Download as docx, pdf, or txt

You might also like

- CPA Review Notes 2019 - FAR (Financial Accounting and Reporting)From EverandCPA Review Notes 2019 - FAR (Financial Accounting and Reporting)Rating: 3.5 out of 5 stars3.5/5 (17)

- Buckwold 21e - CH 4 Selected SolutionsDocument18 pagesBuckwold 21e - CH 4 Selected SolutionsLucy50% (2)

- Employee Benefits 03Document11 pagesEmployee Benefits 03Nelva Quinio33% (3)

- CFA Level 2 FSADocument3 pagesCFA Level 2 FSA素直和夫No ratings yet

- MFRS 119 Employee BenefitsDocument38 pagesMFRS 119 Employee BenefitsAin YanieNo ratings yet

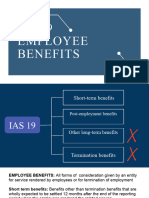

- IAS 19 - Employee BenefitsDocument1 pageIAS 19 - Employee BenefitsClarize R. MabiogNo ratings yet

- Chapter 6 Emplooyee Benefit Part 2Document8 pagesChapter 6 Emplooyee Benefit Part 2maria isabellaNo ratings yet

- Phuket Beach Hotel: Valuing Mutually Exclusive Capital ProjectsDocument23 pagesPhuket Beach Hotel: Valuing Mutually Exclusive Capital Projectsdarwin_butonNo ratings yet

- Class Case3 - Wake Up and Smell The CoffeeDocument24 pagesClass Case3 - Wake Up and Smell The CoffeeHannahPojaFeria0% (1)

- Pederson CPA Review FAR Notes PensionDocument8 pagesPederson CPA Review FAR Notes Pensionboen jaymeNo ratings yet

- Notes Chapter 6 FARDocument5 pagesNotes Chapter 6 FARcpacfa100% (6)

- Postemployment BenefitsDocument2 pagesPostemployment Benefitsbuenaflorgladys11No ratings yet

- FAR - Post-Employement Employee BenefitsDocument5 pagesFAR - Post-Employement Employee BenefitsJohn Mahatma Agripa100% (1)

- IFRS - IAS19 - Employee BenefitsDocument16 pagesIFRS - IAS19 - Employee BenefitsFendy YamiNo ratings yet

- IFRS - IAS19 - Employee BenefitsDocument16 pagesIFRS - IAS19 - Employee BenefitsPramita RoyNo ratings yet

- MODULE Midterm FAR 3 EmpBenefitsDocument15 pagesMODULE Midterm FAR 3 EmpBenefitsJohn Mark FernandoNo ratings yet

- Analysis of Finanacing ActivitiesDocument48 pagesAnalysis of Finanacing ActivitiesPrateek SinglaNo ratings yet

- Unit 7 E-Tutor PresentationDocument18 pagesUnit 7 E-Tutor PresentationKatrina EustaceNo ratings yet

- MODULE Midterm FAR 3 EmpBenefitsDocument15 pagesMODULE Midterm FAR 3 EmpBenefitsKezNo ratings yet

- Employee Benefit PlanDocument8 pagesEmployee Benefit PlantinydmpNo ratings yet

- 1FU491 Employee BenefitsDocument14 pages1FU491 Employee BenefitsEmil DavtyanNo ratings yet

- Employee BenefitsDocument9 pagesEmployee BenefitstinydmpNo ratings yet

- Employee BenefitsDocument9 pagesEmployee BenefitstinydmpNo ratings yet

- Cfas Pas 19Document4 pagesCfas Pas 19Zyribelle Anne JAPSONNo ratings yet

- FARAP-4413 (Post-Employment Benefits)Document5 pagesFARAP-4413 (Post-Employment Benefits)Dizon Ropalito P.No ratings yet

- Employee BenefitsDocument7 pagesEmployee BenefitsJANN HANNAH FAITH CRUTANo ratings yet

- Slide Chapter 3 Analyzing Financing ActivitiesDocument40 pagesSlide Chapter 3 Analyzing Financing ActivitiesardhikasatriaNo ratings yet

- CH20 PDFDocument81 pagesCH20 PDFelaine aureliaNo ratings yet

- Post Employment BenefitsDocument31 pagesPost Employment BenefitsSky SoronoiNo ratings yet

- Employee Benefits Ias19Document42 pagesEmployee Benefits Ias19krishnaguptaNo ratings yet

- IAS 19 Employee Benefits StudentDocument40 pagesIAS 19 Employee Benefits StudentYI WEI CHANGNo ratings yet

- Chapter 17Document11 pagesChapter 17Daniel BalchaNo ratings yet

- Pas 19Document5 pagesPas 19elle friasNo ratings yet

- FARAP-4513 (Post-Employment Benefits)Document5 pagesFARAP-4513 (Post-Employment Benefits)Rinoah Mae OlorosoNo ratings yet

- Frs 119 Employee BenefitDocument54 pagesFrs 119 Employee BenefitNahar SabirahNo ratings yet

- Chapter 03 Analyzing Financing ActivitiesDocument40 pagesChapter 03 Analyzing Financing Activitiesshabrina rNo ratings yet

- SBR - Chapter 5Document6 pagesSBR - Chapter 5Jason KumarNo ratings yet

- Chapter 14 - Post Employment BenefitsDocument4 pagesChapter 14 - Post Employment Benefitslooter198No ratings yet

- Taxation Chapter 4Document8 pagesTaxation Chapter 4Rica CoNo ratings yet

- Defined Benefit Pension PlanDocument2 pagesDefined Benefit Pension PlanAyesha IqbalNo ratings yet

- Dependents or Insurance Companies.: Sharing, Paid Annual Leave, Paid Sick Leave, Non Monetary Benefits)Document3 pagesDependents or Insurance Companies.: Sharing, Paid Annual Leave, Paid Sick Leave, Non Monetary Benefits)Niranjan JainNo ratings yet

- Ia ReportDocument1 pageIa Reportmaubrick khianNo ratings yet

- 29 Ias 19 Employee BenefitsDocument14 pages29 Ias 19 Employee BenefitsSuryaNo ratings yet

- Postemployment BenefitsDocument22 pagesPostemployment BenefitsChoco ButternutNo ratings yet

- Pre Review 1 SEM S.Y. 2011-2012 Practical Accounting 1 / Theory of AccountsDocument11 pagesPre Review 1 SEM S.Y. 2011-2012 Practical Accounting 1 / Theory of AccountsKristine JarinaNo ratings yet

- Reading 14 - Employee Compensation: Post Employment and Share-BasedDocument6 pagesReading 14 - Employee Compensation: Post Employment and Share-BasedJuan MatiasNo ratings yet

- Liabilities - Debt RestructuringDocument4 pagesLiabilities - Debt RestructuringChinchin Ilagan DatayloNo ratings yet

- Ias 19 Employee BenefitsDocument43 pagesIas 19 Employee BenefitsHasan Ali BokhariNo ratings yet

- Employee Benefits: Retirement PlansDocument28 pagesEmployee Benefits: Retirement Plansbose3508No ratings yet

- REVISION Retirement BenefitsDocument23 pagesREVISION Retirement BenefitsREGINo ratings yet

- IAS 19 Employee BenefitsDocument22 pagesIAS 19 Employee Benefitsanon_419651076No ratings yet

- Contribut Ions To Pension and TrustsDocument3 pagesContribut Ions To Pension and TrustsMiracle GraceNo ratings yet

- IAS 19 Employee BenefitsDocument32 pagesIAS 19 Employee BenefitsTamirat Eshetu WoldeNo ratings yet

- Gross Income Regular Tax: MARCH 2019Document57 pagesGross Income Regular Tax: MARCH 2019tyineNo ratings yet

- Ias 19Document9 pagesIas 19Hammad SarwarNo ratings yet

- Ias 19-Employee BenefitsDocument3 pagesIas 19-Employee Benefitsbeth alviolaNo ratings yet

- Week 1-3Document26 pagesWeek 1-3Aliah OdinNo ratings yet

- IAS 19 - Employee BenefitDocument49 pagesIAS 19 - Employee BenefitShah Kamal100% (2)

- LKAS 19 2021 UploadDocument31 pagesLKAS 19 2021 Uploadpriyantha dasanayake100% (2)

- Accounting For Employee BenefitsDocument2 pagesAccounting For Employee BenefitshoneyNo ratings yet

- Dynamic Risk Assessment Template - SafetyCultureDocument4 pagesDynamic Risk Assessment Template - SafetyCulturebarrfranciscoNo ratings yet

- S 37 L 0Document23 pagesS 37 L 0anon-475496No ratings yet

- 04 Republic v. PNBDocument5 pages04 Republic v. PNBCharles MagistradoNo ratings yet

- Research Paper On Working Capital Management in IndiaDocument4 pagesResearch Paper On Working Capital Management in Indiagepuz0gohew2No ratings yet

- Percentages: Multiple-Choice QuestionsDocument4 pagesPercentages: Multiple-Choice QuestionsJason Lam Lam100% (1)

- Chapter 1 The Accountancy ProfessionDocument7 pagesChapter 1 The Accountancy ProfessionJoshua Sapphire AmonNo ratings yet

- IIMA Ph.D. Prog. Brochure 2022-23Document87 pagesIIMA Ph.D. Prog. Brochure 2022-23Amritesh RayNo ratings yet

- Workfile - ZCDocument25 pagesWorkfile - ZCirshadpp999iNo ratings yet

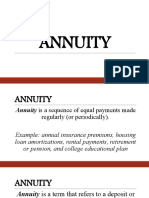

- AnnuityDocument46 pagesAnnuityJeffreyMitra100% (2)

- Hotel Franchising in Europe The Push Continues For New Ways To Expand 9Document1 pageHotel Franchising in Europe The Push Continues For New Ways To Expand 9wloghuntNo ratings yet

- Blue Print,.... Accunting & FinanceDocument21 pagesBlue Print,.... Accunting & FinanceRobel Addis100% (9)

- Luxury in France Mazars Survey 2014 25092014 PDFDocument56 pagesLuxury in France Mazars Survey 2014 25092014 PDFfaizan iqbalNo ratings yet

- Instructions For Completing Form 4506-C (Individial Taxpayer)Document1 pageInstructions For Completing Form 4506-C (Individial Taxpayer)GlendaNo ratings yet

- Chapter 06 - Merchandising ActivitiesDocument114 pagesChapter 06 - Merchandising ActivitiesElio BazNo ratings yet

- Midterm L3L4Document2 pagesMidterm L3L4Nicole LukNo ratings yet

- Alternative Capital Sources For Social EnterprisesDocument12 pagesAlternative Capital Sources For Social EnterprisesADBSocialDevelopmentNo ratings yet

- Bretton Wood SystemDocument17 pagesBretton Wood SystemUmesh Gaikwad0% (1)

- Retained Earnings: Appropriation and Quasi-ReorganizationDocument25 pagesRetained Earnings: Appropriation and Quasi-ReorganizationtruthNo ratings yet

- Extinguishment of Obligations: General ProvisionsDocument72 pagesExtinguishment of Obligations: General ProvisionsSergio ConjugalNo ratings yet

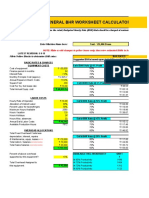

- General BHR Worksheet CalculatorDocument2 pagesGeneral BHR Worksheet CalculatorEmba MadrasNo ratings yet

- 2008 L2 Mock01 - QDocument46 pages2008 L2 Mock01 - QRavi RanjanNo ratings yet

- Madhucon Projects Result UpdatedDocument14 pagesMadhucon Projects Result UpdatedAngel BrokingNo ratings yet

- Cryptocurrency - A New Investment OpportunityDocument26 pagesCryptocurrency - A New Investment OpportunityMohd. Anisul IslamNo ratings yet

- Wei Peng Handbook-of-quantitative-finance-and-risk-management-2010-Chap 92Document17 pagesWei Peng Handbook-of-quantitative-finance-and-risk-management-2010-Chap 9220222991No ratings yet

- Unicorn ValuationDocument12 pagesUnicorn ValuationTony TranNo ratings yet

- Proabg Project Financial FreedomDocument32 pagesProabg Project Financial FreedomUttam Manas100% (1)

- Automation, Manual & Computerised AccountingDocument16 pagesAutomation, Manual & Computerised AccountingAayush AnandNo ratings yet

- Asian Life InsDocument34 pagesAsian Life InsLaxman Thapa100% (1)