Download as pdf or txt

You might also like

- Strategic Management Theory and PracticeDocument61 pagesStrategic Management Theory and Practicelarry.calder828100% (44)

- The Clever Girl Finance RoadmapDocument11 pagesThe Clever Girl Finance RoadmapBrione E Smith100% (2)

- 6 Inventory PDFDocument10 pages6 Inventory PDFJorufel PapasinNo ratings yet

- Inventory Management in Asian PaintsDocument2 pagesInventory Management in Asian PaintsSrinivasan Em75% (4)

- Sale TransactionDocument37 pagesSale TransactionnayhachivaareeNo ratings yet

- Merch 1Document3 pagesMerch 1Angelica EcliseNo ratings yet

- Topic 1.1.1 Additional NotesDocument6 pagesTopic 1.1.1 Additional NotesMei Yi YeoNo ratings yet

- ACT103 Quiz 4Document3 pagesACT103 Quiz 4Jaeyoung JangNo ratings yet

- Basic Documentation and Books of Account: Topic 3Document32 pagesBasic Documentation and Books of Account: Topic 3vickramravi16No ratings yet

- Merchandising Operations JournalizingDocument45 pagesMerchandising Operations JournalizingNeri La LunaNo ratings yet

- Merchandising Organized As A Partnership BusinessDocument23 pagesMerchandising Organized As A Partnership BusinessIzza WrapNo ratings yet

- 05 Activity BADocument2 pages05 Activity BATyron Franz AnoricoNo ratings yet

- Exercise Set-Intro For Merchandising BusinessDocument10 pagesExercise Set-Intro For Merchandising BusinessCha Eun WooNo ratings yet

- Cash and ReceivablesDocument74 pagesCash and ReceivablesChitta LeeNo ratings yet

- Accounting 511 - ConsignmentDocument6 pagesAccounting 511 - ConsignmentLorenz BaguioNo ratings yet

- Accounting Analyzing Business Transaction ReviewerDocument7 pagesAccounting Analyzing Business Transaction Reviewerandreajade.cawaya10No ratings yet

- LECTURE Dec. 12 2022Document17 pagesLECTURE Dec. 12 2022lheamaecayabyab4No ratings yet

- Class Notes of Consignor & ConsigneeDocument13 pagesClass Notes of Consignor & ConsigneeDb100% (1)

- ACC 124 HO 6 Accounts ReceivableDocument3 pagesACC 124 HO 6 Accounts ReceivableJames Cañada GatoNo ratings yet

- CH 5 - Returns, Discounts and Sales Tax - UpdatedDocument31 pagesCH 5 - Returns, Discounts and Sales Tax - Updatedgolooz43No ratings yet

- Accounting For Merchandising Operations: Ricalyn E. Sumpay, CPADocument27 pagesAccounting For Merchandising Operations: Ricalyn E. Sumpay, CPAChathy AbabaNo ratings yet

- 2ND Term S3 Financial AccountDocument24 pages2ND Term S3 Financial Accountsaidu musaNo ratings yet

- CH 5Document35 pagesCH 5Mohamed DiabNo ratings yet

- Lecture 4 - ChapterDocument16 pagesLecture 4 - Chapter200207038No ratings yet

- MerchandisingDocument37 pagesMerchandisingDaniel Togonon Capones Jr.No ratings yet

- Acct Lesson 9Document9 pagesAcct Lesson 9Trisha Rodriguez CapulongNo ratings yet

- Chapter 4 & 5 - Accounts Receivable, Estimation of DaDocument6 pagesChapter 4 & 5 - Accounts Receivable, Estimation of DaAvia Chelsy DeangNo ratings yet

- Lecture Notes On MerchandisingDocument4 pagesLecture Notes On MerchandisingmoNo ratings yet

- Unit 1: Assessment ExercisesDocument2 pagesUnit 1: Assessment ExercisesJaved MushtaqNo ratings yet

- Qn1 - Final Accounts: One ApproachDocument42 pagesQn1 - Final Accounts: One ApproachKILL3R YTNo ratings yet

- Ac 511 Consignments: Consignment - OutDocument2 pagesAc 511 Consignments: Consignment - OutdewiNo ratings yet

- Accounting For Merchandising AE1311Document24 pagesAccounting For Merchandising AE1311Apple Joy YutaNo ratings yet

- Financial Statements With Adjustments: Submitted To:-Ms. Palak Bajaj Submitted By:-Chirag VermaDocument15 pagesFinancial Statements With Adjustments: Submitted To:-Ms. Palak Bajaj Submitted By:-Chirag VermaChiragNo ratings yet

- Learning Module - Accounts ReceivableDocument2 pagesLearning Module - Accounts ReceivableAngelica SamonteNo ratings yet

- Notes INTACC 1Document8 pagesNotes INTACC 1ALLYSA DENIELLE SAYATNo ratings yet

- Revision Points - Accounting GradeDocument8 pagesRevision Points - Accounting GradePrasad NaikNo ratings yet

- AccountingDocument119 pagesAccountingJhunnel LangubanNo ratings yet

- Accounting For MerchandisingDocument2 pagesAccounting For MerchandisingEvelyn MaligayaNo ratings yet

- InventoryDocument109 pagesInventoryco230154No ratings yet

- Chapter 4.2 Accounts ReceivableDocument7 pagesChapter 4.2 Accounts Receivable2021315379No ratings yet

- Acc106 Chapter Four Textbook Questions Nur Hazani 2020818012Document7 pagesAcc106 Chapter Four Textbook Questions Nur Hazani 2020818012nur hazaniNo ratings yet

- Unit II A Accounts ReceivablesDocument12 pagesUnit II A Accounts ReceivablesJulie Ann TolinNo ratings yet

- INTACC 1 - REVIEWER - MIDTERMS (Receivables)Document3 pagesINTACC 1 - REVIEWER - MIDTERMS (Receivables)olerianaryzzsc.56No ratings yet

- ACC 1101 Final MergedDocument50 pagesACC 1101 Final MergedEmdadul HosenNo ratings yet

- Assessment Accounting - Exercise-U1Document5 pagesAssessment Accounting - Exercise-U1Anam KhanNo ratings yet

- Handout - CB Session Gipe Session 8 & 9 - 21 & 22-09-21Document19 pagesHandout - CB Session Gipe Session 8 & 9 - 21 & 22-09-21Aliasgar TamimNo ratings yet

- Reflection Paper-Ba233N IFTransactionDocument7 pagesReflection Paper-Ba233N IFTransactionJoya Labao Macario-BalquinNo ratings yet

- Acc117-Chapter 4-1Document25 pagesAcc117-Chapter 4-1Fadilah JefriNo ratings yet

- Module - ReceivablesDocument10 pagesModule - ReceivablesJohn Lindy SorianoNo ratings yet

- CH 5: Merchandise Operations - Perpetual - Journal Entries: Buyer'S Books Seller'S BooksDocument6 pagesCH 5: Merchandise Operations - Perpetual - Journal Entries: Buyer'S Books Seller'S BooksbharatNo ratings yet

- Accounts ReceivableDocument54 pagesAccounts ReceivableFrancine Thea M. LantayaNo ratings yet

- Module 3. Part 1 - Accounts Receivable For StudentsDocument36 pagesModule 3. Part 1 - Accounts Receivable For Studentslord kwantoniumNo ratings yet

- CHAPTER 2 Double Entryn (MCQ)Document8 pagesCHAPTER 2 Double Entryn (MCQ)saksaman74No ratings yet

- In-Class Exercise Chapter 5Document6 pagesIn-Class Exercise Chapter 5Thomas TermoteNo ratings yet

- Joint VentureDocument32 pagesJoint VentureKaren SomcioNo ratings yet

- Basic Accounting Tutorial Part 2 by DiansuyDocument33 pagesBasic Accounting Tutorial Part 2 by DiansuyMeila GomezNo ratings yet

- Module4 AccountsReceivablePartIDocument6 pagesModule4 AccountsReceivablePartIGab OdonioNo ratings yet

- Ita - Chapter 2Document11 pagesIta - Chapter 2Ali aliNo ratings yet

- MCQs Exam Review Sheet Variant 1Document6 pagesMCQs Exam Review Sheet Variant 1Majid 1 MubarakNo ratings yet

- Financial Statements With Adjustments: Submitted To:-Ms Palak Bajaj Submitted To:-Chirag VermaDocument15 pagesFinancial Statements With Adjustments: Submitted To:-Ms Palak Bajaj Submitted To:-Chirag VermaChiragNo ratings yet

- Merchandising Business - Sample Problem (Answers)Document4 pagesMerchandising Business - Sample Problem (Answers)Eana MabalotNo ratings yet

- The Barrington Guide to Property Management Accounting: The Definitive Guide for Property Owners, Managers, Accountants, and Bookkeepers to ThriveFrom EverandThe Barrington Guide to Property Management Accounting: The Definitive Guide for Property Owners, Managers, Accountants, and Bookkeepers to ThriveNo ratings yet

- Brand KnowledgeDocument23 pagesBrand KnowledgeSabeedEjaz0% (1)

- John F. Kennedy: Bachelor of Science: Major Public AccountingDocument2 pagesJohn F. Kennedy: Bachelor of Science: Major Public AccountingConnor FentonNo ratings yet

- Mining Policy HandbookDocument16 pagesMining Policy HandbookWhitney ANo ratings yet

- Bitcoin Mining SurveyDocument7 pagesBitcoin Mining SurveyxxNo ratings yet

- 2018耗材展 会刊 RemaxWorldDocument240 pages2018耗材展 会刊 RemaxWorldankit.patelNo ratings yet

- 17 181 FirstSolar Thompson PDFDocument33 pages17 181 FirstSolar Thompson PDFGideon Oyibo0% (1)

- A Level Paper 3: 2016 2012 Only Basic Economic Ideas and Resource AllocationDocument36 pagesA Level Paper 3: 2016 2012 Only Basic Economic Ideas and Resource AllocationShehrozSTNo ratings yet

- FOS Lesson PlanDocument6 pagesFOS Lesson PlanReymond SumayloNo ratings yet

- Modelo de Contrato en Ingles Por Locacion de ServiciosDocument15 pagesModelo de Contrato en Ingles Por Locacion de ServiciosMariana ReyNo ratings yet

- JBMA 13 020mohajanDocument9 pagesJBMA 13 020mohajanManjare Hassin RaadNo ratings yet

- Sample of Company Profile3Document33 pagesSample of Company Profile3Muhammad Kawser PatwaryNo ratings yet

- The Insider Trading Anomaly Endures 50 Years After It Was First Identified by Lorie and NiederhofferDocument3 pagesThe Insider Trading Anomaly Endures 50 Years After It Was First Identified by Lorie and Niederhoffertidomam303No ratings yet

- NET PRESENT VALUE (NPV) PwrpointDocument42 pagesNET PRESENT VALUE (NPV) Pwrpointjumar_loocNo ratings yet

- ZCC Full Catalogue 2019 - 511 - 513printDocument1,160 pagesZCC Full Catalogue 2019 - 511 - 513printIrwan SyahputraNo ratings yet

- Vistex Design Rationale - Commission - FlooringDocument40 pagesVistex Design Rationale - Commission - FlooringMosi Debbie0% (1)

- Modutec IEC 61439 Asta Bonanza - ABBDocument23 pagesModutec IEC 61439 Asta Bonanza - ABBRamani ManiNo ratings yet

- Bim Ready CompleteDocument17 pagesBim Ready Completezcf7uuNo ratings yet

- (Test Sample) - SUMMER MIDTERM EXAM (2021)Document2 pages(Test Sample) - SUMMER MIDTERM EXAM (2021)tranthithanhhuong25110211No ratings yet

- Supply Chain Finance Market Assessment KenyaDocument18 pagesSupply Chain Finance Market Assessment Kenyaetebark h/michaleNo ratings yet

- Bplo PDFDocument5 pagesBplo PDFAlan FernandoNo ratings yet

- Specialized Government BanksDocument5 pagesSpecialized Government BanksCarazelli AysonNo ratings yet

- Practical Research 2 2Document28 pagesPractical Research 2 2Alian BarrogaNo ratings yet

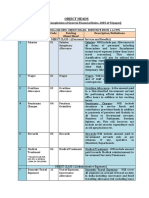

- Object Head List PDFDocument6 pagesObject Head List PDFLal ZahawmaNo ratings yet

- Revision NotesDocument51 pagesRevision NotesMelody RoseNo ratings yet

- Supply Chain of HascolDocument9 pagesSupply Chain of HascolqamarunnisaNo ratings yet

- 1 ModelsDocument30 pages1 Modelssara alshNo ratings yet

- Notes - 50001 2018 EnMSDocument9 pagesNotes - 50001 2018 EnMSJoanna Aubrey LagrosaNo ratings yet