Download as pdf

You might also like

- Kerrie Kennedy, Will KinnearDocument132 pagesKerrie Kennedy, Will KinnearAnonymous LpvYX5U2oK100% (1)

- Third Point Q3 2012 Investor Letter TPOIDocument11 pagesThird Point Q3 2012 Investor Letter TPOIVALUEWALK LLCNo ratings yet

- Ghazi ValueInvestingCongress 100112Document70 pagesGhazi ValueInvestingCongress 100112VALUEWALK LLC100% (1)

- 2012 Third Point Q2 Investor Letter TPOIDocument7 pages2012 Third Point Q2 Investor Letter TPOIVALUEWALK LLC100% (1)

- 2012 Third Point Q2 Investor Letter TPOIDocument7 pages2012 Third Point Q2 Investor Letter TPOIVALUEWALK LLC100% (1)

- Rule of 72Document13 pagesRule of 72api-344976556No ratings yet

- Ratio AnalysisDocument51 pagesRatio AnalysisSeema RahulNo ratings yet

- Surname: First Name: Campus France Registration Number: IN Age: Marital StatusDocument2 pagesSurname: First Name: Campus France Registration Number: IN Age: Marital StatusSahil Shah100% (1)

- FinTech Rising: Navigating the maze of US & EU regulationsFrom EverandFinTech Rising: Navigating the maze of US & EU regulationsRating: 5 out of 5 stars5/5 (1)

- Financial News Articles - COMPLETE ARCHIVEDocument319 pagesFinancial News Articles - COMPLETE ARCHIVEKeith KnightNo ratings yet

- Dodd Frank Explained - CNBCDocument3 pagesDodd Frank Explained - CNBCAks SukhtankarNo ratings yet

- The Rehabilitation of The CDSDocument3 pagesThe Rehabilitation of The CDSJasvinder JosenNo ratings yet

- Policy Fin CrisisDocument7 pagesPolicy Fin CrisisThought LeadersNo ratings yet

- Presentacion Crisis 2008Document1 pagePresentacion Crisis 2008Regina ZamudioNo ratings yet

- Jean Ramirez - Inside Job Movie ReviewDocument14 pagesJean Ramirez - Inside Job Movie ReviewJean Paul RamirezNo ratings yet

- Anatomy of A Credit CrisisDocument39 pagesAnatomy of A Credit CrisisrobertfilmerNo ratings yet

- Movie Review Inside JobDocument7 pagesMovie Review Inside JobVikram Singh MeenaNo ratings yet

- Groupwork Assignment Submission 2 M5Document5 pagesGroupwork Assignment Submission 2 M5Abdullah AbdullahNo ratings yet

- Alow 21 Book ReviewDocument29 pagesAlow 21 Book ReviewianseowNo ratings yet

- Basel 2.5, Basel III. Their Tasks Are To Identify Risks To The Financial Stability of TheDocument5 pagesBasel 2.5, Basel III. Their Tasks Are To Identify Risks To The Financial Stability of TheSahoo SKNo ratings yet

- The 2008 Financial CrisisDocument4 pagesThe 2008 Financial CrisisLede Ann Calipus YapNo ratings yet

- The Big Short Case StudyDocument5 pagesThe Big Short Case StudyMaricar RoqueNo ratings yet

- Who Really Owns Your Stocks and BondsDocument13 pagesWho Really Owns Your Stocks and BondsMuffy Dobbs0% (1)

- Ellen Brown 19052023Document5 pagesEllen Brown 19052023Thuan TrinhNo ratings yet

- Ellen Brown 24032023Document7 pagesEllen Brown 24032023Thuan TrinhNo ratings yet

- Analysis of Ethical Issues Involved in The Global Financial Crisis (2008)Document5 pagesAnalysis of Ethical Issues Involved in The Global Financial Crisis (2008)Abhijeet SiteNo ratings yet

- The Myth of Financial ReformDocument6 pagesThe Myth of Financial ReformManharMayankNo ratings yet

- Anatomy of A Credit CrisisDocument31 pagesAnatomy of A Credit CrisisVikas KapoorNo ratings yet

- En The Credit CrisisDocument3 pagesEn The Credit CrisisDubstep ImtiyajNo ratings yet

- ASF Journal Summer Spring 2011Document42 pagesASF Journal Summer Spring 2011Adam HayaNo ratings yet

- Groupwork Assignment Submission 3 M7Document9 pagesGroupwork Assignment Submission 3 M7Abdullah AbdullahNo ratings yet

- Real Life Conspiracy TheoryDocument25 pagesReal Life Conspiracy TheorySherry HernandezNo ratings yet

- GlobalcreditcrisisDocument3 pagesGlobalcreditcrisisFazulAXNo ratings yet

- Zoltan #28Document4 pagesZoltan #28Zerohedge100% (2)

- Shubhankar Shukla Inside Job StudyDocument5 pagesShubhankar Shukla Inside Job Studysubh mongNo ratings yet

- Sprott November 2009 CommentDocument7 pagesSprott November 2009 CommentZerohedgeNo ratings yet

- Solution Manual For Bank Management and Financial Services 9th Edition Rose Hudgins 0078034671 9780078034671Document36 pagesSolution Manual For Bank Management and Financial Services 9th Edition Rose Hudgins 0078034671 9780078034671charlesblackdmpscxyrfi100% (37)

- CS - Global Money NotesDocument14 pagesCS - Global Money NotesrockstarliveNo ratings yet

- When Catastrophes ColludeDocument9 pagesWhen Catastrophes ColludeMohammed SalahNo ratings yet

- Follow the Money: Fed Largesse, Inflation, and Moon Shots in Financial MarketsFrom EverandFollow the Money: Fed Largesse, Inflation, and Moon Shots in Financial MarketsNo ratings yet

- August 182010 PostsDocument273 pagesAugust 182010 PostsAlbert L. PeiaNo ratings yet

- Legg Mason StrategyDocument6 pagesLegg Mason Strategyapi-26172897No ratings yet

- Bank Management and Financial Services 9th Edition Rose Solutions ManualDocument26 pagesBank Management and Financial Services 9th Edition Rose Solutions ManualMelanieThorntonbcmk100% (60)

- 11-12-05 Criminality at The Top of A Lawless, Bankrupt NationDocument5 pages11-12-05 Criminality at The Top of A Lawless, Bankrupt NationHuman Rights Alert - NGO (RA)No ratings yet

- Diamond and Kashyap On The Recent Financial Upheavals: Steven D. LevittDocument6 pagesDiamond and Kashyap On The Recent Financial Upheavals: Steven D. LevittfarrukhazeemNo ratings yet

- Red FinancialDocument63 pagesRed Financialreegent_9No ratings yet

- Too Big To FailDocument3 pagesToo Big To FailNicolas MarionNo ratings yet

- Summary of Movie Inside JobDocument6 pagesSummary of Movie Inside JobabhinavruhelaNo ratings yet

- JPMorgan London WhaleDocument10 pagesJPMorgan London Whalejanedpe25000No ratings yet

- Ellen Brown 13032023Document7 pagesEllen Brown 13032023Thuan TrinhNo ratings yet

- Ignou Mba MsDocument22 pagesIgnou Mba MssamuelkishNo ratings yet

- Inside JobDocument52 pagesInside JobMariaNo ratings yet

- Dissertation FinalDocument39 pagesDissertation FinalSarvesh Raj MehtaNo ratings yet

- PART 1: How We Got Here?Document5 pagesPART 1: How We Got Here?Abdul Wahab ShahidNo ratings yet

- Dodd-Frank: What It Does and Why It's FlawedDocument232 pagesDodd-Frank: What It Does and Why It's FlawedMercatus Center at George Mason University100% (2)

- Which Were Backed Merely by Derivatives and Credit Default SwapsDocument3 pagesWhich Were Backed Merely by Derivatives and Credit Default SwapsPatrick HookNo ratings yet

- Another Financial Meltdown Is Closer Than It Appears.: Source: FREDDocument14 pagesAnother Financial Meltdown Is Closer Than It Appears.: Source: FREDVidit HarsulkarNo ratings yet

- JPMorgan Chase London Whale ZDocument23 pagesJPMorgan Chase London Whale ZMaksym ShodaNo ratings yet

- ProjectDocument7 pagesProjectmalik waseemNo ratings yet

- Case Analysis of Countrywide Financial - The Subprime MeltdownDocument5 pagesCase Analysis of Countrywide Financial - The Subprime Meltdownharsha_silan1487100% (1)

- Dodd-Frank ACT: 1. Oversees Wall StreetDocument12 pagesDodd-Frank ACT: 1. Oversees Wall StreetTanishaq bindalNo ratings yet

- DZwirn - This Time Its DifferentDocument50 pagesDZwirn - This Time Its Differentfalistor2No ratings yet

- Brian Anthony ByrneDocument4 pagesBrian Anthony ByrneBrianByrne4No ratings yet

- Where Do They Stand?: PerspectiveDocument8 pagesWhere Do They Stand?: Perspectiverajesh palNo ratings yet

- Who Would Lose Under ObamaDocument8 pagesWho Would Lose Under Obamanhoveem_a4No ratings yet

- Money Market Fund (MMF) Comment Letter To FSOC 2/15/13Document27 pagesMoney Market Fund (MMF) Comment Letter To FSOC 2/15/13occupytheSEC100% (1)

- Financial Globalization and The Future of The FedDocument26 pagesFinancial Globalization and The Future of The FedHenry PatnerNo ratings yet

- OWS Money Market Comment LetterDocument5 pagesOWS Money Market Comment LetterMatt StollerNo ratings yet

- Ubben ValueInvestingCongress 100212Document27 pagesUbben ValueInvestingCongress 100212VALUEWALK LLC100% (1)

- 8th Annual New York: Value Investing CongressDocument46 pages8th Annual New York: Value Investing CongressVALUEWALK LLCNo ratings yet

- 8th Annual New York: Value Investing CongressDocument51 pages8th Annual New York: Value Investing CongressVALUEWALK LLCNo ratings yet

- 8th Annual New York: Value Investing CongressDocument53 pages8th Annual New York: Value Investing CongressVALUEWALK LLCNo ratings yet

- Buckley ValueInvestingCongress 100112Document45 pagesBuckley ValueInvestingCongress 100112VALUEWALK LLCNo ratings yet

- HP PresentationDocument69 pagesHP Presentationssc320No ratings yet

- McGuire ValueInvestingCongress 100112Document70 pagesMcGuire ValueInvestingCongress 100112VALUEWALK LLCNo ratings yet

- SHLDDocument18 pagesSHLDduwe7809100% (1)

- Green Mountain Coffee Roasters' Q2 and Q3 2011 Net Sales Figures Look Odd and Why It MattersDocument8 pagesGreen Mountain Coffee Roasters' Q2 and Q3 2011 Net Sales Figures Look Odd and Why It MattersmistervigilanteNo ratings yet

- Value Investing Congress Presentation-Tilson-10!1!12Document93 pagesValue Investing Congress Presentation-Tilson-10!1!12VALUEWALK LLCNo ratings yet

- Mauldin ValueInvestingCongress 100112Document11 pagesMauldin ValueInvestingCongress 100112VALUEWALK LLCNo ratings yet

- Rosenstein ValueInvestingCongress 100112Document42 pagesRosenstein ValueInvestingCongress 100112VALUEWALK LLCNo ratings yet

- Rockstone Research URS1 EnglishDocument32 pagesRockstone Research URS1 EnglishVALUEWALK LLC100% (1)

- Roepers ValueInvestingCongress 100212Document30 pagesRoepers ValueInvestingCongress 100212VALUEWALK LLCNo ratings yet

- Greenlight Q2 Letter To InvestorsDocument5 pagesGreenlight Q2 Letter To InvestorsVALUEWALK LLCNo ratings yet

- T2 Accredited Fund Letter To Investors June 12Document10 pagesT2 Accredited Fund Letter To Investors June 12VALUEWALK LLCNo ratings yet

- GMCR Profits Overstated or MisunderstoodDocument8 pagesGMCR Profits Overstated or MisunderstoodVALUEWALK LLCNo ratings yet

- Fairholme: Ignore The CrowdDocument13 pagesFairholme: Ignore The CrowdVALUEWALK LLCNo ratings yet

- Fairholme: Ignore The CrowdDocument13 pagesFairholme: Ignore The CrowdVALUEWALK LLCNo ratings yet

- Annual Report: March 31, 2011Document23 pagesAnnual Report: March 31, 2011VALUEWALK LLCNo ratings yet

- Pershing Square Q1 12 Investor LetterDocument14 pagesPershing Square Q1 12 Investor LetterVALUEWALK LLCNo ratings yet

- VALUExVail 2012 James ChanosDocument30 pagesVALUExVail 2012 James ChanosVALUEWALK LLCNo ratings yet

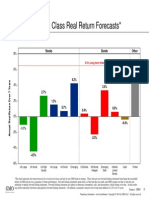

- GMO 7 Year Asset Forecast - Jan 2014Document1 pageGMO 7 Year Asset Forecast - Jan 2014CanadianValueNo ratings yet

- Why We'Re Long J.C. Penney-T2 PartnersDocument18 pagesWhy We'Re Long J.C. Penney-T2 PartnersVALUEWALK LLCNo ratings yet

- Mauboussinonstrategy - Sharerepurchasefromallangles June 2012Document15 pagesMauboussinonstrategy - Sharerepurchasefromallangles June 2012zeebugNo ratings yet

- To Longleaf Shareholders: Cumulative Returns at December 31, 2011Document6 pagesTo Longleaf Shareholders: Cumulative Returns at December 31, 2011VALUEWALK LLCNo ratings yet

- Indian Weekender Vol 6 Issue 2Document40 pagesIndian Weekender Vol 6 Issue 2Indian WeekenderNo ratings yet

- Wcm-Sudha Agri GoldDocument99 pagesWcm-Sudha Agri GoldAdiseshu Chowdary100% (1)

- Mcqs Audit - PRTC2Document16 pagesMcqs Audit - PRTC2jpbluejnNo ratings yet

- DPR Neha FNLDocument51 pagesDPR Neha FNLNaina Verma100% (1)

- Chap 18Document110 pagesChap 18Desai SarvidaNo ratings yet

- Bacungan VsDocument8 pagesBacungan VsKevin Juat BulotanoNo ratings yet

- Investments AssignmentDocument5 pagesInvestments Assignmentapi-276011473No ratings yet

- 02 Accounting Study NotesDocument4 pages02 Accounting Study NotesJonas Scheck100% (2)

- Determinants of Cash HoldingsDocument26 pagesDeterminants of Cash Holdingspoushal100% (1)

- Devi Mahatmyam Durga Saptasati Chapter 12 in TeluguDocument6 pagesDevi Mahatmyam Durga Saptasati Chapter 12 in TeluguPhani AttaluriNo ratings yet

- Machetti v. Hospicio de San Jose, 43 Phil 297 (1922)Document2 pagesMachetti v. Hospicio de San Jose, 43 Phil 297 (1922)Louie SalladorNo ratings yet

- 03 Gilbert Lumber CompanyDocument36 pages03 Gilbert Lumber CompanyEkta Derwal PGP 2022-24 BatchNo ratings yet

- ZAGG Presentation 12-14-10 Final-2Document23 pagesZAGG Presentation 12-14-10 Final-2tony3890100% (1)

- Deed of Absolute SaleDocument2 pagesDeed of Absolute SaleLDNo ratings yet

- Instruction Kit For Eform Chg-1Document22 pagesInstruction Kit For Eform Chg-1Savoir PenNo ratings yet

- Classifieds: HyderabadDocument1 pageClassifieds: HyderabadrsreddysNo ratings yet

- 2016-06-23 GSEs - Former White House Officials Involved in GSE ScandalDocument11 pages2016-06-23 GSEs - Former White House Officials Involved in GSE ScandalJoshua Rosner100% (1)

- Test ID Max Marks: 200 CA CPT December 2014 (Memory Based Paper)Document21 pagesTest ID Max Marks: 200 CA CPT December 2014 (Memory Based Paper)Icaii InfotechNo ratings yet

- GrasimDocument18 pagesGrasimmonish147852No ratings yet

- Draft Budget ManualDocument72 pagesDraft Budget ManualanuNo ratings yet

- MY Own CMADocument15 pagesMY Own CMASaorabh KumarNo ratings yet

- Valuation of Common Stocks and CorporationsDocument79 pagesValuation of Common Stocks and CorporationsAnonymous f7wV1lQKRNo ratings yet

- Toyota of Palo Alto Sunnyvale Mountain View - Print Ad Used Cars Corolla Yaris Camry Prius Highlander Rav4Document1 pageToyota of Palo Alto Sunnyvale Mountain View - Print Ad Used Cars Corolla Yaris Camry Prius Highlander Rav4Toyota of Palo AltoNo ratings yet

- BSP Published Circulars 2017Document2 pagesBSP Published Circulars 2017Remson OrasNo ratings yet

- Media Statement On Student Funding by The Minister of Higher Education and TrainingDocument5 pagesMedia Statement On Student Funding by The Minister of Higher Education and TrainingeNCA.comNo ratings yet

- Hospital Project 1Document49 pagesHospital Project 1Rutvi Shah RathiNo ratings yet