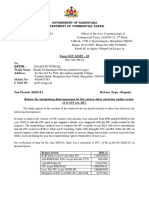

ASSESSMENT_-_IT_ACT[1]

ASSESSMENT_-_IT_ACT[1]

You might also like

- DellDocument1 pageDellNaresh Kumar Yadav (nari)No ratings yet

- Broward County Clerk's Daughter Arrest in RICO CaseDocument46 pagesBroward County Clerk's Daughter Arrest in RICO CaseAndreaTorres100% (1)

- ABAKADA GURO PARTY LIST V ERMITA DigestDocument4 pagesABAKADA GURO PARTY LIST V ERMITA DigestAndrea Tiu100% (3)

- Assesment of Undisclosed Income: SUBMITTED BY - Anshu Kumar ROLL NO-18MB01 MBA2018-2020Document15 pagesAssesment of Undisclosed Income: SUBMITTED BY - Anshu Kumar ROLL NO-18MB01 MBA2018-2020Dhruv BrahmbhattNo ratings yet

- Assessment Procedure PDFDocument9 pagesAssessment Procedure PDFMalkeet SinghNo ratings yet

- AssessmentDocument7 pagesAssessmentGopiNo ratings yet

- Search and SeizureDocument26 pagesSearch and SeizureShivansh JaiswalNo ratings yet

- Types of Assessments Under Income TaxDocument12 pagesTypes of Assessments Under Income TaxSuyash PrakashNo ratings yet

- Types of Assesment Under Income Tax ActDocument11 pagesTypes of Assesment Under Income Tax Actabhi malik100% (1)

- Kinds of AssessmentDocument6 pagesKinds of AssessmentmanikaNo ratings yet

- Module 20 - AssessmentDocument12 pagesModule 20 - AssessmentvaibhavsalgaonkarpcNo ratings yet

- AssessmentDocument8 pagesAssessmentKeerthanaNo ratings yet

- Appeals and Assssments-AssignmentDocument6 pagesAppeals and Assssments-AssignmentArti ModiNo ratings yet

- Bcom-6 Bus. Tax. II Unit 1Document20 pagesBcom-6 Bus. Tax. II Unit 1kdsinh1912No ratings yet

- Assessment Procedure AY 2021-22Document8 pagesAssessment Procedure AY 2021-22anupshetty19No ratings yet

- Assessment ProcedureDocument26 pagesAssessment ProcedureRohit GuptaNo ratings yet

- Assesment Procedure: By: Smriti KhannaDocument25 pagesAssesment Procedure: By: Smriti KhannaSmriti KhannaNo ratings yet

- 33 Various AssessmentsDocument9 pages33 Various AssessmentsVijay Patel InumulaNo ratings yet

- Procedure For Assessment of Income TaxDocument3 pagesProcedure For Assessment of Income Taxdiksha kumariNo ratings yet

- Assessment ProcedureDocument26 pagesAssessment ProcedureRohit Gupta100% (1)

- Procedure For Assessment: Presented By-Rahul Kesarwani III SemesterDocument29 pagesProcedure For Assessment: Presented By-Rahul Kesarwani III Semesterrahulkesarwani01No ratings yet

- 33 Various AssessmentsDocument10 pages33 Various AssessmentsParth UpadhyayNo ratings yet

- Assessment ProcedureDocument14 pagesAssessment ProcedurePragnya mahapatroNo ratings yet

- Self Assessment U/s 140A: CA Abhijit SawarkarDocument5 pagesSelf Assessment U/s 140A: CA Abhijit SawarkarMansi MalikNo ratings yet

- Taxguru - In-Assessments Under Income-Tax Act 1961Document12 pagesTaxguru - In-Assessments Under Income-Tax Act 1961Sudev SinghNo ratings yet

- Various Types of Assessment Under Income Tax Act, 1961Document10 pagesVarious Types of Assessment Under Income Tax Act, 1961165Y020 SATHWICK BUJENDRA GOWDANo ratings yet

- IT12. Assessments and RevisionsDocument12 pagesIT12. Assessments and Revisionsshree varanaNo ratings yet

- Types of AssessmentDocument3 pagesTypes of Assessments.kowshik0018No ratings yet

- Types of Income Tax AssessmentDocument3 pagesTypes of Income Tax AssessmenttayaisgreatNo ratings yet

- Procedure of AssessmentDocument7 pagesProcedure of Assessmentkarthitamil2004No ratings yet

- Assessment Proceedings Under IT Act 1961Document31 pagesAssessment Proceedings Under IT Act 1961amanfreefire555No ratings yet

- Income Tax - MidhunDocument19 pagesIncome Tax - MidhunmidhunNo ratings yet

- Statutory Provisions Part 04Document14 pagesStatutory Provisions Part 04wellawalalasithNo ratings yet

- Tax End Sem RevisionDocument21 pagesTax End Sem Revisionanirudh.vyasNo ratings yet

- Types of AssessmentDocument9 pagesTypes of AssessmentSHANMUGHADAS KGNo ratings yet

- DT Assessment ProceduresDocument6 pagesDT Assessment ProceduresSri PeketiNo ratings yet

- Assessment of Income - Meaning, Scope, Procedure & Time Limit – Section 143 (1) - Taxguru - inDocument3 pagesAssessment of Income - Meaning, Scope, Procedure & Time Limit – Section 143 (1) - Taxguru - inmkadv25No ratings yet

- Direct Tax Final Suggestion: For Offline Admission Call / Whatsapp - +91 70031 65955Document9 pagesDirect Tax Final Suggestion: For Offline Admission Call / Whatsapp - +91 70031 65955AhiaanNo ratings yet

- Assessment: Issues in Assessment & Reassessment Under I. T. ActDocument36 pagesAssessment: Issues in Assessment & Reassessment Under I. T. ActSUNILNo ratings yet

- Unit IVDocument19 pagesUnit IVsatyabratadas688No ratings yet

- Assessment ProceedingsDocument3 pagesAssessment ProceedingsRahulNo ratings yet

- Wtax (A) 721 2015Document13 pagesWtax (A) 721 2015Neena BatlaNo ratings yet

- Assessment: Din IslamDocument18 pagesAssessment: Din IslamH.I. RaheNo ratings yet

- Return of Income: Group 3Document17 pagesReturn of Income: Group 3Khushi SonarNo ratings yet

- Assessment ProcedureDocument15 pagesAssessment ProcedureHassan AliNo ratings yet

- Assessment & AuditDocument17 pagesAssessment & AuditRam SewakNo ratings yet

- Income Tax Assessment TypesDocument2 pagesIncome Tax Assessment TypesJNVU WEBINARNo ratings yet

- Chapter - 1Document16 pagesChapter - 1Vijay KumarNo ratings yet

- What Is Section 145Document5 pagesWhat Is Section 145MOUSOM ROYNo ratings yet

- Advance Ruling Principle Under Income Tax Act 1961Document44 pagesAdvance Ruling Principle Under Income Tax Act 1961Zaheer UsmanNo ratings yet

- Assessment and AuditDocument8 pagesAssessment and AuditAnjali Krishna SNo ratings yet

- Taxation assessmentDocument4 pagesTaxation assessmentNadeem BalochNo ratings yet

- Assessment Under GST ActDocument3 pagesAssessment Under GST ActBargavi NarayananNo ratings yet

- Chapter 13 - Return Filing - NotesDocument6 pagesChapter 13 - Return Filing - NotesAkshay PooniaNo ratings yet

- Assesmenr, Records - AuditDocument102 pagesAssesmenr, Records - Auditdavid.ellis1245No ratings yet

- Responsibilityof Auditors Under Companies Act 2013: Srinivas MethukuDocument31 pagesResponsibilityof Auditors Under Companies Act 2013: Srinivas MethukuSudhakar MadhavediNo ratings yet

- Assessment in Income TaxDocument3 pagesAssessment in Income Taxayush sikkewalNo ratings yet

- Direct Tax Short Notes For CA Final StudentDocument52 pagesDirect Tax Short Notes For CA Final Studentjonnajon920% (1)

- Assessment ProcedureDocument7 pagesAssessment ProcedureVachanamrutha R.VNo ratings yet

- Direct Tax - Unit 4 - Question NotesDocument5 pagesDirect Tax - Unit 4 - Question NotesbhaskarojoNo ratings yet

- Ashish Agarwal Supreme Court AnalysisDocument4 pagesAshish Agarwal Supreme Court AnalysisAdvocateNitinsharmaNo ratings yet

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- T Codes For SAP Sales Register and Excise InvoiceDocument1 pageT Codes For SAP Sales Register and Excise InvoicekssumanthNo ratings yet

- Econ Analysis Report 2016Document340 pagesEcon Analysis Report 2016zinveliu_vasile_florinNo ratings yet

- Tax On Individuals Different Kinds of Taxpayers:: (Part 1 - Applicable From Year 2018 To 2022)Document9 pagesTax On Individuals Different Kinds of Taxpayers:: (Part 1 - Applicable From Year 2018 To 2022)Ellah MaeNo ratings yet

- Tata Consultancy Services LTD: Profit and Loss AccountDocument4 pagesTata Consultancy Services LTD: Profit and Loss AccountHiren SutariyaNo ratings yet

- This Study Resource Was: Tax QuizzerDocument5 pagesThis Study Resource Was: Tax QuizzerGee-Anne GonzalesNo ratings yet

- East Penn Anticipated Budget Revenues 2023-2024Document14 pagesEast Penn Anticipated Budget Revenues 2023-2024Jay BradleyNo ratings yet

- Salary Slip: Gross Pay 25,600 Net Pay 14,710Document3 pagesSalary Slip: Gross Pay 25,600 Net Pay 14,710pratixa ranaNo ratings yet

- Advisor Contest May-18Document8 pagesAdvisor Contest May-18dharam singhNo ratings yet

- The Single Income TaxDocument421 pagesThe Single Income TaxnstenbergNo ratings yet

- 02Document1 page02Rozina TabassumNo ratings yet

- GST Expense Breakup in Tax Audit Report - Taxguru - inDocument3 pagesGST Expense Breakup in Tax Audit Report - Taxguru - inmanoj shahNo ratings yet

- Tax Invoice: Sudarshan Syndicate 4334/20-21 23-Feb-21Document1 pageTax Invoice: Sudarshan Syndicate 4334/20-21 23-Feb-21ziyan skNo ratings yet

- Pay Slip For The Month of July-2023: Bandhan Bank LimitedDocument1 pagePay Slip For The Month of July-2023: Bandhan Bank LimitedBIKRAM KUMAR BEHERA0% (1)

- Tybcom Economics Sem V (Prelims-Heramb)Document2 pagesTybcom Economics Sem V (Prelims-Heramb)A BPNo ratings yet

- Scan Sep 17, 2022Document1 pageScan Sep 17, 2022zunijemNo ratings yet

- PaymentDocument1 pagePaymentM SotanNo ratings yet

- 1112 Dependent Verification Worksheet-1Document2 pages1112 Dependent Verification Worksheet-1Mikey NguyenNo ratings yet

- Swiggy DFDocument2 pagesSwiggy DFhemanth1234No ratings yet

- Business Economics SEM-IV Question Bank Regular Examination PDFDocument13 pagesBusiness Economics SEM-IV Question Bank Regular Examination PDFSudhir NaikNo ratings yet

- Unit-3 Public ExpenditureDocument27 pagesUnit-3 Public ExpendituremelaNo ratings yet

- Assignment 2.1 - Married Individual TaxpayersDocument3 pagesAssignment 2.1 - Married Individual TaxpayersHunternotNo ratings yet

- Payroll Salary SlipDocument4 pagesPayroll Salary SlipDeca ErnandoNo ratings yet

- Reduction in Rate of Tax Deduction at Source (TDS) & Tax Collection at Source (TCS)Document6 pagesReduction in Rate of Tax Deduction at Source (TDS) & Tax Collection at Source (TCS)Kranthi Kumar KatamreddyNo ratings yet

- Chapter 1 - Fundamental Principles: TAXATION - The Process by Which The Sovereign, Through Its Law-Making BodyDocument11 pagesChapter 1 - Fundamental Principles: TAXATION - The Process by Which The Sovereign, Through Its Law-Making BodyLiRose SmithNo ratings yet

- HDFC 1Document1 pageHDFC 1Vivekananda PenumarthiNo ratings yet

- Income Tax Scrutiny NormsDocument6 pagesIncome Tax Scrutiny Normsphani raja kumarNo ratings yet

- The Alternatives To Universal Tax Registration in Sri LankaDocument11 pagesThe Alternatives To Universal Tax Registration in Sri Lankamick mooreNo ratings yet

Download as pdf or txt

You might also like

- DellDocument1 pageDellNaresh Kumar Yadav (nari)No ratings yet

- Broward County Clerk's Daughter Arrest in RICO CaseDocument46 pagesBroward County Clerk's Daughter Arrest in RICO CaseAndreaTorres100% (1)

- ABAKADA GURO PARTY LIST V ERMITA DigestDocument4 pagesABAKADA GURO PARTY LIST V ERMITA DigestAndrea Tiu100% (3)

- Assesment of Undisclosed Income: SUBMITTED BY - Anshu Kumar ROLL NO-18MB01 MBA2018-2020Document15 pagesAssesment of Undisclosed Income: SUBMITTED BY - Anshu Kumar ROLL NO-18MB01 MBA2018-2020Dhruv BrahmbhattNo ratings yet

- Assessment Procedure PDFDocument9 pagesAssessment Procedure PDFMalkeet SinghNo ratings yet

- AssessmentDocument7 pagesAssessmentGopiNo ratings yet

- Search and SeizureDocument26 pagesSearch and SeizureShivansh JaiswalNo ratings yet

- Types of Assessments Under Income TaxDocument12 pagesTypes of Assessments Under Income TaxSuyash PrakashNo ratings yet

- Types of Assesment Under Income Tax ActDocument11 pagesTypes of Assesment Under Income Tax Actabhi malik100% (1)

- Kinds of AssessmentDocument6 pagesKinds of AssessmentmanikaNo ratings yet

- Module 20 - AssessmentDocument12 pagesModule 20 - AssessmentvaibhavsalgaonkarpcNo ratings yet

- AssessmentDocument8 pagesAssessmentKeerthanaNo ratings yet

- Appeals and Assssments-AssignmentDocument6 pagesAppeals and Assssments-AssignmentArti ModiNo ratings yet

- Bcom-6 Bus. Tax. II Unit 1Document20 pagesBcom-6 Bus. Tax. II Unit 1kdsinh1912No ratings yet

- Assessment Procedure AY 2021-22Document8 pagesAssessment Procedure AY 2021-22anupshetty19No ratings yet

- Assessment ProcedureDocument26 pagesAssessment ProcedureRohit GuptaNo ratings yet

- Assesment Procedure: By: Smriti KhannaDocument25 pagesAssesment Procedure: By: Smriti KhannaSmriti KhannaNo ratings yet

- 33 Various AssessmentsDocument9 pages33 Various AssessmentsVijay Patel InumulaNo ratings yet

- Procedure For Assessment of Income TaxDocument3 pagesProcedure For Assessment of Income Taxdiksha kumariNo ratings yet

- Assessment ProcedureDocument26 pagesAssessment ProcedureRohit Gupta100% (1)

- Procedure For Assessment: Presented By-Rahul Kesarwani III SemesterDocument29 pagesProcedure For Assessment: Presented By-Rahul Kesarwani III Semesterrahulkesarwani01No ratings yet

- 33 Various AssessmentsDocument10 pages33 Various AssessmentsParth UpadhyayNo ratings yet

- Assessment ProcedureDocument14 pagesAssessment ProcedurePragnya mahapatroNo ratings yet

- Self Assessment U/s 140A: CA Abhijit SawarkarDocument5 pagesSelf Assessment U/s 140A: CA Abhijit SawarkarMansi MalikNo ratings yet

- Taxguru - In-Assessments Under Income-Tax Act 1961Document12 pagesTaxguru - In-Assessments Under Income-Tax Act 1961Sudev SinghNo ratings yet

- Various Types of Assessment Under Income Tax Act, 1961Document10 pagesVarious Types of Assessment Under Income Tax Act, 1961165Y020 SATHWICK BUJENDRA GOWDANo ratings yet

- IT12. Assessments and RevisionsDocument12 pagesIT12. Assessments and Revisionsshree varanaNo ratings yet

- Types of AssessmentDocument3 pagesTypes of Assessments.kowshik0018No ratings yet

- Types of Income Tax AssessmentDocument3 pagesTypes of Income Tax AssessmenttayaisgreatNo ratings yet

- Procedure of AssessmentDocument7 pagesProcedure of Assessmentkarthitamil2004No ratings yet

- Assessment Proceedings Under IT Act 1961Document31 pagesAssessment Proceedings Under IT Act 1961amanfreefire555No ratings yet

- Income Tax - MidhunDocument19 pagesIncome Tax - MidhunmidhunNo ratings yet

- Statutory Provisions Part 04Document14 pagesStatutory Provisions Part 04wellawalalasithNo ratings yet

- Tax End Sem RevisionDocument21 pagesTax End Sem Revisionanirudh.vyasNo ratings yet

- Types of AssessmentDocument9 pagesTypes of AssessmentSHANMUGHADAS KGNo ratings yet

- DT Assessment ProceduresDocument6 pagesDT Assessment ProceduresSri PeketiNo ratings yet

- Assessment of Income - Meaning, Scope, Procedure & Time Limit – Section 143 (1) - Taxguru - inDocument3 pagesAssessment of Income - Meaning, Scope, Procedure & Time Limit – Section 143 (1) - Taxguru - inmkadv25No ratings yet

- Direct Tax Final Suggestion: For Offline Admission Call / Whatsapp - +91 70031 65955Document9 pagesDirect Tax Final Suggestion: For Offline Admission Call / Whatsapp - +91 70031 65955AhiaanNo ratings yet

- Assessment: Issues in Assessment & Reassessment Under I. T. ActDocument36 pagesAssessment: Issues in Assessment & Reassessment Under I. T. ActSUNILNo ratings yet

- Unit IVDocument19 pagesUnit IVsatyabratadas688No ratings yet

- Assessment ProceedingsDocument3 pagesAssessment ProceedingsRahulNo ratings yet

- Wtax (A) 721 2015Document13 pagesWtax (A) 721 2015Neena BatlaNo ratings yet

- Assessment: Din IslamDocument18 pagesAssessment: Din IslamH.I. RaheNo ratings yet

- Return of Income: Group 3Document17 pagesReturn of Income: Group 3Khushi SonarNo ratings yet

- Assessment ProcedureDocument15 pagesAssessment ProcedureHassan AliNo ratings yet

- Assessment & AuditDocument17 pagesAssessment & AuditRam SewakNo ratings yet

- Income Tax Assessment TypesDocument2 pagesIncome Tax Assessment TypesJNVU WEBINARNo ratings yet

- Chapter - 1Document16 pagesChapter - 1Vijay KumarNo ratings yet

- What Is Section 145Document5 pagesWhat Is Section 145MOUSOM ROYNo ratings yet

- Advance Ruling Principle Under Income Tax Act 1961Document44 pagesAdvance Ruling Principle Under Income Tax Act 1961Zaheer UsmanNo ratings yet

- Assessment and AuditDocument8 pagesAssessment and AuditAnjali Krishna SNo ratings yet

- Taxation assessmentDocument4 pagesTaxation assessmentNadeem BalochNo ratings yet

- Assessment Under GST ActDocument3 pagesAssessment Under GST ActBargavi NarayananNo ratings yet

- Chapter 13 - Return Filing - NotesDocument6 pagesChapter 13 - Return Filing - NotesAkshay PooniaNo ratings yet

- Assesmenr, Records - AuditDocument102 pagesAssesmenr, Records - Auditdavid.ellis1245No ratings yet

- Responsibilityof Auditors Under Companies Act 2013: Srinivas MethukuDocument31 pagesResponsibilityof Auditors Under Companies Act 2013: Srinivas MethukuSudhakar MadhavediNo ratings yet

- Assessment in Income TaxDocument3 pagesAssessment in Income Taxayush sikkewalNo ratings yet

- Direct Tax Short Notes For CA Final StudentDocument52 pagesDirect Tax Short Notes For CA Final Studentjonnajon920% (1)

- Assessment ProcedureDocument7 pagesAssessment ProcedureVachanamrutha R.VNo ratings yet

- Direct Tax - Unit 4 - Question NotesDocument5 pagesDirect Tax - Unit 4 - Question NotesbhaskarojoNo ratings yet

- Ashish Agarwal Supreme Court AnalysisDocument4 pagesAshish Agarwal Supreme Court AnalysisAdvocateNitinsharmaNo ratings yet

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- T Codes For SAP Sales Register and Excise InvoiceDocument1 pageT Codes For SAP Sales Register and Excise InvoicekssumanthNo ratings yet

- Econ Analysis Report 2016Document340 pagesEcon Analysis Report 2016zinveliu_vasile_florinNo ratings yet

- Tax On Individuals Different Kinds of Taxpayers:: (Part 1 - Applicable From Year 2018 To 2022)Document9 pagesTax On Individuals Different Kinds of Taxpayers:: (Part 1 - Applicable From Year 2018 To 2022)Ellah MaeNo ratings yet

- Tata Consultancy Services LTD: Profit and Loss AccountDocument4 pagesTata Consultancy Services LTD: Profit and Loss AccountHiren SutariyaNo ratings yet

- This Study Resource Was: Tax QuizzerDocument5 pagesThis Study Resource Was: Tax QuizzerGee-Anne GonzalesNo ratings yet

- East Penn Anticipated Budget Revenues 2023-2024Document14 pagesEast Penn Anticipated Budget Revenues 2023-2024Jay BradleyNo ratings yet

- Salary Slip: Gross Pay 25,600 Net Pay 14,710Document3 pagesSalary Slip: Gross Pay 25,600 Net Pay 14,710pratixa ranaNo ratings yet

- Advisor Contest May-18Document8 pagesAdvisor Contest May-18dharam singhNo ratings yet

- The Single Income TaxDocument421 pagesThe Single Income TaxnstenbergNo ratings yet

- 02Document1 page02Rozina TabassumNo ratings yet

- GST Expense Breakup in Tax Audit Report - Taxguru - inDocument3 pagesGST Expense Breakup in Tax Audit Report - Taxguru - inmanoj shahNo ratings yet

- Tax Invoice: Sudarshan Syndicate 4334/20-21 23-Feb-21Document1 pageTax Invoice: Sudarshan Syndicate 4334/20-21 23-Feb-21ziyan skNo ratings yet

- Pay Slip For The Month of July-2023: Bandhan Bank LimitedDocument1 pagePay Slip For The Month of July-2023: Bandhan Bank LimitedBIKRAM KUMAR BEHERA0% (1)

- Tybcom Economics Sem V (Prelims-Heramb)Document2 pagesTybcom Economics Sem V (Prelims-Heramb)A BPNo ratings yet

- Scan Sep 17, 2022Document1 pageScan Sep 17, 2022zunijemNo ratings yet

- PaymentDocument1 pagePaymentM SotanNo ratings yet

- 1112 Dependent Verification Worksheet-1Document2 pages1112 Dependent Verification Worksheet-1Mikey NguyenNo ratings yet

- Swiggy DFDocument2 pagesSwiggy DFhemanth1234No ratings yet

- Business Economics SEM-IV Question Bank Regular Examination PDFDocument13 pagesBusiness Economics SEM-IV Question Bank Regular Examination PDFSudhir NaikNo ratings yet

- Unit-3 Public ExpenditureDocument27 pagesUnit-3 Public ExpendituremelaNo ratings yet

- Assignment 2.1 - Married Individual TaxpayersDocument3 pagesAssignment 2.1 - Married Individual TaxpayersHunternotNo ratings yet

- Payroll Salary SlipDocument4 pagesPayroll Salary SlipDeca ErnandoNo ratings yet

- Reduction in Rate of Tax Deduction at Source (TDS) & Tax Collection at Source (TCS)Document6 pagesReduction in Rate of Tax Deduction at Source (TDS) & Tax Collection at Source (TCS)Kranthi Kumar KatamreddyNo ratings yet

- Chapter 1 - Fundamental Principles: TAXATION - The Process by Which The Sovereign, Through Its Law-Making BodyDocument11 pagesChapter 1 - Fundamental Principles: TAXATION - The Process by Which The Sovereign, Through Its Law-Making BodyLiRose SmithNo ratings yet

- HDFC 1Document1 pageHDFC 1Vivekananda PenumarthiNo ratings yet

- Income Tax Scrutiny NormsDocument6 pagesIncome Tax Scrutiny Normsphani raja kumarNo ratings yet

- The Alternatives To Universal Tax Registration in Sri LankaDocument11 pagesThe Alternatives To Universal Tax Registration in Sri Lankamick mooreNo ratings yet