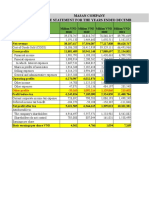

Source of Finance

Source of Finance

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5823)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (898)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (823)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Solution Manual - Partnership & Corporation, 2014-2015 PDFDocument77 pagesSolution Manual - Partnership & Corporation, 2014-2015 PDFRomerJoieUgmadCultura78% (88)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- CA Inter Accounting - Chapter 1Document37 pagesCA Inter Accounting - Chapter 1Gokarakonda Sandeep100% (1)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- MicroEcon Exam 1Document6 pagesMicroEcon Exam 1Paul TuctoNo ratings yet

- QuickbooksDocument54 pagesQuickbooksyes1nth100% (2)

- Nature and Introduction of Investment DecisionsDocument7 pagesNature and Introduction of Investment Decisionsrethvi100% (2)

- Institute of Industrial Electronics Engineering, (Pcsir) KarachiDocument10 pagesInstitute of Industrial Electronics Engineering, (Pcsir) KarachiHassan Ahmed KhanNo ratings yet

- Procurement & Sourcing: Instructor: Mr. Babar KamalDocument19 pagesProcurement & Sourcing: Instructor: Mr. Babar KamalHassan Ahmed KhanNo ratings yet

- Student Name:Arsalan Ahmed Khan Reg. ID:024-18-110489 Program: MBA Instructor: Mr. Babar Kamal Subject: Procurement & SourcingDocument4 pagesStudent Name:Arsalan Ahmed Khan Reg. ID:024-18-110489 Program: MBA Instructor: Mr. Babar Kamal Subject: Procurement & SourcingHassan Ahmed KhanNo ratings yet

- 2e8a45d7deff45379446479d045cb145Document2 pages2e8a45d7deff45379446479d045cb145Hassan Ahmed KhanNo ratings yet

- Arsalan Mid LogisticsDocument3 pagesArsalan Mid LogisticsHassan Ahmed KhanNo ratings yet

- NPVDocument3 pagesNPVHassan Ahmed KhanNo ratings yet

- Arsalan Ahmed CBDocument3 pagesArsalan Ahmed CBHassan Ahmed KhanNo ratings yet

- NPVDocument3 pagesNPVHassan Ahmed KhanNo ratings yet

- SawantQs DavidMoseleyDocument2 pagesSawantQs DavidMoseleyheidigrooverNo ratings yet

- Characteristics of Four Market StructureDocument2 pagesCharacteristics of Four Market StructureClaire Aira TravenioNo ratings yet

- Dabur's Acquisition of Balsara by Tripti N GroupDocument22 pagesDabur's Acquisition of Balsara by Tripti N Grouptripti_verve0% (1)

- Business Model of Unilever IndonesiaDocument18 pagesBusiness Model of Unilever Indonesiayandhie57100% (2)

- Venugopal Gopinatha N Nair: Shoppers Stop LimitedDocument2 pagesVenugopal Gopinatha N Nair: Shoppers Stop LimitedAkchikaNo ratings yet

- Mdi 0618Document24 pagesMdi 0618macc407150% (2)

- Cashflow FormatDocument4 pagesCashflow FormatRaja kumarNo ratings yet

- Tender Specification: Kakatiya Thermal Power ProjectDocument65 pagesTender Specification: Kakatiya Thermal Power Projectisquare77No ratings yet

- Vouching of Building N Bill PayableDocument10 pagesVouching of Building N Bill PayableMohammed BilalNo ratings yet

- SAP UnderstandingDocument5 pagesSAP UnderstandingSanchit BagaiNo ratings yet

- Larsen & ToubroDocument15 pagesLarsen & ToubroAngel BrokingNo ratings yet

- Compound Interest More Than ONCEDocument24 pagesCompound Interest More Than ONCEJennifer MagangoNo ratings yet

- Full FormDocument2 pagesFull FormJemish ItaliyaNo ratings yet

- 2-4 2004 Jun QDocument11 pages2-4 2004 Jun QAjay TakiarNo ratings yet

- Accounting For Bad DebtsDocument3 pagesAccounting For Bad Debtsanurag_09No ratings yet

- MEFADocument4 pagesMEFABangi Sunil KumarNo ratings yet

- Guidance Note On GST Audit ICAI PDFDocument529 pagesGuidance Note On GST Audit ICAI PDFLitesh ChopraNo ratings yet

- Module 4 - ImpairmentDocument5 pagesModule 4 - ImpairmentLuiNo ratings yet

- Course Outline Financial Management-2018-19Document4 pagesCourse Outline Financial Management-2018-19Jayesh MahajanNo ratings yet

- Profile On Granite CuttingDocument12 pagesProfile On Granite CuttingAnkit Morani100% (1)

- Comparative Study of Private and Public SectorDocument7 pagesComparative Study of Private and Public SectorVinay KumarNo ratings yet

- MasanDocument46 pagesMasanNgọc BíchNo ratings yet

- CA CPT Exam December 2012Document24 pagesCA CPT Exam December 2012Tushar BhattacharyyaNo ratings yet

- Acb21103 Tutorial Business Income 2023Document8 pagesAcb21103 Tutorial Business Income 2023alifarhanah6No ratings yet

- Variable Costing: A Tool For Management: Garrison, Noreen, Brewer, Cheng & Yuen Mcgraw-Hill Education (Asia)Document79 pagesVariable Costing: A Tool For Management: Garrison, Noreen, Brewer, Cheng & Yuen Mcgraw-Hill Education (Asia)Kos PaviliunNo ratings yet

Download as docx, pdf, or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5823)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (898)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (823)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Solution Manual - Partnership & Corporation, 2014-2015 PDFDocument77 pagesSolution Manual - Partnership & Corporation, 2014-2015 PDFRomerJoieUgmadCultura78% (88)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- CA Inter Accounting - Chapter 1Document37 pagesCA Inter Accounting - Chapter 1Gokarakonda Sandeep100% (1)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- MicroEcon Exam 1Document6 pagesMicroEcon Exam 1Paul TuctoNo ratings yet

- QuickbooksDocument54 pagesQuickbooksyes1nth100% (2)

- Nature and Introduction of Investment DecisionsDocument7 pagesNature and Introduction of Investment Decisionsrethvi100% (2)

- Institute of Industrial Electronics Engineering, (Pcsir) KarachiDocument10 pagesInstitute of Industrial Electronics Engineering, (Pcsir) KarachiHassan Ahmed KhanNo ratings yet

- Procurement & Sourcing: Instructor: Mr. Babar KamalDocument19 pagesProcurement & Sourcing: Instructor: Mr. Babar KamalHassan Ahmed KhanNo ratings yet

- Student Name:Arsalan Ahmed Khan Reg. ID:024-18-110489 Program: MBA Instructor: Mr. Babar Kamal Subject: Procurement & SourcingDocument4 pagesStudent Name:Arsalan Ahmed Khan Reg. ID:024-18-110489 Program: MBA Instructor: Mr. Babar Kamal Subject: Procurement & SourcingHassan Ahmed KhanNo ratings yet

- 2e8a45d7deff45379446479d045cb145Document2 pages2e8a45d7deff45379446479d045cb145Hassan Ahmed KhanNo ratings yet

- Arsalan Mid LogisticsDocument3 pagesArsalan Mid LogisticsHassan Ahmed KhanNo ratings yet

- NPVDocument3 pagesNPVHassan Ahmed KhanNo ratings yet

- Arsalan Ahmed CBDocument3 pagesArsalan Ahmed CBHassan Ahmed KhanNo ratings yet

- NPVDocument3 pagesNPVHassan Ahmed KhanNo ratings yet

- SawantQs DavidMoseleyDocument2 pagesSawantQs DavidMoseleyheidigrooverNo ratings yet

- Characteristics of Four Market StructureDocument2 pagesCharacteristics of Four Market StructureClaire Aira TravenioNo ratings yet

- Dabur's Acquisition of Balsara by Tripti N GroupDocument22 pagesDabur's Acquisition of Balsara by Tripti N Grouptripti_verve0% (1)

- Business Model of Unilever IndonesiaDocument18 pagesBusiness Model of Unilever Indonesiayandhie57100% (2)

- Venugopal Gopinatha N Nair: Shoppers Stop LimitedDocument2 pagesVenugopal Gopinatha N Nair: Shoppers Stop LimitedAkchikaNo ratings yet

- Mdi 0618Document24 pagesMdi 0618macc407150% (2)

- Cashflow FormatDocument4 pagesCashflow FormatRaja kumarNo ratings yet

- Tender Specification: Kakatiya Thermal Power ProjectDocument65 pagesTender Specification: Kakatiya Thermal Power Projectisquare77No ratings yet

- Vouching of Building N Bill PayableDocument10 pagesVouching of Building N Bill PayableMohammed BilalNo ratings yet

- SAP UnderstandingDocument5 pagesSAP UnderstandingSanchit BagaiNo ratings yet

- Larsen & ToubroDocument15 pagesLarsen & ToubroAngel BrokingNo ratings yet

- Compound Interest More Than ONCEDocument24 pagesCompound Interest More Than ONCEJennifer MagangoNo ratings yet

- Full FormDocument2 pagesFull FormJemish ItaliyaNo ratings yet

- 2-4 2004 Jun QDocument11 pages2-4 2004 Jun QAjay TakiarNo ratings yet

- Accounting For Bad DebtsDocument3 pagesAccounting For Bad Debtsanurag_09No ratings yet

- MEFADocument4 pagesMEFABangi Sunil KumarNo ratings yet

- Guidance Note On GST Audit ICAI PDFDocument529 pagesGuidance Note On GST Audit ICAI PDFLitesh ChopraNo ratings yet

- Module 4 - ImpairmentDocument5 pagesModule 4 - ImpairmentLuiNo ratings yet

- Course Outline Financial Management-2018-19Document4 pagesCourse Outline Financial Management-2018-19Jayesh MahajanNo ratings yet

- Profile On Granite CuttingDocument12 pagesProfile On Granite CuttingAnkit Morani100% (1)

- Comparative Study of Private and Public SectorDocument7 pagesComparative Study of Private and Public SectorVinay KumarNo ratings yet

- MasanDocument46 pagesMasanNgọc BíchNo ratings yet

- CA CPT Exam December 2012Document24 pagesCA CPT Exam December 2012Tushar BhattacharyyaNo ratings yet

- Acb21103 Tutorial Business Income 2023Document8 pagesAcb21103 Tutorial Business Income 2023alifarhanah6No ratings yet

- Variable Costing: A Tool For Management: Garrison, Noreen, Brewer, Cheng & Yuen Mcgraw-Hill Education (Asia)Document79 pagesVariable Costing: A Tool For Management: Garrison, Noreen, Brewer, Cheng & Yuen Mcgraw-Hill Education (Asia)Kos PaviliunNo ratings yet