 NAS 8 - SetPasswordDhruba AdhikariNo ratings yet

- Accounting Policies, Changes in Accounting Estimates and ErrorsDocument18 pagesAccounting Policies, Changes in Accounting Estimates and ErrorscindhyNo ratings yet

- Indian Accounting Standard (Ind AS) 8 - Taxguru - inDocument11 pagesIndian Accounting Standard (Ind AS) 8 - Taxguru - inaaosarlbNo ratings yet

- Accounting Policies, Changes in Accounting Estimates and ErrorsDocument20 pagesAccounting Policies, Changes in Accounting Estimates and ErrorsMa Precylla Cerraine FloresNo ratings yet

- Lkas 8 Accounting Policies Changes in Accounting Estimates and ErrorsDocument18 pagesLkas 8 Accounting Policies Changes in Accounting Estimates and ErrorsW V C JAYAMININo ratings yet

- Indian Accounting Standard (Ind AS) 8: Accounting Policies, Changes in Accounting Estimates and ErrorsDocument19 pagesIndian Accounting Standard (Ind AS) 8: Accounting Policies, Changes in Accounting Estimates and ErrorsAnkush GoelNo ratings yet

- IPAS 8 - Accounting Policies Changes in Accounting Estimates and ErrorsDocument22 pagesIPAS 8 - Accounting Policies Changes in Accounting Estimates and ErrorsJhea LirasanNo ratings yet

- Nepal Accounting Standards On Accounting Policies, Changes in Accounting Estimates & ErrorsDocument25 pagesNepal Accounting Standards On Accounting Policies, Changes in Accounting Estimates & Errorsshama_rana20036778No ratings yet

- Review Materials: Prepared By: Junior Philippine Institute of Accountants UC-Banilad Chapter F.Y. 2019-2020Document33 pagesReview Materials: Prepared By: Junior Philippine Institute of Accountants UC-Banilad Chapter F.Y. 2019-2020AB CloydNo ratings yet

- Accounting Policies, Changes in Accounting Estimates and ErrorsDocument32 pagesAccounting Policies, Changes in Accounting Estimates and ErrorsAmrita TamangNo ratings yet

- Amendments To PAS 8 - PrefaceDocument13 pagesAmendments To PAS 8 - PrefacejolanreidNo ratings yet

- IND AS 8 Raw PDFDocument41 pagesIND AS 8 Raw PDFrajesh reddyNo ratings yet

- Ind As On Measurement Based On Accounting PoliciesDocument38 pagesInd As On Measurement Based On Accounting Policiespulkitddude_24114888No ratings yet

- Accounting Policies, Changes in Accounting Estimates and ErrorsDocument18 pagesAccounting Policies, Changes in Accounting Estimates and ErrorsSineth NeththasingheNo ratings yet

- Module 014 Week005-Statement of Changes in Equity, Accounting Policies, Changes in Accounting Estimates and ErrorsDocument9 pagesModule 014 Week005-Statement of Changes in Equity, Accounting Policies, Changes in Accounting Estimates and Errorsman ibeNo ratings yet

- 74888bos60524 cp4 U1Document50 pages74888bos60524 cp4 U1Bala Guru Prasad TadikamallaNo ratings yet

- Accounting Policies, Changes in Accounting Estimates and ErrorsDocument67 pagesAccounting Policies, Changes in Accounting Estimates and ErrorsDafrosa HonorNo ratings yet

- Ias 8 Accounting Policies Changes in Accounting Estimates and Errors SummaryDocument5 pagesIas 8 Accounting Policies Changes in Accounting Estimates and Errors SummaryWilmar AbriolNo ratings yet

- Accounting Policies Changes in Accounting Estimates and Errors - IAS 8Document6 pagesAccounting Policies Changes in Accounting Estimates and Errors - IAS 8Anonymous P1xUTHstHTNo ratings yet

- Indian Accounting Standard 108Document2 pagesIndian Accounting Standard 108ca.sanket1No ratings yet

- PAS 8 - Accounting Policies, Changes in Accounting Estimates and ErrorsDocument11 pagesPAS 8 - Accounting Policies, Changes in Accounting Estimates and ErrorsKrizzia DizonNo ratings yet

- As 8 Alc PoliciesDocument50 pagesAs 8 Alc PoliciesAkhil AkhyNo ratings yet

- 11 Ias 8Document5 pages11 Ias 8Irtiza AbbasNo ratings yet

- FRS108Document8 pagesFRS108Aritz EpitNo ratings yet

- Ias 8 Accounting Policies, Changes in Accounting Estimates and ErrorsDocument7 pagesIas 8 Accounting Policies, Changes in Accounting Estimates and Errorsmusic niNo ratings yet

- Accounting For Changes and ErrorsDocument7 pagesAccounting For Changes and ErrorsMeludyNo ratings yet

- Nepal Accounting Standard 8: Accounting Policies, Changes in Accounting Estimates and ErrorsDocument13 pagesNepal Accounting Standard 8: Accounting Policies, Changes in Accounting Estimates and ErrorsRochak ShresthaNo ratings yet

- LKAS 8 Accounting Policies (New)Document33 pagesLKAS 8 Accounting Policies (New)Kogularamanan NithiananthanNo ratings yet

- Change in Accounting Policy, Estimates and Error PAS 8Document17 pagesChange in Accounting Policy, Estimates and Error PAS 8RNo ratings yet

- IAS 8 - Accounting Policies, Changes in Accounting Estimates and ErrorsDocument48 pagesIAS 8 - Accounting Policies, Changes in Accounting Estimates and ErrorsNitroNo ratings yet

- As 01Document9 pagesAs 01Dipak UgaleNo ratings yet

- Ias 8Document9 pagesIas 8Muhammad SaeedNo ratings yet

- Ias No.8Document41 pagesIas No.8rafikaNo ratings yet

- Disclosure of Accounting PoliciesDocument7 pagesDisclosure of Accounting PoliciesgimmyjoyNo ratings yet

- Accounting Policies, Changes in Accounting Estimates and ErrorsDocument29 pagesAccounting Policies, Changes in Accounting Estimates and ErrorsSheda AshrafNo ratings yet

- IAS8-Summary Notes PDFDocument8 pagesIAS8-Summary Notes PDFWaqas Younas BandukdaNo ratings yet

- Disclosure of Accounting PoliciesDocument8 pagesDisclosure of Accounting Policiesabdullah0331No ratings yet

- Differences in Ind As and Existing AsDocument32 pagesDifferences in Ind As and Existing AsSanket DandawateNo ratings yet

- Ias 8 Accounting Policies, Changes in Accounting Estimates and ErrorsDocument27 pagesIas 8 Accounting Policies, Changes in Accounting Estimates and ErrorsMK RKNo ratings yet

- Document 2Document8 pagesDocument 2sohamNo ratings yet

- Accounting Policies, Changes in Accounting Estimates and ErrorsDocument37 pagesAccounting Policies, Changes in Accounting Estimates and ErrorsSun DaygyNo ratings yet

- NAS 8 - Best SummaryDocument5 pagesNAS 8 - Best Summarysitoulamanish100No ratings yet

- Accounting Policies, Changes in Accounting Estimates and ErrorsDocument6 pagesAccounting Policies, Changes in Accounting Estimates and ErrorsGlen JavellanaNo ratings yet

- As-1 Disclosure of Accounting PoliciesDocument7 pagesAs-1 Disclosure of Accounting PoliciesPrakash_Tandon_583No ratings yet

- Ias 8 Accounting Policies, Changes in Accounting Estimates and ErrorsDocument10 pagesIas 8 Accounting Policies, Changes in Accounting Estimates and ErrorsBagudu Bilal GamboNo ratings yet

- Accounting Policies, Changes in Accounting Estimates and ErrorsDocument19 pagesAccounting Policies, Changes in Accounting Estimates and ErrorsNimona BeyeneNo ratings yet

- Ias8 PDFDocument3 pagesIas8 PDFNozipho MpofuNo ratings yet

- University of Perpetual Help System Dalta: Calamba Campus, Brgy. Paciano RizalDocument3 pagesUniversity of Perpetual Help System Dalta: Calamba Campus, Brgy. Paciano RizalJeanette LampitocNo ratings yet

- Annual Update and Practice Issues for Preparation, Compilation, and Review EngagementsFrom EverandAnnual Update and Practice Issues for Preparation, Compilation, and Review EngagementsNo ratings yet

- Engagement Essentials: Preparation, Compilation, and Review of Financial StatementsFrom EverandEngagement Essentials: Preparation, Compilation, and Review of Financial StatementsNo ratings yet

- Audit Risk Alert: General Accounting and Auditing Developments, 2017/18From EverandAudit Risk Alert: General Accounting and Auditing Developments, 2017/18No ratings yet

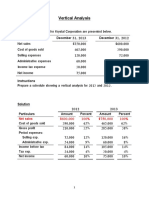

- Vertical Analysis SolutionsDocument5 pagesVertical Analysis SolutionsSamer IsmaelNo ratings yet

- Chapter - 1 Inventories Definition: - Inventory Is Used To DesignateDocument14 pagesChapter - 1 Inventories Definition: - Inventory Is Used To DesignateMulugeta TsegaNo ratings yet

- Use Market Risk Premium For Expected Market ReturnDocument5 pagesUse Market Risk Premium For Expected Market Returnselozok1No ratings yet

- FM 6 Financial Statements Analysis MBADocument50 pagesFM 6 Financial Statements Analysis MBAMisganaw GishenNo ratings yet

- Consolidated Statement of Profit and LossDocument9 pagesConsolidated Statement of Profit and LossHrushikesh DahaleNo ratings yet

- PolicyDocument AspxDocument2 pagesPolicyDocument AspxdNo ratings yet

- Mission of Pubali Bank LTDDocument8 pagesMission of Pubali Bank LTDTalha_Adil_3097No ratings yet

- V12-021 Flash Boys PollDocument10 pagesV12-021 Flash Boys PolltabbforumNo ratings yet

- Financial Statment Analysis of Hero MotocorpDocument66 pagesFinancial Statment Analysis of Hero MotocorpWebsoft Tech-HydNo ratings yet

- TPH Day4Document100 pagesTPH Day4adyani_0997100% (1)

- Quiz 4 Practice ProblemsDocument9 pagesQuiz 4 Practice ProblemsMena WalidNo ratings yet

- Ce 351 A2Document12 pagesCe 351 A2IsraelNo ratings yet

- QuestionsDocument2 pagesQuestionsTeh Chu LeongNo ratings yet

- Stolyarov MFE Study GuideDocument279 pagesStolyarov MFE Study GuideChamu ChiwaraNo ratings yet

- E Receipt For State Bank Collect Payment: 13731 Suryansh .Tiwari Ug GN Mme Btech Hall3 156 Suryansh@Iitk - Ac.In 55890 0Document1 pageE Receipt For State Bank Collect Payment: 13731 Suryansh .Tiwari Ug GN Mme Btech Hall3 156 Suryansh@Iitk - Ac.In 55890 0Abhishek KulkarniNo ratings yet

- June 2021Document21 pagesJune 2021Anjana TimalsinaNo ratings yet

- LAWDocument4 pagesLAWCatherine SelladoNo ratings yet

- Mehran Sugar Mills - Six Years Financial Review at A GlanceDocument3 pagesMehran Sugar Mills - Six Years Financial Review at A GlanceUmair ChandaNo ratings yet

- FA2Document3 pagesFA2lulughoshNo ratings yet

- MBBcurrent 511074534516 2019-07-31Document9 pagesMBBcurrent 511074534516 2019-07-31Jannah TajudinNo ratings yet

- Manvi PuriDocument2 pagesManvi PuriGaurav GaggarNo ratings yet

- Kelas A PA1 Matcha Hal 93 Dan 154Document7 pagesKelas A PA1 Matcha Hal 93 Dan 154Kinka NurrindraNo ratings yet

- Job Location: Pokhara No. of Vacancies: 1: 1. AccountantDocument1 pageJob Location: Pokhara No. of Vacancies: 1: 1. AccountantShubhekchha Neupane PandayNo ratings yet

- 18TH Pre Agm 2024Document63 pages18TH Pre Agm 2024pkibet872No ratings yet

- 39759Document3 pages39759MonikaNo ratings yet

- Mathiba Evaluation 2011 PDFDocument112 pagesMathiba Evaluation 2011 PDFDicky NovendraNo ratings yet

- CorporateDocument28 pagesCorporateRalkan KantonNo ratings yet