Download as pdf or txt

You might also like

- The Process of Financial Planning, 2nd Edition: Developing a Financial PlanFrom EverandThe Process of Financial Planning, 2nd Edition: Developing a Financial PlanNo ratings yet

- IFRS Simplified: A fast and easy-to-understand overview of the new International Financial Reporting StandardsFrom EverandIFRS Simplified: A fast and easy-to-understand overview of the new International Financial Reporting StandardsRating: 4 out of 5 stars4/5 (11)

- A Project Report ON: Ifrs (International Financial Reporting Standards) & Its Convergence in IndiaDocument80 pagesA Project Report ON: Ifrs (International Financial Reporting Standards) & Its Convergence in IndialalsinghNo ratings yet

- 101 FDI-SinDocument49 pages101 FDI-SinLê Hoàng Việt HảiNo ratings yet

- IFRS US GAAP and Mexican FRS Similarities and DifferencesDocument196 pagesIFRS US GAAP and Mexican FRS Similarities and DifferencesArturo Vertti0% (1)

- 13 Japan Under The ShogunDocument22 pages13 Japan Under The Shogunapi-29949541290% (10)

- IFRS and US GAAP DifferencesDocument232 pagesIFRS and US GAAP Differencesarvi78No ratings yet

- Achieving A SingleDocument3 pagesAchieving A SingleAristha Purwanthari SawitriNo ratings yet

- Us Assurance International Financial Reporting STD 030108Document4 pagesUs Assurance International Financial Reporting STD 030108Pallavi PalluNo ratings yet

- Background of Convergence of Us Gaap and Ifrs Accounting EssayDocument4 pagesBackground of Convergence of Us Gaap and Ifrs Accounting EssayVimal SoniNo ratings yet

- Leadership in The WorkplaceDocument7 pagesLeadership in The WorkplaceJayReneNo ratings yet

- Advantages of Convergence of Us Gaap and Ifrs Accounting EssayDocument4 pagesAdvantages of Convergence of Us Gaap and Ifrs Accounting EssayVimal SoniNo ratings yet

- A Perspective On The SEC's Proposal To Accept Financial Statements Prepared in Accordance With International Financial Reporting Standards (IFRS) Without ReconciliationDocument9 pagesA Perspective On The SEC's Proposal To Accept Financial Statements Prepared in Accordance With International Financial Reporting Standards (IFRS) Without ReconciliationBhupendra RaiNo ratings yet

- Gaap To Ifrs 1Document32 pagesGaap To Ifrs 1prb323No ratings yet

- Ifrs Vs Us Gaap Basics March 2010Document56 pagesIfrs Vs Us Gaap Basics March 2010rahulchutiaNo ratings yet

- Solutions - Tutorial 2Document3 pagesSolutions - Tutorial 2s.h.j.braamhaarNo ratings yet

- Act 330Document9 pagesAct 330Samiul21No ratings yet

- Differences Between IFRS and US GAAPDocument7 pagesDifferences Between IFRS and US GAAPAderonke AjibolaNo ratings yet

- Gaap Vs IfrsDocument6 pagesGaap Vs IfrsCy WallNo ratings yet

- The Economic Impact of IFRSDocument22 pagesThe Economic Impact of IFRSSillyBee1205No ratings yet

- The Impact of Combining The US GAAP & IFRSDocument7 pagesThe Impact of Combining The US GAAP & IFRSoptimistic07No ratings yet

- Chapter-1 Introducti ONDocument61 pagesChapter-1 Introducti ONprashant mhatreNo ratings yet

- Benefits of and Obstacles To Global Convergence of Accounting StandardsDocument6 pagesBenefits of and Obstacles To Global Convergence of Accounting StandardsAtia IbnatNo ratings yet

- Ifrs WhitepaperDocument14 pagesIfrs Whitepapervcsekhar_caNo ratings yet

- Master Thesis IfrsDocument8 pagesMaster Thesis Ifrsbrendapotterreno100% (1)

- Financial Accounting (Assignment)Document7 pagesFinancial Accounting (Assignment)Bella SeahNo ratings yet

- Lectures 7, 8, 9Document6 pagesLectures 7, 8, 9Natalia MatuNo ratings yet

- Accounting Standards - Are We Ready For Principles-Based Guidelines (2002)Document9 pagesAccounting Standards - Are We Ready For Principles-Based Guidelines (2002)John Derama SagapsapanNo ratings yet

- ACC101 What Is A Conceptual FrameworkDocument3 pagesACC101 What Is A Conceptual Frameworklaredami64No ratings yet

- Convergence and Foreign InvestmentsDocument26 pagesConvergence and Foreign InvestmentsFlorie-May Garcia100% (1)

- The Greater Emphasis On The Conceptual FrameworkDocument10 pagesThe Greater Emphasis On The Conceptual FrameworkMuh Niswar AdhyatmaNo ratings yet

- What Is IFRSDocument5 pagesWhat Is IFRSRR Triani ANo ratings yet

- The Differences of IFRS and U.S. GAAP and The Importance of Their Integration Liberty University ACCT 301-B02 Charles BuckleyDocument11 pagesThe Differences of IFRS and U.S. GAAP and The Importance of Their Integration Liberty University ACCT 301-B02 Charles BuckleyMohamed BoutalebNo ratings yet

- Ifrs in The United StatesDocument11 pagesIfrs in The United StatesAli salamehNo ratings yet

- Introduction To IFRS: Slides From Ernst & Young Foundation and KPMG FoundationDocument32 pagesIntroduction To IFRS: Slides From Ernst & Young Foundation and KPMG FoundationbrcraoNo ratings yet

- Sonn - KopyaDocument3 pagesSonn - KopyaSinem TekcorapNo ratings yet

- Solution Manual For Ethical Obligations and Decision Making in Accounting Text and Cases 2nd Edition by MintzDocument16 pagesSolution Manual For Ethical Obligations and Decision Making in Accounting Text and Cases 2nd Edition by MintzLoriSmithamdt100% (47)

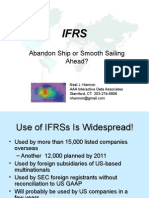

- Abandon Ship or Smooth Sailing Ahead?: Neal J. Hannon AAA Interactive Data Associates Stamford, CT 203-274-6806Document44 pagesAbandon Ship or Smooth Sailing Ahead?: Neal J. Hannon AAA Interactive Data Associates Stamford, CT 203-274-6806Akram KhanNo ratings yet

- Some Issues About The Transition From U.S. Generally Accepted Accounting Principles (Gaap) To International Financial Reporting Standards (Ifrs)Document15 pagesSome Issues About The Transition From U.S. Generally Accepted Accounting Principles (Gaap) To International Financial Reporting Standards (Ifrs)FIRAOL CHERUNo ratings yet

- Running Head: Convergence of Accounting Principles 1Document6 pagesRunning Head: Convergence of Accounting Principles 1Macharia NgunjiriNo ratings yet

- Volckers SpeechDocument6 pagesVolckers SpeechSoeba1No ratings yet

- Oracle IfrsDocument36 pagesOracle IfrsAdnan RiazNo ratings yet

- IFRS - 10 Years Later: Accounting and Business ResearchDocument28 pagesIFRS - 10 Years Later: Accounting and Business ResearchUbaid DarNo ratings yet

- IFRS 10 Years LaterDocument28 pagesIFRS 10 Years LaterMark Dela CruzNo ratings yet

- The Differences Between IFRS and GAAPDocument12 pagesThe Differences Between IFRS and GAAPAli salamehNo ratings yet

- Reading Task 1Document3 pagesReading Task 1Florensi Marlis AbleloNo ratings yet

- Intermediate Accounting IFRS 3rd Edition-43-62Document20 pagesIntermediate Accounting IFRS 3rd Edition-43-62dindaNo ratings yet

- Assgt AnswersDocument25 pagesAssgt AnswersmalaNo ratings yet

- Accounting Theory Assignment 1410531056Document5 pagesAccounting Theory Assignment 1410531056diahNo ratings yet

- AAAC Chapter03Document38 pagesAAAC Chapter03benazi22No ratings yet

- Hull University Business School 2011-2011: Student Name: So Min PoDocument10 pagesHull University Business School 2011-2011: Student Name: So Min PoPo SoNo ratings yet

- Indian and International Accounting StandardsDocument6 pagesIndian and International Accounting StandardsGirish KriznanNo ratings yet

- 8 Critical Perspectives On The Implementation of IFRS in Canada - 22Document22 pages8 Critical Perspectives On The Implementation of IFRS in Canada - 22Carla Cardador RamalhoNo ratings yet

- 19 Advantages and Disadvantages of Adopting IFRSDocument5 pages19 Advantages and Disadvantages of Adopting IFRSGift Malulu100% (1)

- Accounting Theory Chapter 4Document4 pagesAccounting Theory Chapter 4ghldcNo ratings yet

- What Is IFRSDocument21 pagesWhat Is IFRSDivisha AgarwalNo ratings yet

- CH 11solutionsDocument8 pagesCH 11solutionsVincent Oluoch Odhiambo67% (3)

- Transparency in Financial Reporting: A concise comparison of IFRS and US GAAPFrom EverandTransparency in Financial Reporting: A concise comparison of IFRS and US GAAPRating: 4.5 out of 5 stars4.5/5 (3)

- International Financial Statement AnalysisFrom EverandInternational Financial Statement AnalysisRating: 1 out of 5 stars1/5 (1)

- Engagement Essentials: Preparation, Compilation, and Review of Financial StatementsFrom EverandEngagement Essentials: Preparation, Compilation, and Review of Financial StatementsNo ratings yet

- United States v. Richard Rutgerson, 11th Cir. (2016)Document34 pagesUnited States v. Richard Rutgerson, 11th Cir. (2016)Scribd Government DocsNo ratings yet

- Business Math Report On TaxDocument23 pagesBusiness Math Report On TaxJustine Kaye PorcadillaNo ratings yet

- TD - 06B - 3228 - 011 - Dique Norte - QSO: Size Distribution P-ValuesDocument8 pagesTD - 06B - 3228 - 011 - Dique Norte - QSO: Size Distribution P-ValuesCYNTHIA CALDERON VACANo ratings yet

- 10 Total Mark: 10 X 1 10: NPTEL Online Certification Courses Indian Institute of Technology KharagpurDocument6 pages10 Total Mark: 10 X 1 10: NPTEL Online Certification Courses Indian Institute of Technology KharagpurvitNo ratings yet

- Iot Based Real Time Potholes Detection System Using Image Processing TechniquesDocument5 pagesIot Based Real Time Potholes Detection System Using Image Processing TechniquesanjaleemanageNo ratings yet

- Nx-8035-G7 Specification: Model Nutanix: Per Node ( (2) Per Block) NX-8035-G7 (Configure To Order)Document2 pagesNx-8035-G7 Specification: Model Nutanix: Per Node ( (2) Per Block) NX-8035-G7 (Configure To Order)Nazakat MallickNo ratings yet

- Notes in PharmacologyDocument95 pagesNotes in PharmacologyMylz MendozaNo ratings yet

- Soal B. Inggris Kls 10 Genap, 2023Document3 pagesSoal B. Inggris Kls 10 Genap, 2023smkterpadu insancitaNo ratings yet

- Opengl Es Common/Common-Lite Profile Specification: Version 1.1.12 (Difference Specification) (Annotated)Document128 pagesOpengl Es Common/Common-Lite Profile Specification: Version 1.1.12 (Difference Specification) (Annotated)bitNo ratings yet

- Relations and FunctionsDocument9 pagesRelations and Functions789No ratings yet

- ACP-EU Business Climate Facility Awarded 'Investment Climate Initiative of The Year'-2009Document1 pageACP-EU Business Climate Facility Awarded 'Investment Climate Initiative of The Year'-2009dmaproiectNo ratings yet

- Ad 2 Fapp enDocument12 pagesAd 2 Fapp enNagapranav Nagapranavm.jNo ratings yet

- Structural Bionic Design For Digging Shovel of CasDocument12 pagesStructural Bionic Design For Digging Shovel of CasAmeer SaeedNo ratings yet

- Immunoglobulins - Structure and Function Definition: Immunoglobulins (Ig)Document9 pagesImmunoglobulins - Structure and Function Definition: Immunoglobulins (Ig)Valdez Francis ZaccheauNo ratings yet

- Sigmacover 525: Curing table for dft up to 125 μm CuringDocument2 pagesSigmacover 525: Curing table for dft up to 125 μm CuringEngTamerNo ratings yet

- Ipa Parmendra Kumar SinghDocument2 pagesIpa Parmendra Kumar SinghAhtesham Umar TaqiNo ratings yet

- Unit-2: Linear Data Structure StackDocument37 pagesUnit-2: Linear Data Structure StackDivyes P100% (1)

- Dokumen 2Document1 pageDokumen 2Balamurugan HNo ratings yet

- TTR ProspektDocument6 pagesTTR ProspektHussein EidNo ratings yet

- OS8 Gap AnalysisDocument3 pagesOS8 Gap AnalysisMihaela MikaNo ratings yet

- CX200 Sales Spec Sheet (Euro 5) R09Document2 pagesCX200 Sales Spec Sheet (Euro 5) R09RobertNo ratings yet

- S-000-535Z-002 - 2 HvacDocument64 pagesS-000-535Z-002 - 2 HvacMidhun K ChandraboseNo ratings yet

- 1964 - Blyholder ModelDocument1 page1964 - Blyholder Model1592162022No ratings yet

- SLG700 34-SL-03-03Document41 pagesSLG700 34-SL-03-03RADAMANTHIS9No ratings yet

- 006 PLI - Form - Inspection Lifting GearDocument3 pages006 PLI - Form - Inspection Lifting GearRicky Stormbringer ChristianNo ratings yet

- Issai 100 20210906114606Document37 pagesIssai 100 20210906114606Eddy ETMNo ratings yet

- A. Palko - Pregnant PolytraumaDocument60 pagesA. Palko - Pregnant PolytraumaLazar VučetićNo ratings yet

- Module in Earth and Life Science: Levels of Organization of Living ThingsDocument20 pagesModule in Earth and Life Science: Levels of Organization of Living ThingsAna Kristelle Grace SyNo ratings yet