Synopsis Disst.

Synopsis Disst.

You might also like

- Financial Analysis of The Laxmi Bank Latest VersionDocument10 pagesFinancial Analysis of The Laxmi Bank Latest VersionMillionaire MentalityNo ratings yet

- Measuring Customer Satisfaction: Exploring Customer Satisfaction’s Relationship with Purchase BehaviorFrom EverandMeasuring Customer Satisfaction: Exploring Customer Satisfaction’s Relationship with Purchase BehaviorRating: 4.5 out of 5 stars4.5/5 (6)

- Summer Training Report Diya 1Document40 pagesSummer Training Report Diya 1navdeep2309No ratings yet

- Synopsis Customer Satisfaction in Retail BankingDocument9 pagesSynopsis Customer Satisfaction in Retail BankingRuchi KashyapNo ratings yet

- 7.hasnain Safdar Butt Final PaperDocument11 pages7.hasnain Safdar Butt Final PaperiisteNo ratings yet

- Review of Related LiteratureDocument11 pagesReview of Related LiteratureRo BinNo ratings yet

- Report First Draft-First CorrectedDocument39 pagesReport First Draft-First CorrectedPrakash KhadkaNo ratings yet

- Related Theories: and Keller 2006, 144.)Document8 pagesRelated Theories: and Keller 2006, 144.)Jiro SantiagoNo ratings yet

- Grab Food Food Panda RRL LeDocument5 pagesGrab Food Food Panda RRL LeAui PauNo ratings yet

- Chapter 1Document6 pagesChapter 1Fakir TajulNo ratings yet

- New Microsoft Word Document - OdtDocument5 pagesNew Microsoft Word Document - OdtObsetan HurisaNo ratings yet

- CHPTER2Document25 pagesCHPTER2JOEFRAN ENRIQUEZNo ratings yet

- Chapter 2 Literature ReviewDocument5 pagesChapter 2 Literature ReviewAmarnath KNo ratings yet

- KuzakDocument3 pagesKuzakAnonymous OxMAxCHNo ratings yet

- Research Proposal - BU7756Document16 pagesResearch Proposal - BU7756Yugandhar KumarNo ratings yet

- Name: Aima Shahid Roll No: 15401 Semster Submitted To: Sir ShaukatDocument11 pagesName: Aima Shahid Roll No: 15401 Semster Submitted To: Sir ShaukatAhmad MujtabaNo ratings yet

- ProjectDocument85 pagesProjectPansy ShardaNo ratings yet

- Customer Satisfaction TheoryDocument8 pagesCustomer Satisfaction TheoryFibin Haneefa100% (1)

- CultfitDocument12 pagesCultfitKS SreeragNo ratings yet

- Oriental Bank of CommerceDocument35 pagesOriental Bank of CommerceAmit Kumar ChaurasiaNo ratings yet

- Project Report On AdidasDocument33 pagesProject Report On Adidassanyam74% (38)

- Customer Satisfaction in Kancheepuram 2003Document11 pagesCustomer Satisfaction in Kancheepuram 2003Shano InbarajNo ratings yet

- Chapter 2Document22 pagesChapter 2Okorie Chinedu PNo ratings yet

- Measuring Customer Satisfaction in The Banking IndustryDocument9 pagesMeasuring Customer Satisfaction in The Banking Industrymevrick_guyNo ratings yet

- Chapter 2Document6 pagesChapter 2DivaxNo ratings yet

- 03 - Chapter 2 PDFDocument22 pages03 - Chapter 2 PDFLalajom HarveyNo ratings yet

- Review of Related Literature and StudiesDocument7 pagesReview of Related Literature and StudiesNadineNo ratings yet

- A Research ProposalDocument14 pagesA Research ProposalMIAN USMANNo ratings yet

- 1.1. Background of The StudyDocument35 pages1.1. Background of The StudyfitsumNo ratings yet

- Factors Determining Customer SatisfactionDocument24 pagesFactors Determining Customer SatisfactionAnand sharmaNo ratings yet

- Review of Related LiteratureDocument3 pagesReview of Related LiteratureAya Leah0% (1)

- Chapter One 1.1 Background of The StudyDocument23 pagesChapter One 1.1 Background of The StudyDamtewNo ratings yet

- Coca Cola ReportDocument49 pagesCoca Cola ReportBhaskarani PradeepNo ratings yet

- Dhampur Sugar MillsDocument27 pagesDhampur Sugar MillsSuneel SinghNo ratings yet

- Customer SatisfactionDocument4 pagesCustomer SatisfactionThat Pahadi GirlNo ratings yet

- Background To The StudyDocument98 pagesBackground To The StudyJehan Marie GiananNo ratings yet

- Rajeshwari Final ReportDocument53 pagesRajeshwari Final ReportLakshmi SaraswathiNo ratings yet

- Renita-Why Do Customer SwitchDocument18 pagesRenita-Why Do Customer SwitchakfaditadikapariraNo ratings yet

- MR Gowtham Aashirwad Kumar - A Study On Customer SatisfactionDocument19 pagesMR Gowtham Aashirwad Kumar - A Study On Customer SatisfactionRohit KumarNo ratings yet

- A Written PropoposalDocument7 pagesA Written Propoposalvalentina cultivo100% (1)

- Customer Satisfaction, A: Business TermDocument4 pagesCustomer Satisfaction, A: Business TermDurga Prasad KNo ratings yet

- Market Research Survey ReportDocument25 pagesMarket Research Survey ReportRahul SahuNo ratings yet

- Chapter 1 BpoDocument12 pagesChapter 1 BpogkzunigaNo ratings yet

- AbstractDocument46 pagesAbstractArpit CmNo ratings yet

- Factors Influencing Customer SatisfactioDocument8 pagesFactors Influencing Customer SatisfactioashutoshNo ratings yet

- Indiamart Internship ReportDocument94 pagesIndiamart Internship Reportdhavalshukla50% (2)

- What Is Customer SatisfactionDocument8 pagesWhat Is Customer SatisfactionDeepa .SNo ratings yet

- Relationship Between Customer Satisfaction and ProfitabilityDocument51 pagesRelationship Between Customer Satisfaction and ProfitabilityNajie LawiNo ratings yet

- Marketing: Customer Satisfaction Is A Term Frequently Used inDocument7 pagesMarketing: Customer Satisfaction Is A Term Frequently Used inLucky YadavNo ratings yet

- The Relationship Between Customer Satisfaction and Customer Loyalty in The Banking Sector in SyriaDocument9 pagesThe Relationship Between Customer Satisfaction and Customer Loyalty in The Banking Sector in Syriamr kevinNo ratings yet

- 044 Emrah CengizDocument13 pages044 Emrah CengizChiranjeevi Revalpalli RNo ratings yet

- Customer SatisfactionDocument40 pagesCustomer SatisfactionVenkata PrasadNo ratings yet

- ManuscriptDocument13 pagesManuscriptleizelNo ratings yet

- Review of Literature: SatisfactionDocument10 pagesReview of Literature: SatisfactionKing KrishNo ratings yet

- Customer SatisfactionDocument7 pagesCustomer SatisfactionSSEMATIC RAQUIBNo ratings yet

- Chapter 2 - Review of LiteratureDocument10 pagesChapter 2 - Review of LiteratureLaniNo ratings yet

- Literature ReviewDocument2 pagesLiterature ReviewRuee TambatNo ratings yet

- Customer SatisfactionDocument5 pagesCustomer SatisfactionSalwa KamarudinNo ratings yet

- Chapter-1 Introduction and Research Design: 1.1.1 Customer SatisfactionDocument16 pagesChapter-1 Introduction and Research Design: 1.1.1 Customer SatisfactionpiusadrienNo ratings yet

- The Changing Global Marketplace Landscape: Understanding Customer Intentions, Attitudes, Beliefs, and FeelingsFrom EverandThe Changing Global Marketplace Landscape: Understanding Customer Intentions, Attitudes, Beliefs, and FeelingsNo ratings yet

- The Successful Strategies from Customer Managment ExcellenceFrom EverandThe Successful Strategies from Customer Managment ExcellenceNo ratings yet

- Suffolk Federal Credit Union, Plaintiff, vs. Federal National Mortgage Association Defendant.Document29 pagesSuffolk Federal Credit Union, Plaintiff, vs. Federal National Mortgage Association Defendant.Foreclosure FraudNo ratings yet

- Investment Banking Interview QuestionsDocument3 pagesInvestment Banking Interview QuestionsdaweiliNo ratings yet

- Credit CardDocument3 pagesCredit Cardprashant1807No ratings yet

- Challan 45005 BrilliantDocument1 pageChallan 45005 BrilliantDreamers' ProductionNo ratings yet

- Branch Banking SystemDocument16 pagesBranch Banking SystemPrathyusha ReddyNo ratings yet

- CH10 Finan Acc Long Term Liab LectDocument28 pagesCH10 Finan Acc Long Term Liab LectAbdul KabeerNo ratings yet

- AB BankDocument134 pagesAB BankENAMUL HAQUENo ratings yet

- Q2 W1 General MathematicsDocument39 pagesQ2 W1 General MathematicsSamantha ManibogNo ratings yet

- Pfi KPK FormDocument3 pagesPfi KPK FormSaud ur RehmanNo ratings yet

- What The Finance Function Is: The Determination of Fund RequirementsDocument6 pagesWhat The Finance Function Is: The Determination of Fund RequirementsAmyiel FloresNo ratings yet

- Contract in Islamic Finance and Banking.: BWSS 2093Document49 pagesContract in Islamic Finance and Banking.: BWSS 2093otaku himeNo ratings yet

- Media Lions ShortlistDocument18 pagesMedia Lions Shortlistadobo magazineNo ratings yet

- Case DigestDocument7 pagesCase DigestYolanda Janice Sayan FalingaoNo ratings yet

- SHUATS Online Application FormDocument2 pagesSHUATS Online Application FormANJALI BINDNo ratings yet

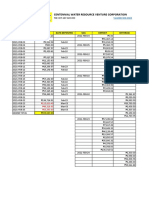

- Morong Branch: Centennial Water Resource Venture CorporationDocument10 pagesMorong Branch: Centennial Water Resource Venture CorporationChesca SantiagoNo ratings yet

- Thomson Reuters PresentationDocument19 pagesThomson Reuters PresentationSashi DandamudiNo ratings yet

- April 2019Document72 pagesApril 2019Sunil UndarNo ratings yet

- Internship Report (Sakibul Alam)Document36 pagesInternship Report (Sakibul Alam)Mohammad MamunNo ratings yet

- SummerInternships DRUCKDocument8 pagesSummerInternships DRUCKRishim90No ratings yet

- Case Study On NDB and DFCCDocument34 pagesCase Study On NDB and DFCCRantharu AttanayakeNo ratings yet

- FDIC v. Icard, Merrill, Cullis, Timm, Furen & Ginsburg, P.A., 11th Cir. (2014)Document24 pagesFDIC v. Icard, Merrill, Cullis, Timm, Furen & Ginsburg, P.A., 11th Cir. (2014)Scribd Government DocsNo ratings yet

- Money 4 LifeDocument92 pagesMoney 4 LifeDamilolaNo ratings yet

- As Cabanatuan RFO BungalowDocument1 pageAs Cabanatuan RFO BungalowMao WatanabeNo ratings yet

- The SanctuaryDocument5 pagesThe SanctuaryDaniel Charaf LossadaNo ratings yet

- Pas 24 Related Party DisclosuresDocument1 pagePas 24 Related Party DisclosuresJNo ratings yet

- AP Debt WaiverDocument10 pagesAP Debt WaiverChandra ReddyNo ratings yet

- Quiz BFDocument7 pagesQuiz BFjolinaNo ratings yet

- A Study On Customer Satisfaction at HDFC Bank, VijayapuraDocument70 pagesA Study On Customer Satisfaction at HDFC Bank, Vijayapurapatelhotel786No ratings yet

Download as docx, pdf, or txt

You might also like

- Financial Analysis of The Laxmi Bank Latest VersionDocument10 pagesFinancial Analysis of The Laxmi Bank Latest VersionMillionaire MentalityNo ratings yet

- Measuring Customer Satisfaction: Exploring Customer Satisfaction’s Relationship with Purchase BehaviorFrom EverandMeasuring Customer Satisfaction: Exploring Customer Satisfaction’s Relationship with Purchase BehaviorRating: 4.5 out of 5 stars4.5/5 (6)

- Summer Training Report Diya 1Document40 pagesSummer Training Report Diya 1navdeep2309No ratings yet

- Synopsis Customer Satisfaction in Retail BankingDocument9 pagesSynopsis Customer Satisfaction in Retail BankingRuchi KashyapNo ratings yet

- 7.hasnain Safdar Butt Final PaperDocument11 pages7.hasnain Safdar Butt Final PaperiisteNo ratings yet

- Review of Related LiteratureDocument11 pagesReview of Related LiteratureRo BinNo ratings yet

- Report First Draft-First CorrectedDocument39 pagesReport First Draft-First CorrectedPrakash KhadkaNo ratings yet

- Related Theories: and Keller 2006, 144.)Document8 pagesRelated Theories: and Keller 2006, 144.)Jiro SantiagoNo ratings yet

- Grab Food Food Panda RRL LeDocument5 pagesGrab Food Food Panda RRL LeAui PauNo ratings yet

- Chapter 1Document6 pagesChapter 1Fakir TajulNo ratings yet

- New Microsoft Word Document - OdtDocument5 pagesNew Microsoft Word Document - OdtObsetan HurisaNo ratings yet

- CHPTER2Document25 pagesCHPTER2JOEFRAN ENRIQUEZNo ratings yet

- Chapter 2 Literature ReviewDocument5 pagesChapter 2 Literature ReviewAmarnath KNo ratings yet

- KuzakDocument3 pagesKuzakAnonymous OxMAxCHNo ratings yet

- Research Proposal - BU7756Document16 pagesResearch Proposal - BU7756Yugandhar KumarNo ratings yet

- Name: Aima Shahid Roll No: 15401 Semster Submitted To: Sir ShaukatDocument11 pagesName: Aima Shahid Roll No: 15401 Semster Submitted To: Sir ShaukatAhmad MujtabaNo ratings yet

- ProjectDocument85 pagesProjectPansy ShardaNo ratings yet

- Customer Satisfaction TheoryDocument8 pagesCustomer Satisfaction TheoryFibin Haneefa100% (1)

- CultfitDocument12 pagesCultfitKS SreeragNo ratings yet

- Oriental Bank of CommerceDocument35 pagesOriental Bank of CommerceAmit Kumar ChaurasiaNo ratings yet

- Project Report On AdidasDocument33 pagesProject Report On Adidassanyam74% (38)

- Customer Satisfaction in Kancheepuram 2003Document11 pagesCustomer Satisfaction in Kancheepuram 2003Shano InbarajNo ratings yet

- Chapter 2Document22 pagesChapter 2Okorie Chinedu PNo ratings yet

- Measuring Customer Satisfaction in The Banking IndustryDocument9 pagesMeasuring Customer Satisfaction in The Banking Industrymevrick_guyNo ratings yet

- Chapter 2Document6 pagesChapter 2DivaxNo ratings yet

- 03 - Chapter 2 PDFDocument22 pages03 - Chapter 2 PDFLalajom HarveyNo ratings yet

- Review of Related Literature and StudiesDocument7 pagesReview of Related Literature and StudiesNadineNo ratings yet

- A Research ProposalDocument14 pagesA Research ProposalMIAN USMANNo ratings yet

- 1.1. Background of The StudyDocument35 pages1.1. Background of The StudyfitsumNo ratings yet

- Factors Determining Customer SatisfactionDocument24 pagesFactors Determining Customer SatisfactionAnand sharmaNo ratings yet

- Review of Related LiteratureDocument3 pagesReview of Related LiteratureAya Leah0% (1)

- Chapter One 1.1 Background of The StudyDocument23 pagesChapter One 1.1 Background of The StudyDamtewNo ratings yet

- Coca Cola ReportDocument49 pagesCoca Cola ReportBhaskarani PradeepNo ratings yet

- Dhampur Sugar MillsDocument27 pagesDhampur Sugar MillsSuneel SinghNo ratings yet

- Customer SatisfactionDocument4 pagesCustomer SatisfactionThat Pahadi GirlNo ratings yet

- Background To The StudyDocument98 pagesBackground To The StudyJehan Marie GiananNo ratings yet

- Rajeshwari Final ReportDocument53 pagesRajeshwari Final ReportLakshmi SaraswathiNo ratings yet

- Renita-Why Do Customer SwitchDocument18 pagesRenita-Why Do Customer SwitchakfaditadikapariraNo ratings yet

- MR Gowtham Aashirwad Kumar - A Study On Customer SatisfactionDocument19 pagesMR Gowtham Aashirwad Kumar - A Study On Customer SatisfactionRohit KumarNo ratings yet

- A Written PropoposalDocument7 pagesA Written Propoposalvalentina cultivo100% (1)

- Customer Satisfaction, A: Business TermDocument4 pagesCustomer Satisfaction, A: Business TermDurga Prasad KNo ratings yet

- Market Research Survey ReportDocument25 pagesMarket Research Survey ReportRahul SahuNo ratings yet

- Chapter 1 BpoDocument12 pagesChapter 1 BpogkzunigaNo ratings yet

- AbstractDocument46 pagesAbstractArpit CmNo ratings yet

- Factors Influencing Customer SatisfactioDocument8 pagesFactors Influencing Customer SatisfactioashutoshNo ratings yet

- Indiamart Internship ReportDocument94 pagesIndiamart Internship Reportdhavalshukla50% (2)

- What Is Customer SatisfactionDocument8 pagesWhat Is Customer SatisfactionDeepa .SNo ratings yet

- Relationship Between Customer Satisfaction and ProfitabilityDocument51 pagesRelationship Between Customer Satisfaction and ProfitabilityNajie LawiNo ratings yet

- Marketing: Customer Satisfaction Is A Term Frequently Used inDocument7 pagesMarketing: Customer Satisfaction Is A Term Frequently Used inLucky YadavNo ratings yet

- The Relationship Between Customer Satisfaction and Customer Loyalty in The Banking Sector in SyriaDocument9 pagesThe Relationship Between Customer Satisfaction and Customer Loyalty in The Banking Sector in Syriamr kevinNo ratings yet

- 044 Emrah CengizDocument13 pages044 Emrah CengizChiranjeevi Revalpalli RNo ratings yet

- Customer SatisfactionDocument40 pagesCustomer SatisfactionVenkata PrasadNo ratings yet

- ManuscriptDocument13 pagesManuscriptleizelNo ratings yet

- Review of Literature: SatisfactionDocument10 pagesReview of Literature: SatisfactionKing KrishNo ratings yet

- Customer SatisfactionDocument7 pagesCustomer SatisfactionSSEMATIC RAQUIBNo ratings yet

- Chapter 2 - Review of LiteratureDocument10 pagesChapter 2 - Review of LiteratureLaniNo ratings yet

- Literature ReviewDocument2 pagesLiterature ReviewRuee TambatNo ratings yet

- Customer SatisfactionDocument5 pagesCustomer SatisfactionSalwa KamarudinNo ratings yet

- Chapter-1 Introduction and Research Design: 1.1.1 Customer SatisfactionDocument16 pagesChapter-1 Introduction and Research Design: 1.1.1 Customer SatisfactionpiusadrienNo ratings yet

- The Changing Global Marketplace Landscape: Understanding Customer Intentions, Attitudes, Beliefs, and FeelingsFrom EverandThe Changing Global Marketplace Landscape: Understanding Customer Intentions, Attitudes, Beliefs, and FeelingsNo ratings yet

- The Successful Strategies from Customer Managment ExcellenceFrom EverandThe Successful Strategies from Customer Managment ExcellenceNo ratings yet

- Suffolk Federal Credit Union, Plaintiff, vs. Federal National Mortgage Association Defendant.Document29 pagesSuffolk Federal Credit Union, Plaintiff, vs. Federal National Mortgage Association Defendant.Foreclosure FraudNo ratings yet

- Investment Banking Interview QuestionsDocument3 pagesInvestment Banking Interview QuestionsdaweiliNo ratings yet

- Credit CardDocument3 pagesCredit Cardprashant1807No ratings yet

- Challan 45005 BrilliantDocument1 pageChallan 45005 BrilliantDreamers' ProductionNo ratings yet

- Branch Banking SystemDocument16 pagesBranch Banking SystemPrathyusha ReddyNo ratings yet

- CH10 Finan Acc Long Term Liab LectDocument28 pagesCH10 Finan Acc Long Term Liab LectAbdul KabeerNo ratings yet

- AB BankDocument134 pagesAB BankENAMUL HAQUENo ratings yet

- Q2 W1 General MathematicsDocument39 pagesQ2 W1 General MathematicsSamantha ManibogNo ratings yet

- Pfi KPK FormDocument3 pagesPfi KPK FormSaud ur RehmanNo ratings yet

- What The Finance Function Is: The Determination of Fund RequirementsDocument6 pagesWhat The Finance Function Is: The Determination of Fund RequirementsAmyiel FloresNo ratings yet

- Contract in Islamic Finance and Banking.: BWSS 2093Document49 pagesContract in Islamic Finance and Banking.: BWSS 2093otaku himeNo ratings yet

- Media Lions ShortlistDocument18 pagesMedia Lions Shortlistadobo magazineNo ratings yet

- Case DigestDocument7 pagesCase DigestYolanda Janice Sayan FalingaoNo ratings yet

- SHUATS Online Application FormDocument2 pagesSHUATS Online Application FormANJALI BINDNo ratings yet

- Morong Branch: Centennial Water Resource Venture CorporationDocument10 pagesMorong Branch: Centennial Water Resource Venture CorporationChesca SantiagoNo ratings yet

- Thomson Reuters PresentationDocument19 pagesThomson Reuters PresentationSashi DandamudiNo ratings yet

- April 2019Document72 pagesApril 2019Sunil UndarNo ratings yet

- Internship Report (Sakibul Alam)Document36 pagesInternship Report (Sakibul Alam)Mohammad MamunNo ratings yet

- SummerInternships DRUCKDocument8 pagesSummerInternships DRUCKRishim90No ratings yet

- Case Study On NDB and DFCCDocument34 pagesCase Study On NDB and DFCCRantharu AttanayakeNo ratings yet

- FDIC v. Icard, Merrill, Cullis, Timm, Furen & Ginsburg, P.A., 11th Cir. (2014)Document24 pagesFDIC v. Icard, Merrill, Cullis, Timm, Furen & Ginsburg, P.A., 11th Cir. (2014)Scribd Government DocsNo ratings yet

- Money 4 LifeDocument92 pagesMoney 4 LifeDamilolaNo ratings yet

- As Cabanatuan RFO BungalowDocument1 pageAs Cabanatuan RFO BungalowMao WatanabeNo ratings yet

- The SanctuaryDocument5 pagesThe SanctuaryDaniel Charaf LossadaNo ratings yet

- Pas 24 Related Party DisclosuresDocument1 pagePas 24 Related Party DisclosuresJNo ratings yet

- AP Debt WaiverDocument10 pagesAP Debt WaiverChandra ReddyNo ratings yet

- Quiz BFDocument7 pagesQuiz BFjolinaNo ratings yet

- A Study On Customer Satisfaction at HDFC Bank, VijayapuraDocument70 pagesA Study On Customer Satisfaction at HDFC Bank, Vijayapurapatelhotel786No ratings yet