Download as pdf or txt

You might also like

- Past BillsDocument39 pagesPast BillsSal Salas100% (3)

- PastBills PDFDocument37 pagesPastBills PDFKhanhNo ratings yet

- Oct Bank - NewDocument7 pagesOct Bank - NewLisa Hester100% (1)

- Consumer Wireless 021711Document4 pagesConsumer Wireless 021711AndreHendricksNo ratings yet

- StatementDocument20 pagesStatementLevi Paul OrlickNo ratings yet

- ATT 298066469287 20140216 FebDocument10 pagesATT 298066469287 20140216 FebDixit ManishNo ratings yet

- BUS345 Midterm 1 NotesDocument31 pagesBUS345 Midterm 1 NotesՄարիա ՄինասեանNo ratings yet

- Court Documents Filed by Gary Thibodeau's AttorneysDocument192 pagesCourt Documents Filed by Gary Thibodeau's AttorneysTime Warner Cable News100% (1)

- Ils Cat II-III ChecksDocument2 pagesIls Cat II-III ChecksEnrique Corvalán HernándezNo ratings yet

- California Cities and County Sales and Use Tax Rates 2012Document23 pagesCalifornia Cities and County Sales and Use Tax Rates 2012L. A. PatersonNo ratings yet

- Sales and Use Tax Guide: February 2011Document52 pagesSales and Use Tax Guide: February 2011dinkemNo ratings yet

- Sales and Use Tax in Maryland Presentation To Legislature 20110726Document29 pagesSales and Use Tax in Maryland Presentation To Legislature 20110726Paul MastersNo ratings yet

- Filing Instructions: Please Follow These Instructions CarefullyDocument4 pagesFiling Instructions: Please Follow These Instructions CarefullyMafer ChavezNo ratings yet

- Sales Tax FormDocument4 pagesSales Tax FormzilchhourNo ratings yet

- 5891 14342821954Document16 pages5891 14342821954rachelj_85No ratings yet

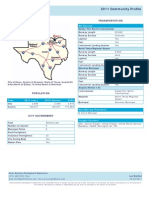

- 2011 Ladonia ProfileDocument5 pages2011 Ladonia ProfileTCOG Community & Economic DevelopmentNo ratings yet

- Chris Fick League of Oregon Cities Mayors Open Forum September 27, 2012Document20 pagesChris Fick League of Oregon Cities Mayors Open Forum September 27, 2012Statesman JournalNo ratings yet

- BOE Letter To Taxpayers Informing Them of Use TaxDocument1 pageBOE Letter To Taxpayers Informing Them of Use TaxDavid DuranNo ratings yet

- California City and County Sales and Use Tax Rates: California State Board of EqualizationDocument23 pagesCalifornia City and County Sales and Use Tax Rates: California State Board of Equalizationapi-2494755100% (2)

- Fiscal Sustainability Analysis: Nassau CountyDocument22 pagesFiscal Sustainability Analysis: Nassau Countyapi-298511181No ratings yet

- Do Not Call Data: National RegistryDocument24 pagesDo Not Call Data: National RegistryMark ReinhardtNo ratings yet

- Business Permitting and Licensing SystemDocument13 pagesBusiness Permitting and Licensing SystemCharlie C. BastidaNo ratings yet

- Property Tax Reform PresentationDocument29 pagesProperty Tax Reform PresentationStatesman JournalNo ratings yet

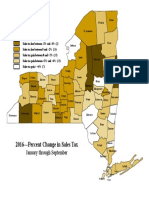

- Map of Sales TaxDocument1 pageMap of Sales TaxrkarlinNo ratings yet

- State Tax GuideDocument158 pagesState Tax GuidecamatnguNo ratings yet

- Localsalestaxcollections0215 PDFDocument3 pagesLocalsalestaxcollections0215 PDFjspectorNo ratings yet

- FL Voluntary Disclosure ProgramDocument3 pagesFL Voluntary Disclosure Programmcampo7No ratings yet

- Utah Form TC-20 Tax Return and InstructionsDocument26 pagesUtah Form TC-20 Tax Return and InstructionsBrandonNo ratings yet

- Budget OpinionnaireDocument22 pagesBudget OpinionnaireVivek JhaNo ratings yet

- SummaryDocument2 pagesSummaryChris AlcalaNo ratings yet

- CA District TaxDocument5 pagesCA District Taxkimhoang_16927574No ratings yet

- 21 Usefulcharts 2012-13Document20 pages21 Usefulcharts 2012-13sharmaji23No ratings yet

- PPD 647 - Tax Paper - Cross Border Shopping - RaraDocument6 pagesPPD 647 - Tax Paper - Cross Border Shopping - RarararaNo ratings yet

- LGU Taxation and Revenue Practices October 2015Document46 pagesLGU Taxation and Revenue Practices October 2015Mark Lester Lee Aure100% (2)

- Envelope PDFDocument104 pagesEnvelope PDFLeonard BrownNo ratings yet

- 2011 Howe ProfileDocument5 pages2011 Howe ProfileTCOG Community & Economic DevelopmentNo ratings yet

- Dallas Garage Sales Ordinance UpdateDocument11 pagesDallas Garage Sales Ordinance UpdateRobert WilonskyNo ratings yet

- 130 UDocument2 pages130 UNoelleNo ratings yet

- Type or Print Neatly in Ink: SPV $ Appraisal Value $Document2 pagesType or Print Neatly in Ink: SPV $ Appraisal Value $uriel huertaNo ratings yet

- F 1040 VDocument2 pagesF 1040 Vhottadot730@gmail.comNo ratings yet

- 130 U 3Document2 pages130 U 3Juan Escobar JuncalNo ratings yet

- GEN 010 Lesson 1-4Document28 pagesGEN 010 Lesson 1-4Carswel Hidalgo HornedoNo ratings yet

- 2010 IRS Notifications To The City of Lauderdake LakesDocument8 pages2010 IRS Notifications To The City of Lauderdake LakesMy-Acts Of-SeditionNo ratings yet

- Data Book: For Fiscal Year 2010Document24 pagesData Book: For Fiscal Year 2010Mark ReinhardtNo ratings yet

- International Marketing 200094 Pre-Class Activities Chapters 3 & 4Document8 pagesInternational Marketing 200094 Pre-Class Activities Chapters 3 & 4Uyen Nhi LeNo ratings yet

- BIR Form 2307Document20 pagesBIR Form 2307Lean Isidro0% (1)

- UST GN 2011 - Taxation Law IndexDocument2 pagesUST GN 2011 - Taxation Law IndexGhost100% (1)

- 4 Self Contained Units (FourPlex)Document6 pages4 Self Contained Units (FourPlex)VinceNo ratings yet

- Certificate of Creditable Tax Withheld at Source: Kawanihan NG Rentas InternasDocument3 pagesCertificate of Creditable Tax Withheld at Source: Kawanihan NG Rentas InternasAurora Pelagio VallejosNo ratings yet

- GT 800013Document3 pagesGT 800013Marco CorvoNo ratings yet

- US Internal Revenue Service: p1045 - 2002Document12 pagesUS Internal Revenue Service: p1045 - 2002IRSNo ratings yet

- Vin 1vxbr12excp901213Document3 pagesVin 1vxbr12excp901213Agung JackNo ratings yet

- Credit Policy Updates - May 8, 2013: Sliding Scale Maximum Loan To Value (LTV) - Conventional (1 To 4 Unit Properties)Document3 pagesCredit Policy Updates - May 8, 2013: Sliding Scale Maximum Loan To Value (LTV) - Conventional (1 To 4 Unit Properties)Mortgage ResourcesNo ratings yet

- Sales Tax: Main ArticleDocument1 pageSales Tax: Main ArticleMaika J. PudaderaNo ratings yet

- 2011 Publication BallotDocument4 pages2011 Publication BallotvaildailyNo ratings yet

- 2016 State Shared Revenue Report FinalDocument10 pages2016 State Shared Revenue Report Finalapi-243774512No ratings yet

- General Income Tax and Benefit Guide: Canada Revenue AgencyDocument63 pagesGeneral Income Tax and Benefit Guide: Canada Revenue AgencyvolvoproNo ratings yet

- In The United States Bankruptcy Court Eastern District of Michigan Southern DivisionDocument2 pagesIn The United States Bankruptcy Court Eastern District of Michigan Southern DivisionChapter 11 DocketsNo ratings yet

- State Sales and Use Tax ReturnDocument2 pagesState Sales and Use Tax ReturnRick JordanNo ratings yet

- AN ALTERNATIVE GOVERNMENT SYSTEM: NEW PROVISIONAL INCOME TAX SYSTEM NEW ELECTION AND VOTING SYSTEMFrom EverandAN ALTERNATIVE GOVERNMENT SYSTEM: NEW PROVISIONAL INCOME TAX SYSTEM NEW ELECTION AND VOTING SYSTEMNo ratings yet

- J.K. Lasser's Guide to Self-Employment: Taxes, Strategies, and Money-Saving Tips for Schedule C FilersFrom EverandJ.K. Lasser's Guide to Self-Employment: Taxes, Strategies, and Money-Saving Tips for Schedule C FilersNo ratings yet

- US V Sheldon Silver ComplaintDocument35 pagesUS V Sheldon Silver ComplaintNick ReismanNo ratings yet

- A Public Health Review of High Volume Hydraulic Fracturing For Shale Gas DevelopmentDocument184 pagesA Public Health Review of High Volume Hydraulic Fracturing For Shale Gas DevelopmentMatthew LeonardNo ratings yet

- Market .Impact of A Proposed Tyre, New York Casino On Turning Stone - Final.10.27.2014Document100 pagesMarket .Impact of A Proposed Tyre, New York Casino On Turning Stone - Final.10.27.2014glenncoin100% (1)

- Section IV Softball Brackets: DDocument1 pageSection IV Softball Brackets: DTime Warner Cable NewsNo ratings yet

- Eric Frein: What He Had in The HangarDocument14 pagesEric Frein: What He Had in The HangarAnonymous arnc2g2NNo ratings yet

- Judge's Ruling Dismissing Murder Charge Against Oral "Nick" HillaryDocument7 pagesJudge's Ruling Dismissing Murder Charge Against Oral "Nick" HillaryTime Warner Cable NewsNo ratings yet

- Cuomo Pens Letter To Push Quicker Action On Medical MarijuanaDocument1 pageCuomo Pens Letter To Push Quicker Action On Medical MarijuanaTime Warner Cable NewsNo ratings yet

- Section IV Softball 2014 TournamentDocument5 pagesSection IV Softball 2014 TournamentTime Warner Cable NewsNo ratings yet

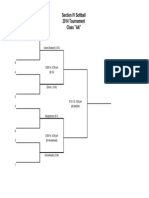

- Section IV Playoff Bracket: Softball ADocument1 pageSection IV Playoff Bracket: Softball ATime Warner Cable NewsNo ratings yet

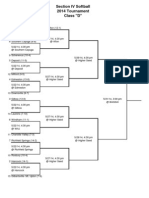

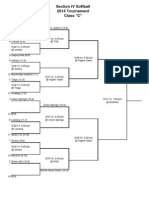

- Section IV Softball 2014 Tournament Class "C"Document1 pageSection IV Softball 2014 Tournament Class "C"Time Warner Cable NewsNo ratings yet

- Baseball Brackets 2014Document6 pagesBaseball Brackets 2014Time Warner Cable NewsNo ratings yet

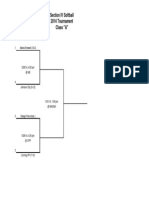

- Section IV Softball 2014 Tournament Class "AA"Document1 pageSection IV Softball 2014 Tournament Class "AA"Time Warner Cable NewsNo ratings yet

- Girls Lacrosse 2014 BracketsDocument3 pagesGirls Lacrosse 2014 BracketsTime Warner Cable NewsNo ratings yet

- Ffa History Lesson PlanDocument10 pagesFfa History Lesson Planapi-353178625100% (1)

- 9300.97 12-13-19 XFIIRE Models 300B - 1000B Type H & WH IPLDocument7 pages9300.97 12-13-19 XFIIRE Models 300B - 1000B Type H & WH IPLHector FajardoNo ratings yet

- Prowessiq Data Dictionary PDFDocument5,313 pagesProwessiq Data Dictionary PDFUtkarsh SinhaNo ratings yet

- ISB HandbookDocument62 pagesISB HandbookSteve RichardsNo ratings yet

- Baseball Golf OutingDocument2 pagesBaseball Golf OutingDaveNo ratings yet

- Creating Analytical Apps: Alteryx Tutorial Workshop Series 4Document19 pagesCreating Analytical Apps: Alteryx Tutorial Workshop Series 4meajagunNo ratings yet

- Ibs Kuantan Main 1 30/06/19Document1 pageIbs Kuantan Main 1 30/06/19Muhammad Zaim EmbongNo ratings yet

- Refurbishment and Subcontracting 2 Test CatalogDocument15 pagesRefurbishment and Subcontracting 2 Test CatalogmallikNo ratings yet

- Motor ProtectionDocument40 pagesMotor Protection7esabat7033No ratings yet

- SQL Top 50 Interview Questions and AnswersDocument28 pagesSQL Top 50 Interview Questions and AnswersBiplab SarkarNo ratings yet

- Exyte Malaysia - Energized Electrical Work (EEW) TrainingDocument35 pagesExyte Malaysia - Energized Electrical Work (EEW) TrainingThirumaran MuthusamyNo ratings yet

- Windows KMS Activator Ultimate 2021 5.3Document13 pagesWindows KMS Activator Ultimate 2021 5.3dadymamewa0% (1)

- Ra 11549Document6 pagesRa 11549Joemar Manaois TabanaoNo ratings yet

- Databases and Applications ProgramsDocument7 pagesDatabases and Applications ProgramsShibinMohammedIqbalNo ratings yet

- Trash Bin Monitoring SystemDocument15 pagesTrash Bin Monitoring SystemJanjie OlaivarNo ratings yet

- Riverside County FY 2020-21 First Quarter Budget ReportDocument50 pagesRiverside County FY 2020-21 First Quarter Budget ReportThe Press-Enterprise / pressenterprise.comNo ratings yet

- Multimedia Magic!: Microsoft Powerpoint) To Make BusinessDocument1 pageMultimedia Magic!: Microsoft Powerpoint) To Make BusinessfarveNo ratings yet

- Benefits of Binary MLM Plan For Network MarketingDocument4 pagesBenefits of Binary MLM Plan For Network MarketingSachin SinghNo ratings yet

- An Agent-Based Dynamic Occupancy Schedule Model For Prediction of HVAC Energy Demand in An Airport Terminal BuildingDocument10 pagesAn Agent-Based Dynamic Occupancy Schedule Model For Prediction of HVAC Energy Demand in An Airport Terminal BuildingKapil SinhaNo ratings yet

- TCB Installation Booklet HRCDocument11 pagesTCB Installation Booklet HRCAlexandre FonsecaNo ratings yet

- TicketParquesSintra 1Document3 pagesTicketParquesSintra 1hyper16No ratings yet

- Weller WCB 2 Mjerac Tempearture PDFDocument1 pageWeller WCB 2 Mjerac Tempearture PDFslvidovicNo ratings yet

- Stepsmart Assignment July 30Document15 pagesStepsmart Assignment July 30MeconNo ratings yet

- War Diary October 1943 (All) PDFDocument59 pagesWar Diary October 1943 (All) PDFSeaforth WebmasterNo ratings yet

- Grade 8 - Criteria B and C Factors Affecting Rocket Performance AssessmentDocument8 pagesGrade 8 - Criteria B and C Factors Affecting Rocket Performance Assessmentapi-291745547No ratings yet

- Makalah Bahasa InggrisDocument9 pagesMakalah Bahasa InggrisFluxNo ratings yet

- 1 - en - Print - Indd - 0014431Document261 pages1 - en - Print - Indd - 0014431Custom Case BMWNo ratings yet

- Rotary Newsletter May 4 2010Document3 pagesRotary Newsletter May 4 2010David KellerNo ratings yet

- LO 3. Control Hazards and Risks in The Workplace 3.1 Follow Consistently OHS Procedure For Controlling Hazards/risksDocument3 pagesLO 3. Control Hazards and Risks in The Workplace 3.1 Follow Consistently OHS Procedure For Controlling Hazards/risksChristine Joy ValenciaNo ratings yet