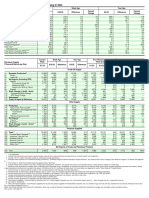

Coal Outlook

Coal Outlook

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5820)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (845)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (898)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- ICT Mentorship Month 1 NotesDocument32 pagesICT Mentorship Month 1 NotesJoe Ledesma94% (99)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- I CT Material ReferenceDocument96 pagesI CT Material Referencefsolomon100% (20)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Financial System and The Economy - Éric Tymoigne PDFDocument258 pagesThe Financial System and The Economy - Éric Tymoigne PDFAfonso d'EcclesiisNo ratings yet

- OTE FreemodelDocument20 pagesOTE Freemodelvadavada96% (24)

- ETF Metals Prospectus-MergedDocument306 pagesETF Metals Prospectus-MergedJames Staines100% (1)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Facts and Fantasies About Commodity Futures Ten Years LaterDocument31 pagesFacts and Fantasies About Commodity Futures Ten Years LaterSoren K. GroupNo ratings yet

- WHP Fine and Specialty Chemicals 154169Document8 pagesWHP Fine and Specialty Chemicals 154169sanjayshah99No ratings yet

- Company ProfileDocument5 pagesCompany Profilesanjayshah99No ratings yet

- Sector Analysis: Chemical IndustryDocument28 pagesSector Analysis: Chemical Industrysanjayshah99No ratings yet

- OverviewDocument8 pagesOverviewsanjayshah99No ratings yet

- Chemical Business Focus: A Monthly Roundup and Analysis of The Key Factors Shaping World Chemical MarketsDocument27 pagesChemical Business Focus: A Monthly Roundup and Analysis of The Key Factors Shaping World Chemical Marketssanjayshah99No ratings yet

- Canada PlasticDocument47 pagesCanada Plasticsanjayshah99No ratings yet

- WEO2017 Launch BrusselsDocument14 pagesWEO2017 Launch Brusselssanjayshah99No ratings yet

- GCO - Pillar I - Trends and IndicatorsDocument92 pagesGCO - Pillar I - Trends and Indicatorssanjayshah99No ratings yet

- Downstream Petroleum Sector and Fuel Quality: The Quality of Transport FuelsDocument7 pagesDownstream Petroleum Sector and Fuel Quality: The Quality of Transport Fuelssanjayshah99No ratings yet

- EthanolDocument2 pagesEthanolsanjayshah99No ratings yet

- EthanolDocument2 pagesEthanolsanjayshah99No ratings yet

- Coal Chemical - SampleDocument39 pagesCoal Chemical - Samplesanjayshah99No ratings yet

- Sec Usa 2010Document172 pagesSec Usa 2010MicsomsNo ratings yet

- Currency Trader Magazine (08-2006) (Finance Forex Trading Review Analysis Commentary)Document46 pagesCurrency Trader Magazine (08-2006) (Finance Forex Trading Review Analysis Commentary)TradingSystemNo ratings yet

- Chuck ConnerDocument2 pagesChuck ConnerMarketsWikiNo ratings yet

- Orbis InstitutionalDocument61 pagesOrbis Institutionalsaharsh narangNo ratings yet

- Anti-Money Laundering Regulation of Cryptocurrency: U.S. and Global ApproachesDocument14 pagesAnti-Money Laundering Regulation of Cryptocurrency: U.S. and Global ApproachesFiorella VásquezNo ratings yet

- OCR Portal Client Quick Start Guide 7.12.2021Document17 pagesOCR Portal Client Quick Start Guide 7.12.2021jangbaangNo ratings yet

- Regulation of The Securities MarketDocument24 pagesRegulation of The Securities Marketlegalmatters100% (5)

- The Gold Market-OutlineDocument5 pagesThe Gold Market-OutlineMartin SeruggaNo ratings yet

- 1Document38 pages1Jonathan GrevhallNo ratings yet

- Commitment of Traders ReportDocument14 pagesCommitment of Traders ReportZerohedgeNo ratings yet

- Richard Dennis Sonterra Capital Vs Cba Nab Anz Macquarie Gov - Uscourts.nysd.461685.1.0-1Document87 pagesRichard Dennis Sonterra Capital Vs Cba Nab Anz Macquarie Gov - Uscourts.nysd.461685.1.0-1Maverick MinitriesNo ratings yet

- Hedge Funds. A Basic OverviewDocument41 pagesHedge Funds. A Basic OverviewBilal MalikNo ratings yet

- OTC Derivatives - Product History and Regulation (9-09)Document87 pagesOTC Derivatives - Product History and Regulation (9-09)Manish AnandNo ratings yet

- Hearings: Reauthorizing The Commodity Futures Trading CommissionDocument215 pagesHearings: Reauthorizing The Commodity Futures Trading CommissionScribd Government DocsNo ratings yet

- How To Succeed As A Sell Side Trader: Brent DonnellyDocument9 pagesHow To Succeed As A Sell Side Trader: Brent DonnellyAlvinNo ratings yet

- Improving Energy Market Regulation: Domestic and International IssuesDocument20 pagesImproving Energy Market Regulation: Domestic and International IssuesFransiska Ardie YantiNo ratings yet

- An Excerpt From A Human's Guide To Machine IntelligenceDocument10 pagesAn Excerpt From A Human's Guide To Machine Intelligencewamu885No ratings yet

- DDFX FOREX TRADING SYSTEM v4 PDFDocument15 pagesDDFX FOREX TRADING SYSTEM v4 PDFstrettt100% (1)

- LedgerX Amended Order 09-02-2020 SignedDocument4 pagesLedgerX Amended Order 09-02-2020 SignedMichaelPatrickMcSweeneyNo ratings yet

- BJSS Case Study - Regulatory Compliance v1.0 (US)Document8 pagesBJSS Case Study - Regulatory Compliance v1.0 (US)tabbforumNo ratings yet

- TheEconomist 2023 04 01Document297 pagesTheEconomist 2023 04 01Sh FNo ratings yet

- The Growth of Cryptocurrency in India: Its Challenges & Potential Impacts On LegislationDocument23 pagesThe Growth of Cryptocurrency in India: Its Challenges & Potential Impacts On LegislationHiren WaghelaNo ratings yet

- Moskowitz Time Series Momentum PaperDocument23 pagesMoskowitz Time Series Momentum PaperthyagosmesmeNo ratings yet

- Hayes Sentencing LetterDocument65 pagesHayes Sentencing LetterMichaelPatrickMcSweeneyNo ratings yet

Download as pdf or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5820)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (845)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (898)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- ICT Mentorship Month 1 NotesDocument32 pagesICT Mentorship Month 1 NotesJoe Ledesma94% (99)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- I CT Material ReferenceDocument96 pagesI CT Material Referencefsolomon100% (20)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Financial System and The Economy - Éric Tymoigne PDFDocument258 pagesThe Financial System and The Economy - Éric Tymoigne PDFAfonso d'EcclesiisNo ratings yet

- OTE FreemodelDocument20 pagesOTE Freemodelvadavada96% (24)

- ETF Metals Prospectus-MergedDocument306 pagesETF Metals Prospectus-MergedJames Staines100% (1)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Facts and Fantasies About Commodity Futures Ten Years LaterDocument31 pagesFacts and Fantasies About Commodity Futures Ten Years LaterSoren K. GroupNo ratings yet

- WHP Fine and Specialty Chemicals 154169Document8 pagesWHP Fine and Specialty Chemicals 154169sanjayshah99No ratings yet

- Company ProfileDocument5 pagesCompany Profilesanjayshah99No ratings yet

- Sector Analysis: Chemical IndustryDocument28 pagesSector Analysis: Chemical Industrysanjayshah99No ratings yet

- OverviewDocument8 pagesOverviewsanjayshah99No ratings yet

- Chemical Business Focus: A Monthly Roundup and Analysis of The Key Factors Shaping World Chemical MarketsDocument27 pagesChemical Business Focus: A Monthly Roundup and Analysis of The Key Factors Shaping World Chemical Marketssanjayshah99No ratings yet

- Canada PlasticDocument47 pagesCanada Plasticsanjayshah99No ratings yet

- WEO2017 Launch BrusselsDocument14 pagesWEO2017 Launch Brusselssanjayshah99No ratings yet

- GCO - Pillar I - Trends and IndicatorsDocument92 pagesGCO - Pillar I - Trends and Indicatorssanjayshah99No ratings yet

- Downstream Petroleum Sector and Fuel Quality: The Quality of Transport FuelsDocument7 pagesDownstream Petroleum Sector and Fuel Quality: The Quality of Transport Fuelssanjayshah99No ratings yet

- EthanolDocument2 pagesEthanolsanjayshah99No ratings yet

- EthanolDocument2 pagesEthanolsanjayshah99No ratings yet

- Coal Chemical - SampleDocument39 pagesCoal Chemical - Samplesanjayshah99No ratings yet

- Sec Usa 2010Document172 pagesSec Usa 2010MicsomsNo ratings yet

- Currency Trader Magazine (08-2006) (Finance Forex Trading Review Analysis Commentary)Document46 pagesCurrency Trader Magazine (08-2006) (Finance Forex Trading Review Analysis Commentary)TradingSystemNo ratings yet

- Chuck ConnerDocument2 pagesChuck ConnerMarketsWikiNo ratings yet

- Orbis InstitutionalDocument61 pagesOrbis Institutionalsaharsh narangNo ratings yet

- Anti-Money Laundering Regulation of Cryptocurrency: U.S. and Global ApproachesDocument14 pagesAnti-Money Laundering Regulation of Cryptocurrency: U.S. and Global ApproachesFiorella VásquezNo ratings yet

- OCR Portal Client Quick Start Guide 7.12.2021Document17 pagesOCR Portal Client Quick Start Guide 7.12.2021jangbaangNo ratings yet

- Regulation of The Securities MarketDocument24 pagesRegulation of The Securities Marketlegalmatters100% (5)

- The Gold Market-OutlineDocument5 pagesThe Gold Market-OutlineMartin SeruggaNo ratings yet

- 1Document38 pages1Jonathan GrevhallNo ratings yet

- Commitment of Traders ReportDocument14 pagesCommitment of Traders ReportZerohedgeNo ratings yet

- Richard Dennis Sonterra Capital Vs Cba Nab Anz Macquarie Gov - Uscourts.nysd.461685.1.0-1Document87 pagesRichard Dennis Sonterra Capital Vs Cba Nab Anz Macquarie Gov - Uscourts.nysd.461685.1.0-1Maverick MinitriesNo ratings yet

- Hedge Funds. A Basic OverviewDocument41 pagesHedge Funds. A Basic OverviewBilal MalikNo ratings yet

- OTC Derivatives - Product History and Regulation (9-09)Document87 pagesOTC Derivatives - Product History and Regulation (9-09)Manish AnandNo ratings yet

- Hearings: Reauthorizing The Commodity Futures Trading CommissionDocument215 pagesHearings: Reauthorizing The Commodity Futures Trading CommissionScribd Government DocsNo ratings yet

- How To Succeed As A Sell Side Trader: Brent DonnellyDocument9 pagesHow To Succeed As A Sell Side Trader: Brent DonnellyAlvinNo ratings yet

- Improving Energy Market Regulation: Domestic and International IssuesDocument20 pagesImproving Energy Market Regulation: Domestic and International IssuesFransiska Ardie YantiNo ratings yet

- An Excerpt From A Human's Guide To Machine IntelligenceDocument10 pagesAn Excerpt From A Human's Guide To Machine Intelligencewamu885No ratings yet

- DDFX FOREX TRADING SYSTEM v4 PDFDocument15 pagesDDFX FOREX TRADING SYSTEM v4 PDFstrettt100% (1)

- LedgerX Amended Order 09-02-2020 SignedDocument4 pagesLedgerX Amended Order 09-02-2020 SignedMichaelPatrickMcSweeneyNo ratings yet

- BJSS Case Study - Regulatory Compliance v1.0 (US)Document8 pagesBJSS Case Study - Regulatory Compliance v1.0 (US)tabbforumNo ratings yet

- TheEconomist 2023 04 01Document297 pagesTheEconomist 2023 04 01Sh FNo ratings yet

- The Growth of Cryptocurrency in India: Its Challenges & Potential Impacts On LegislationDocument23 pagesThe Growth of Cryptocurrency in India: Its Challenges & Potential Impacts On LegislationHiren WaghelaNo ratings yet

- Moskowitz Time Series Momentum PaperDocument23 pagesMoskowitz Time Series Momentum PaperthyagosmesmeNo ratings yet

- Hayes Sentencing LetterDocument65 pagesHayes Sentencing LetterMichaelPatrickMcSweeneyNo ratings yet