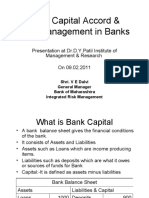

Lecture 10

Lecture 10

You might also like

- Financial Institutions Management A Risk Management Approach 8th Edition Saunders Solutions Manual 1Document17 pagesFinancial Institutions Management A Risk Management Approach 8th Edition Saunders Solutions Manual 1iva100% (47)

- Credit Pitch Overview - SampleDocument15 pagesCredit Pitch Overview - SampleChintu KumarNo ratings yet

- UC1.docx ACP iNSTITUTIONAL aSSESWSMENTDocument5 pagesUC1.docx ACP iNSTITUTIONAL aSSESWSMENTDanny R. Salvador100% (2)

- Workshop Financial Institutions STAFF1Document34 pagesWorkshop Financial Institutions STAFF1Ishan MalakarNo ratings yet

- Treasury ManagementDocument108 pagesTreasury Managementchinmoymishra100% (1)

- Mos Painting Works.Document4 pagesMos Painting Works.aniesbaekNo ratings yet

- Lecture 9Document61 pagesLecture 9copytradingwikiNo ratings yet

- Basel 3Document32 pagesBasel 3Venkat SaiNo ratings yet

- Lecture 7Document65 pagesLecture 7copytradingwikiNo ratings yet

- Chapter 9Document33 pagesChapter 9Faris IkhwanNo ratings yet

- Bank Capital NDocument38 pagesBank Capital NNANDINI GUPTANo ratings yet

- Lecture 11Document60 pagesLecture 11copytradingwikiNo ratings yet

- 20240429 125.364 Topic 07 Part 02 (2022 Teaching Version)Document24 pages20240429 125.364 Topic 07 Part 02 (2022 Teaching Version)jiejialing08No ratings yet

- Banking Laws and RegulationDocument19 pagesBanking Laws and RegulationAbdullah ZakariyyaNo ratings yet

- Capital Adequacy in Islamic BanksDocument32 pagesCapital Adequacy in Islamic BanksAmine ElghaziNo ratings yet

- Functions of Bank CapitalDocument4 pagesFunctions of Bank CapitalG117100% (1)

- TUT2TRMDocument17 pagesTUT2TRMQuynh Ngoc DangNo ratings yet

- BU7506 L1 SlidesDocument91 pagesBU7506 L1 SlidesAmritha VenkateshNo ratings yet

- Credit DerivativesDocument64 pagesCredit DerivativesJesta ZillaNo ratings yet

- F9-11 Weighted Average Cost of Capital and GearingDocument22 pagesF9-11 Weighted Average Cost of Capital and GearingPaiNo ratings yet

- L3 Capital ManagementDocument35 pagesL3 Capital ManagementZhiyu KamNo ratings yet

- ERM Training Material For InternalDocument99 pagesERM Training Material For InternalDwcastcarNo ratings yet

- Lecture 3_WC ManagementDocument130 pagesLecture 3_WC Managementphuongquyenle3No ratings yet

- Lecture21 Cdo & CdsDocument25 pagesLecture21 Cdo & Cdsfunkchunk33No ratings yet

- Credit RiskDocument26 pagesCredit RiskSecret PsychologyNo ratings yet

- FRM Lecture 11 2020 2021 HandoutDocument31 pagesFRM Lecture 11 2020 2021 HandoutDaanNo ratings yet

- Lecture 1: Capital Structure: Lorenzo BretscherDocument76 pagesLecture 1: Capital Structure: Lorenzo BretscherKatarina SusaNo ratings yet

- 01 Capitalstructure Lecture ADocument76 pages01 Capitalstructure Lecture AKatarina SusaNo ratings yet

- Lecture 5Document63 pagesLecture 5copytradingwikiNo ratings yet

- IFRS 9 2019 PresentationDocument25 pagesIFRS 9 2019 PresentationTina PhilipNo ratings yet

- BN 01 Basel Model SimplifiedDocument26 pagesBN 01 Basel Model SimplifiedVictory BalogunNo ratings yet

- Lecture 3_WC Management - EDITDocument131 pagesLecture 3_WC Management - EDITphuongquyenle3No ratings yet

- The Process of Portfolio Management: Portfolio Construction, Management, & Protection, 5e, Robert A. StrongDocument33 pagesThe Process of Portfolio Management: Portfolio Construction, Management, & Protection, 5e, Robert A. StrongQamarulArifinNo ratings yet

- 20240312_125.364 Topic03Document45 pages20240312_125.364 Topic03jiejialing08No ratings yet

- Lec3 Capital BudgetingDocument35 pagesLec3 Capital BudgetingThato HollaufNo ratings yet

- Basel Capital Accord & Risk Management in BanksDocument75 pagesBasel Capital Accord & Risk Management in Banksrahulg0710No ratings yet

- Basel 3Document3 pagesBasel 3NITIN PATHAKNo ratings yet

- Topic 3. Corporate FinanceDocument19 pagesTopic 3. Corporate FinancemhbytfhpzmNo ratings yet

- What Is The Difference Between Tier 1 Capital and Tier 2 Capital - InvestopediaDocument6 pagesWhat Is The Difference Between Tier 1 Capital and Tier 2 Capital - Investopediakiller dramaNo ratings yet

- Bank Regulations 2020Document35 pagesBank Regulations 2020SuvajitLaikNo ratings yet

- ALM HartfordDocument16 pagesALM HartfordIbnu NugrohoNo ratings yet

- eFM2e, CH 01, SlidesDocument13 pageseFM2e, CH 01, Slidesroyaf1203No ratings yet

- Chap 012 BBDocument8 pagesChap 012 BBMyaNo ratings yet

- Sales Handbook: For PartnersDocument44 pagesSales Handbook: For PartnersAnantha RamanNo ratings yet

- AnalytixWise - Risk Analytics Unit 3 Credit Risk AnalyticsDocument29 pagesAnalytixWise - Risk Analytics Unit 3 Credit Risk AnalyticsUrvashi Singh100% (1)

- Capital StructureDocument18 pagesCapital StructureGauri TyagiNo ratings yet

- CH16Document27 pagesCH16sajaabdullah195No ratings yet

- Applied Corporate FinanceDocument258 pagesApplied Corporate Financesirkoywayo6628No ratings yet

- The Process of Portfolio Management: Portfolio Construction, Management, & Protection, 4e, Robert A. StrongDocument35 pagesThe Process of Portfolio Management: Portfolio Construction, Management, & Protection, 4e, Robert A. StrongAkshay TyagiNo ratings yet

- Resa - The Review School of Accountancy Management ServicesDocument8 pagesResa - The Review School of Accountancy Management ServicesKindred Wolfe100% (1)

- Basel Typed NotesDocument18 pagesBasel Typed NotesSAYAN HARINo ratings yet

- Lecture Agency Tunneling Ownership FULL ForRepro Apr19 2024Document210 pagesLecture Agency Tunneling Ownership FULL ForRepro Apr19 2024jpl.laresistanceNo ratings yet

- Fin Corp CSDocument48 pagesFin Corp CSИрина МигусNo ratings yet

- The Process of Portfolio ManagementDocument35 pagesThe Process of Portfolio ManagementlalitNo ratings yet

- The Process of Portfolio ManagementDocument34 pagesThe Process of Portfolio ManagementMaazuuNo ratings yet

- Applied Corporate Finance: Aswath Damodaran For Material Specific To This Package, Go ToDocument72 pagesApplied Corporate Finance: Aswath Damodaran For Material Specific To This Package, Go TomeidianizaNo ratings yet

- FinanceDocument34 pagesFinancemillionaire's mindNo ratings yet

- Revise Corporate FinanceDocument4 pagesRevise Corporate FinanceNgoc Tran QuangNo ratings yet

- Asset & Liability Management Under Basel IIIDocument7 pagesAsset & Liability Management Under Basel IIIssj7cjqq2dNo ratings yet

- Lecture 1Document22 pagesLecture 1Дмитрий КолесниковNo ratings yet

- Handout. WCM - Basic ConceptsDocument31 pagesHandout. WCM - Basic ConceptsNaia SNo ratings yet

- Modern Security Analysis: Understanding Wall Street FundamentalsFrom EverandModern Security Analysis: Understanding Wall Street FundamentalsRating: 4 out of 5 stars4/5 (2)

- A. Kinesiology of HumanDocument7 pagesA. Kinesiology of HumanleyluuuuuhNo ratings yet

- Strengthen ShoulderDocument5 pagesStrengthen Shouldernacole78No ratings yet

- Arsenic TreatmentDocument31 pagesArsenic Treatmentnzy06No ratings yet

- Smitham Intuitive Eating Efficacy Bed 02 16 09Document43 pagesSmitham Intuitive Eating Efficacy Bed 02 16 09Evelyn Tribole, MS, RDNo ratings yet

- CESD-10 Website PDFDocument3 pagesCESD-10 Website PDFDoc HadiNo ratings yet

- Age Basic Conflict Basic Strength/ Virtue Core Pathology Important Event OutcomeDocument1 pageAge Basic Conflict Basic Strength/ Virtue Core Pathology Important Event OutcomeErnestjohnBelasotoNo ratings yet

- Smart Aquaculture Controlling System (S-AQUA)Document13 pagesSmart Aquaculture Controlling System (S-AQUA)pintuNo ratings yet

- Practical Guide To Dispersing AgentsDocument32 pagesPractical Guide To Dispersing AgentsGABRIEL ANGELO SANTOSNo ratings yet

- International Glass Art Retail DirectoryDocument82 pagesInternational Glass Art Retail DirectorytoxicwindNo ratings yet

- SRS Medical ManagementDocument7 pagesSRS Medical ManagementAtharv KatkarNo ratings yet

- Sickness Reimbursement B-304 PDFDocument2 pagesSickness Reimbursement B-304 PDFkaateviNo ratings yet

- ENVIRONMENTAL OUTLOOK To 2050 The Consequences of Inaction 2Document8 pagesENVIRONMENTAL OUTLOOK To 2050 The Consequences of Inaction 2Abcvdgtyio Sos RsvgNo ratings yet

- The Dowser's Handbook - Pendulums, Muscle Testing, Applied Kinesiology by Jimmy MackDocument44 pagesThe Dowser's Handbook - Pendulums, Muscle Testing, Applied Kinesiology by Jimmy MackZach90% (10)

- Revised DMLC I Template - January 2017Document10 pagesRevised DMLC I Template - January 2017waleed yehiaNo ratings yet

- Going Bananas: The World 'S Favorite Fruit Could Disappear Forever in 10 Years ' TimeDocument5 pagesGoing Bananas: The World 'S Favorite Fruit Could Disappear Forever in 10 Years ' TimeHa Quang Huy0% (1)

- Idiomatic ExpressionDocument27 pagesIdiomatic ExpressionJess Jess100% (1)

- Apx A1 Eng A4Document56 pagesApx A1 Eng A4kapokidNo ratings yet

- D 977 - 98 - Rdk3ny05oa - PDFDocument3 pagesD 977 - 98 - Rdk3ny05oa - PDFRichar DiegoNo ratings yet

- Thermetco-Thermocouple Welder TW9Document10 pagesThermetco-Thermocouple Welder TW9ghostinshellNo ratings yet

- Double Immunodiffusion TestDocument4 pagesDouble Immunodiffusion Testmuddassir attarNo ratings yet

- Bright 1958 Automation and ManagementDocument25 pagesBright 1958 Automation and ManagementGrupo sufrimiento, salud mental y trabajo.No ratings yet

- Prescription WritingDocument26 pagesPrescription WritingShaHiL HuSsAinNo ratings yet

- 1992-2001 Johnson Evinrude 65-300 HP V4 V6 V8 Engines Service Repair Manual PDFDocument522 pages1992-2001 Johnson Evinrude 65-300 HP V4 V6 V8 Engines Service Repair Manual PDFThợ Máy100% (7)

- General Chemistry Quarter 2 Week 1 3Document7 pagesGeneral Chemistry Quarter 2 Week 1 3Istian VlogsNo ratings yet

- Danika Sanders Student Teacher ResumeDocument2 pagesDanika Sanders Student Teacher Resumeapi-496485131No ratings yet

- Filter MiliporeDocument8 pagesFilter Miliporemotasa mojosarilabNo ratings yet

- Mina NEGRA HUANUSHA 2 ParteDocument23 pagesMina NEGRA HUANUSHA 2 ParteRoberto VillegasNo ratings yet

- Analisis Jarak Dilatasi Struktur Bangunan Menggunakan Sistem Dilatasi Dua KolomDocument11 pagesAnalisis Jarak Dilatasi Struktur Bangunan Menggunakan Sistem Dilatasi Dua KolomVvvg JNo ratings yet

Download as pdf or txt

You might also like

- Financial Institutions Management A Risk Management Approach 8th Edition Saunders Solutions Manual 1Document17 pagesFinancial Institutions Management A Risk Management Approach 8th Edition Saunders Solutions Manual 1iva100% (47)

- Credit Pitch Overview - SampleDocument15 pagesCredit Pitch Overview - SampleChintu KumarNo ratings yet

- UC1.docx ACP iNSTITUTIONAL aSSESWSMENTDocument5 pagesUC1.docx ACP iNSTITUTIONAL aSSESWSMENTDanny R. Salvador100% (2)

- Workshop Financial Institutions STAFF1Document34 pagesWorkshop Financial Institutions STAFF1Ishan MalakarNo ratings yet

- Treasury ManagementDocument108 pagesTreasury Managementchinmoymishra100% (1)

- Mos Painting Works.Document4 pagesMos Painting Works.aniesbaekNo ratings yet

- Lecture 9Document61 pagesLecture 9copytradingwikiNo ratings yet

- Basel 3Document32 pagesBasel 3Venkat SaiNo ratings yet

- Lecture 7Document65 pagesLecture 7copytradingwikiNo ratings yet

- Chapter 9Document33 pagesChapter 9Faris IkhwanNo ratings yet

- Bank Capital NDocument38 pagesBank Capital NNANDINI GUPTANo ratings yet

- Lecture 11Document60 pagesLecture 11copytradingwikiNo ratings yet

- 20240429 125.364 Topic 07 Part 02 (2022 Teaching Version)Document24 pages20240429 125.364 Topic 07 Part 02 (2022 Teaching Version)jiejialing08No ratings yet

- Banking Laws and RegulationDocument19 pagesBanking Laws and RegulationAbdullah ZakariyyaNo ratings yet

- Capital Adequacy in Islamic BanksDocument32 pagesCapital Adequacy in Islamic BanksAmine ElghaziNo ratings yet

- Functions of Bank CapitalDocument4 pagesFunctions of Bank CapitalG117100% (1)

- TUT2TRMDocument17 pagesTUT2TRMQuynh Ngoc DangNo ratings yet

- BU7506 L1 SlidesDocument91 pagesBU7506 L1 SlidesAmritha VenkateshNo ratings yet

- Credit DerivativesDocument64 pagesCredit DerivativesJesta ZillaNo ratings yet

- F9-11 Weighted Average Cost of Capital and GearingDocument22 pagesF9-11 Weighted Average Cost of Capital and GearingPaiNo ratings yet

- L3 Capital ManagementDocument35 pagesL3 Capital ManagementZhiyu KamNo ratings yet

- ERM Training Material For InternalDocument99 pagesERM Training Material For InternalDwcastcarNo ratings yet

- Lecture 3_WC ManagementDocument130 pagesLecture 3_WC Managementphuongquyenle3No ratings yet

- Lecture21 Cdo & CdsDocument25 pagesLecture21 Cdo & Cdsfunkchunk33No ratings yet

- Credit RiskDocument26 pagesCredit RiskSecret PsychologyNo ratings yet

- FRM Lecture 11 2020 2021 HandoutDocument31 pagesFRM Lecture 11 2020 2021 HandoutDaanNo ratings yet

- Lecture 1: Capital Structure: Lorenzo BretscherDocument76 pagesLecture 1: Capital Structure: Lorenzo BretscherKatarina SusaNo ratings yet

- 01 Capitalstructure Lecture ADocument76 pages01 Capitalstructure Lecture AKatarina SusaNo ratings yet

- Lecture 5Document63 pagesLecture 5copytradingwikiNo ratings yet

- IFRS 9 2019 PresentationDocument25 pagesIFRS 9 2019 PresentationTina PhilipNo ratings yet

- BN 01 Basel Model SimplifiedDocument26 pagesBN 01 Basel Model SimplifiedVictory BalogunNo ratings yet

- Lecture 3_WC Management - EDITDocument131 pagesLecture 3_WC Management - EDITphuongquyenle3No ratings yet

- The Process of Portfolio Management: Portfolio Construction, Management, & Protection, 5e, Robert A. StrongDocument33 pagesThe Process of Portfolio Management: Portfolio Construction, Management, & Protection, 5e, Robert A. StrongQamarulArifinNo ratings yet

- 20240312_125.364 Topic03Document45 pages20240312_125.364 Topic03jiejialing08No ratings yet

- Lec3 Capital BudgetingDocument35 pagesLec3 Capital BudgetingThato HollaufNo ratings yet

- Basel Capital Accord & Risk Management in BanksDocument75 pagesBasel Capital Accord & Risk Management in Banksrahulg0710No ratings yet

- Basel 3Document3 pagesBasel 3NITIN PATHAKNo ratings yet

- Topic 3. Corporate FinanceDocument19 pagesTopic 3. Corporate FinancemhbytfhpzmNo ratings yet

- What Is The Difference Between Tier 1 Capital and Tier 2 Capital - InvestopediaDocument6 pagesWhat Is The Difference Between Tier 1 Capital and Tier 2 Capital - Investopediakiller dramaNo ratings yet

- Bank Regulations 2020Document35 pagesBank Regulations 2020SuvajitLaikNo ratings yet

- ALM HartfordDocument16 pagesALM HartfordIbnu NugrohoNo ratings yet

- eFM2e, CH 01, SlidesDocument13 pageseFM2e, CH 01, Slidesroyaf1203No ratings yet

- Chap 012 BBDocument8 pagesChap 012 BBMyaNo ratings yet

- Sales Handbook: For PartnersDocument44 pagesSales Handbook: For PartnersAnantha RamanNo ratings yet

- AnalytixWise - Risk Analytics Unit 3 Credit Risk AnalyticsDocument29 pagesAnalytixWise - Risk Analytics Unit 3 Credit Risk AnalyticsUrvashi Singh100% (1)

- Capital StructureDocument18 pagesCapital StructureGauri TyagiNo ratings yet

- CH16Document27 pagesCH16sajaabdullah195No ratings yet

- Applied Corporate FinanceDocument258 pagesApplied Corporate Financesirkoywayo6628No ratings yet

- The Process of Portfolio Management: Portfolio Construction, Management, & Protection, 4e, Robert A. StrongDocument35 pagesThe Process of Portfolio Management: Portfolio Construction, Management, & Protection, 4e, Robert A. StrongAkshay TyagiNo ratings yet

- Resa - The Review School of Accountancy Management ServicesDocument8 pagesResa - The Review School of Accountancy Management ServicesKindred Wolfe100% (1)

- Basel Typed NotesDocument18 pagesBasel Typed NotesSAYAN HARINo ratings yet

- Lecture Agency Tunneling Ownership FULL ForRepro Apr19 2024Document210 pagesLecture Agency Tunneling Ownership FULL ForRepro Apr19 2024jpl.laresistanceNo ratings yet

- Fin Corp CSDocument48 pagesFin Corp CSИрина МигусNo ratings yet

- The Process of Portfolio ManagementDocument35 pagesThe Process of Portfolio ManagementlalitNo ratings yet

- The Process of Portfolio ManagementDocument34 pagesThe Process of Portfolio ManagementMaazuuNo ratings yet

- Applied Corporate Finance: Aswath Damodaran For Material Specific To This Package, Go ToDocument72 pagesApplied Corporate Finance: Aswath Damodaran For Material Specific To This Package, Go TomeidianizaNo ratings yet

- FinanceDocument34 pagesFinancemillionaire's mindNo ratings yet

- Revise Corporate FinanceDocument4 pagesRevise Corporate FinanceNgoc Tran QuangNo ratings yet

- Asset & Liability Management Under Basel IIIDocument7 pagesAsset & Liability Management Under Basel IIIssj7cjqq2dNo ratings yet

- Lecture 1Document22 pagesLecture 1Дмитрий КолесниковNo ratings yet

- Handout. WCM - Basic ConceptsDocument31 pagesHandout. WCM - Basic ConceptsNaia SNo ratings yet

- Modern Security Analysis: Understanding Wall Street FundamentalsFrom EverandModern Security Analysis: Understanding Wall Street FundamentalsRating: 4 out of 5 stars4/5 (2)

- A. Kinesiology of HumanDocument7 pagesA. Kinesiology of HumanleyluuuuuhNo ratings yet

- Strengthen ShoulderDocument5 pagesStrengthen Shouldernacole78No ratings yet

- Arsenic TreatmentDocument31 pagesArsenic Treatmentnzy06No ratings yet

- Smitham Intuitive Eating Efficacy Bed 02 16 09Document43 pagesSmitham Intuitive Eating Efficacy Bed 02 16 09Evelyn Tribole, MS, RDNo ratings yet

- CESD-10 Website PDFDocument3 pagesCESD-10 Website PDFDoc HadiNo ratings yet

- Age Basic Conflict Basic Strength/ Virtue Core Pathology Important Event OutcomeDocument1 pageAge Basic Conflict Basic Strength/ Virtue Core Pathology Important Event OutcomeErnestjohnBelasotoNo ratings yet

- Smart Aquaculture Controlling System (S-AQUA)Document13 pagesSmart Aquaculture Controlling System (S-AQUA)pintuNo ratings yet

- Practical Guide To Dispersing AgentsDocument32 pagesPractical Guide To Dispersing AgentsGABRIEL ANGELO SANTOSNo ratings yet

- International Glass Art Retail DirectoryDocument82 pagesInternational Glass Art Retail DirectorytoxicwindNo ratings yet

- SRS Medical ManagementDocument7 pagesSRS Medical ManagementAtharv KatkarNo ratings yet

- Sickness Reimbursement B-304 PDFDocument2 pagesSickness Reimbursement B-304 PDFkaateviNo ratings yet

- ENVIRONMENTAL OUTLOOK To 2050 The Consequences of Inaction 2Document8 pagesENVIRONMENTAL OUTLOOK To 2050 The Consequences of Inaction 2Abcvdgtyio Sos RsvgNo ratings yet

- The Dowser's Handbook - Pendulums, Muscle Testing, Applied Kinesiology by Jimmy MackDocument44 pagesThe Dowser's Handbook - Pendulums, Muscle Testing, Applied Kinesiology by Jimmy MackZach90% (10)

- Revised DMLC I Template - January 2017Document10 pagesRevised DMLC I Template - January 2017waleed yehiaNo ratings yet

- Going Bananas: The World 'S Favorite Fruit Could Disappear Forever in 10 Years ' TimeDocument5 pagesGoing Bananas: The World 'S Favorite Fruit Could Disappear Forever in 10 Years ' TimeHa Quang Huy0% (1)

- Idiomatic ExpressionDocument27 pagesIdiomatic ExpressionJess Jess100% (1)

- Apx A1 Eng A4Document56 pagesApx A1 Eng A4kapokidNo ratings yet

- D 977 - 98 - Rdk3ny05oa - PDFDocument3 pagesD 977 - 98 - Rdk3ny05oa - PDFRichar DiegoNo ratings yet

- Thermetco-Thermocouple Welder TW9Document10 pagesThermetco-Thermocouple Welder TW9ghostinshellNo ratings yet

- Double Immunodiffusion TestDocument4 pagesDouble Immunodiffusion Testmuddassir attarNo ratings yet

- Bright 1958 Automation and ManagementDocument25 pagesBright 1958 Automation and ManagementGrupo sufrimiento, salud mental y trabajo.No ratings yet

- Prescription WritingDocument26 pagesPrescription WritingShaHiL HuSsAinNo ratings yet

- 1992-2001 Johnson Evinrude 65-300 HP V4 V6 V8 Engines Service Repair Manual PDFDocument522 pages1992-2001 Johnson Evinrude 65-300 HP V4 V6 V8 Engines Service Repair Manual PDFThợ Máy100% (7)

- General Chemistry Quarter 2 Week 1 3Document7 pagesGeneral Chemistry Quarter 2 Week 1 3Istian VlogsNo ratings yet

- Danika Sanders Student Teacher ResumeDocument2 pagesDanika Sanders Student Teacher Resumeapi-496485131No ratings yet

- Filter MiliporeDocument8 pagesFilter Miliporemotasa mojosarilabNo ratings yet

- Mina NEGRA HUANUSHA 2 ParteDocument23 pagesMina NEGRA HUANUSHA 2 ParteRoberto VillegasNo ratings yet

- Analisis Jarak Dilatasi Struktur Bangunan Menggunakan Sistem Dilatasi Dua KolomDocument11 pagesAnalisis Jarak Dilatasi Struktur Bangunan Menggunakan Sistem Dilatasi Dua KolomVvvg JNo ratings yet