ArogyaSanjeevani-PolicyDocument

ArogyaSanjeevani-PolicyDocument

You might also like

- List of Directors and Shareholding Pattern CertificateDocument1 pageList of Directors and Shareholding Pattern Certificateakhil kwatra50% (2)

- G&U S SetBU1Document74 pagesG&U S SetBU1Limos LmaNo ratings yet

- ReAssure - Policy - Document - PDF ... NEWDocument37 pagesReAssure - Policy - Document - PDF ... NEWPrasath NagendraNo ratings yet

- Bharti AXA Arogya SanjeevaniDocument37 pagesBharti AXA Arogya Sanjeevanirutiksankapal21No ratings yet

- Arogya Sanjeevani Policy Policy WordingsDocument13 pagesArogya Sanjeevani Policy Policy WordingsSunil HakhooNo ratings yet

- HASPSTD1 - Policy Clause - Arogya Sanjeevani Insurance Policy - V.11 - WebDocument11 pagesHASPSTD1 - Policy Clause - Arogya Sanjeevani Insurance Policy - V.11 - Webmani kumarNo ratings yet

- NB ReAssure Policy WordingDocument28 pagesNB ReAssure Policy WordingAmit Kumar KandiNo ratings yet

- Corona Kavach - PolicyDocument11 pagesCorona Kavach - PolicyvishalNo ratings yet

- Aditya Birla Health Insurance Co. LimitedDocument11 pagesAditya Birla Health Insurance Co. LimitedSouvik BanerjeeNo ratings yet

- Kotak Group Hospital Cash Policy Wording: DefinitionsDocument30 pagesKotak Group Hospital Cash Policy Wording: DefinitionsravitrainNo ratings yet

- Corona Cavach Policy WordingsDocument14 pagesCorona Cavach Policy WordingsRajesh SirsathNo ratings yet

- Terms Mediclaim PolicyDocument29 pagesTerms Mediclaim PolicyAmit KumarNo ratings yet

- PolicyWording 484343905Document28 pagesPolicyWording 484343905GovindNo ratings yet

- Individual Health Wordings 0Document25 pagesIndividual Health Wordings 0ZubairNo ratings yet

- Heal TR DingDocument30 pagesHeal TR DinggodhandaramankNo ratings yet

- Policy Wording GMC 2020Document24 pagesPolicy Wording GMC 2020Ashfaq MNo ratings yet

- Policy Wording GMC 2020Document24 pagesPolicy Wording GMC 2020puli sai kumarNo ratings yet

- SantoshDocument42 pagesSantoshsantoshkumarNo ratings yet

- PolicyWording 496933128Document36 pagesPolicyWording 496933128gajanan taydeNo ratings yet

- Health Companion Policy WordingDocument26 pagesHealth Companion Policy WordingRaj GopalNo ratings yet

- Zuno Arogya Sanjeevani Policy Wording V 1 0 b012523846Document27 pagesZuno Arogya Sanjeevani Policy Wording V 1 0 b012523846Aman PriyadarshiNo ratings yet

- Indianbank Policy WordingsDocument32 pagesIndianbank Policy WordingsRaja KatareNo ratings yet

- Health Advantedge - Apex Plus - Policy WordingsDocument36 pagesHealth Advantedge - Apex Plus - Policy Wordingssatishch27No ratings yet

- Nbhpaip22153v012122 Health2138Document30 pagesNbhpaip22153v012122 Health2138kiransfevNo ratings yet

- Standard ITGI GMC Policy WordingDocument8 pagesStandard ITGI GMC Policy WordingsrinivasNo ratings yet

- Goactive Policy DocumentDocument50 pagesGoactive Policy Documentwaran RMNo ratings yet

- Health Assurance Policy Wording - v13 - Revised With LogoDocument17 pagesHealth Assurance Policy Wording - v13 - Revised With LogolightNo ratings yet

- Activ Health Platinum Policy WordingDocument67 pagesActiv Health Platinum Policy WordingKetan Dot Iimahd BhattNo ratings yet

- Group Health Insurance (Revised) Policy WordingDocument48 pagesGroup Health Insurance (Revised) Policy WordingSakshi G AwasthiNo ratings yet

- Chihlip22047v012122 Health2082Document66 pagesChihlip22047v012122 Health2082Aarti A BhardwajNo ratings yet

- Aspire PWDocument30 pagesAspire PWBhavesh Santosh MhaskarNo ratings yet

- Health Companion Policy Document: 1. PreambleDocument30 pagesHealth Companion Policy Document: 1. PreambleBhadang BoysNo ratings yet

- New India Top-Up MediclaimDocument29 pagesNew India Top-Up MediclaimSathish ArumugamNo ratings yet

- Care Classic (Health Insurance Product) Policy Terms & ConditionsDocument38 pagesCare Classic (Health Insurance Product) Policy Terms & ConditionsyashmaheshwariNo ratings yet

- HBPolicy-WordingDocument66 pagesHBPolicy-WordingIdris SiddiquiNo ratings yet

- Arogya Sanjeevani Policy - Acko General Insurance LimitedDocument36 pagesArogya Sanjeevani Policy - Acko General Insurance LimitedSukesh SethiNo ratings yet

- Future - Generali - Health - Total - Prospectus - FGH - UW - RET - 86 - 02Document17 pagesFuture - Generali - Health - Total - Prospectus - FGH - UW - RET - 86 - 02Saurabh GuptaNo ratings yet

- National Parivar Mediclaim Plus Policy (Floater Policy) - 01.10.2021Document28 pagesNational Parivar Mediclaim Plus Policy (Floater Policy) - 01.10.2021Keerthivasan KpNo ratings yet

- Health Asure Clause Page 4Document1 pageHealth Asure Clause Page 4mvkulkarni5No ratings yet

- Policy ClauseDocument16 pagesPolicy Clauseyoga.crossfit.kickboxingNo ratings yet

- National Mediclaim Policy (NMP)Document19 pagesNational Mediclaim Policy (NMP)Joe ManuelNo ratings yet

- Star Comprehensive Policy Clause New 1Document15 pagesStar Comprehensive Policy Clause New 1sreejilmenon4724No ratings yet

- GyyrffDocument27 pagesGyyrffac2813460No ratings yet

- Care Supreme - Policy Terms and Conditions PDFDocument44 pagesCare Supreme - Policy Terms and Conditions PDFpraharshafciNo ratings yet

- ReAssure 2.0 - Policy WordingDocument24 pagesReAssure 2.0 - Policy WordingMohit VarmaNo ratings yet

- Health Infinity PW NewDocument34 pagesHealth Infinity PW Newsachaniya.prashantNo ratings yet

- Mediclaim Policy - Buy Group Health Insurance Online - Future GeneraliDocument39 pagesMediclaim Policy - Buy Group Health Insurance Online - Future GeneraliRizwan KhanNo ratings yet

- Arogya Plus Policy - 2014-2015Document25 pagesArogya Plus Policy - 2014-2015Noopur JaiswalNo ratings yet

- Group Medi Care 6c57b64356Document26 pagesGroup Medi Care 6c57b64356raghunandhan.cvNo ratings yet

- Arogya Sanjeevani Policy Navi General Insurance Limited - Policy Wordings - 0 RSy5b44Document37 pagesArogya Sanjeevani Policy Navi General Insurance Limited - Policy Wordings - 0 RSy5b44harivindNo ratings yet

- Policy Clause New India Mediclaim Policy (Wef 1st October 2021)Document34 pagesPolicy Clause New India Mediclaim Policy (Wef 1st October 2021)abcdefabcNo ratings yet

- Total Health Plan 5Document1 pageTotal Health Plan 5arajendermcomNo ratings yet

- Extra Care Plus Policy WordingsDocument23 pagesExtra Care Plus Policy Wordingsrakesh08nagarNo ratings yet

- Health PremiaDocument78 pagesHealth PremiaFarshid BokdawallaNo ratings yet

- TMB Uni Mahila Health Insurance: United India Insurance Company LimitedDocument66 pagesTMB Uni Mahila Health Insurance: United India Insurance Company LimitedSakshi G AwasthiNo ratings yet

- Super Top UpDocument22 pagesSuper Top UpYogesh ShahNo ratings yet

- ICICI TNCDocument65 pagesICICI TNCNidlok Style and Soiree Pvt. Ltd.No ratings yet

- Group Health Insurance PWDocument44 pagesGroup Health Insurance PWShivanikuldeep dubeyNo ratings yet

- Health Companion_Policy Document_Variant 2022 and 2023_V7Document23 pagesHealth Companion_Policy Document_Variant 2022 and 2023_V7wedefoh932No ratings yet

- Supertopup TNC May22Document17 pagesSupertopup TNC May22Aniket YadavNo ratings yet

- 83960group - Care - Kypb - (2016 - 11 - 05 17 - 12 - 11 Utc)Document13 pages83960group - Care - Kypb - (2016 - 11 - 05 17 - 12 - 11 Utc)Myntra NewNo ratings yet

- Silver HealthDocument32 pagesSilver HealthRakeshs MailmeNo ratings yet

- Antyodaya Shramik Suraksha Yojana Policy Wording (1)Document21 pagesAntyodaya Shramik Suraksha Yojana Policy Wording (1)akhil kwatraNo ratings yet

- 14 Nov Self Emp Data 2Document4 pages14 Nov Self Emp Data 2akhil kwatraNo ratings yet

- Janta Personal Accident Insurance Proposal FormDocument2 pagesJanta Personal Accident Insurance Proposal Formakhil kwatraNo ratings yet

- 14 Nov Prop DataDocument53 pages14 Nov Prop Dataakhil kwatraNo ratings yet

- DSR FormatDocument1 pageDSR Formatakhil kwatraNo ratings yet

- 14 Nov Self Emp Data 5Document10 pages14 Nov Self Emp Data 5akhil kwatraNo ratings yet

- 14 Nov Self Emp Data 3Document4 pages14 Nov Self Emp Data 3akhil kwatraNo ratings yet

- 14 Nov Self Emp Data 1Document4 pages14 Nov Self Emp Data 1akhil kwatraNo ratings yet

- 14 Nov Self Emp Data 1Document4 pages14 Nov Self Emp Data 1akhil kwatraNo ratings yet

- Statuses Finalized For DiallerDocument1 pageStatuses Finalized For Diallerakhil kwatraNo ratings yet

- ITR Compilation 4u5346Document4 pagesITR Compilation 4u5346akhil kwatraNo ratings yet

- Ministry of Corporate Affairs - MCA ServicesDocument1 pageMinistry of Corporate Affairs - MCA Servicesakhil kwatraNo ratings yet

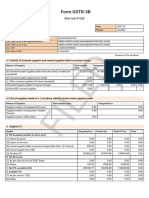

- GSTR3B 06aadcg4814c1z3 032022Document2 pagesGSTR3B 06aadcg4814c1z3 032022akhil kwatraNo ratings yet

- Balance SheetDocument16 pagesBalance Sheetakhil kwatraNo ratings yet

- Gurgaon Chamber OF COMMERCE MSMEDocument1 pageGurgaon Chamber OF COMMERCE MSMEakhil kwatraNo ratings yet

- Certificate of OriginizationDocument1 pageCertificate of Originizationakhil kwatraNo ratings yet

- KarnalDocument3 pagesKarnalakhil kwatraNo ratings yet

- Classifications in Child and Adolescent Psychiatry: Maria-Vittoria SquillanteDocument5 pagesClassifications in Child and Adolescent Psychiatry: Maria-Vittoria SquillanteTry Wahyudi Jeremi LoLyNo ratings yet

- Hydrogen Peroxide TherapyDocument17 pagesHydrogen Peroxide TherapyAmy MarlerNo ratings yet

- Nutrition PresDocument65 pagesNutrition PresJustin BergNo ratings yet

- Nursing Care With PenumoniaDocument44 pagesNursing Care With PenumoniaFahmi SyarifNo ratings yet

- Rad Rle Guide - Written Requirements Nicole Zschech C Leyson Section: Bsna9 Maternal Rle 1 Name Ofclinical Instructor: Gil Platon SorianoDocument21 pagesRad Rle Guide - Written Requirements Nicole Zschech C Leyson Section: Bsna9 Maternal Rle 1 Name Ofclinical Instructor: Gil Platon SorianoBrian Arthur LeysonNo ratings yet

- Premenstrual SyndromeDocument5 pagesPremenstrual SyndromeAan Pohan100% (1)

- Lecture Notes On Medical Nursing IiiDocument614 pagesLecture Notes On Medical Nursing IiiAnim Richard DuoduNo ratings yet

- PallitiveDocument10 pagesPallitiveapi-197110397No ratings yet

- Revision Unit 2: Health: Exercise 1: Odd One OutDocument3 pagesRevision Unit 2: Health: Exercise 1: Odd One OutNguyễn Minh AnhNo ratings yet

- Could It Be DiabetesDocument4 pagesCould It Be DiabetesElena IonescuNo ratings yet

- CHILD WITH AIH - Volk - Diagnosis and Management of Autoimmune Hepatitis in Adults and Children ADocument5 pagesCHILD WITH AIH - Volk - Diagnosis and Management of Autoimmune Hepatitis in Adults and Children AAsad KakarNo ratings yet

- Rheumatic Heart DiseaseDocument15 pagesRheumatic Heart DiseaseAica AnisNo ratings yet

- Your AnswersDocument9 pagesYour AnswersHuyền PhạmNo ratings yet

- Role of Open Surgical Drainage or Aspiration in Management of Amoebic Liver AbscessDocument9 pagesRole of Open Surgical Drainage or Aspiration in Management of Amoebic Liver AbscessIJAR JOURNALNo ratings yet

- Labor and Delivery MedicationsDocument10 pagesLabor and Delivery MedicationsLuis RiveraNo ratings yet

- "Ecstasy of St. Teresa": A. B. C. DDocument3 pages"Ecstasy of St. Teresa": A. B. C. DRalphNo ratings yet

- RenalDocument54 pagesRenalUSC Upstate Nursing Coaches100% (1)

- Stomach-Esophagus MedCosmos Surgery - MCQDocument39 pagesStomach-Esophagus MedCosmos Surgery - MCQMike G100% (1)

- Anxiety and Sports Performance in Young FemalesDocument11 pagesAnxiety and Sports Performance in Young FemalesGuille monsterNo ratings yet

- Drug StudyDocument11 pagesDrug StudyKaloy KamaoNo ratings yet

- 15 iMAGE BASED MCQSDocument9 pages15 iMAGE BASED MCQSonline mbbsNo ratings yet

- Marijuana Legalization (Copypasta Pastiche)Document4 pagesMarijuana Legalization (Copypasta Pastiche)LeEminenceGriseNo ratings yet

- GlyburideDocument3 pagesGlyburideapi-3797941No ratings yet

- Microbiology Research ProposalDocument20 pagesMicrobiology Research ProposalSalman KhanNo ratings yet

- PARKINSONDocument59 pagesPARKINSONvannyNo ratings yet

- Glomerulonephritis PDFDocument5 pagesGlomerulonephritis PDFmist73No ratings yet

- Pigeon and Dove Manual PDFDocument13 pagesPigeon and Dove Manual PDFMelpi Norawati Simarmata100% (1)

- LIBERTY's Basic Food HygieneDocument156 pagesLIBERTY's Basic Food Hygienestarlite100% (1)

- Final Exam in PE and Health 10Document1 pageFinal Exam in PE and Health 10Mary Grace Palis-MaulionNo ratings yet

Download as pdf or txt

You might also like

- List of Directors and Shareholding Pattern CertificateDocument1 pageList of Directors and Shareholding Pattern Certificateakhil kwatra50% (2)

- G&U S SetBU1Document74 pagesG&U S SetBU1Limos LmaNo ratings yet

- ReAssure - Policy - Document - PDF ... NEWDocument37 pagesReAssure - Policy - Document - PDF ... NEWPrasath NagendraNo ratings yet

- Bharti AXA Arogya SanjeevaniDocument37 pagesBharti AXA Arogya Sanjeevanirutiksankapal21No ratings yet

- Arogya Sanjeevani Policy Policy WordingsDocument13 pagesArogya Sanjeevani Policy Policy WordingsSunil HakhooNo ratings yet

- HASPSTD1 - Policy Clause - Arogya Sanjeevani Insurance Policy - V.11 - WebDocument11 pagesHASPSTD1 - Policy Clause - Arogya Sanjeevani Insurance Policy - V.11 - Webmani kumarNo ratings yet

- NB ReAssure Policy WordingDocument28 pagesNB ReAssure Policy WordingAmit Kumar KandiNo ratings yet

- Corona Kavach - PolicyDocument11 pagesCorona Kavach - PolicyvishalNo ratings yet

- Aditya Birla Health Insurance Co. LimitedDocument11 pagesAditya Birla Health Insurance Co. LimitedSouvik BanerjeeNo ratings yet

- Kotak Group Hospital Cash Policy Wording: DefinitionsDocument30 pagesKotak Group Hospital Cash Policy Wording: DefinitionsravitrainNo ratings yet

- Corona Cavach Policy WordingsDocument14 pagesCorona Cavach Policy WordingsRajesh SirsathNo ratings yet

- Terms Mediclaim PolicyDocument29 pagesTerms Mediclaim PolicyAmit KumarNo ratings yet

- PolicyWording 484343905Document28 pagesPolicyWording 484343905GovindNo ratings yet

- Individual Health Wordings 0Document25 pagesIndividual Health Wordings 0ZubairNo ratings yet

- Heal TR DingDocument30 pagesHeal TR DinggodhandaramankNo ratings yet

- Policy Wording GMC 2020Document24 pagesPolicy Wording GMC 2020Ashfaq MNo ratings yet

- Policy Wording GMC 2020Document24 pagesPolicy Wording GMC 2020puli sai kumarNo ratings yet

- SantoshDocument42 pagesSantoshsantoshkumarNo ratings yet

- PolicyWording 496933128Document36 pagesPolicyWording 496933128gajanan taydeNo ratings yet

- Health Companion Policy WordingDocument26 pagesHealth Companion Policy WordingRaj GopalNo ratings yet

- Zuno Arogya Sanjeevani Policy Wording V 1 0 b012523846Document27 pagesZuno Arogya Sanjeevani Policy Wording V 1 0 b012523846Aman PriyadarshiNo ratings yet

- Indianbank Policy WordingsDocument32 pagesIndianbank Policy WordingsRaja KatareNo ratings yet

- Health Advantedge - Apex Plus - Policy WordingsDocument36 pagesHealth Advantedge - Apex Plus - Policy Wordingssatishch27No ratings yet

- Nbhpaip22153v012122 Health2138Document30 pagesNbhpaip22153v012122 Health2138kiransfevNo ratings yet

- Standard ITGI GMC Policy WordingDocument8 pagesStandard ITGI GMC Policy WordingsrinivasNo ratings yet

- Goactive Policy DocumentDocument50 pagesGoactive Policy Documentwaran RMNo ratings yet

- Health Assurance Policy Wording - v13 - Revised With LogoDocument17 pagesHealth Assurance Policy Wording - v13 - Revised With LogolightNo ratings yet

- Activ Health Platinum Policy WordingDocument67 pagesActiv Health Platinum Policy WordingKetan Dot Iimahd BhattNo ratings yet

- Group Health Insurance (Revised) Policy WordingDocument48 pagesGroup Health Insurance (Revised) Policy WordingSakshi G AwasthiNo ratings yet

- Chihlip22047v012122 Health2082Document66 pagesChihlip22047v012122 Health2082Aarti A BhardwajNo ratings yet

- Aspire PWDocument30 pagesAspire PWBhavesh Santosh MhaskarNo ratings yet

- Health Companion Policy Document: 1. PreambleDocument30 pagesHealth Companion Policy Document: 1. PreambleBhadang BoysNo ratings yet

- New India Top-Up MediclaimDocument29 pagesNew India Top-Up MediclaimSathish ArumugamNo ratings yet

- Care Classic (Health Insurance Product) Policy Terms & ConditionsDocument38 pagesCare Classic (Health Insurance Product) Policy Terms & ConditionsyashmaheshwariNo ratings yet

- HBPolicy-WordingDocument66 pagesHBPolicy-WordingIdris SiddiquiNo ratings yet

- Arogya Sanjeevani Policy - Acko General Insurance LimitedDocument36 pagesArogya Sanjeevani Policy - Acko General Insurance LimitedSukesh SethiNo ratings yet

- Future - Generali - Health - Total - Prospectus - FGH - UW - RET - 86 - 02Document17 pagesFuture - Generali - Health - Total - Prospectus - FGH - UW - RET - 86 - 02Saurabh GuptaNo ratings yet

- National Parivar Mediclaim Plus Policy (Floater Policy) - 01.10.2021Document28 pagesNational Parivar Mediclaim Plus Policy (Floater Policy) - 01.10.2021Keerthivasan KpNo ratings yet

- Health Asure Clause Page 4Document1 pageHealth Asure Clause Page 4mvkulkarni5No ratings yet

- Policy ClauseDocument16 pagesPolicy Clauseyoga.crossfit.kickboxingNo ratings yet

- National Mediclaim Policy (NMP)Document19 pagesNational Mediclaim Policy (NMP)Joe ManuelNo ratings yet

- Star Comprehensive Policy Clause New 1Document15 pagesStar Comprehensive Policy Clause New 1sreejilmenon4724No ratings yet

- GyyrffDocument27 pagesGyyrffac2813460No ratings yet

- Care Supreme - Policy Terms and Conditions PDFDocument44 pagesCare Supreme - Policy Terms and Conditions PDFpraharshafciNo ratings yet

- ReAssure 2.0 - Policy WordingDocument24 pagesReAssure 2.0 - Policy WordingMohit VarmaNo ratings yet

- Health Infinity PW NewDocument34 pagesHealth Infinity PW Newsachaniya.prashantNo ratings yet

- Mediclaim Policy - Buy Group Health Insurance Online - Future GeneraliDocument39 pagesMediclaim Policy - Buy Group Health Insurance Online - Future GeneraliRizwan KhanNo ratings yet

- Arogya Plus Policy - 2014-2015Document25 pagesArogya Plus Policy - 2014-2015Noopur JaiswalNo ratings yet

- Group Medi Care 6c57b64356Document26 pagesGroup Medi Care 6c57b64356raghunandhan.cvNo ratings yet

- Arogya Sanjeevani Policy Navi General Insurance Limited - Policy Wordings - 0 RSy5b44Document37 pagesArogya Sanjeevani Policy Navi General Insurance Limited - Policy Wordings - 0 RSy5b44harivindNo ratings yet

- Policy Clause New India Mediclaim Policy (Wef 1st October 2021)Document34 pagesPolicy Clause New India Mediclaim Policy (Wef 1st October 2021)abcdefabcNo ratings yet

- Total Health Plan 5Document1 pageTotal Health Plan 5arajendermcomNo ratings yet

- Extra Care Plus Policy WordingsDocument23 pagesExtra Care Plus Policy Wordingsrakesh08nagarNo ratings yet

- Health PremiaDocument78 pagesHealth PremiaFarshid BokdawallaNo ratings yet

- TMB Uni Mahila Health Insurance: United India Insurance Company LimitedDocument66 pagesTMB Uni Mahila Health Insurance: United India Insurance Company LimitedSakshi G AwasthiNo ratings yet

- Super Top UpDocument22 pagesSuper Top UpYogesh ShahNo ratings yet

- ICICI TNCDocument65 pagesICICI TNCNidlok Style and Soiree Pvt. Ltd.No ratings yet

- Group Health Insurance PWDocument44 pagesGroup Health Insurance PWShivanikuldeep dubeyNo ratings yet

- Health Companion_Policy Document_Variant 2022 and 2023_V7Document23 pagesHealth Companion_Policy Document_Variant 2022 and 2023_V7wedefoh932No ratings yet

- Supertopup TNC May22Document17 pagesSupertopup TNC May22Aniket YadavNo ratings yet

- 83960group - Care - Kypb - (2016 - 11 - 05 17 - 12 - 11 Utc)Document13 pages83960group - Care - Kypb - (2016 - 11 - 05 17 - 12 - 11 Utc)Myntra NewNo ratings yet

- Silver HealthDocument32 pagesSilver HealthRakeshs MailmeNo ratings yet

- Antyodaya Shramik Suraksha Yojana Policy Wording (1)Document21 pagesAntyodaya Shramik Suraksha Yojana Policy Wording (1)akhil kwatraNo ratings yet

- 14 Nov Self Emp Data 2Document4 pages14 Nov Self Emp Data 2akhil kwatraNo ratings yet

- Janta Personal Accident Insurance Proposal FormDocument2 pagesJanta Personal Accident Insurance Proposal Formakhil kwatraNo ratings yet

- 14 Nov Prop DataDocument53 pages14 Nov Prop Dataakhil kwatraNo ratings yet

- DSR FormatDocument1 pageDSR Formatakhil kwatraNo ratings yet

- 14 Nov Self Emp Data 5Document10 pages14 Nov Self Emp Data 5akhil kwatraNo ratings yet

- 14 Nov Self Emp Data 3Document4 pages14 Nov Self Emp Data 3akhil kwatraNo ratings yet

- 14 Nov Self Emp Data 1Document4 pages14 Nov Self Emp Data 1akhil kwatraNo ratings yet

- 14 Nov Self Emp Data 1Document4 pages14 Nov Self Emp Data 1akhil kwatraNo ratings yet

- Statuses Finalized For DiallerDocument1 pageStatuses Finalized For Diallerakhil kwatraNo ratings yet

- ITR Compilation 4u5346Document4 pagesITR Compilation 4u5346akhil kwatraNo ratings yet

- Ministry of Corporate Affairs - MCA ServicesDocument1 pageMinistry of Corporate Affairs - MCA Servicesakhil kwatraNo ratings yet

- GSTR3B 06aadcg4814c1z3 032022Document2 pagesGSTR3B 06aadcg4814c1z3 032022akhil kwatraNo ratings yet

- Balance SheetDocument16 pagesBalance Sheetakhil kwatraNo ratings yet

- Gurgaon Chamber OF COMMERCE MSMEDocument1 pageGurgaon Chamber OF COMMERCE MSMEakhil kwatraNo ratings yet

- Certificate of OriginizationDocument1 pageCertificate of Originizationakhil kwatraNo ratings yet

- KarnalDocument3 pagesKarnalakhil kwatraNo ratings yet

- Classifications in Child and Adolescent Psychiatry: Maria-Vittoria SquillanteDocument5 pagesClassifications in Child and Adolescent Psychiatry: Maria-Vittoria SquillanteTry Wahyudi Jeremi LoLyNo ratings yet

- Hydrogen Peroxide TherapyDocument17 pagesHydrogen Peroxide TherapyAmy MarlerNo ratings yet

- Nutrition PresDocument65 pagesNutrition PresJustin BergNo ratings yet

- Nursing Care With PenumoniaDocument44 pagesNursing Care With PenumoniaFahmi SyarifNo ratings yet

- Rad Rle Guide - Written Requirements Nicole Zschech C Leyson Section: Bsna9 Maternal Rle 1 Name Ofclinical Instructor: Gil Platon SorianoDocument21 pagesRad Rle Guide - Written Requirements Nicole Zschech C Leyson Section: Bsna9 Maternal Rle 1 Name Ofclinical Instructor: Gil Platon SorianoBrian Arthur LeysonNo ratings yet

- Premenstrual SyndromeDocument5 pagesPremenstrual SyndromeAan Pohan100% (1)

- Lecture Notes On Medical Nursing IiiDocument614 pagesLecture Notes On Medical Nursing IiiAnim Richard DuoduNo ratings yet

- PallitiveDocument10 pagesPallitiveapi-197110397No ratings yet

- Revision Unit 2: Health: Exercise 1: Odd One OutDocument3 pagesRevision Unit 2: Health: Exercise 1: Odd One OutNguyễn Minh AnhNo ratings yet

- Could It Be DiabetesDocument4 pagesCould It Be DiabetesElena IonescuNo ratings yet

- CHILD WITH AIH - Volk - Diagnosis and Management of Autoimmune Hepatitis in Adults and Children ADocument5 pagesCHILD WITH AIH - Volk - Diagnosis and Management of Autoimmune Hepatitis in Adults and Children AAsad KakarNo ratings yet

- Rheumatic Heart DiseaseDocument15 pagesRheumatic Heart DiseaseAica AnisNo ratings yet

- Your AnswersDocument9 pagesYour AnswersHuyền PhạmNo ratings yet

- Role of Open Surgical Drainage or Aspiration in Management of Amoebic Liver AbscessDocument9 pagesRole of Open Surgical Drainage or Aspiration in Management of Amoebic Liver AbscessIJAR JOURNALNo ratings yet

- Labor and Delivery MedicationsDocument10 pagesLabor and Delivery MedicationsLuis RiveraNo ratings yet

- "Ecstasy of St. Teresa": A. B. C. DDocument3 pages"Ecstasy of St. Teresa": A. B. C. DRalphNo ratings yet

- RenalDocument54 pagesRenalUSC Upstate Nursing Coaches100% (1)

- Stomach-Esophagus MedCosmos Surgery - MCQDocument39 pagesStomach-Esophagus MedCosmos Surgery - MCQMike G100% (1)

- Anxiety and Sports Performance in Young FemalesDocument11 pagesAnxiety and Sports Performance in Young FemalesGuille monsterNo ratings yet

- Drug StudyDocument11 pagesDrug StudyKaloy KamaoNo ratings yet

- 15 iMAGE BASED MCQSDocument9 pages15 iMAGE BASED MCQSonline mbbsNo ratings yet

- Marijuana Legalization (Copypasta Pastiche)Document4 pagesMarijuana Legalization (Copypasta Pastiche)LeEminenceGriseNo ratings yet

- GlyburideDocument3 pagesGlyburideapi-3797941No ratings yet

- Microbiology Research ProposalDocument20 pagesMicrobiology Research ProposalSalman KhanNo ratings yet

- PARKINSONDocument59 pagesPARKINSONvannyNo ratings yet

- Glomerulonephritis PDFDocument5 pagesGlomerulonephritis PDFmist73No ratings yet

- Pigeon and Dove Manual PDFDocument13 pagesPigeon and Dove Manual PDFMelpi Norawati Simarmata100% (1)

- LIBERTY's Basic Food HygieneDocument156 pagesLIBERTY's Basic Food Hygienestarlite100% (1)

- Final Exam in PE and Health 10Document1 pageFinal Exam in PE and Health 10Mary Grace Palis-MaulionNo ratings yet