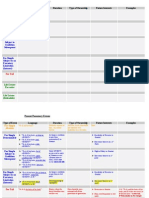

Basics - Formation, Planning, Representing, Documents Constituents

Basics - Formation, Planning, Representing, Documents Constituents

You might also like

- Pli Mpre Exam 1 2003Document16 pagesPli Mpre Exam 1 2003thanhdra0% (2)

- Corporations Outline Partnoy PalmiterDocument20 pagesCorporations Outline Partnoy PalmiterMatt ToothacreNo ratings yet

- Pepsi CoDocument3 pagesPepsi CoCH Hanzala AmjadNo ratings yet

- Marshall Chapter 3 Case StudyDocument2 pagesMarshall Chapter 3 Case Studyapi-3173686540% (1)

- Torts OutlineDocument16 pagesTorts OutlineHenryNo ratings yet

- Corporations, Kraakman, Fall 2012Document61 pagesCorporations, Kraakman, Fall 2012Chaim SchwarzNo ratings yet

- HypotheticalsDocument20 pagesHypotheticalsCory BakerNo ratings yet

- Contracts II OutlineDocument79 pagesContracts II Outlinenathanlawschool100% (1)

- Armour - Corporations - 2009F - Allen Kraakman Subramian 3rdDocument153 pagesArmour - Corporations - 2009F - Allen Kraakman Subramian 3rdSimon Hsien-Wen HsiaoNo ratings yet

- Torts Outline Mortazavi 2013Document19 pagesTorts Outline Mortazavi 2013deenydoll4125No ratings yet

- Transformational Company GuideDocument109 pagesTransformational Company Guidesukush100% (1)

- Case Study Corwin CorporationDocument13 pagesCase Study Corwin CorporationChirag Shah100% (1)

- Executive SummaryDocument15 pagesExecutive SummaryNattNo ratings yet

- IL Corporations Bar OutlineDocument8 pagesIL Corporations Bar OutlineJulia NiebrzydowskiNo ratings yet

- Business Organizations: Outlines and Case Summaries: Law School Survival Guides, #10From EverandBusiness Organizations: Outlines and Case Summaries: Law School Survival Guides, #10No ratings yet

- Student Supplementary Materials Answers To Test Yourself QuestionsDocument118 pagesStudent Supplementary Materials Answers To Test Yourself Questionsmilk teaNo ratings yet

- Torts OutlineDocument15 pagesTorts OutlineMichael SantosNo ratings yet

- Business Associations Outline I. Entity Forms 1. S P O ODocument29 pagesBusiness Associations Outline I. Entity Forms 1. S P O OMattie ParkerNo ratings yet

- Constitutional Law I Funk 2005docDocument24 pagesConstitutional Law I Funk 2005docLaura SkaarNo ratings yet

- Family Law OutlineDocument18 pagesFamily Law OutlineBill TrecoNo ratings yet

- I. The Supreme Court Rises: (Conservative)Document8 pagesI. The Supreme Court Rises: (Conservative)izdr1No ratings yet

- Contracts 2 Outline Spring20Document66 pagesContracts 2 Outline Spring20Amelia PooreNo ratings yet

- Biz Orgs Outline: ÑelationshipsDocument26 pagesBiz Orgs Outline: ÑelationshipsTyler PritchettNo ratings yet

- Analysis Under The State Action DoctrineDocument2 pagesAnalysis Under The State Action Doctrinejdav456No ratings yet

- Civil Procedure Outline Part VI: Erie DoctrineDocument6 pagesCivil Procedure Outline Part VI: Erie DoctrineMorgyn Shae CooperNo ratings yet

- Chapter 1: The Federal Judicial Power A. The Authority For Judicial ReviewDocument28 pagesChapter 1: The Federal Judicial Power A. The Authority For Judicial ReviewNicole AmaranteNo ratings yet

- Business Associations OutlineDocument52 pagesBusiness Associations OutlineChi Wen YeoNo ratings yet

- Business OrganizationsDocument71 pagesBusiness Organizationsjdadas100% (2)

- Labor LawDocument91 pagesLabor Lawmaxcharlie1100% (1)

- Estates QuizDocument2 pagesEstates Quizasebeo1No ratings yet

- Torts OutlineDocument78 pagesTorts Outlineblair_bartonNo ratings yet

- Conflicts of Laws OutlineDocument56 pagesConflicts of Laws Outlinekristin1717No ratings yet

- Agencyandpartnership 12712275603502 Phpapp01Document48 pagesAgencyandpartnership 12712275603502 Phpapp01Atif AshrafNo ratings yet

- Con Law OutlineDocument18 pagesCon Law OutlineJane MullisNo ratings yet

- Con OutlineDocument98 pagesCon OutlineRick CoyleNo ratings yet

- Ethics OutlineDocument35 pagesEthics OutlinePaul UlitskyNo ratings yet

- Rincipal Gent Iability IN ORT: UnlessDocument4 pagesRincipal Gent Iability IN ORT: UnlessLaura CNo ratings yet

- Con Law Short OutlineDocument17 pagesCon Law Short OutlineJennifer IsaacsNo ratings yet

- First Amendment: Is There State Action Regulating Speech?Document1 pageFirst Amendment: Is There State Action Regulating Speech?rhdrucker113084No ratings yet

- Constitutional Law OutlineDocument41 pagesConstitutional Law OutlineLaura SkaarNo ratings yet

- Business Associations I - Preliminary VersionDocument10 pagesBusiness Associations I - Preliminary Versionlogan doopNo ratings yet

- Professional Responsibility MaymesterDocument64 pagesProfessional Responsibility MaymesterSierra ChildersNo ratings yet

- Professional Responsibility OutlineDocument38 pagesProfessional Responsibility Outlineprentice brown50% (2)

- Hybrid OutlineDocument24 pagesHybrid OutlineAaron FlemingNo ratings yet

- Con Law Outline - Fall 2011 SeamanDocument30 pagesCon Law Outline - Fall 2011 Seamanzoti_lejdi100% (1)

- Civil Procedure OutlineDocument25 pagesCivil Procedure OutlineElNo ratings yet

- Con Law OutlineDocument48 pagesCon Law OutlineSeth WalkerNo ratings yet

- Really Good Prop OutlineDocument60 pagesReally Good Prop OutlineJustin Wilson100% (3)

- Biz Orgs OutlineDocument74 pagesBiz Orgs OutlineRonnie Barcena Jr.No ratings yet

- Domestic Relations - OutlineDocument15 pagesDomestic Relations - Outlinejsara1180No ratings yet

- CivPro OutlineDocument238 pagesCivPro OutlineNoam LiranNo ratings yet

- Accomplice Common LawDocument1 pageAccomplice Common LawLiliane KimNo ratings yet

- Family Law - Stein Fall 2011 Outline FINALDocument93 pagesFamily Law - Stein Fall 2011 Outline FINALbiglank99No ratings yet

- BA Outline - OKellyDocument69 pagesBA Outline - OKellylshahNo ratings yet

- Con Question OutlineDocument5 pagesCon Question OutlineKeiara PatherNo ratings yet

- Con Law Outline-29Document41 pagesCon Law Outline-29Scott HymanNo ratings yet

- Con Law I Final Cheat SheetDocument3 pagesCon Law I Final Cheat SheetKathryn CzekalskiNo ratings yet

- Prop I Attack Outline Ehrlich 2014Document6 pagesProp I Attack Outline Ehrlich 2014superxl2009No ratings yet

- Con Law II Outline PKDocument106 pagesCon Law II Outline PKSasha DadanNo ratings yet

- Con Law OutlineDocument72 pagesCon Law OutlineAdam DippelNo ratings yet

- Entity ComparisonDocument3 pagesEntity Comparisoncthunder_1No ratings yet

- Fall 2011 Exam Model Answers and Feedback MemoDocument47 pagesFall 2011 Exam Model Answers and Feedback MemotcsNo ratings yet

- Property Law Model AnswersDocument12 pagesProperty Law Model AnswersAlexNo ratings yet

- Mortgages OutlineDocument54 pagesMortgages OutlineJames HrissikopoulosNo ratings yet

- MPRE Unpacked: Professional Responsibility Explained & Applied for Multistate Professional Responsibility ExamFrom EverandMPRE Unpacked: Professional Responsibility Explained & Applied for Multistate Professional Responsibility ExamNo ratings yet

- Chapter 2 Business EthicsDocument36 pagesChapter 2 Business EthicsnayabNo ratings yet

- Project Management For ManagersDocument22 pagesProject Management For ManagersBiswanathMudiNo ratings yet

- ByeDocument12 pagesByeRaprap FernandezNo ratings yet

- Manage Platform DemandDocument18 pagesManage Platform DemandNoorNo ratings yet

- CFAP 3 - Study Manual (Final)Document243 pagesCFAP 3 - Study Manual (Final)danishjaved133841No ratings yet

- Strategic Management: Fall 2020 Lecture 11 02 December Associate Professor Nazlee Siddiqui North South UniversityDocument17 pagesStrategic Management: Fall 2020 Lecture 11 02 December Associate Professor Nazlee Siddiqui North South UniversityRedwan RahmanNo ratings yet

- Project Based OrganizationsDocument6 pagesProject Based OrganizationsClaudia TomaNo ratings yet

- Carporate Social ResponsibilityDocument58 pagesCarporate Social ResponsibilitySri KamalNo ratings yet

- Scheme of Work: Cambridge IGCSE / Cambridge IGCSE (9 1) Business Studies 0450 / 0986Document45 pagesScheme of Work: Cambridge IGCSE / Cambridge IGCSE (9 1) Business Studies 0450 / 0986Rico C. FranszNo ratings yet

- Barclays 2007Document79 pagesBarclays 2007Cetty RotondoNo ratings yet

- C01 Mini Case Porsche 1Document17 pagesC01 Mini Case Porsche 1c3564430No ratings yet

- Assist. Ph.D. Student Bocean Claudiu University of Craiova Faculty of Economics and Business Administration Craiova, RomaniaDocument6 pagesAssist. Ph.D. Student Bocean Claudiu University of Craiova Faculty of Economics and Business Administration Craiova, RomaniaDana MoraruNo ratings yet

- Unit 1 Introduction To EthicsDocument54 pagesUnit 1 Introduction To EthicsDivya NabarNo ratings yet

- Understanding Management'S Context: Constraints and ChallengesDocument23 pagesUnderstanding Management'S Context: Constraints and ChallengesMehranisLiveNo ratings yet

- Managing Within The Dynamic Business Environment: Taking Risks and Making ProfitsDocument20 pagesManaging Within The Dynamic Business Environment: Taking Risks and Making ProfitsRafayet Omar Shuvo100% (1)

- Four Faces of Corporate CitizenshipDocument7 pagesFour Faces of Corporate CitizenshipAbbey ZhangNo ratings yet

- Enron Case Study Questions PDFDocument6 pagesEnron Case Study Questions PDFSree Mathi SuntheriNo ratings yet

- Managing For StakeholdersDocument58 pagesManaging For StakeholdersNicacio LucenaNo ratings yet

- MiM Thesis 2017 - Alexia Twingler and PriscillDocument64 pagesMiM Thesis 2017 - Alexia Twingler and PriscillPierre WoodmanNo ratings yet

- CDI-T 5th Management (1-12)Document124 pagesCDI-T 5th Management (1-12)Felipe CamposNo ratings yet

- Flyer Triplet A4 V3Document2 pagesFlyer Triplet A4 V3Gisela GoncalvesNo ratings yet

- Corporate Social ResponsibilityDocument26 pagesCorporate Social ResponsibilityIfemideNo ratings yet

- The CEO Report v2 PDFDocument36 pagesThe CEO Report v2 PDFplanet_o100% (1)

- SM Quiz1Document4 pagesSM Quiz1Ah BiiNo ratings yet

- Project Stakeholders ManagementDocument24 pagesProject Stakeholders ManagementmukhlisNo ratings yet

Download as docx, pdf, or txt

You might also like

- Pli Mpre Exam 1 2003Document16 pagesPli Mpre Exam 1 2003thanhdra0% (2)

- Corporations Outline Partnoy PalmiterDocument20 pagesCorporations Outline Partnoy PalmiterMatt ToothacreNo ratings yet

- Pepsi CoDocument3 pagesPepsi CoCH Hanzala AmjadNo ratings yet

- Marshall Chapter 3 Case StudyDocument2 pagesMarshall Chapter 3 Case Studyapi-3173686540% (1)

- Torts OutlineDocument16 pagesTorts OutlineHenryNo ratings yet

- Corporations, Kraakman, Fall 2012Document61 pagesCorporations, Kraakman, Fall 2012Chaim SchwarzNo ratings yet

- HypotheticalsDocument20 pagesHypotheticalsCory BakerNo ratings yet

- Contracts II OutlineDocument79 pagesContracts II Outlinenathanlawschool100% (1)

- Armour - Corporations - 2009F - Allen Kraakman Subramian 3rdDocument153 pagesArmour - Corporations - 2009F - Allen Kraakman Subramian 3rdSimon Hsien-Wen HsiaoNo ratings yet

- Torts Outline Mortazavi 2013Document19 pagesTorts Outline Mortazavi 2013deenydoll4125No ratings yet

- Transformational Company GuideDocument109 pagesTransformational Company Guidesukush100% (1)

- Case Study Corwin CorporationDocument13 pagesCase Study Corwin CorporationChirag Shah100% (1)

- Executive SummaryDocument15 pagesExecutive SummaryNattNo ratings yet

- IL Corporations Bar OutlineDocument8 pagesIL Corporations Bar OutlineJulia NiebrzydowskiNo ratings yet

- Business Organizations: Outlines and Case Summaries: Law School Survival Guides, #10From EverandBusiness Organizations: Outlines and Case Summaries: Law School Survival Guides, #10No ratings yet

- Student Supplementary Materials Answers To Test Yourself QuestionsDocument118 pagesStudent Supplementary Materials Answers To Test Yourself Questionsmilk teaNo ratings yet

- Torts OutlineDocument15 pagesTorts OutlineMichael SantosNo ratings yet

- Business Associations Outline I. Entity Forms 1. S P O ODocument29 pagesBusiness Associations Outline I. Entity Forms 1. S P O OMattie ParkerNo ratings yet

- Constitutional Law I Funk 2005docDocument24 pagesConstitutional Law I Funk 2005docLaura SkaarNo ratings yet

- Family Law OutlineDocument18 pagesFamily Law OutlineBill TrecoNo ratings yet

- I. The Supreme Court Rises: (Conservative)Document8 pagesI. The Supreme Court Rises: (Conservative)izdr1No ratings yet

- Contracts 2 Outline Spring20Document66 pagesContracts 2 Outline Spring20Amelia PooreNo ratings yet

- Biz Orgs Outline: ÑelationshipsDocument26 pagesBiz Orgs Outline: ÑelationshipsTyler PritchettNo ratings yet

- Analysis Under The State Action DoctrineDocument2 pagesAnalysis Under The State Action Doctrinejdav456No ratings yet

- Civil Procedure Outline Part VI: Erie DoctrineDocument6 pagesCivil Procedure Outline Part VI: Erie DoctrineMorgyn Shae CooperNo ratings yet

- Chapter 1: The Federal Judicial Power A. The Authority For Judicial ReviewDocument28 pagesChapter 1: The Federal Judicial Power A. The Authority For Judicial ReviewNicole AmaranteNo ratings yet

- Business Associations OutlineDocument52 pagesBusiness Associations OutlineChi Wen YeoNo ratings yet

- Business OrganizationsDocument71 pagesBusiness Organizationsjdadas100% (2)

- Labor LawDocument91 pagesLabor Lawmaxcharlie1100% (1)

- Estates QuizDocument2 pagesEstates Quizasebeo1No ratings yet

- Torts OutlineDocument78 pagesTorts Outlineblair_bartonNo ratings yet

- Conflicts of Laws OutlineDocument56 pagesConflicts of Laws Outlinekristin1717No ratings yet

- Agencyandpartnership 12712275603502 Phpapp01Document48 pagesAgencyandpartnership 12712275603502 Phpapp01Atif AshrafNo ratings yet

- Con Law OutlineDocument18 pagesCon Law OutlineJane MullisNo ratings yet

- Con OutlineDocument98 pagesCon OutlineRick CoyleNo ratings yet

- Ethics OutlineDocument35 pagesEthics OutlinePaul UlitskyNo ratings yet

- Rincipal Gent Iability IN ORT: UnlessDocument4 pagesRincipal Gent Iability IN ORT: UnlessLaura CNo ratings yet

- Con Law Short OutlineDocument17 pagesCon Law Short OutlineJennifer IsaacsNo ratings yet

- First Amendment: Is There State Action Regulating Speech?Document1 pageFirst Amendment: Is There State Action Regulating Speech?rhdrucker113084No ratings yet

- Constitutional Law OutlineDocument41 pagesConstitutional Law OutlineLaura SkaarNo ratings yet

- Business Associations I - Preliminary VersionDocument10 pagesBusiness Associations I - Preliminary Versionlogan doopNo ratings yet

- Professional Responsibility MaymesterDocument64 pagesProfessional Responsibility MaymesterSierra ChildersNo ratings yet

- Professional Responsibility OutlineDocument38 pagesProfessional Responsibility Outlineprentice brown50% (2)

- Hybrid OutlineDocument24 pagesHybrid OutlineAaron FlemingNo ratings yet

- Con Law Outline - Fall 2011 SeamanDocument30 pagesCon Law Outline - Fall 2011 Seamanzoti_lejdi100% (1)

- Civil Procedure OutlineDocument25 pagesCivil Procedure OutlineElNo ratings yet

- Con Law OutlineDocument48 pagesCon Law OutlineSeth WalkerNo ratings yet

- Really Good Prop OutlineDocument60 pagesReally Good Prop OutlineJustin Wilson100% (3)

- Biz Orgs OutlineDocument74 pagesBiz Orgs OutlineRonnie Barcena Jr.No ratings yet

- Domestic Relations - OutlineDocument15 pagesDomestic Relations - Outlinejsara1180No ratings yet

- CivPro OutlineDocument238 pagesCivPro OutlineNoam LiranNo ratings yet

- Accomplice Common LawDocument1 pageAccomplice Common LawLiliane KimNo ratings yet

- Family Law - Stein Fall 2011 Outline FINALDocument93 pagesFamily Law - Stein Fall 2011 Outline FINALbiglank99No ratings yet

- BA Outline - OKellyDocument69 pagesBA Outline - OKellylshahNo ratings yet

- Con Question OutlineDocument5 pagesCon Question OutlineKeiara PatherNo ratings yet

- Con Law Outline-29Document41 pagesCon Law Outline-29Scott HymanNo ratings yet

- Con Law I Final Cheat SheetDocument3 pagesCon Law I Final Cheat SheetKathryn CzekalskiNo ratings yet

- Prop I Attack Outline Ehrlich 2014Document6 pagesProp I Attack Outline Ehrlich 2014superxl2009No ratings yet

- Con Law II Outline PKDocument106 pagesCon Law II Outline PKSasha DadanNo ratings yet

- Con Law OutlineDocument72 pagesCon Law OutlineAdam DippelNo ratings yet

- Entity ComparisonDocument3 pagesEntity Comparisoncthunder_1No ratings yet

- Fall 2011 Exam Model Answers and Feedback MemoDocument47 pagesFall 2011 Exam Model Answers and Feedback MemotcsNo ratings yet

- Property Law Model AnswersDocument12 pagesProperty Law Model AnswersAlexNo ratings yet

- Mortgages OutlineDocument54 pagesMortgages OutlineJames HrissikopoulosNo ratings yet

- MPRE Unpacked: Professional Responsibility Explained & Applied for Multistate Professional Responsibility ExamFrom EverandMPRE Unpacked: Professional Responsibility Explained & Applied for Multistate Professional Responsibility ExamNo ratings yet

- Chapter 2 Business EthicsDocument36 pagesChapter 2 Business EthicsnayabNo ratings yet

- Project Management For ManagersDocument22 pagesProject Management For ManagersBiswanathMudiNo ratings yet

- ByeDocument12 pagesByeRaprap FernandezNo ratings yet

- Manage Platform DemandDocument18 pagesManage Platform DemandNoorNo ratings yet

- CFAP 3 - Study Manual (Final)Document243 pagesCFAP 3 - Study Manual (Final)danishjaved133841No ratings yet

- Strategic Management: Fall 2020 Lecture 11 02 December Associate Professor Nazlee Siddiqui North South UniversityDocument17 pagesStrategic Management: Fall 2020 Lecture 11 02 December Associate Professor Nazlee Siddiqui North South UniversityRedwan RahmanNo ratings yet

- Project Based OrganizationsDocument6 pagesProject Based OrganizationsClaudia TomaNo ratings yet

- Carporate Social ResponsibilityDocument58 pagesCarporate Social ResponsibilitySri KamalNo ratings yet

- Scheme of Work: Cambridge IGCSE / Cambridge IGCSE (9 1) Business Studies 0450 / 0986Document45 pagesScheme of Work: Cambridge IGCSE / Cambridge IGCSE (9 1) Business Studies 0450 / 0986Rico C. FranszNo ratings yet

- Barclays 2007Document79 pagesBarclays 2007Cetty RotondoNo ratings yet

- C01 Mini Case Porsche 1Document17 pagesC01 Mini Case Porsche 1c3564430No ratings yet

- Assist. Ph.D. Student Bocean Claudiu University of Craiova Faculty of Economics and Business Administration Craiova, RomaniaDocument6 pagesAssist. Ph.D. Student Bocean Claudiu University of Craiova Faculty of Economics and Business Administration Craiova, RomaniaDana MoraruNo ratings yet

- Unit 1 Introduction To EthicsDocument54 pagesUnit 1 Introduction To EthicsDivya NabarNo ratings yet

- Understanding Management'S Context: Constraints and ChallengesDocument23 pagesUnderstanding Management'S Context: Constraints and ChallengesMehranisLiveNo ratings yet

- Managing Within The Dynamic Business Environment: Taking Risks and Making ProfitsDocument20 pagesManaging Within The Dynamic Business Environment: Taking Risks and Making ProfitsRafayet Omar Shuvo100% (1)

- Four Faces of Corporate CitizenshipDocument7 pagesFour Faces of Corporate CitizenshipAbbey ZhangNo ratings yet

- Enron Case Study Questions PDFDocument6 pagesEnron Case Study Questions PDFSree Mathi SuntheriNo ratings yet

- Managing For StakeholdersDocument58 pagesManaging For StakeholdersNicacio LucenaNo ratings yet

- MiM Thesis 2017 - Alexia Twingler and PriscillDocument64 pagesMiM Thesis 2017 - Alexia Twingler and PriscillPierre WoodmanNo ratings yet

- CDI-T 5th Management (1-12)Document124 pagesCDI-T 5th Management (1-12)Felipe CamposNo ratings yet

- Flyer Triplet A4 V3Document2 pagesFlyer Triplet A4 V3Gisela GoncalvesNo ratings yet

- Corporate Social ResponsibilityDocument26 pagesCorporate Social ResponsibilityIfemideNo ratings yet

- The CEO Report v2 PDFDocument36 pagesThe CEO Report v2 PDFplanet_o100% (1)

- SM Quiz1Document4 pagesSM Quiz1Ah BiiNo ratings yet

- Project Stakeholders ManagementDocument24 pagesProject Stakeholders ManagementmukhlisNo ratings yet