Download as pdf or txt

You might also like

- Acct For ConsignmnetDocument12 pagesAcct For Consignmnetsamuel debebe100% (2)

- 6 Inventory PDFDocument10 pages6 Inventory PDFJorufel PapasinNo ratings yet

- TK03 Aks Liana DamayantiDocument7 pagesTK03 Aks Liana DamayantiLiana DamayantiNo ratings yet

- Buy TransactionDocument37 pagesBuy TransactionnayhachivaareeNo ratings yet

- Acct Lesson 9Document9 pagesAcct Lesson 9Trisha Rodriguez CapulongNo ratings yet

- Accounting 511 - ConsignmentDocument6 pagesAccounting 511 - ConsignmentLorenz BaguioNo ratings yet

- Merchandising Operations JournalizingDocument45 pagesMerchandising Operations JournalizingNeri La LunaNo ratings yet

- Chapter 4.2 Accounts ReceivableDocument7 pagesChapter 4.2 Accounts Receivable2021315379No ratings yet

- CH 5Document35 pagesCH 5Mohamed DiabNo ratings yet

- Cachuela 4Document25 pagesCachuela 4Daphn CuencaNo ratings yet

- Merchandising Organized As A Partnership BusinessDocument23 pagesMerchandising Organized As A Partnership BusinessIzza WrapNo ratings yet

- ACC 124 HO 6 Accounts ReceivableDocument3 pagesACC 124 HO 6 Accounts ReceivableJames Cañada GatoNo ratings yet

- Topic 1.1.1 Additional NotesDocument6 pagesTopic 1.1.1 Additional NotesMei Yi YeoNo ratings yet

- ACT103 Quiz 4Document3 pagesACT103 Quiz 4Jaeyoung JangNo ratings yet

- Accounting PrinciplesDocument35 pagesAccounting Principlesnaveed azeemNo ratings yet

- Lecture Notes On MerchandisingDocument4 pagesLecture Notes On MerchandisingmoNo ratings yet

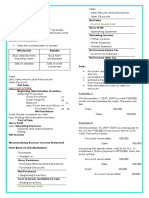

- Financial Statements With Adjustments: Submitted To:-Ms. Palak Bajaj Submitted By:-Chirag VermaDocument15 pagesFinancial Statements With Adjustments: Submitted To:-Ms. Palak Bajaj Submitted By:-Chirag VermaChiragNo ratings yet

- Accounting For Merchandising AE1311Document24 pagesAccounting For Merchandising AE1311Apple Joy YutaNo ratings yet

- Ac 511 Consignments: Consignment - OutDocument2 pagesAc 511 Consignments: Consignment - OutdewiNo ratings yet

- Exercise Set-Intro For Merchandising BusinessDocument10 pagesExercise Set-Intro For Merchandising BusinessCha Eun WooNo ratings yet

- Accounting PrinciplesDocument36 pagesAccounting PrinciplesEshetieNo ratings yet

- Class Notes of Consignor & ConsigneeDocument13 pagesClass Notes of Consignor & ConsigneeDb100% (1)

- ConsignmentDocument6 pagesConsignmentendouusaNo ratings yet

- Cerbas Accounts ReceivableDocument23 pagesCerbas Accounts Receivablemarites yuNo ratings yet

- Accounts ReceivableDocument54 pagesAccounts ReceivableFrancine Thea M. LantayaNo ratings yet

- Accounting For Merchandising Operations: Ricalyn E. Sumpay, CPADocument27 pagesAccounting For Merchandising Operations: Ricalyn E. Sumpay, CPAChathy AbabaNo ratings yet

- Consignment Accounting Journal EntriesDocument22 pagesConsignment Accounting Journal EntriesRashid HussainNo ratings yet

- This Study Resource WasDocument2 pagesThis Study Resource WasTrixie HicaldeNo ratings yet

- MerchandisingDocument37 pagesMerchandisingDaniel Togonon Capones Jr.No ratings yet

- Merch 1Document3 pagesMerch 1Angelica EcliseNo ratings yet

- Accounting For MerchandisingDocument2 pagesAccounting For MerchandisingEvelyn MaligayaNo ratings yet

- Module - ReceivablesDocument10 pagesModule - ReceivablesJohn Lindy SorianoNo ratings yet

- CONSIGNMENT ACCOUNT - Docx2Document8 pagesCONSIGNMENT ACCOUNT - Docx2Gamer nestNo ratings yet

- Cash and ReceivablesDocument74 pagesCash and ReceivablesChitta LeeNo ratings yet

- Consignment ConceptsDocument34 pagesConsignment ConceptsRanne BalanaNo ratings yet

- Inventory System - UpdatedDocument42 pagesInventory System - UpdatedAngel WestNo ratings yet

- Financial Statements With Adjustments: Submitted To:-Ms Palak Bajaj Submitted To:-Chirag VermaDocument15 pagesFinancial Statements With Adjustments: Submitted To:-Ms Palak Bajaj Submitted To:-Chirag VermaChiragNo ratings yet

- Chapter 4 & 5 - Accounts Receivable, Estimation of DaDocument6 pagesChapter 4 & 5 - Accounts Receivable, Estimation of DaAvia Chelsy DeangNo ratings yet

- FAR QTR2 Part1.notesDocument27 pagesFAR QTR2 Part1.notestygurNo ratings yet

- 4 Accounts ReceivableDocument10 pages4 Accounts ReceivableAYEZZA SAMSONNo ratings yet

- Merchandising Business - Sample Problem (Answers)Document4 pagesMerchandising Business - Sample Problem (Answers)Eana MabalotNo ratings yet

- Receivable ManagementDocument49 pagesReceivable Managementrekha123No ratings yet

- Unit VII - Consignment SalesDocument5 pagesUnit VII - Consignment SalesNovylyn AldaveNo ratings yet

- Basic Documentation and Books of Account: Topic 3Document32 pagesBasic Documentation and Books of Account: Topic 3vickramravi16No ratings yet

- Case Problem 1 (King Distributors) : Chart of Accounts For Journalizing, Posting and Trial Balance AssetsDocument2 pagesCase Problem 1 (King Distributors) : Chart of Accounts For Journalizing, Posting and Trial Balance AssetsRolly BaroyNo ratings yet

- 06.marchandising Operation-FinalDocument53 pages06.marchandising Operation-FinalChowdhury Mobarrat Haider AdnanNo ratings yet

- Module4 AccountsReceivablePartIDocument6 pagesModule4 AccountsReceivablePartIGab OdonioNo ratings yet

- Acc106 Chapter Four Textbook Questions Nur Hazani 2020818012Document7 pagesAcc106 Chapter Four Textbook Questions Nur Hazani 2020818012nur hazaniNo ratings yet

- Accounts Receivable: Notwithstanding, Are Classified As Current AssetsDocument13 pagesAccounts Receivable: Notwithstanding, Are Classified As Current AssetsAdyangNo ratings yet

- Basic Accounting Tutorial Part 2 by DiansuyDocument33 pagesBasic Accounting Tutorial Part 2 by DiansuyMeila GomezNo ratings yet

- Lecture On Merchandising OperationDocument44 pagesLecture On Merchandising OperationJean Paula SequiñoNo ratings yet

- Trade and Other Receivables (IA)Document6 pagesTrade and Other Receivables (IA)pcdesktop.brarNo ratings yet

- Week 3 The Accounting Cycle Merchandising BusinessDocument8 pagesWeek 3 The Accounting Cycle Merchandising BusinessVinz Danzel BialaNo ratings yet

- Sale of Merchandise or ServicesDocument4 pagesSale of Merchandise or ServicesAngelica PagaduanNo ratings yet

- Module 1 - Credit Bad DebtsDocument21 pagesModule 1 - Credit Bad Debtsiacpa.aialmeNo ratings yet

- Module 3. Part 1 - Accounts Receivable For StudentsDocument36 pagesModule 3. Part 1 - Accounts Receivable For Studentslord kwantoniumNo ratings yet

- Cuenca 4Document31 pagesCuenca 4Daphn CuencaNo ratings yet

- Chapter 7 09302019Document38 pagesChapter 7 09302019Arjay Molina100% (1)

- In-Class Exercise Chapter 5Document6 pagesIn-Class Exercise Chapter 5Thomas TermoteNo ratings yet

- The All-New Real Estate Foreclosure, Short-Selling, Underwater, Property Auction, Positive Cash Flow Book: Your Ultimate Guide to Making Money in a Crashing MarketFrom EverandThe All-New Real Estate Foreclosure, Short-Selling, Underwater, Property Auction, Positive Cash Flow Book: Your Ultimate Guide to Making Money in a Crashing MarketNo ratings yet

- Chapter 1 Cash and Cash EquivalentsDocument29 pagesChapter 1 Cash and Cash EquivalentsENCARNACION Princess MarieNo ratings yet

- Chapter 4 Recording of TransactiosDocument24 pagesChapter 4 Recording of TransactiosJohn Mark MaligaligNo ratings yet

- PD For Banking-01Document44 pagesPD For Banking-01khanarif16No ratings yet

- PCMRP Manual 790Document541 pagesPCMRP Manual 790Diiee Fürstin JojoNo ratings yet

- Verma Glass CoDocument8 pagesVerma Glass CoJai Bhushan BharmouriaNo ratings yet

- CPWA CODE 151-200 (Guide Part 5) PDFDocument13 pagesCPWA CODE 151-200 (Guide Part 5) PDFshekarj0% (1)

- Chapter 10Document44 pagesChapter 10Rifai RifaiNo ratings yet

- Internship Report at FFCDocument93 pagesInternship Report at FFCmuhammad irfan100% (8)

- 1 VJP 0 LTVX WHN RV ZUCj NLDocument10 pages1 VJP 0 LTVX WHN RV ZUCj NLVanshika BhatiNo ratings yet

- Sap SD Process FlowsDocument19 pagesSap SD Process Flowsramesh100% (1)

- Concept Paper: (Available For Comments Up To April 15, 2016)Document23 pagesConcept Paper: (Available For Comments Up To April 15, 2016)SanjeevNo ratings yet

- El Detalle de Las TransferenciasDocument44 pagesEl Detalle de Las TransferenciasTodo NoticiasNo ratings yet

- Chapter 8 Adjusting Entries 2 SHSDocument81 pagesChapter 8 Adjusting Entries 2 SHSTep TepNo ratings yet

- Macroeconomics ConsolidatedDocument118 pagesMacroeconomics ConsolidatedViral SavlaNo ratings yet

- BBA BIM BBM 2nd Semester Model Question AllDocument22 pagesBBA BIM BBM 2nd Semester Model Question AllGLOBAL I.Q.No ratings yet

- General Ledger: Instructor: MANISH CHAUHANDocument53 pagesGeneral Ledger: Instructor: MANISH CHAUHANRanbeer CoolNo ratings yet

- 2007 LCCI Level 2 Series 3 (HK) Model AnswersDocument12 pages2007 LCCI Level 2 Series 3 (HK) Model AnswersChoi Kin Yi Carmen67% (3)

- Ch01 - 04 - Sample Blank WS, GJ, GLDocument42 pagesCh01 - 04 - Sample Blank WS, GJ, GLThanh UyênNo ratings yet

- ACCOUNTING P1 GR11 QP NOVEMBER 2020 EnglishDocument12 pagesACCOUNTING P1 GR11 QP NOVEMBER 2020 EnglishbmtnrcmzqyNo ratings yet

- Half Yearly Syllabus 2021-2022Document9 pagesHalf Yearly Syllabus 2021-2022kalyani kumariNo ratings yet

- Acctg 1 Problems - JMCDocument1 pageAcctg 1 Problems - JMCJohn Alfred CastinoNo ratings yet

- InventoryDocument19 pagesInventorynabihahNo ratings yet

- Intacc 1 Reviewer FinalsDocument13 pagesIntacc 1 Reviewer Finalscelynah.rheudeNo ratings yet

- BookkeepingDocument20 pagesBookkeepingzhanel bekenovaNo ratings yet

- Working Capital Project Report 1Document44 pagesWorking Capital Project Report 1Evelyn Keane100% (1)

- Incomplete Records QDocument34 pagesIncomplete Records Qcharliedry1920No ratings yet

- Jethro S. Cortado BSA 1B Goverment Grants and BorrowingDocument5 pagesJethro S. Cortado BSA 1B Goverment Grants and BorrowingJi Eun VinceNo ratings yet

- Users Guide For Peachtree Complete Accounting 2011Document17 pagesUsers Guide For Peachtree Complete Accounting 2011JalilQureshiNo ratings yet

- Lecture 5 - Books of Accounts and Double Entry SystemDocument7 pagesLecture 5 - Books of Accounts and Double Entry SystemmallarilecarNo ratings yet