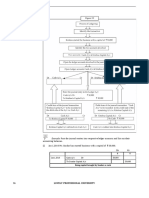

The Fall of Lehman Brothers

The Fall of Lehman Brothers

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5834)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (903)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (350)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (824)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (405)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- CHAPTER 34 - Biological Assets: Problem 34-1 (IFRS)Document13 pagesCHAPTER 34 - Biological Assets: Problem 34-1 (IFRS)Kimberly Claire Atienza100% (3)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Managerial Economics (Chapter 3)Document72 pagesManagerial Economics (Chapter 3)api-370372471% (14)

- Capital Market AssumptionsDocument19 pagesCapital Market AssumptionsKerim GokayNo ratings yet

- Service Marketing: Session: 9 & 10 Prof: Yasmin SDocument41 pagesService Marketing: Session: 9 & 10 Prof: Yasmin SmayurgharatNo ratings yet

- Chap 011Document18 pagesChap 011Xeniya Morozova Kurmayeva100% (9)

- Dec 2023 Financials UpdatedDocument102 pagesDec 2023 Financials Updatedpraveenramesh058No ratings yet

- Sample Marketing MCQ Part-1Document2 pagesSample Marketing MCQ Part-1KyuubiKittyNo ratings yet

- Under Armour's Case AnalysisDocument5 pagesUnder Armour's Case AnalysisericNo ratings yet

- IEB PresentationDocument11 pagesIEB PresentationKanika MaheshwariNo ratings yet

- Role That CA's Can Play in Growth of Indian EconomyDocument3 pagesRole That CA's Can Play in Growth of Indian EconomySwarna LathaNo ratings yet

- Federal Ministry of Labour and EmploymentDocument12 pagesFederal Ministry of Labour and EmploymentPhilip Ngbede OkawuNo ratings yet

- Case Map For Foundations of Finance, 7/eDocument2 pagesCase Map For Foundations of Finance, 7/eJoseph Schizmo100% (1)

- Janvi Bhatia 6th Sem BBA GenDocument43 pagesJanvi Bhatia 6th Sem BBA GenVishal GuptaNo ratings yet

- DimsonMarshStauntonarticle PDFDocument18 pagesDimsonMarshStauntonarticle PDFpneuma110100% (1)

- Amro Faisal ResumeDocument3 pagesAmro Faisal ResumeAmroNo ratings yet

- Chopra3 PPT ch02Document21 pagesChopra3 PPT ch02SatishNo ratings yet

- Experience: Territory Manager, BlackberryDocument3 pagesExperience: Territory Manager, BlackberryAshish LohaniNo ratings yet

- Part 1 - Acc - 2016Document10 pagesPart 1 - Acc - 2016Sheikh Mass JahNo ratings yet

- Case Analysis SAPDocument2 pagesCase Analysis SAPSandeep GangulyNo ratings yet

- Afm 5Document2 pagesAfm 5helpevery7No ratings yet

- Lap NeracaDocument2 pagesLap Neracasri riyantiNo ratings yet

- Advertising Is Defined As Any Paid Form of Nonpersonal Communication About AnDocument6 pagesAdvertising Is Defined As Any Paid Form of Nonpersonal Communication About AnBablu JamdarNo ratings yet

- Tutorial ACW 162 Chapter 3Document13 pagesTutorial ACW 162 Chapter 3raye brahmNo ratings yet

- Executive SummaryDocument38 pagesExecutive SummarySunshine Liwanag TrigueNo ratings yet

- CA Ipcc - Costing - May 2019 - Suggested AnswersDocument30 pagesCA Ipcc - Costing - May 2019 - Suggested Answerssainaraien2001No ratings yet

- Mco-06 Solved Assignment For Mcom: Like Our Facebook Page For UpdatesDocument14 pagesMco-06 Solved Assignment For Mcom: Like Our Facebook Page For UpdatesAjayNo ratings yet

- Project-Sebi Takeover CodeDocument50 pagesProject-Sebi Takeover CodeAbhishekJain75% (8)

- LPMPC Policies and Guidelines 2021Document26 pagesLPMPC Policies and Guidelines 2021Jugger Afrondoza100% (1)

- ASSIGNMENT DeepakDocument9 pagesASSIGNMENT DeepakHarsh AgarwalNo ratings yet

- Fa - 6 Amalgamation & LLPDocument10 pagesFa - 6 Amalgamation & LLPalokchowdhury111No ratings yet

Download as docx, pdf, or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5834)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (903)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (350)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (824)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (405)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- CHAPTER 34 - Biological Assets: Problem 34-1 (IFRS)Document13 pagesCHAPTER 34 - Biological Assets: Problem 34-1 (IFRS)Kimberly Claire Atienza100% (3)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Managerial Economics (Chapter 3)Document72 pagesManagerial Economics (Chapter 3)api-370372471% (14)

- Capital Market AssumptionsDocument19 pagesCapital Market AssumptionsKerim GokayNo ratings yet

- Service Marketing: Session: 9 & 10 Prof: Yasmin SDocument41 pagesService Marketing: Session: 9 & 10 Prof: Yasmin SmayurgharatNo ratings yet

- Chap 011Document18 pagesChap 011Xeniya Morozova Kurmayeva100% (9)

- Dec 2023 Financials UpdatedDocument102 pagesDec 2023 Financials Updatedpraveenramesh058No ratings yet

- Sample Marketing MCQ Part-1Document2 pagesSample Marketing MCQ Part-1KyuubiKittyNo ratings yet

- Under Armour's Case AnalysisDocument5 pagesUnder Armour's Case AnalysisericNo ratings yet

- IEB PresentationDocument11 pagesIEB PresentationKanika MaheshwariNo ratings yet

- Role That CA's Can Play in Growth of Indian EconomyDocument3 pagesRole That CA's Can Play in Growth of Indian EconomySwarna LathaNo ratings yet

- Federal Ministry of Labour and EmploymentDocument12 pagesFederal Ministry of Labour and EmploymentPhilip Ngbede OkawuNo ratings yet

- Case Map For Foundations of Finance, 7/eDocument2 pagesCase Map For Foundations of Finance, 7/eJoseph Schizmo100% (1)

- Janvi Bhatia 6th Sem BBA GenDocument43 pagesJanvi Bhatia 6th Sem BBA GenVishal GuptaNo ratings yet

- DimsonMarshStauntonarticle PDFDocument18 pagesDimsonMarshStauntonarticle PDFpneuma110100% (1)

- Amro Faisal ResumeDocument3 pagesAmro Faisal ResumeAmroNo ratings yet

- Chopra3 PPT ch02Document21 pagesChopra3 PPT ch02SatishNo ratings yet

- Experience: Territory Manager, BlackberryDocument3 pagesExperience: Territory Manager, BlackberryAshish LohaniNo ratings yet

- Part 1 - Acc - 2016Document10 pagesPart 1 - Acc - 2016Sheikh Mass JahNo ratings yet

- Case Analysis SAPDocument2 pagesCase Analysis SAPSandeep GangulyNo ratings yet

- Afm 5Document2 pagesAfm 5helpevery7No ratings yet

- Lap NeracaDocument2 pagesLap Neracasri riyantiNo ratings yet

- Advertising Is Defined As Any Paid Form of Nonpersonal Communication About AnDocument6 pagesAdvertising Is Defined As Any Paid Form of Nonpersonal Communication About AnBablu JamdarNo ratings yet

- Tutorial ACW 162 Chapter 3Document13 pagesTutorial ACW 162 Chapter 3raye brahmNo ratings yet

- Executive SummaryDocument38 pagesExecutive SummarySunshine Liwanag TrigueNo ratings yet

- CA Ipcc - Costing - May 2019 - Suggested AnswersDocument30 pagesCA Ipcc - Costing - May 2019 - Suggested Answerssainaraien2001No ratings yet

- Mco-06 Solved Assignment For Mcom: Like Our Facebook Page For UpdatesDocument14 pagesMco-06 Solved Assignment For Mcom: Like Our Facebook Page For UpdatesAjayNo ratings yet

- Project-Sebi Takeover CodeDocument50 pagesProject-Sebi Takeover CodeAbhishekJain75% (8)

- LPMPC Policies and Guidelines 2021Document26 pagesLPMPC Policies and Guidelines 2021Jugger Afrondoza100% (1)

- ASSIGNMENT DeepakDocument9 pagesASSIGNMENT DeepakHarsh AgarwalNo ratings yet

- Fa - 6 Amalgamation & LLPDocument10 pagesFa - 6 Amalgamation & LLPalokchowdhury111No ratings yet