Download as pdf or txt

You might also like

- CH 15 Mini CaseDocument16 pagesCH 15 Mini CaseMahmud Mostakim TakrimNo ratings yet

- 2022-2023 Price Action Trading Guide for Beginners in 45 MinutesFrom Everand2022-2023 Price Action Trading Guide for Beginners in 45 MinutesRating: 4.5 out of 5 stars4.5/5 (4)

- Pecchiari MatteoDocument79 pagesPecchiari MatteoSteven Josue ANo ratings yet

- THE TRADING EMPIRE cr7 22Document29 pagesTHE TRADING EMPIRE cr7 22ASDFNo ratings yet

- The (Questionable) Legality of High-Speed "Pinging" and "Front Running" in The Futures MarketsDocument92 pagesThe (Questionable) Legality of High-Speed "Pinging" and "Front Running" in The Futures Marketslanassa2785No ratings yet

- Algo Trading Intro 2013 Steinki Session 8 PDFDocument21 pagesAlgo Trading Intro 2013 Steinki Session 8 PDFProfitiserNo ratings yet

- Crypto GuideDocument47 pagesCrypto GuideShah MuradNo ratings yet

- Trading Related QuestionsDocument10 pagesTrading Related QuestionsttrajaanNo ratings yet

- PureDMA Manual IgmDocument12 pagesPureDMA Manual IgmMichelle RobertsNo ratings yet

- Understanding Order ProcessDocument7 pagesUnderstanding Order ProcessfilipNo ratings yet

- High Frequency Trading: Price Dynamics Models and Market Making StrategiesDocument40 pagesHigh Frequency Trading: Price Dynamics Models and Market Making StrategiesSeyyed Mohammad Hossein SherafatNo ratings yet

- Inverse and Quanto Inverse Options in A Black-Scholes WorldDocument36 pagesInverse and Quanto Inverse Options in A Black-Scholes WorldJulien KuntzNo ratings yet

- HFT SchrodersDocument7 pagesHFT SchrodersalypatyNo ratings yet

- Proficient FXDocument8 pagesProficient FXTaylorNo ratings yet

- Zahar Udin PHD ThesisDocument201 pagesZahar Udin PHD ThesisSunny ChaturvediNo ratings yet

- Overnight Returns and The Hidden Cost of Buying at The OpenDocument28 pagesOvernight Returns and The Hidden Cost of Buying at The OpenFábio RigoniNo ratings yet

- NinjaTrader FXCM Connection Guide - NinjaTraderDocument1 pageNinjaTrader FXCM Connection Guide - NinjaTraderShahbaz SyedNo ratings yet

- Derivatives - Futures vs. Forwards: Characteristics of Futures ContractsDocument5 pagesDerivatives - Futures vs. Forwards: Characteristics of Futures ContractsSam JamtshoNo ratings yet

- ITG Trading Around The Close 11-7-2012Document11 pagesITG Trading Around The Close 11-7-2012ej129No ratings yet

- Zero Hold Time - FAQs PDFDocument4 pagesZero Hold Time - FAQs PDFJorge LuisNo ratings yet

- Trading and SettlementDocument12 pagesTrading and SettlementLakhan KodiyatarNo ratings yet

- "Arbitrage" in Foreign Exchange MarketDocument1 page"Arbitrage" in Foreign Exchange MarketKajal ChaudharyNo ratings yet

- Orderflow AbstractDocument2 pagesOrderflow AbstractpostscriptNo ratings yet

- 2.adjustments For FasterThinnerVolatile MarketsDocument5 pages2.adjustments For FasterThinnerVolatile MarketsSajeebChandraNo ratings yet

- Trading Strategies of Institutional Investors in ADocument4 pagesTrading Strategies of Institutional Investors in AJames OkramNo ratings yet

- Blindly: Its Time To Adopt Smartest Technology Tool 91 99790 66966Document6 pagesBlindly: Its Time To Adopt Smartest Technology Tool 91 99790 66966Varun VasurendranNo ratings yet

- Optimal Strategies of High Frequency Traders SSRN-id2382378Document50 pagesOptimal Strategies of High Frequency Traders SSRN-id2382378Cristian Huanca QuisbertNo ratings yet

- Limit Orders, Depth, and VolatilityDocument39 pagesLimit Orders, Depth, and VolatilitySamuel Martini CasagrandeNo ratings yet

- G5-T5 How To Use The Stochastic IndicatorDocument4 pagesG5-T5 How To Use The Stochastic IndicatorThe ShitNo ratings yet

- What Is Spread Betting (Good) PDFDocument4 pagesWhat Is Spread Betting (Good) PDFMyriam GrissaNo ratings yet

- Fox Wave by Ahmed MaherDocument20 pagesFox Wave by Ahmed MaherPranav IweNo ratings yet

- Limit Order BookDocument48 pagesLimit Order BookSyroes NouromidNo ratings yet

- Trading VolumeDocument67 pagesTrading VolumedanangsecurityNo ratings yet

- Information Theory and Market BehaviorDocument25 pagesInformation Theory and Market BehaviorAbhinavJainNo ratings yet

- Survivor SetupsDocument12 pagesSurvivor Setupsjnk987No ratings yet

- Fibonacci Retracement and DivergenceDocument6 pagesFibonacci Retracement and DivergenceUprising TopicsNo ratings yet

- What Is Open InterestDocument6 pagesWhat Is Open InterestDeepak Damani0% (1)

- Liquidity Grab With Support & Resistance IndicatorDocument6 pagesLiquidity Grab With Support & Resistance Indicatorst augusNo ratings yet

- SecuritisationDocument28 pagesSecuritisationChinmayee ChoudhuryNo ratings yet

- NQoos Floor Trader 918Document6 pagesNQoos Floor Trader 918bagoesNo ratings yet

- An Empirical Analysis of The Limit Order Book and The Order Flow in The Paris BourseDocument36 pagesAn Empirical Analysis of The Limit Order Book and The Order Flow in The Paris BourseYuxiang WuNo ratings yet

- Tradingfxhub Com Blog How To Identify Supply and Demand CurveDocument15 pagesTradingfxhub Com Blog How To Identify Supply and Demand CurveKrunal Parab0% (1)

- IOF - Standard DevDocument15 pagesIOF - Standard DevOtsile Charisma Otsile SaqNo ratings yet

- Tradingfxhub Com Blog How To Trade Supply and Demand Using CciDocument12 pagesTradingfxhub Com Blog How To Trade Supply and Demand Using CciKrunal ParabNo ratings yet

- Trading Strategies. PDF. (HULL) PDFDocument15 pagesTrading Strategies. PDF. (HULL) PDFMuskan AroraNo ratings yet

- TM ManualDocument15 pagesTM Manualboatran8No ratings yet

- HighFrequencyMarketMaking PreviewDocument72 pagesHighFrequencyMarketMaking PreviewIrfan Sihab100% (1)

- ArbitrageDocument2 pagesArbitrageajaydayaNo ratings yet

- Forex Ict Amp MMM Notespdf - Compress - 1 PDFDocument109 pagesForex Ict Amp MMM Notespdf - Compress - 1 PDFjean louNo ratings yet

- Trading 101 BasicsDocument3 pagesTrading 101 BasicsNaveen KumarNo ratings yet

- Getting Your Charts Ready Printer FriendlyDocument13 pagesGetting Your Charts Ready Printer FriendlyHobbes556No ratings yet

- Seminar Report - Algorithmic TradingDocument32 pagesSeminar Report - Algorithmic TradingHarshal LolgeNo ratings yet

- Adversity Is Often The Mother of Innovation: by Tom J. ReavisDocument72 pagesAdversity Is Often The Mother of Innovation: by Tom J. ReavisŞamil CeyhanNo ratings yet

- Research Smart MoneyDocument50 pagesResearch Smart MoneyZeitun Noor100% (1)

- Top Three Triggers To Identify Front-Running: Do You Know Who Is Trading Ahead of You?Document5 pagesTop Three Triggers To Identify Front-Running: Do You Know Who Is Trading Ahead of You?j3585873No ratings yet

- Introduction To Derivatives: Nse Academy CertifiedDocument55 pagesIntroduction To Derivatives: Nse Academy CertifiedSrividhya RaghavanNo ratings yet

- Limit Order Books: Ren e CarmonaDocument38 pagesLimit Order Books: Ren e Carmonadheeraj8rNo ratings yet

- What Does Open Interest in Stock Market IndicateDocument3 pagesWhat Does Open Interest in Stock Market IndicateAneeshAntony100% (1)

- Risk Management Through Forex Derivatives: Presented ByDocument31 pagesRisk Management Through Forex Derivatives: Presented ByRoma ManwaniNo ratings yet

- Limit Order Book Model For Latency ArbitrageDocument28 pagesLimit Order Book Model For Latency ArbitrageJong-Kwon LeeNo ratings yet

- Bidding Principles: Programme TradingDocument6 pagesBidding Principles: Programme TradingmshchetkNo ratings yet

- Comparative AdvertisingDocument3 pagesComparative Advertisingdnrwn0% (1)

- Berks Broadcasting Co V CraumerDocument1 pageBerks Broadcasting Co V Craumervmanalo16No ratings yet

- Economics Firm Analysis 7-11Document16 pagesEconomics Firm Analysis 7-11Julius Miguel PeñamanteNo ratings yet

- PPE Plus Depn1Document3 pagesPPE Plus Depn1Sheena GutierrezNo ratings yet

- The Barth Report: H O P S 2 0 1 5 / 2 0 1 6Document32 pagesThe Barth Report: H O P S 2 0 1 5 / 2 0 1 6Daniel TossNo ratings yet

- Toyota RecallDocument2 pagesToyota RecallJohnChoiNo ratings yet

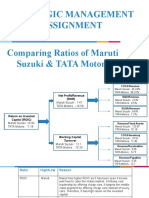

- Strategic Management Assignment Comparing Ratios of Maruti Suzuki & TATA MotorsDocument4 pagesStrategic Management Assignment Comparing Ratios of Maruti Suzuki & TATA MotorsNamanNo ratings yet

- Plastic Industry Project ReportDocument6 pagesPlastic Industry Project Reportloveaute15100% (1)

- Types of DistributorsDocument6 pagesTypes of DistributorsRosHan AwanNo ratings yet

- ChipotleDocument22 pagesChipotleChen JinghanNo ratings yet

- Valuation For M&a Parag Ved MumbaiDocument22 pagesValuation For M&a Parag Ved MumbaiRavikumar KurnalNo ratings yet

- CH 11 - CF Estimation Mini Case Sols Excel 14edDocument36 pagesCH 11 - CF Estimation Mini Case Sols Excel 14edأثير مخوNo ratings yet

- PMP Notes From Andy CroweDocument21 pagesPMP Notes From Andy CroweRobincrusoe100% (4)

- Interest Bearing Non Interest Bearing Notes HandoutsDocument4 pagesInterest Bearing Non Interest Bearing Notes HandoutsAliezaNo ratings yet

- Water WorksDocument161 pagesWater WorksJustus OtungaNo ratings yet

- Regulatory Purpose: Non-Revenue/ Special or RegulatoryDocument6 pagesRegulatory Purpose: Non-Revenue/ Special or Regulatorykristel jane caldozaNo ratings yet

- HUL CasestudyDocument15 pagesHUL CasestudyBecky PaulNo ratings yet

- Macroeconomics-Lecture Slides PDFDocument142 pagesMacroeconomics-Lecture Slides PDFAbhishekNo ratings yet

- ECON3310 Unit Outline FinalDocument17 pagesECON3310 Unit Outline FinalmasithreadNo ratings yet

- Development of A Competitive Air-Transport Market in Vietnam: Issues and Experience For Countries in TransitionDocument13 pagesDevelopment of A Competitive Air-Transport Market in Vietnam: Issues and Experience For Countries in TransitionNgọc QuỳnhNo ratings yet

- Customer Satisfaction ResearchDocument11 pagesCustomer Satisfaction Researchseetha100% (2)

- Business Proposal Private Oye-Mba 1Document6 pagesBusiness Proposal Private Oye-Mba 1api-640303670No ratings yet

- Maruti Suzuki India Balance Sheet, Maruti Suzuki India Financial Statement & AccountsDocument3 pagesMaruti Suzuki India Balance Sheet, Maruti Suzuki India Financial Statement & Accountsankur51No ratings yet

- Final Account VijDocument60 pagesFinal Account Vijamity_acel100% (1)

- Semira - Kuku - Mba 502-3-2 Final Project.Document3 pagesSemira - Kuku - Mba 502-3-2 Final Project.Eric WogbeNo ratings yet

- CapitalBudgeting WACCDocument3 pagesCapitalBudgeting WACCRahul SharmaNo ratings yet

- Case Presentation PART 2+PART 3Document3 pagesCase Presentation PART 2+PART 3jackywen1024No ratings yet

- Knowledge Session: ArthashastraDocument27 pagesKnowledge Session: ArthashastraRomali DasNo ratings yet

- AA025 Chapter AT8Document3 pagesAA025 Chapter AT8norismah isaNo ratings yet