Download as pdf or txt

You might also like

- Chinese Creation MythDocument4 pagesChinese Creation MythprominusNo ratings yet

- Saint Silouan The Athonite - Akathist PDFDocument9 pagesSaint Silouan The Athonite - Akathist PDFmrjpleeNo ratings yet

- Unit 1: Business and The Business Environment: Assignment BriefDocument5 pagesUnit 1: Business and The Business Environment: Assignment BriefNguyễn Quốc AnhNo ratings yet

- Herbert Marcuse - Industrialization and Capitalism in The Works of Max WeberDocument19 pagesHerbert Marcuse - Industrialization and Capitalism in The Works of Max WeberАлФредо Элисондо100% (1)

- Investor Presentation: Bharti Airtel LimitedDocument27 pagesInvestor Presentation: Bharti Airtel LimitedChandrashekhar N ChintalwarNo ratings yet

- Investor Presentation: Bharti Airtel LimitedDocument29 pagesInvestor Presentation: Bharti Airtel LimitedVishal JainNo ratings yet

- ICICIdirect NewTelecomPolicy2011 SectorUpdateDocument3 pagesICICIdirect NewTelecomPolicy2011 SectorUpdateSoodamany Ponnu PandianNo ratings yet

- Investor Presentation (Company Update)Document36 pagesInvestor Presentation (Company Update)Shyam SunderNo ratings yet

- DishTV Investor PresentationDocument32 pagesDishTV Investor Presentationmrinal_kakkar8215No ratings yet

- Idea Investor Presentation 2015Document38 pagesIdea Investor Presentation 2015Mukund KabraNo ratings yet

- Ir PPT 4qfy15Document50 pagesIr PPT 4qfy15droomNo ratings yet

- Airtel PresentationDocument40 pagesAirtel PresentationAbhimanyu Gupta100% (1)

- Dish TV India Limited: Investor PresentationDocument27 pagesDish TV India Limited: Investor Presentationmohitegaurv87No ratings yet

- Asian Pay Television Trust: Management Presentation JUNE 2013Document22 pagesAsian Pay Television Trust: Management Presentation JUNE 2013Invest StockNo ratings yet

- Dish TV Investor Presentation UBSDocument23 pagesDish TV Investor Presentation UBSIshan BansalNo ratings yet

- 2010 Interim Results Release: 31 August 2010Document19 pages2010 Interim Results Release: 31 August 2010naderpourNo ratings yet

- Intimation of "Company Overview of GTPL Hathway Limited", A Material Subsidiary of The Company (Company Update)Document15 pagesIntimation of "Company Overview of GTPL Hathway Limited", A Material Subsidiary of The Company (Company Update)Shyam SunderNo ratings yet

- Investor Presentation June 2011Document35 pagesInvestor Presentation June 2011zainu01No ratings yet

- Investor Day 2008: 2008-2010 Strategic Plan PresentationDocument13 pagesInvestor Day 2008: 2008-2010 Strategic Plan PresentationPiaggiogroupNo ratings yet

- Kempower-Q4 Financial-Review Presentation v1Document22 pagesKempower-Q4 Financial-Review Presentation v1cwbjorkendahlNo ratings yet

- Investor / Analyst Presentation (Company Update)Document44 pagesInvestor / Analyst Presentation (Company Update)Shyam SunderNo ratings yet

- Investor Presentation (Company Update)Document27 pagesInvestor Presentation (Company Update)Shyam SunderNo ratings yet

- Media Apr 07Document11 pagesMedia Apr 07uttaramenonNo ratings yet

- Market Research On Potential of DTH Technology in Nashik CityDocument24 pagesMarket Research On Potential of DTH Technology in Nashik CitySweetie PunjabiNo ratings yet

- Assignment For LicensingDocument6 pagesAssignment For Licensingm tvlNo ratings yet

- Telecom Sector: NTP 2011 - A Non-EventDocument3 pagesTelecom Sector: NTP 2011 - A Non-EventAngel BrokingNo ratings yet

- Kempower-Q1 Interim-Report Presentation FinalDocument22 pagesKempower-Q1 Interim-Report Presentation FinalcwbjorkendahlNo ratings yet

- Global IPTV Equipment Market and Provider Competitor AnalysisDocument32 pagesGlobal IPTV Equipment Market and Provider Competitor AnalysisRajesh JainNo ratings yet

- IR PPT May 12 PDFDocument29 pagesIR PPT May 12 PDFmohitegaurv87No ratings yet

- MTAR Technologies Limited: Reaching For The SkiesDocument42 pagesMTAR Technologies Limited: Reaching For The SkiesMajor ShobhitNo ratings yet

- BlueDart PresentationDocument26 pagesBlueDart PresentationSwamiNo ratings yet

- Rough DishDocument6 pagesRough DishmalavyasNo ratings yet

- Presentation (Company Update)Document13 pagesPresentation (Company Update)Shyam SunderNo ratings yet

- Market Research On Potential of DTH TechnologyDocument49 pagesMarket Research On Potential of DTH TechnologysaquibishaqueNo ratings yet

- Falcon Media House Investor Deck 20 March 2017Document33 pagesFalcon Media House Investor Deck 20 March 2017media mindNo ratings yet

- Investor Presentation (Company Update)Document26 pagesInvestor Presentation (Company Update)Shyam SunderNo ratings yet

- Business RadioDocument11 pagesBusiness RadioKaushikBongiriNo ratings yet

- PRO: To Determine The Factors Influencing The Consumer's: Choice of Television Service ProvidersDocument42 pagesPRO: To Determine The Factors Influencing The Consumer's: Choice of Television Service Providersavinasha89No ratings yet

- Report On Budget 2012-13Document4 pagesReport On Budget 2012-13Kunal JainNo ratings yet

- Media and EntertainmentDocument5 pagesMedia and EntertainmentAhmed MastanNo ratings yet

- MTAR Technologies Limited: Reaching For The SkiesDocument41 pagesMTAR Technologies Limited: Reaching For The SkiesMajor ShobhitNo ratings yet

- V Vietnam Ietnam: T Telec Elecommunica Ommunications R Tions Report EportDocument53 pagesV Vietnam Ietnam: T Telec Elecommunica Ommunications R Tions Report EportK59 Tran Kha Vy100% (1)

- Hydrodec INVESTOR PPT October 2013Document28 pagesHydrodec INVESTOR PPT October 2013leblancbjNo ratings yet

- Management MeetDocument4 pagesManagement MeetRohit GadekarNo ratings yet

- Investor Presentation (Company Update)Document28 pagesInvestor Presentation (Company Update)Shyam SunderNo ratings yet

- Institutional Presentation (Roadshow)Document23 pagesInstitutional Presentation (Roadshow)Seye BassirNo ratings yet

- Q3FY24Document36 pagesQ3FY24anik.harry1017No ratings yet

- Media EntertainmentDocument352 pagesMedia EntertainmentArun Venkataramani100% (2)

- Indian Television (Media & Entertainment) Industry & Firm AnalysisDocument19 pagesIndian Television (Media & Entertainment) Industry & Firm AnalysisjackNo ratings yet

- Subscriber Base Continues To Decline: Telecom: December 2012 Subscriber AdditionsDocument0 pagesSubscriber Base Continues To Decline: Telecom: December 2012 Subscriber AdditionsdarshanmaldeNo ratings yet

- DTH Industry in India - Future Prospectus: R. SrinivasanDocument4 pagesDTH Industry in India - Future Prospectus: R. Srinivasanvisakan_kamarajNo ratings yet

- Direct To Home FinalDocument26 pagesDirect To Home FinalRanbir ChimniNo ratings yet

- FDI in The Media and Entertainment IndustryDocument3 pagesFDI in The Media and Entertainment IndustryYogesh Anant WaghNo ratings yet

- NALCO Corporate Presentation 2013Document36 pagesNALCO Corporate Presentation 2013Sahoo SKNo ratings yet

- Idea Cellular Limited: Investor PresentationDocument20 pagesIdea Cellular Limited: Investor PresentationArpita NagarNo ratings yet

- Market Outlook 10th January 2012Document4 pagesMarket Outlook 10th January 2012Angel BrokingNo ratings yet

- FDI in Media & Entertainment: P 4 of 9, para 10Document4 pagesFDI in Media & Entertainment: P 4 of 9, para 10saivsNo ratings yet

- HT Media LTD 1qfy12Document3 pagesHT Media LTD 1qfy12Seema GusainNo ratings yet

- Mitra Company Summary SenergyDocument23 pagesMitra Company Summary Senergyskywalk189No ratings yet

- Bharti-Airtel-Limited - June 5 2009Document24 pagesBharti-Airtel-Limited - June 5 2009kohlinishaNo ratings yet

- Ielts PracticeDocument7 pagesIelts Practicesanjeev thakurNo ratings yet

- Linear and Non-Linear Video and TV Applications: Using IPv6 and IPv6 MulticastFrom EverandLinear and Non-Linear Video and TV Applications: Using IPv6 and IPv6 MulticastNo ratings yet

- Fintech Policy Tool Kit For Regulators and Policy Makers in Asia and the PacificFrom EverandFintech Policy Tool Kit For Regulators and Policy Makers in Asia and the PacificRating: 5 out of 5 stars5/5 (1)

- Annex 6 Documents To Prepare For The Amfori BSCI AuditDocument5 pagesAnnex 6 Documents To Prepare For The Amfori BSCI AuditFabiola FranciaNo ratings yet

- April 2007 Grants Pass Gospel Rescue Mission NewsletterDocument6 pagesApril 2007 Grants Pass Gospel Rescue Mission NewsletterGrants Pass Gospel Rescue MissionNo ratings yet

- How To Perfectly Hide IP Address in PC and SmartphoneDocument17 pagesHow To Perfectly Hide IP Address in PC and SmartphoneFulad AfzaliNo ratings yet

- Spruance Course 2016 SyllabusDocument316 pagesSpruance Course 2016 SyllabusKalyan Kumar SarkarNo ratings yet

- Icic Bank: Icici Bank Limited IsDocument18 pagesIcic Bank: Icici Bank Limited Isvenkatesh RNo ratings yet

- Currency Trader Magazine 2011-06Document31 pagesCurrency Trader Magazine 2011-06Lascu RomanNo ratings yet

- Leader of GRP 1 Science TeacherDocument2 pagesLeader of GRP 1 Science TeacherJoshua De LeonNo ratings yet

- Remember by Sarah Draget LyricsDocument2 pagesRemember by Sarah Draget LyricsKashmyr Faye CastroNo ratings yet

- KasambahayDocument7 pagesKasambahayJanice Dulotan CastorNo ratings yet

- Playing With Thy NameDocument1 pagePlaying With Thy NameArt LadagaNo ratings yet

- Maharaja New DRTDocument18 pagesMaharaja New DRTKannan GopalakrishnanNo ratings yet

- Bismillah Pak Forces: Coaching & Educational Academy (Chiniot)Document2 pagesBismillah Pak Forces: Coaching & Educational Academy (Chiniot)Kamrankhan KamranNo ratings yet

- Pilot Testing - 21st Century LiteratureDocument6 pagesPilot Testing - 21st Century LiteratureTanjiro KamadoNo ratings yet

- ORF IssueBrief 228 BuddhismDocument12 pagesORF IssueBrief 228 BuddhismAnkur RaiNo ratings yet

- Metro Project LATESTDocument39 pagesMetro Project LATESTRahul ChauhanNo ratings yet

- Jeanne G. Quimata: Mitchell F. Thompson, EsqDocument3 pagesJeanne G. Quimata: Mitchell F. Thompson, EsqEquality Case FilesNo ratings yet

- COMMISSIONING AND TRIAL OPERATION Rev01Document2 pagesCOMMISSIONING AND TRIAL OPERATION Rev01Ricardo Escudero VinasNo ratings yet

- Vis The Ruffianly Bitch and A Pair of Grim Shaggy Sheep-Dogs, Who SharedDocument10 pagesVis The Ruffianly Bitch and A Pair of Grim Shaggy Sheep-Dogs, Who SharedChris BartlettNo ratings yet

- BESWMC Plan 2023Document2 pagesBESWMC Plan 2023Maynard Agustin Agraan100% (4)

- East Asian Financial CrisisDocument19 pagesEast Asian Financial CrisisChandrakanti BeheraNo ratings yet

- Report-MKT 623-Promotional MarketingDocument22 pagesReport-MKT 623-Promotional MarketingMd. Faisal ImamNo ratings yet

- Bell Atlantic Corp v. TwomblyDocument4 pagesBell Atlantic Corp v. Twomblylfei1216No ratings yet

- Nova Scotia Home Finder January 2014Document104 pagesNova Scotia Home Finder January 2014Nancy BainNo ratings yet

- Ocak DeryaDocument102 pagesOcak DeryaMátyás SüketNo ratings yet

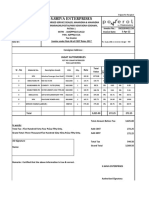

- S.Shiva Enterprises: Jagat AutomobilesDocument2 pagesS.Shiva Enterprises: Jagat AutomobilesS.SHIVA ENTERPRISESNo ratings yet

- René Guénon and InitiationDocument6 pagesRené Guénon and Initiationabaris13No ratings yet