Havells (India) LTD: Key Financial Indicators

Havells (India) LTD: Key Financial Indicators

You might also like

- Case Study - Transaction Exposure - LufthansaDocument2 pagesCase Study - Transaction Exposure - LufthansaRaguRagupathy100% (3)

- Step AcquisitionsDocument7 pagesStep AcquisitionsKelvin Leong100% (1)

- Illustration - Chapter 2Document2 pagesIllustration - Chapter 2Jahzceel CecelNo ratings yet

- Honeywell Automation 2009 ReportDocument4 pagesHoneywell Automation 2009 ReportmworahNo ratings yet

- BPL LTD: Key Financial IndicatorsDocument4 pagesBPL LTD: Key Financial IndicatorsakkuekNo ratings yet

- Havels Most Mar 11Document24 pagesHavels Most Mar 11Ravi SwaminathanNo ratings yet

- Havell Q4 FY2011Document6 pagesHavell Q4 FY2011Tushar DasNo ratings yet

- Manu Mam Term PaperDocument46 pagesManu Mam Term PaperSubodh KumarNo ratings yet

- Finolex Cables, 1Q FY 2014Document14 pagesFinolex Cables, 1Q FY 2014Angel BrokingNo ratings yet

- Havells India LTD - 09042013Document20 pagesHavells India LTD - 09042013shilpaarora988No ratings yet

- Angel Broking: Bharat Heavy ElectricalsDocument27 pagesAngel Broking: Bharat Heavy ElectricalsChintan JethvaNo ratings yet

- Sterlite Technologies Limited (STEOPT) : Well Placed in High Growth MarketsDocument25 pagesSterlite Technologies Limited (STEOPT) : Well Placed in High Growth Marketssourabh_chowdhury_1No ratings yet

- Market Outlook 27th February 2012Document5 pagesMarket Outlook 27th February 2012Angel BrokingNo ratings yet

- Havells India LTD: Market Data Buy Target Price: Rs 500 Investment RationaleDocument6 pagesHavells India LTD: Market Data Buy Target Price: Rs 500 Investment Rationalenalinschwarz123No ratings yet

- Salzer-Electronics-Limited 495 InitiatingCoverageDocument12 pagesSalzer-Electronics-Limited 495 InitiatingCoveragemayur_sgNo ratings yet

- Atul LTDDocument4 pagesAtul LTDFast SwiftNo ratings yet

- Reliance Communications LTDDocument4 pagesReliance Communications LTDSahil JainNo ratings yet

- Elantas BeckDocument6 pagesElantas Beckvivek dkrpuNo ratings yet

- Havells Final ProjectDocument17 pagesHavells Final Projectsimran agarwalNo ratings yet

- Quant Havells Initiating CoverageDocument26 pagesQuant Havells Initiating CoverageviralnshahNo ratings yet

- Havells India June 2012Document20 pagesHavells India June 2012VikramGhatgeNo ratings yet

- Blue Dart Express LTD: Key Financial IndicatorsDocument4 pagesBlue Dart Express LTD: Key Financial IndicatorsSagar DholeNo ratings yet

- KEC International, 4th February, 2013Document11 pagesKEC International, 4th February, 2013Angel BrokingNo ratings yet

- Havells India Jan 09 Fairwealth Securities Initiate-Buy Target280Document9 pagesHavells India Jan 09 Fairwealth Securities Initiate-Buy Target280Sovid Gupta100% (1)

- Market Outlook 11th October 2011Document5 pagesMarket Outlook 11th October 2011Angel BrokingNo ratings yet

- BYD Annual Report 2011Document106 pagesBYD Annual Report 2011krabadiNo ratings yet

- Company Presentation September 2010 PDFDocument20 pagesCompany Presentation September 2010 PDFsonar_neelNo ratings yet

- Thermax: Performance HighlightsDocument10 pagesThermax: Performance HighlightsAngel BrokingNo ratings yet

- Market Outlook 2nd December 2011Document6 pagesMarket Outlook 2nd December 2011Angel BrokingNo ratings yet

- Project Report On VodafoneDocument11 pagesProject Report On Vodafoneanshul_kh29150% (1)

- Larsen & ToubroDocument15 pagesLarsen & ToubroAngel BrokingNo ratings yet

- C&S Electric Limited: Rating History Instrument Rating Outstanding Previous Ratings March, 2010 September, 2008Document4 pagesC&S Electric Limited: Rating History Instrument Rating Outstanding Previous Ratings March, 2010 September, 2008sgoswami_1No ratings yet

- 5.4 Rashtriya Ispat Nigam LTD.: Performance HighlightsDocument2 pages5.4 Rashtriya Ispat Nigam LTD.: Performance HighlightsRavi ChandNo ratings yet

- Havells India LimitedDocument15 pagesHavells India LimitedRohit PandeyNo ratings yet

- Fie M Industries LimitedDocument4 pagesFie M Industries LimitedDavuluri OmprakashNo ratings yet

- Videocon Industries LTD: Key Financial IndicatorsDocument4 pagesVideocon Industries LTD: Key Financial IndicatorsryreddyNo ratings yet

- Steel Authority of IndiaDocument13 pagesSteel Authority of IndiaAngel BrokingNo ratings yet

- YTL Power IC - 20070912 - Global Utility PlayDocument18 pagesYTL Power IC - 20070912 - Global Utility PlayMuhamad Firdaus MinhadNo ratings yet

- Rakon Announcement 14 Feb 08Document6 pagesRakon Announcement 14 Feb 08Peter CorbanNo ratings yet

- Trends in Public and Private Sector in India 2381Document29 pagesTrends in Public and Private Sector in India 2381Munish NagarNo ratings yet

- Performance Highlights: NeutralDocument11 pagesPerformance Highlights: NeutralAngel BrokingNo ratings yet

- Mid Cap Ideas - Value and Growth Investing 250112 - 11 - 0602120242Document21 pagesMid Cap Ideas - Value and Growth Investing 250112 - 11 - 0602120242Chetan MaheshwariNo ratings yet

- Apar IndustriesDocument16 pagesApar Industriesh_o_mNo ratings yet

- A Global Air Conditioning and Engineering Services CompanyDocument50 pagesA Global Air Conditioning and Engineering Services Companyraj_mrecj6511No ratings yet

- Sharp Corporation: Company ProfileDocument9 pagesSharp Corporation: Company ProfileVivi Sabrina BaswedanNo ratings yet

- Bhel Group 1Document16 pagesBhel Group 1arijitguha07No ratings yet

- HavellsDocument20 pagesHavellsvraj.patelsmpic090No ratings yet

- Steel Authority of India Result UpdatedDocument13 pagesSteel Authority of India Result UpdatedAngel BrokingNo ratings yet

- Havells Initiating Coverage 27 Apr 2011Document23 pagesHavells Initiating Coverage 27 Apr 2011ananth999No ratings yet

- Blue Star Limited: Initiating Coverage Report Rating: Strong Buy Target Price: '230Document24 pagesBlue Star Limited: Initiating Coverage Report Rating: Strong Buy Target Price: '230DoraiBalamohanNo ratings yet

- GTL Infrastructure LTD: Key Financial IndicatorsDocument4 pagesGTL Infrastructure LTD: Key Financial IndicatorsMehakBatlaNo ratings yet

- Finolex Cables: Performance HighlightsDocument10 pagesFinolex Cables: Performance HighlightsAngel BrokingNo ratings yet

- Technocraft Industries (India) : Crafting Value Global Leader at Attractive PriceDocument8 pagesTechnocraft Industries (India) : Crafting Value Global Leader at Attractive PricesanjeevpandaNo ratings yet

- Sharekhan Top Picks: October 01, 2011Document7 pagesSharekhan Top Picks: October 01, 2011harsha_iitmNo ratings yet

- Hinduja Ventures Ltd. CMP: Rs. 385.2: Stock Note April 19, 2012Document9 pagesHinduja Ventures Ltd. CMP: Rs. 385.2: Stock Note April 19, 2012rohitcfNo ratings yet

- Honeywell Automation India LTDDocument19 pagesHoneywell Automation India LTDManish BuxiNo ratings yet

- MC 200203 LucasDocument4 pagesMC 200203 LucasArvindkumar ShanmugamNo ratings yet

- Eaton InvestorsDocument42 pagesEaton InvestorsZulfikar GadhiyaNo ratings yet

- Electrical Equipment IndustryDocument3 pagesElectrical Equipment IndustryNamita ChaudharyNo ratings yet

- Exide Industries: Performance HighlightsDocument12 pagesExide Industries: Performance HighlightsAngel BrokingNo ratings yet

- Moulded Case Circuit Breakers, 750 Volts & Below World Summary: Market Sector Values & Financials by CountryFrom EverandMoulded Case Circuit Breakers, 750 Volts & Below World Summary: Market Sector Values & Financials by CountryNo ratings yet

- Nonmetallic Coated Abrasive Products, Buffing & Polishing Wheels & Laps World Summary: Market Sector Values & Financials by CountryFrom EverandNonmetallic Coated Abrasive Products, Buffing & Polishing Wheels & Laps World Summary: Market Sector Values & Financials by CountryNo ratings yet

- Clay Refractory Products World Summary: Market Sector Values & Financials by CountryFrom EverandClay Refractory Products World Summary: Market Sector Values & Financials by CountryNo ratings yet

- CIMA F2 Financial Management Quick Review SlidesDocument50 pagesCIMA F2 Financial Management Quick Review Slidessadiq626No ratings yet

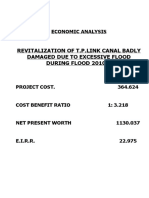

- Revitalization of T.P.Link Canal Badly Damaged Due To Excessive Flood During Flood 2010"Document4 pagesRevitalization of T.P.Link Canal Badly Damaged Due To Excessive Flood During Flood 2010"Xshf AkNo ratings yet

- Accountancy Capital and RevenueDocument3 pagesAccountancy Capital and RevenueJyotti BajajNo ratings yet

- Balance Sheet: Hindalco IndustriesDocument20 pagesBalance Sheet: Hindalco Industriesparinay202No ratings yet

- Accounting/Series 4 2007 (Code3001)Document17 pagesAccounting/Series 4 2007 (Code3001)Hein Linn Kyaw100% (2)

- Test Bank For College Accounting Chapters 1-27-23rd Edition James A Heintz Robert W Parry Full DownloadDocument23 pagesTest Bank For College Accounting Chapters 1-27-23rd Edition James A Heintz Robert W Parry Full Downloadamandadanielsxrngoqkefp100% (46)

- Investment Banking Origination & Advisory TrendsDocument29 pagesInvestment Banking Origination & Advisory TrendsNabhan AhmadNo ratings yet

- Portflio 4Document32 pagesPortflio 4gurudev21No ratings yet

- Merchant BankDocument13 pagesMerchant Bankmdeepak1989No ratings yet

- Chapter 9 - Operations, Dividends, BVPS, & EPSDocument6 pagesChapter 9 - Operations, Dividends, BVPS, & EPSSarah Nicole S. LagrimasNo ratings yet

- Legacy Foreign Public Positions 6-30-20 - PositionsDocument65 pagesLegacy Foreign Public Positions 6-30-20 - PositionsRob PortNo ratings yet

- Tutorial 7 Chapter 15: Cash Conversion CycleDocument8 pagesTutorial 7 Chapter 15: Cash Conversion CycleAlvaroNo ratings yet

- Samudera Indonesia TBK - 31 Mar 2023Document116 pagesSamudera Indonesia TBK - 31 Mar 2023damycenelNo ratings yet

- SM МануалDocument3 pagesSM МануалnaderNo ratings yet

- Jack Poupore Resume NauDocument1 pageJack Poupore Resume Nauapi-302205401No ratings yet

- Rationale in Studying Financial Markets and InstitutionsDocument3 pagesRationale in Studying Financial Markets and InstitutionsGwen AgrimorNo ratings yet

- Foreign Exchange Risk: Foreign Exchange Risk (Also Known As Exchange Rate Risk or Currency Risk) Is ADocument3 pagesForeign Exchange Risk: Foreign Exchange Risk (Also Known As Exchange Rate Risk or Currency Risk) Is ASonali RawatNo ratings yet

- Market Mantra 290719Document13 pagesMarket Mantra 290719Bhavin KariaNo ratings yet

- Vouching and VerificationDocument10 pagesVouching and VerificationSaloni AgarwalNo ratings yet

- Acc 1 Financial Statement Analysis (Part 2)Document27 pagesAcc 1 Financial Statement Analysis (Part 2)juthi rawnakNo ratings yet

- Chapter OneDocument63 pagesChapter OneMeklitNo ratings yet

- Adv Acc-Final-May08Document19 pagesAdv Acc-Final-May08V SwaminathanNo ratings yet

- Valuation Case Study - Mr. Burger.Document1 pageValuation Case Study - Mr. Burger.syed ali mujtabaNo ratings yet

- SAP TcodesDocument47 pagesSAP Tcodesdushyant mudgalNo ratings yet

- White Paper Structured Commodity Strategy Synopsis 2010Document2 pagesWhite Paper Structured Commodity Strategy Synopsis 2010Alexander WoodNo ratings yet

- FIX/FAST Market Data Channel Definitions - PUMA Production EnvironmentDocument4 pagesFIX/FAST Market Data Channel Definitions - PUMA Production EnvironmentVaibhav PoddarNo ratings yet

- Comparitive Analysis of Mutual Funds With Equity Shares Project ReportDocument83 pagesComparitive Analysis of Mutual Funds With Equity Shares Project ReportRaghavendra yadav KM78% (69)

Download as pdf or txt

You might also like

- Case Study - Transaction Exposure - LufthansaDocument2 pagesCase Study - Transaction Exposure - LufthansaRaguRagupathy100% (3)

- Step AcquisitionsDocument7 pagesStep AcquisitionsKelvin Leong100% (1)

- Illustration - Chapter 2Document2 pagesIllustration - Chapter 2Jahzceel CecelNo ratings yet

- Honeywell Automation 2009 ReportDocument4 pagesHoneywell Automation 2009 ReportmworahNo ratings yet

- BPL LTD: Key Financial IndicatorsDocument4 pagesBPL LTD: Key Financial IndicatorsakkuekNo ratings yet

- Havels Most Mar 11Document24 pagesHavels Most Mar 11Ravi SwaminathanNo ratings yet

- Havell Q4 FY2011Document6 pagesHavell Q4 FY2011Tushar DasNo ratings yet

- Manu Mam Term PaperDocument46 pagesManu Mam Term PaperSubodh KumarNo ratings yet

- Finolex Cables, 1Q FY 2014Document14 pagesFinolex Cables, 1Q FY 2014Angel BrokingNo ratings yet

- Havells India LTD - 09042013Document20 pagesHavells India LTD - 09042013shilpaarora988No ratings yet

- Angel Broking: Bharat Heavy ElectricalsDocument27 pagesAngel Broking: Bharat Heavy ElectricalsChintan JethvaNo ratings yet

- Sterlite Technologies Limited (STEOPT) : Well Placed in High Growth MarketsDocument25 pagesSterlite Technologies Limited (STEOPT) : Well Placed in High Growth Marketssourabh_chowdhury_1No ratings yet

- Market Outlook 27th February 2012Document5 pagesMarket Outlook 27th February 2012Angel BrokingNo ratings yet

- Havells India LTD: Market Data Buy Target Price: Rs 500 Investment RationaleDocument6 pagesHavells India LTD: Market Data Buy Target Price: Rs 500 Investment Rationalenalinschwarz123No ratings yet

- Salzer-Electronics-Limited 495 InitiatingCoverageDocument12 pagesSalzer-Electronics-Limited 495 InitiatingCoveragemayur_sgNo ratings yet

- Atul LTDDocument4 pagesAtul LTDFast SwiftNo ratings yet

- Reliance Communications LTDDocument4 pagesReliance Communications LTDSahil JainNo ratings yet

- Elantas BeckDocument6 pagesElantas Beckvivek dkrpuNo ratings yet

- Havells Final ProjectDocument17 pagesHavells Final Projectsimran agarwalNo ratings yet

- Quant Havells Initiating CoverageDocument26 pagesQuant Havells Initiating CoverageviralnshahNo ratings yet

- Havells India June 2012Document20 pagesHavells India June 2012VikramGhatgeNo ratings yet

- Blue Dart Express LTD: Key Financial IndicatorsDocument4 pagesBlue Dart Express LTD: Key Financial IndicatorsSagar DholeNo ratings yet

- KEC International, 4th February, 2013Document11 pagesKEC International, 4th February, 2013Angel BrokingNo ratings yet

- Havells India Jan 09 Fairwealth Securities Initiate-Buy Target280Document9 pagesHavells India Jan 09 Fairwealth Securities Initiate-Buy Target280Sovid Gupta100% (1)

- Market Outlook 11th October 2011Document5 pagesMarket Outlook 11th October 2011Angel BrokingNo ratings yet

- BYD Annual Report 2011Document106 pagesBYD Annual Report 2011krabadiNo ratings yet

- Company Presentation September 2010 PDFDocument20 pagesCompany Presentation September 2010 PDFsonar_neelNo ratings yet

- Thermax: Performance HighlightsDocument10 pagesThermax: Performance HighlightsAngel BrokingNo ratings yet

- Market Outlook 2nd December 2011Document6 pagesMarket Outlook 2nd December 2011Angel BrokingNo ratings yet

- Project Report On VodafoneDocument11 pagesProject Report On Vodafoneanshul_kh29150% (1)

- Larsen & ToubroDocument15 pagesLarsen & ToubroAngel BrokingNo ratings yet

- C&S Electric Limited: Rating History Instrument Rating Outstanding Previous Ratings March, 2010 September, 2008Document4 pagesC&S Electric Limited: Rating History Instrument Rating Outstanding Previous Ratings March, 2010 September, 2008sgoswami_1No ratings yet

- 5.4 Rashtriya Ispat Nigam LTD.: Performance HighlightsDocument2 pages5.4 Rashtriya Ispat Nigam LTD.: Performance HighlightsRavi ChandNo ratings yet

- Havells India LimitedDocument15 pagesHavells India LimitedRohit PandeyNo ratings yet

- Fie M Industries LimitedDocument4 pagesFie M Industries LimitedDavuluri OmprakashNo ratings yet

- Videocon Industries LTD: Key Financial IndicatorsDocument4 pagesVideocon Industries LTD: Key Financial IndicatorsryreddyNo ratings yet

- Steel Authority of IndiaDocument13 pagesSteel Authority of IndiaAngel BrokingNo ratings yet

- YTL Power IC - 20070912 - Global Utility PlayDocument18 pagesYTL Power IC - 20070912 - Global Utility PlayMuhamad Firdaus MinhadNo ratings yet

- Rakon Announcement 14 Feb 08Document6 pagesRakon Announcement 14 Feb 08Peter CorbanNo ratings yet

- Trends in Public and Private Sector in India 2381Document29 pagesTrends in Public and Private Sector in India 2381Munish NagarNo ratings yet

- Performance Highlights: NeutralDocument11 pagesPerformance Highlights: NeutralAngel BrokingNo ratings yet

- Mid Cap Ideas - Value and Growth Investing 250112 - 11 - 0602120242Document21 pagesMid Cap Ideas - Value and Growth Investing 250112 - 11 - 0602120242Chetan MaheshwariNo ratings yet

- Apar IndustriesDocument16 pagesApar Industriesh_o_mNo ratings yet

- A Global Air Conditioning and Engineering Services CompanyDocument50 pagesA Global Air Conditioning and Engineering Services Companyraj_mrecj6511No ratings yet

- Sharp Corporation: Company ProfileDocument9 pagesSharp Corporation: Company ProfileVivi Sabrina BaswedanNo ratings yet

- Bhel Group 1Document16 pagesBhel Group 1arijitguha07No ratings yet

- HavellsDocument20 pagesHavellsvraj.patelsmpic090No ratings yet

- Steel Authority of India Result UpdatedDocument13 pagesSteel Authority of India Result UpdatedAngel BrokingNo ratings yet

- Havells Initiating Coverage 27 Apr 2011Document23 pagesHavells Initiating Coverage 27 Apr 2011ananth999No ratings yet

- Blue Star Limited: Initiating Coverage Report Rating: Strong Buy Target Price: '230Document24 pagesBlue Star Limited: Initiating Coverage Report Rating: Strong Buy Target Price: '230DoraiBalamohanNo ratings yet

- GTL Infrastructure LTD: Key Financial IndicatorsDocument4 pagesGTL Infrastructure LTD: Key Financial IndicatorsMehakBatlaNo ratings yet

- Finolex Cables: Performance HighlightsDocument10 pagesFinolex Cables: Performance HighlightsAngel BrokingNo ratings yet

- Technocraft Industries (India) : Crafting Value Global Leader at Attractive PriceDocument8 pagesTechnocraft Industries (India) : Crafting Value Global Leader at Attractive PricesanjeevpandaNo ratings yet

- Sharekhan Top Picks: October 01, 2011Document7 pagesSharekhan Top Picks: October 01, 2011harsha_iitmNo ratings yet

- Hinduja Ventures Ltd. CMP: Rs. 385.2: Stock Note April 19, 2012Document9 pagesHinduja Ventures Ltd. CMP: Rs. 385.2: Stock Note April 19, 2012rohitcfNo ratings yet

- Honeywell Automation India LTDDocument19 pagesHoneywell Automation India LTDManish BuxiNo ratings yet

- MC 200203 LucasDocument4 pagesMC 200203 LucasArvindkumar ShanmugamNo ratings yet

- Eaton InvestorsDocument42 pagesEaton InvestorsZulfikar GadhiyaNo ratings yet

- Electrical Equipment IndustryDocument3 pagesElectrical Equipment IndustryNamita ChaudharyNo ratings yet

- Exide Industries: Performance HighlightsDocument12 pagesExide Industries: Performance HighlightsAngel BrokingNo ratings yet

- Moulded Case Circuit Breakers, 750 Volts & Below World Summary: Market Sector Values & Financials by CountryFrom EverandMoulded Case Circuit Breakers, 750 Volts & Below World Summary: Market Sector Values & Financials by CountryNo ratings yet

- Nonmetallic Coated Abrasive Products, Buffing & Polishing Wheels & Laps World Summary: Market Sector Values & Financials by CountryFrom EverandNonmetallic Coated Abrasive Products, Buffing & Polishing Wheels & Laps World Summary: Market Sector Values & Financials by CountryNo ratings yet

- Clay Refractory Products World Summary: Market Sector Values & Financials by CountryFrom EverandClay Refractory Products World Summary: Market Sector Values & Financials by CountryNo ratings yet

- CIMA F2 Financial Management Quick Review SlidesDocument50 pagesCIMA F2 Financial Management Quick Review Slidessadiq626No ratings yet

- Revitalization of T.P.Link Canal Badly Damaged Due To Excessive Flood During Flood 2010"Document4 pagesRevitalization of T.P.Link Canal Badly Damaged Due To Excessive Flood During Flood 2010"Xshf AkNo ratings yet

- Accountancy Capital and RevenueDocument3 pagesAccountancy Capital and RevenueJyotti BajajNo ratings yet

- Balance Sheet: Hindalco IndustriesDocument20 pagesBalance Sheet: Hindalco Industriesparinay202No ratings yet

- Accounting/Series 4 2007 (Code3001)Document17 pagesAccounting/Series 4 2007 (Code3001)Hein Linn Kyaw100% (2)

- Test Bank For College Accounting Chapters 1-27-23rd Edition James A Heintz Robert W Parry Full DownloadDocument23 pagesTest Bank For College Accounting Chapters 1-27-23rd Edition James A Heintz Robert W Parry Full Downloadamandadanielsxrngoqkefp100% (46)

- Investment Banking Origination & Advisory TrendsDocument29 pagesInvestment Banking Origination & Advisory TrendsNabhan AhmadNo ratings yet

- Portflio 4Document32 pagesPortflio 4gurudev21No ratings yet

- Merchant BankDocument13 pagesMerchant Bankmdeepak1989No ratings yet

- Chapter 9 - Operations, Dividends, BVPS, & EPSDocument6 pagesChapter 9 - Operations, Dividends, BVPS, & EPSSarah Nicole S. LagrimasNo ratings yet

- Legacy Foreign Public Positions 6-30-20 - PositionsDocument65 pagesLegacy Foreign Public Positions 6-30-20 - PositionsRob PortNo ratings yet

- Tutorial 7 Chapter 15: Cash Conversion CycleDocument8 pagesTutorial 7 Chapter 15: Cash Conversion CycleAlvaroNo ratings yet

- Samudera Indonesia TBK - 31 Mar 2023Document116 pagesSamudera Indonesia TBK - 31 Mar 2023damycenelNo ratings yet

- SM МануалDocument3 pagesSM МануалnaderNo ratings yet

- Jack Poupore Resume NauDocument1 pageJack Poupore Resume Nauapi-302205401No ratings yet

- Rationale in Studying Financial Markets and InstitutionsDocument3 pagesRationale in Studying Financial Markets and InstitutionsGwen AgrimorNo ratings yet

- Foreign Exchange Risk: Foreign Exchange Risk (Also Known As Exchange Rate Risk or Currency Risk) Is ADocument3 pagesForeign Exchange Risk: Foreign Exchange Risk (Also Known As Exchange Rate Risk or Currency Risk) Is ASonali RawatNo ratings yet

- Market Mantra 290719Document13 pagesMarket Mantra 290719Bhavin KariaNo ratings yet

- Vouching and VerificationDocument10 pagesVouching and VerificationSaloni AgarwalNo ratings yet

- Acc 1 Financial Statement Analysis (Part 2)Document27 pagesAcc 1 Financial Statement Analysis (Part 2)juthi rawnakNo ratings yet

- Chapter OneDocument63 pagesChapter OneMeklitNo ratings yet

- Adv Acc-Final-May08Document19 pagesAdv Acc-Final-May08V SwaminathanNo ratings yet

- Valuation Case Study - Mr. Burger.Document1 pageValuation Case Study - Mr. Burger.syed ali mujtabaNo ratings yet

- SAP TcodesDocument47 pagesSAP Tcodesdushyant mudgalNo ratings yet

- White Paper Structured Commodity Strategy Synopsis 2010Document2 pagesWhite Paper Structured Commodity Strategy Synopsis 2010Alexander WoodNo ratings yet

- FIX/FAST Market Data Channel Definitions - PUMA Production EnvironmentDocument4 pagesFIX/FAST Market Data Channel Definitions - PUMA Production EnvironmentVaibhav PoddarNo ratings yet

- Comparitive Analysis of Mutual Funds With Equity Shares Project ReportDocument83 pagesComparitive Analysis of Mutual Funds With Equity Shares Project ReportRaghavendra yadav KM78% (69)