5.1 Dynamic Programming and The HJB Equation: k+1 K K K K

5.1 Dynamic Programming and The HJB Equation: k+1 K K K K

You might also like

- CS 229, Public Course Problem Set #1 Solutions: Supervised LearningDocument10 pagesCS 229, Public Course Problem Set #1 Solutions: Supervised Learningsuhar adiNo ratings yet

- Ps and Solution CS229Document55 pagesPs and Solution CS229Anonymous COa5DYzJwNo ratings yet

- Sandoval - Political Law & Public International Law Notes (2018)Document125 pagesSandoval - Political Law & Public International Law Notes (2018)freegalado100% (10)

- Final Project On Outsourcing in IndiaDocument23 pagesFinal Project On Outsourcing in IndiaLaxman Zagge100% (3)

- Summer 2Document29 pagesSummer 2jimwaoNo ratings yet

- Woolseylecture 1Document4 pagesWoolseylecture 1Qing LiNo ratings yet

- 0 Tlemcen Mio Contrib PDFDocument48 pages0 Tlemcen Mio Contrib PDFManvir Singh GillNo ratings yet

- Optimal Control ApparentlyDocument32 pagesOptimal Control ApparentlySisa JoboNo ratings yet

- Lec 3Document22 pagesLec 3mohammed.elbakkalielammariNo ratings yet

- Deterministic Continuous Time Optimal Control and The Hamilton-Jacobi-Bellman EquationDocument7 pagesDeterministic Continuous Time Optimal Control and The Hamilton-Jacobi-Bellman EquationAbdesselem BoulkrouneNo ratings yet

- Andersson Djehiche - AMO 2011Document16 pagesAndersson Djehiche - AMO 2011artemischen0606No ratings yet

- Robotics: Control TheoryDocument54 pagesRobotics: Control TheoryPrakash RajNo ratings yet

- 8 PontryaginDocument31 pages8 PontryaginBogdan ManeaNo ratings yet

- 0 Tlemcen Mio ContribDocument49 pages0 Tlemcen Mio Contribtesfayetlh_400418456No ratings yet

- 5 - HJBDocument12 pages5 - HJBBogdan ManeaNo ratings yet

- Linear Quadratic ControlDocument7 pagesLinear Quadratic ControlnaumzNo ratings yet

- Chapter One: 1.1 Optimal Control ProblemDocument25 pagesChapter One: 1.1 Optimal Control ProblemOyster MacNo ratings yet

- Control CourseDocument126 pagesControl CourseDang Hai NguyenNo ratings yet

- Analisa NumerikDocument62 pagesAnalisa Numerikmohammad affanNo ratings yet

- Pontryagin Principle of Maximum Time-Optimal Control: Constrained Control, Bang-Bang ControlDocument14 pagesPontryagin Principle of Maximum Time-Optimal Control: Constrained Control, Bang-Bang ControldhayanethraNo ratings yet

- Optimal ControlDocument51 pagesOptimal ControlRidho AkbarNo ratings yet

- Equations of Motion of 2 DOF FlightDocument6 pagesEquations of Motion of 2 DOF FlightRam Krishan ShuklaNo ratings yet

- Optimal Control ExercisesDocument79 pagesOptimal Control ExercisesAlejandroHerreraGurideChile100% (2)

- DC 13 Appendix ADocument42 pagesDC 13 Appendix ABeny AbdouNo ratings yet

- ENGM541 Lab5 Runge Kutta SimulinkstatespaceDocument5 pagesENGM541 Lab5 Runge Kutta SimulinkstatespaceAbiodun GbengaNo ratings yet

- Mathii at Su and Sse: John Hassler Iies, Stockholm University February 25, 2005Document87 pagesMathii at Su and Sse: John Hassler Iies, Stockholm University February 25, 2005kolman2No ratings yet

- Homework Set 3 SolutionsDocument15 pagesHomework Set 3 SolutionsEunchan KimNo ratings yet

- An Introduction To Mathematical OptimalDocument126 pagesAn Introduction To Mathematical OptimalMauro VasconcellosNo ratings yet

- Introduction To Optimal Control Theory and Hamilton-Jacobi EquationsDocument55 pagesIntroduction To Optimal Control Theory and Hamilton-Jacobi EquationsPREETISH VIJNo ratings yet

- Optimizing Nonlinear Control AllocationDocument6 pagesOptimizing Nonlinear Control AllocationSamo SpontanostNo ratings yet

- 031 TuriniciDocument9 pages031 Turinicisatitz chongNo ratings yet

- Derivada de FréchetDocument18 pagesDerivada de FréchetVa LentínNo ratings yet

- Parameterized Expectations Algorithm: Lecture Notes 8Document33 pagesParameterized Expectations Algorithm: Lecture Notes 8Safis HajjouzNo ratings yet

- Robust Design of Linear Control Laws For Constrained Nonlinear Dynamic SystemsDocument6 pagesRobust Design of Linear Control Laws For Constrained Nonlinear Dynamic SystemsedutogNo ratings yet

- Topic 4 Convolution IntegralDocument5 pagesTopic 4 Convolution IntegralRona SharmaNo ratings yet

- Integral and Measure-Turnpike Properties For Infinite-Dimensional Optimal Control SystemsDocument34 pagesIntegral and Measure-Turnpike Properties For Infinite-Dimensional Optimal Control SystemsehsanhspNo ratings yet

- Pontryagin's Maximum Principle: Emo TodorovDocument12 pagesPontryagin's Maximum Principle: Emo TodorovmanishNo ratings yet

- Lecture 3 Opt ControlDocument35 pagesLecture 3 Opt ControlJaco GreeffNo ratings yet

- Time Dep SCH EqnDocument33 pagesTime Dep SCH Eqnutkarsh khandelwalNo ratings yet

- Limiting Average Cost Control Problems in A Class of Discrete-Time Stochastic SystemsDocument13 pagesLimiting Average Cost Control Problems in A Class of Discrete-Time Stochastic SystemsLuis Alberto FuentesNo ratings yet

- Approximate Solutions To Dynamic Models - Linear Methods: Harald UhligDocument12 pagesApproximate Solutions To Dynamic Models - Linear Methods: Harald UhligTony BuNo ratings yet

- Chapt 6Document12 pagesChapt 6NewtoniXNo ratings yet

- Sam HW2Document4 pagesSam HW2Ali HassanNo ratings yet

- Dynamic Programming and Stochastic Control Processes: Ici-L RD Bellm AnDocument12 pagesDynamic Programming and Stochastic Control Processes: Ici-L RD Bellm AnArturo ReynosoNo ratings yet

- 16.323 Principles of Optimal Control: Mit OpencoursewareDocument4 pages16.323 Principles of Optimal Control: Mit OpencoursewareMohand Achour TouatNo ratings yet

- 16.323 Principles of Optimal Control: Mit OpencoursewareDocument4 pages16.323 Principles of Optimal Control: Mit OpencoursewareMohand Achour TouatNo ratings yet

- The Action, The Lagrangian and Hamilton's PrincipleDocument15 pagesThe Action, The Lagrangian and Hamilton's PrincipleMayank TiwariNo ratings yet

- Optimal Control of An Oscillator SystemDocument6 pagesOptimal Control of An Oscillator SystemJoão HenriquesNo ratings yet

- Elements of Optimal Control Theory Pontryagin's Maximum PrincipleDocument11 pagesElements of Optimal Control Theory Pontryagin's Maximum PrinciplefaskillerNo ratings yet

- (Evans L.C.) An Introduction To Mathematical OptimDocument125 pages(Evans L.C.) An Introduction To Mathematical Optimhanu hanuNo ratings yet

- Lec02 2012eightDocument5 pagesLec02 2012eightPhạm Ngọc HòaNo ratings yet

- BellmanDocument8 pagesBellmanchiranjeevi kindinlaNo ratings yet

- Pde PDFDocument5 pagesPde PDFAlex Cruz CabreraNo ratings yet

- 1 Solving Systems of Linear InequalitiesDocument4 pages1 Solving Systems of Linear InequalitiesylwNo ratings yet

- Lect Notes 9Document43 pagesLect Notes 9Safis HajjouzNo ratings yet

- Advanced Algorithms Course. Lecture Notes. Part 11: Chernoff BoundsDocument4 pagesAdvanced Algorithms Course. Lecture Notes. Part 11: Chernoff BoundsKasapaNo ratings yet

- HW1Document11 pagesHW1Tao Liu YuNo ratings yet

- Green's Function Estimates for Lattice Schrödinger Operators and Applications. (AM-158)From EverandGreen's Function Estimates for Lattice Schrödinger Operators and Applications. (AM-158)No ratings yet

- 9 CH 1 2024-25Document12 pages9 CH 1 2024-25Muhammad Abdullah ToufiqueNo ratings yet

- Annual Report 2018 04 BothSN PDFDocument168 pagesAnnual Report 2018 04 BothSN PDFjoenediath9345No ratings yet

- Nidhi Gupta Resume UpdatedDocument4 pagesNidhi Gupta Resume Updatedshannbaby22No ratings yet

- Cabinet Cooler System Sizing GuideDocument1 pageCabinet Cooler System Sizing GuideAlexis BerrúNo ratings yet

- C203 C253 C353 Installation ManualDocument18 pagesC203 C253 C353 Installation ManuallaitangNo ratings yet

- Double Take Chinese Optics and Their Media in Postglobal PDFDocument47 pagesDouble Take Chinese Optics and Their Media in Postglobal PDFparker03No ratings yet

- Proposal NewDocument19 pagesProposal NewAzimSyahmiNo ratings yet

- Annulment of Marriage - Psycho IncapacityDocument53 pagesAnnulment of Marriage - Psycho IncapacityLawrence OlidNo ratings yet

- Barto Thesis 2020Document34 pagesBarto Thesis 2020Arjun Chitradurga RamachandraRaoNo ratings yet

- Welcome To Oneg ShabbatDocument19 pagesWelcome To Oneg ShabbatTovaNo ratings yet

- Multiple SclerosisDocument45 pagesMultiple Sclerosispriyanka bhowmikNo ratings yet

- Zohdy, Eaton & Mabey - Application of Surface Geophysics To Ground-Water Investigations - USGSDocument63 pagesZohdy, Eaton & Mabey - Application of Surface Geophysics To Ground-Water Investigations - USGSSalman AkbarNo ratings yet

- SkincareDocument84 pagesSkincareNikoletta AslanidiNo ratings yet

- Sankalp Final ProjectDocument40 pagesSankalp Final Projectsankalp mohantyNo ratings yet

- Acute Coronary SyndromeDocument9 pagesAcute Coronary Syndromekimchi girlNo ratings yet

- Ijiset V2 I12 50Document11 pagesIjiset V2 I12 50AndiNo ratings yet

- Articulo Sordo CegueraDocument11 pagesArticulo Sordo CegueraIsidoraBelénRojasTorresNo ratings yet

- Islam & Modern Science by Waleed1991Document118 pagesIslam & Modern Science by Waleed1991waleed1991No ratings yet

- MCNW2820 ThinkBook 16p Gen 4 v041423Document131 pagesMCNW2820 ThinkBook 16p Gen 4 v041423james cabrezosNo ratings yet

- Back To School LiturgyDocument2 pagesBack To School LiturgyChristopher C HootonNo ratings yet

- Reading Comprehension: Pacific OceanDocument2 pagesReading Comprehension: Pacific OceanMarlene Roa100% (1)

- Component Identification of GearDocument6 pagesComponent Identification of GearWandiNo ratings yet

- Technical Interview Questions - Active DirectoryDocument74 pagesTechnical Interview Questions - Active DirectoryMadhava SwamyNo ratings yet

- Literature Review On Hospital Information SystemsDocument8 pagesLiterature Review On Hospital Information Systemsc5mr3mxfNo ratings yet

- 1Registration-View Registration 230pm PDFDocument14 pages1Registration-View Registration 230pm PDFNeil CNo ratings yet

- Factors Affecting Kimchi Fermentation: Mheen, Tae IckDocument16 pagesFactors Affecting Kimchi Fermentation: Mheen, Tae IckNguyên Trân Nguyễn PhúcNo ratings yet

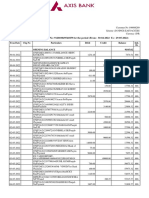

- Statement of Axis Account No:912010049541859 For The Period (From: 30-04-2022 To: 29-05-2022)Document5 pagesStatement of Axis Account No:912010049541859 For The Period (From: 30-04-2022 To: 29-05-2022)Rahul BansalNo ratings yet

- Chapter 9 - Segmentation - Targeting - PositioningDocument37 pagesChapter 9 - Segmentation - Targeting - PositioningMariano Jose MerubiaNo ratings yet

Download as pdf or txt

You might also like

- CS 229, Public Course Problem Set #1 Solutions: Supervised LearningDocument10 pagesCS 229, Public Course Problem Set #1 Solutions: Supervised Learningsuhar adiNo ratings yet

- Ps and Solution CS229Document55 pagesPs and Solution CS229Anonymous COa5DYzJwNo ratings yet

- Sandoval - Political Law & Public International Law Notes (2018)Document125 pagesSandoval - Political Law & Public International Law Notes (2018)freegalado100% (10)

- Final Project On Outsourcing in IndiaDocument23 pagesFinal Project On Outsourcing in IndiaLaxman Zagge100% (3)

- Summer 2Document29 pagesSummer 2jimwaoNo ratings yet

- Woolseylecture 1Document4 pagesWoolseylecture 1Qing LiNo ratings yet

- 0 Tlemcen Mio Contrib PDFDocument48 pages0 Tlemcen Mio Contrib PDFManvir Singh GillNo ratings yet

- Optimal Control ApparentlyDocument32 pagesOptimal Control ApparentlySisa JoboNo ratings yet

- Lec 3Document22 pagesLec 3mohammed.elbakkalielammariNo ratings yet

- Deterministic Continuous Time Optimal Control and The Hamilton-Jacobi-Bellman EquationDocument7 pagesDeterministic Continuous Time Optimal Control and The Hamilton-Jacobi-Bellman EquationAbdesselem BoulkrouneNo ratings yet

- Andersson Djehiche - AMO 2011Document16 pagesAndersson Djehiche - AMO 2011artemischen0606No ratings yet

- Robotics: Control TheoryDocument54 pagesRobotics: Control TheoryPrakash RajNo ratings yet

- 8 PontryaginDocument31 pages8 PontryaginBogdan ManeaNo ratings yet

- 0 Tlemcen Mio ContribDocument49 pages0 Tlemcen Mio Contribtesfayetlh_400418456No ratings yet

- 5 - HJBDocument12 pages5 - HJBBogdan ManeaNo ratings yet

- Linear Quadratic ControlDocument7 pagesLinear Quadratic ControlnaumzNo ratings yet

- Chapter One: 1.1 Optimal Control ProblemDocument25 pagesChapter One: 1.1 Optimal Control ProblemOyster MacNo ratings yet

- Control CourseDocument126 pagesControl CourseDang Hai NguyenNo ratings yet

- Analisa NumerikDocument62 pagesAnalisa Numerikmohammad affanNo ratings yet

- Pontryagin Principle of Maximum Time-Optimal Control: Constrained Control, Bang-Bang ControlDocument14 pagesPontryagin Principle of Maximum Time-Optimal Control: Constrained Control, Bang-Bang ControldhayanethraNo ratings yet

- Optimal ControlDocument51 pagesOptimal ControlRidho AkbarNo ratings yet

- Equations of Motion of 2 DOF FlightDocument6 pagesEquations of Motion of 2 DOF FlightRam Krishan ShuklaNo ratings yet

- Optimal Control ExercisesDocument79 pagesOptimal Control ExercisesAlejandroHerreraGurideChile100% (2)

- DC 13 Appendix ADocument42 pagesDC 13 Appendix ABeny AbdouNo ratings yet

- ENGM541 Lab5 Runge Kutta SimulinkstatespaceDocument5 pagesENGM541 Lab5 Runge Kutta SimulinkstatespaceAbiodun GbengaNo ratings yet

- Mathii at Su and Sse: John Hassler Iies, Stockholm University February 25, 2005Document87 pagesMathii at Su and Sse: John Hassler Iies, Stockholm University February 25, 2005kolman2No ratings yet

- Homework Set 3 SolutionsDocument15 pagesHomework Set 3 SolutionsEunchan KimNo ratings yet

- An Introduction To Mathematical OptimalDocument126 pagesAn Introduction To Mathematical OptimalMauro VasconcellosNo ratings yet

- Introduction To Optimal Control Theory and Hamilton-Jacobi EquationsDocument55 pagesIntroduction To Optimal Control Theory and Hamilton-Jacobi EquationsPREETISH VIJNo ratings yet

- Optimizing Nonlinear Control AllocationDocument6 pagesOptimizing Nonlinear Control AllocationSamo SpontanostNo ratings yet

- 031 TuriniciDocument9 pages031 Turinicisatitz chongNo ratings yet

- Derivada de FréchetDocument18 pagesDerivada de FréchetVa LentínNo ratings yet

- Parameterized Expectations Algorithm: Lecture Notes 8Document33 pagesParameterized Expectations Algorithm: Lecture Notes 8Safis HajjouzNo ratings yet

- Robust Design of Linear Control Laws For Constrained Nonlinear Dynamic SystemsDocument6 pagesRobust Design of Linear Control Laws For Constrained Nonlinear Dynamic SystemsedutogNo ratings yet

- Topic 4 Convolution IntegralDocument5 pagesTopic 4 Convolution IntegralRona SharmaNo ratings yet

- Integral and Measure-Turnpike Properties For Infinite-Dimensional Optimal Control SystemsDocument34 pagesIntegral and Measure-Turnpike Properties For Infinite-Dimensional Optimal Control SystemsehsanhspNo ratings yet

- Pontryagin's Maximum Principle: Emo TodorovDocument12 pagesPontryagin's Maximum Principle: Emo TodorovmanishNo ratings yet

- Lecture 3 Opt ControlDocument35 pagesLecture 3 Opt ControlJaco GreeffNo ratings yet

- Time Dep SCH EqnDocument33 pagesTime Dep SCH Eqnutkarsh khandelwalNo ratings yet

- Limiting Average Cost Control Problems in A Class of Discrete-Time Stochastic SystemsDocument13 pagesLimiting Average Cost Control Problems in A Class of Discrete-Time Stochastic SystemsLuis Alberto FuentesNo ratings yet

- Approximate Solutions To Dynamic Models - Linear Methods: Harald UhligDocument12 pagesApproximate Solutions To Dynamic Models - Linear Methods: Harald UhligTony BuNo ratings yet

- Chapt 6Document12 pagesChapt 6NewtoniXNo ratings yet

- Sam HW2Document4 pagesSam HW2Ali HassanNo ratings yet

- Dynamic Programming and Stochastic Control Processes: Ici-L RD Bellm AnDocument12 pagesDynamic Programming and Stochastic Control Processes: Ici-L RD Bellm AnArturo ReynosoNo ratings yet

- 16.323 Principles of Optimal Control: Mit OpencoursewareDocument4 pages16.323 Principles of Optimal Control: Mit OpencoursewareMohand Achour TouatNo ratings yet

- 16.323 Principles of Optimal Control: Mit OpencoursewareDocument4 pages16.323 Principles of Optimal Control: Mit OpencoursewareMohand Achour TouatNo ratings yet

- The Action, The Lagrangian and Hamilton's PrincipleDocument15 pagesThe Action, The Lagrangian and Hamilton's PrincipleMayank TiwariNo ratings yet

- Optimal Control of An Oscillator SystemDocument6 pagesOptimal Control of An Oscillator SystemJoão HenriquesNo ratings yet

- Elements of Optimal Control Theory Pontryagin's Maximum PrincipleDocument11 pagesElements of Optimal Control Theory Pontryagin's Maximum PrinciplefaskillerNo ratings yet

- (Evans L.C.) An Introduction To Mathematical OptimDocument125 pages(Evans L.C.) An Introduction To Mathematical Optimhanu hanuNo ratings yet

- Lec02 2012eightDocument5 pagesLec02 2012eightPhạm Ngọc HòaNo ratings yet

- BellmanDocument8 pagesBellmanchiranjeevi kindinlaNo ratings yet

- Pde PDFDocument5 pagesPde PDFAlex Cruz CabreraNo ratings yet

- 1 Solving Systems of Linear InequalitiesDocument4 pages1 Solving Systems of Linear InequalitiesylwNo ratings yet

- Lect Notes 9Document43 pagesLect Notes 9Safis HajjouzNo ratings yet

- Advanced Algorithms Course. Lecture Notes. Part 11: Chernoff BoundsDocument4 pagesAdvanced Algorithms Course. Lecture Notes. Part 11: Chernoff BoundsKasapaNo ratings yet

- HW1Document11 pagesHW1Tao Liu YuNo ratings yet

- Green's Function Estimates for Lattice Schrödinger Operators and Applications. (AM-158)From EverandGreen's Function Estimates for Lattice Schrödinger Operators and Applications. (AM-158)No ratings yet

- 9 CH 1 2024-25Document12 pages9 CH 1 2024-25Muhammad Abdullah ToufiqueNo ratings yet

- Annual Report 2018 04 BothSN PDFDocument168 pagesAnnual Report 2018 04 BothSN PDFjoenediath9345No ratings yet

- Nidhi Gupta Resume UpdatedDocument4 pagesNidhi Gupta Resume Updatedshannbaby22No ratings yet

- Cabinet Cooler System Sizing GuideDocument1 pageCabinet Cooler System Sizing GuideAlexis BerrúNo ratings yet

- C203 C253 C353 Installation ManualDocument18 pagesC203 C253 C353 Installation ManuallaitangNo ratings yet

- Double Take Chinese Optics and Their Media in Postglobal PDFDocument47 pagesDouble Take Chinese Optics and Their Media in Postglobal PDFparker03No ratings yet

- Proposal NewDocument19 pagesProposal NewAzimSyahmiNo ratings yet

- Annulment of Marriage - Psycho IncapacityDocument53 pagesAnnulment of Marriage - Psycho IncapacityLawrence OlidNo ratings yet

- Barto Thesis 2020Document34 pagesBarto Thesis 2020Arjun Chitradurga RamachandraRaoNo ratings yet

- Welcome To Oneg ShabbatDocument19 pagesWelcome To Oneg ShabbatTovaNo ratings yet

- Multiple SclerosisDocument45 pagesMultiple Sclerosispriyanka bhowmikNo ratings yet

- Zohdy, Eaton & Mabey - Application of Surface Geophysics To Ground-Water Investigations - USGSDocument63 pagesZohdy, Eaton & Mabey - Application of Surface Geophysics To Ground-Water Investigations - USGSSalman AkbarNo ratings yet

- SkincareDocument84 pagesSkincareNikoletta AslanidiNo ratings yet

- Sankalp Final ProjectDocument40 pagesSankalp Final Projectsankalp mohantyNo ratings yet

- Acute Coronary SyndromeDocument9 pagesAcute Coronary Syndromekimchi girlNo ratings yet

- Ijiset V2 I12 50Document11 pagesIjiset V2 I12 50AndiNo ratings yet

- Articulo Sordo CegueraDocument11 pagesArticulo Sordo CegueraIsidoraBelénRojasTorresNo ratings yet

- Islam & Modern Science by Waleed1991Document118 pagesIslam & Modern Science by Waleed1991waleed1991No ratings yet

- MCNW2820 ThinkBook 16p Gen 4 v041423Document131 pagesMCNW2820 ThinkBook 16p Gen 4 v041423james cabrezosNo ratings yet

- Back To School LiturgyDocument2 pagesBack To School LiturgyChristopher C HootonNo ratings yet

- Reading Comprehension: Pacific OceanDocument2 pagesReading Comprehension: Pacific OceanMarlene Roa100% (1)

- Component Identification of GearDocument6 pagesComponent Identification of GearWandiNo ratings yet

- Technical Interview Questions - Active DirectoryDocument74 pagesTechnical Interview Questions - Active DirectoryMadhava SwamyNo ratings yet

- Literature Review On Hospital Information SystemsDocument8 pagesLiterature Review On Hospital Information Systemsc5mr3mxfNo ratings yet

- 1Registration-View Registration 230pm PDFDocument14 pages1Registration-View Registration 230pm PDFNeil CNo ratings yet

- Factors Affecting Kimchi Fermentation: Mheen, Tae IckDocument16 pagesFactors Affecting Kimchi Fermentation: Mheen, Tae IckNguyên Trân Nguyễn PhúcNo ratings yet

- Statement of Axis Account No:912010049541859 For The Period (From: 30-04-2022 To: 29-05-2022)Document5 pagesStatement of Axis Account No:912010049541859 For The Period (From: 30-04-2022 To: 29-05-2022)Rahul BansalNo ratings yet

- Chapter 9 - Segmentation - Targeting - PositioningDocument37 pagesChapter 9 - Segmentation - Targeting - PositioningMariano Jose MerubiaNo ratings yet