Download as pdf or txt

You might also like

- ECN 204 Final Exam ReviewDocument24 pagesECN 204 Final Exam ReviewLinette YangNo ratings yet

- Cap. 4 - Carlin e Soskice - Solutions Ch. 04Document8 pagesCap. 4 - Carlin e Soskice - Solutions Ch. 04Rafael MatosNo ratings yet

- Investment Multiplier - EconomicsDocument5 pagesInvestment Multiplier - Economicsanon_357116694100% (1)

- Consumption Savings Investment. ParadoxDocument46 pagesConsumption Savings Investment. ParadoxChristine Joy LanabanNo ratings yet

- Consumption FunctionDocument39 pagesConsumption FunctionAnku SharmaNo ratings yet

- Chapter 8 Notes Aggregate Expenditure ModelDocument14 pagesChapter 8 Notes Aggregate Expenditure ModelBeatriz CanchilaNo ratings yet

- Income Determination in Short Run: Basic Model: Ae Y AE (C+I) Ae YDocument31 pagesIncome Determination in Short Run: Basic Model: Ae Y AE (C+I) Ae YAman Singh RajputNo ratings yet

- Chapter 6 (Macro)Document10 pagesChapter 6 (Macro)mashibani01No ratings yet

- Macro - Module - 16 3Document23 pagesMacro - Module - 16 3AlexNo ratings yet

- Week9 Thursday SlidesDocument36 pagesWeek9 Thursday SlidesSiham BuuleNo ratings yet

- Aggregate Expenditure and Equilibrium OutputDocument69 pagesAggregate Expenditure and Equilibrium OutputhongphakdeyNo ratings yet

- Week 9 - SII2013 PDFDocument67 pagesWeek 9 - SII2013 PDFGorge SorosNo ratings yet

- 113 Unit VDocument61 pages113 Unit V21002hadiNo ratings yet

- Business Cycles: The TheoryDocument39 pagesBusiness Cycles: The TheorySagar IndranNo ratings yet

- Consumption Function and MultiplierDocument24 pagesConsumption Function and MultiplierVikku AgarwalNo ratings yet

- Aggregate Supply and Aggregate Demand: R. Santos, "Economics: Principles & Application." Prepared by Rick HelserDocument18 pagesAggregate Supply and Aggregate Demand: R. Santos, "Economics: Principles & Application." Prepared by Rick HelserIndivineNo ratings yet

- WINSEMFY2022-23 TLAW166L TH CH2022232300383 Reference Material I 06-03-2023 Macro MultiplierDocument17 pagesWINSEMFY2022-23 TLAW166L TH CH2022232300383 Reference Material I 06-03-2023 Macro MultiplierHaresh .sNo ratings yet

- Unit 3 Consumption and InvestmentDocument38 pagesUnit 3 Consumption and InvestmentisabelNo ratings yet

- Aggregate Expenditure and Equilibrium OutputDocument69 pagesAggregate Expenditure and Equilibrium Outputwaqar2010No ratings yet

- Determinants of Aggregate Demand: by Samran and The FuduDocument8 pagesDeterminants of Aggregate Demand: by Samran and The FuduNina BahiaNo ratings yet

- Key Term U11Document8 pagesKey Term U11Sam LeNo ratings yet

- Introduction VT2024Document39 pagesIntroduction VT2024aleema anjumNo ratings yet

- Aggregate Demand & Keynesian Multiplier PDFDocument6 pagesAggregate Demand & Keynesian Multiplier PDFArunabh ChoudhuryNo ratings yet

- Economics 2004-06: Section 2: Microeconomics Higher 2.1 Markets 2.2.3 Income Elasticity of DemandDocument22 pagesEconomics 2004-06: Section 2: Microeconomics Higher 2.1 Markets 2.2.3 Income Elasticity of DemandAn-An PhitakchatchawalNo ratings yet

- Chap 5Document24 pagesChap 5Hisham JawharNo ratings yet

- Theories of Consumption and InvestmentDocument25 pagesTheories of Consumption and InvestmentSamridh AgarwalNo ratings yet

- 5.2 Consumption FunctionDocument20 pages5.2 Consumption FunctionAshwini SakpalNo ratings yet

- MultiplierDocument16 pagesMultiplierNaman LadhaNo ratings yet

- IGNOU MEC-002 Free Solved Assignment 2012Document8 pagesIGNOU MEC-002 Free Solved Assignment 2012manish.cdmaNo ratings yet

- Theories of Multiplier, Accelerator and Business CyclesDocument30 pagesTheories of Multiplier, Accelerator and Business CyclesProfessor Tarun DasNo ratings yet

- An Outline of Keynesian Theory of EmploymentDocument26 pagesAn Outline of Keynesian Theory of Employmentsamrulezzz100% (4)

- Aggregate Demand - MacroDocument21 pagesAggregate Demand - MacroHaardik GandhiNo ratings yet

- CB 2 - MacroDocument106 pagesCB 2 - MacroSurbi SabharwalNo ratings yet

- T5 2014 SolutionsDocument6 pagesT5 2014 Solutionsjpvmdv4vg4No ratings yet

- Note Sur La Finance CorporativeDocument19 pagesNote Sur La Finance CorporativewilliamNo ratings yet

- Chapter 2Document35 pagesChapter 2ZachClementNo ratings yet

- The Income Consumption / Income Saving RelationshipDocument13 pagesThe Income Consumption / Income Saving Relationshipkam_bruisterNo ratings yet

- Monetary Policy - MidtermDocument56 pagesMonetary Policy - MidtermCA's HobbyNo ratings yet

- IGNOU MEC-002 Free Solved Assignment 2012Document8 pagesIGNOU MEC-002 Free Solved Assignment 2012manuraj4No ratings yet

- Solution Manual Macroeconomics Robert J Gordon The Answers From The Book On Both The Questions and The Problems Chapter 3Document6 pagesSolution Manual Macroeconomics Robert J Gordon The Answers From The Book On Both The Questions and The Problems Chapter 3Eng Hinji RudgeNo ratings yet

- Consumption and Savings: Banez, Cathrine MaeDocument58 pagesConsumption and Savings: Banez, Cathrine MaeYvonne BerdosNo ratings yet

- Saving and Investment: Principles of Economics by G. Mankiw (Chapter 26) Core Economics (Unit 13: 13.7)Document40 pagesSaving and Investment: Principles of Economics by G. Mankiw (Chapter 26) Core Economics (Unit 13: 13.7)Tawasul Hussain Shah RizviNo ratings yet

- Unit 14 - Unemployment and Fiscal Policy - 1.0Document41 pagesUnit 14 - Unemployment and Fiscal Policy - 1.0Georgius Yeremia CandraNo ratings yet

- Lecture #7 - Theory of Income DeterminationDocument53 pagesLecture #7 - Theory of Income DeterminationMike Viet Hoa NguyenNo ratings yet

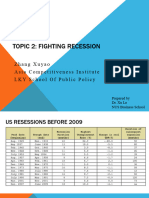

- Week 2 Fighting RecessionDocument42 pagesWeek 2 Fighting Recessiondaisyruyu2001No ratings yet

- Topic (5) - Theory of National Income DeterminationDocument14 pagesTopic (5) - Theory of National Income Determinationfuck offNo ratings yet

- Consumption Function: "Consumption Is The Sole End and Purpose of All Production." Adam SmithDocument28 pagesConsumption Function: "Consumption Is The Sole End and Purpose of All Production." Adam SmithPooja SheoranNo ratings yet

- Saving InvestmentDocument58 pagesSaving InvestmentTumbal GrowtopiaNo ratings yet

- Macro !! Cha 3 $ 4Document54 pagesMacro !! Cha 3 $ 4dehinnetagimasNo ratings yet

- Name: Roll#: Course: Advanced Macroeconomics Code: (806) Level:MSC Economics Semester: Spring, 2021 Assignment No. 2Document12 pagesName: Roll#: Course: Advanced Macroeconomics Code: (806) Level:MSC Economics Semester: Spring, 2021 Assignment No. 2Sajid AliNo ratings yet

- A2 Macro Past Papers Questions' Solutions PDFDocument41 pagesA2 Macro Past Papers Questions' Solutions PDFUzair SiddiquiNo ratings yet

- Macro5 Lecppt ch11Document88 pagesMacro5 Lecppt ch11이가빈[학생](국제대학 국제학과)No ratings yet

- Law of ConsumptionDocument16 pagesLaw of ConsumptionAnkit JoshiNo ratings yet

- National Income and Price DeterminationDocument104 pagesNational Income and Price Determinationhassankazimi23No ratings yet

- 2.2. Saving Investment and The Financial SystemDocument27 pages2.2. Saving Investment and The Financial SystemLEIGHANNE ZYRIL SANTOSNo ratings yet

- Keynesian TheoryDocument98 pagesKeynesian TheorysamrulezzzNo ratings yet

- Economic GrowthDocument23 pagesEconomic GrowthZaid ZubairiNo ratings yet

- Classical Economic TheoryDocument10 pagesClassical Economic Theorymedinearpacioglu8No ratings yet

- The Investment MultiplierDocument12 pagesThe Investment MultipliersurbhissNo ratings yet

- Insurance Brokers in RomaniaDocument10 pagesInsurance Brokers in RomaniaIrina StefanaNo ratings yet

- Insurance Brokers in Romania - Group 136Document10 pagesInsurance Brokers in Romania - Group 136Irina StefanaNo ratings yet

- Written AssignmentDocument2 pagesWritten AssignmentIrina StefanaNo ratings yet

- Statistics ResearchDocument28 pagesStatistics ResearchIrina StefanaNo ratings yet

- Marketing Project - Beer Market AnalysisDocument11 pagesMarketing Project - Beer Market AnalysisIrina StefanaNo ratings yet

- Education Strategy 4-12-2011Document112 pagesEducation Strategy 4-12-2011Jennie PhillipsNo ratings yet

- Bba - 18.06.2018 FinalDocument59 pagesBba - 18.06.2018 FinalSakshi RelanNo ratings yet

- Ey Mena Quarterly Banking Report q2 2020Document26 pagesEy Mena Quarterly Banking Report q2 2020Mira Hout100% (1)

- 1Q3-Rev Summary 93SNA-1Document51 pages1Q3-Rev Summary 93SNA-1pmellaNo ratings yet

- Marco-Economics Assignment: Topic: Is-Lm ModelDocument6 pagesMarco-Economics Assignment: Topic: Is-Lm ModelVishwanath Sagar100% (1)

- Bba 2002 NewDocument21 pagesBba 2002 NewyonghuiNo ratings yet

- ASSIGNMENT II - UNEMPLOYMENT AND INFLATION - Attempt ReviewDocument17 pagesASSIGNMENT II - UNEMPLOYMENT AND INFLATION - Attempt Reviewharleensomal28No ratings yet

- Beco1001 2021 Spring Assignment2Document7 pagesBeco1001 2021 Spring Assignment2K cheangNo ratings yet

- Chapter 10 QuestionsDocument2 pagesChapter 10 QuestionsFreeBooksandMaterialNo ratings yet

- Banking&Ms 13Document29 pagesBanking&Ms 13Manish JaiswalNo ratings yet

- MNI Foreign Exchange Bullet Points - US English - 1Document1 pageMNI Foreign Exchange Bullet Points - US English - 1rancang empatNo ratings yet

- Union Budget 2019-20: Comment by Dr. Pankaj TrivediDocument19 pagesUnion Budget 2019-20: Comment by Dr. Pankaj TrivediVikas AroraNo ratings yet

- Konsep & Macam Indikator Ekonomi: Prof. Insukindro, PH.DDocument21 pagesKonsep & Macam Indikator Ekonomi: Prof. Insukindro, PH.DAndri IantoNo ratings yet

- General Foundations of Managerial EconomicsDocument8 pagesGeneral Foundations of Managerial Economicsmanu8alakode100% (2)

- What Is The Market EconomyDocument17 pagesWhat Is The Market EconomysharifNo ratings yet

- EconomicsDocument12 pagesEconomicsASMARA HABIBNo ratings yet

- The Effect of Reducing Quantitative Easing On Emerging MarketsDocument13 pagesThe Effect of Reducing Quantitative Easing On Emerging MarketsMbongeni ShongweNo ratings yet

- Calvo, G (1988) - Servicing The Public Debt - The Role of ExpectationsDocument16 pagesCalvo, G (1988) - Servicing The Public Debt - The Role of ExpectationsDaniela SanabriaNo ratings yet

- Strategic Management Assignment 2Document8 pagesStrategic Management Assignment 2Shafiq RehmanNo ratings yet

- AS Level Paper 2: CHAPTER 1: Basic Economic Ideas and Resource AllocationDocument32 pagesAS Level Paper 2: CHAPTER 1: Basic Economic Ideas and Resource AllocationLaila100% (1)

- Project Proposal BKH1610076FDocument4 pagesProject Proposal BKH1610076FSalma AkterNo ratings yet

- Eco402-Midterm Solved McqsDocument5 pagesEco402-Midterm Solved McqsNoor VirkNo ratings yet

- Admas University SeminarDocument32 pagesAdmas University SeminarFirezer TeshomeNo ratings yet

- 2021 Annual Economic Survey 20220605 PDFDocument148 pages2021 Annual Economic Survey 20220605 PDFRiannaNo ratings yet

- Bedri Managerial Economics ExamDocument3 pagesBedri Managerial Economics ExamBedri M AhmeduNo ratings yet

- Factors Influencing Economic Growth of BangladeshDocument52 pagesFactors Influencing Economic Growth of BangladeshMahmud EnterpriseNo ratings yet

- Absa Africa Financial Market IndexDocument40 pagesAbsa Africa Financial Market IndexSandraNo ratings yet

- Position Paper IN Economic Development: Topic: Is Inflation Morally Wrong?Document20 pagesPosition Paper IN Economic Development: Topic: Is Inflation Morally Wrong?Robert GarlandNo ratings yet

- Module 1.3 FIN112Document3 pagesModule 1.3 FIN112Pauline Joy LumibaoNo ratings yet

- BSPDocument11 pagesBSPMeloy ApiladoNo ratings yet