Download as ppt, pdf, or txt

You might also like

- Week 1.basis Period Change in Accounting Dates - With Q ADocument39 pagesWeek 1.basis Period Change in Accounting Dates - With Q Asahrasaqsd0% (1)

- Income Taxation (Banggawan) - Midterm SolmanDocument10 pagesIncome Taxation (Banggawan) - Midterm Solmanlili64% (11)

- Chapter 1 - Basis Period and Change in Accounting DatesDocument7 pagesChapter 1 - Basis Period and Change in Accounting DatesNURKHAIRUNNISA100% (3)

- Income Tax Practice NotesDocument50 pagesIncome Tax Practice NotesKessy Juma92% (12)

- Notes On Basis PeriodDocument11 pagesNotes On Basis PeriodNajib JalalNo ratings yet

- Basis PeriodDocument58 pagesBasis PeriodEliz ChangNo ratings yet

- Filing Obligation GuidanceDocument10 pagesFiling Obligation GuidanceTaha AhmedNo ratings yet

- Accounting Period: AssignmentDocument15 pagesAccounting Period: Assignmentankitb9No ratings yet

- Basis PeriodDocument26 pagesBasis Periodbehzadji7No ratings yet

- Lesson 5 Accounting PeriodDocument42 pagesLesson 5 Accounting PeriodCASTRO, HANNAH CAMILLE E.No ratings yet

- Accounting PeriodsDocument12 pagesAccounting PeriodspaquibulanzybelleNo ratings yet

- Principles of Accounting: Section - B By: Ghalib Hussain Class - XIDocument7 pagesPrinciples of Accounting: Section - B By: Ghalib Hussain Class - XIGhalib HussainNo ratings yet

- Adjusting EntriesDocument2 pagesAdjusting Entriesyeeaahh56No ratings yet

- Tax317 Topic 1 BPDocument32 pagesTax317 Topic 1 BPhizzat firdausNo ratings yet

- Lecture 3 - Accounting Period and Methods of AccountingDocument21 pagesLecture 3 - Accounting Period and Methods of AccountingSKEETER BRITNEY COSTANo ratings yet

- C4 - Basis PeriodDocument45 pagesC4 - Basis Periodnabilah natashaNo ratings yet

- Taxable Period: General RuleDocument2 pagesTaxable Period: General RuleHanselNo ratings yet

- Chapter 4 Basis Period 2023-10-30 02 - 00 - 05Document43 pagesChapter 4 Basis Period 2023-10-30 02 - 00 - 05amyNo ratings yet

- Basis PeriodDocument3 pagesBasis PeriodAbhiraj RNo ratings yet

- Abdelrahman Samy - Fiscal YearDocument6 pagesAbdelrahman Samy - Fiscal Yearabdelrahmansamy181No ratings yet

- Fiscal YearDocument8 pagesFiscal Yearakki72000No ratings yet

- PDF 20221213 214318 0000 PDFDocument117 pagesPDF 20221213 214318 0000 PDFNCTDREAM 07No ratings yet

- Tax Calender: San Corporate Advisors PVT LTD in Association With A N GAWADE & CO, Chartered AccountantsDocument6 pagesTax Calender: San Corporate Advisors PVT LTD in Association With A N GAWADE & CO, Chartered AccountantsvruaklNo ratings yet

- WEEK 4.4 - 5.4 - Accounting Learning GainsDocument1 pageWEEK 4.4 - 5.4 - Accounting Learning Gainskyla perezNo ratings yet

- Accounting Periods and MethodsDocument51 pagesAccounting Periods and MethodsKenzel lawasNo ratings yet

- Lesson 4 Tax Accounting PrinciplesDocument25 pagesLesson 4 Tax Accounting PrincipleslehbhronephilipNo ratings yet

- Lecture 3 Concept of Income Accounting Period and Methods of AccountingDocument21 pagesLecture 3 Concept of Income Accounting Period and Methods of AccountingCassie ParkNo ratings yet

- Accounting Periods and Methods and Other Compliance RequirementsDocument5 pagesAccounting Periods and Methods and Other Compliance RequirementsTurks50% (2)

- Practice Note On Change in Accounting DateDocument8 pagesPractice Note On Change in Accounting DatememphixxNo ratings yet

- IAS34:Interim Financial ReportingDocument37 pagesIAS34:Interim Financial ReportingTanvir HossainNo ratings yet

- Fiscal Year (2611)Document16 pagesFiscal Year (2611)David PendyalaNo ratings yet

- Adjusting EntriesDocument21 pagesAdjusting EntriesRegine ChuaNo ratings yet

- Closing Entries: Done By: SeyedDocument11 pagesClosing Entries: Done By: SeyedSeyed Mohammad Ahlesaadat0% (1)

- Tutorial Chapter 1Document2 pagesTutorial Chapter 1SITI HAMIZAH HAMZAHNo ratings yet

- Concept of Previous Year and Assessment YearDocument7 pagesConcept of Previous Year and Assessment YearGoldi Ks100% (1)

- MMPV & MMRVDocument4 pagesMMPV & MMRVJp PrabakarNo ratings yet

- Shortend Fiscal Year Variant GoodDocument5 pagesShortend Fiscal Year Variant GoodDhivya DhanalakshmiNo ratings yet

- HC1011/HF1008: Topic 5 Accounting Cycle & Accounting SystemsDocument9 pagesHC1011/HF1008: Topic 5 Accounting Cycle & Accounting SystemsleNo ratings yet

- Các Dạng Bài Tập Trong Tax f6Document1 pageCác Dạng Bài Tập Trong Tax f6namhua54No ratings yet

- Fiscal Year and Calendar YearDocument9 pagesFiscal Year and Calendar YearbngideaNo ratings yet

- Fundamentals of EconomicsDocument6 pagesFundamentals of EconomicsUsman Qureshii - YTNo ratings yet

- Basis PeriodDocument9 pagesBasis PeriodaishahNo ratings yet

- Introduction To Adjusting Entries DDocument14 pagesIntroduction To Adjusting Entries DYuj Cuares Cervantes100% (1)

- Session 2Document13 pagesSession 2Jahnvi DubeyNo ratings yet

- Unit 3. Audit of Receivables, Related Revenues and Credit Losses - Handout - Final - t31516Document9 pagesUnit 3. Audit of Receivables, Related Revenues and Credit Losses - Handout - Final - t31516mimi96No ratings yet

- Chap05-Completing The Accounting CycleDocument23 pagesChap05-Completing The Accounting CycleParesh PrasadNo ratings yet

- Tutorial 3 - Basis Period (Continue)Document2 pagesTutorial 3 - Basis Period (Continue)Chan Ying100% (1)

- Introduction To Adjusting EntriesDocument1 pageIntroduction To Adjusting EntriesAnj HwanNo ratings yet

- Accounting Cycle, Entries and ConceptDocument64 pagesAccounting Cycle, Entries and Conceptdude devil100% (1)

- Profit or Loss Pre and Post Incorporation PDFDocument59 pagesProfit or Loss Pre and Post Incorporation PDFsvenkat375% (4)

- Adjusting EntriesDocument7 pagesAdjusting EntriesAleck CondesNo ratings yet

- Terms of SaleDocument6 pagesTerms of SaleMary100% (1)

- 7taxyear 130817074826 Phpapp02Document7 pages7taxyear 130817074826 Phpapp02inamooNo ratings yet

- Microsoft Dynamics AX Shared Financial Data Management White Paper PDFDocument18 pagesMicrosoft Dynamics AX Shared Financial Data Management White Paper PDFArturo GonzalezNo ratings yet

- Chapter 4-Case 1 - CommencementDocument9 pagesChapter 4-Case 1 - CommencementgerlaniamelgacoNo ratings yet

- Periodicity AssumptionDocument1 pagePeriodicity AssumptionElla SimoneNo ratings yet

- Summary of Recent Accounting and Auditing Standards (With Effective Dates and Salient Points)Document4 pagesSummary of Recent Accounting and Auditing Standards (With Effective Dates and Salient Points)Charles B. HallNo ratings yet

- Generally Accepted Accounting Principle: GaapDocument19 pagesGenerally Accepted Accounting Principle: GaapediwowNo ratings yet

- ACT 501 - AssignmentDocument6 pagesACT 501 - AssignmentShariful Islam ShaheenNo ratings yet

- Financial Accounting - Want to Become Financial Accountant in 30 Days?From EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Rating: 3.5 out of 5 stars3.5/5 (2)

- Budget AnalysisDocument27 pagesBudget AnalysisSaurabh GNo ratings yet

- D) CIR Vs Standard Chartered Bank G.R. 192173, July 29, 2015Document67 pagesD) CIR Vs Standard Chartered Bank G.R. 192173, July 29, 2015JouseffLionelColosoMacolNo ratings yet

- Input Tax CreditDocument16 pagesInput Tax CreditPreeti SapkalNo ratings yet

- Bill FormatDocument7 pagesBill FormatJay Rupchandani100% (1)

- Tax 1Document43 pagesTax 1opep77No ratings yet

- Invoice 2022 06Document2 pagesInvoice 2022 06violetaNo ratings yet

- InvoiceDocument1 pageInvoicemohammad touffiqueNo ratings yet

- Opinion On Tax Residency Certificate Recipient: RECIPIENT NAME Date - 15th Mar, 2023Document4 pagesOpinion On Tax Residency Certificate Recipient: RECIPIENT NAME Date - 15th Mar, 2023Akash BagrechaNo ratings yet

- Strategi Peningkatan Penerimaan Pendapatan Pajak Reklame Dikabupaten BogorDocument16 pagesStrategi Peningkatan Penerimaan Pendapatan Pajak Reklame Dikabupaten BogorZulNo ratings yet

- 12A & 80G ProcedureDocument4 pages12A & 80G ProcedurekshripalNo ratings yet

- 26096442469Document1 page26096442469Alaric Manen JamirNo ratings yet

- Quiz 2 - ACGN PrelimsDocument8 pagesQuiz 2 - ACGN Prelimsnatalie clyde matesNo ratings yet

- IDT SaranshDocument204 pagesIDT Saranshconnectsujata1No ratings yet

- The Payroll Cycle: Learning ObjectivesDocument19 pagesThe Payroll Cycle: Learning ObjectivesChaitu ChaituNo ratings yet

- InvoiceDocument1 pageInvoiceShahil Kumar ShawNo ratings yet

- TAX QuizzesDocument2 pagesTAX Quizzesnichols greenNo ratings yet

- Equilibrium Income and Output: Two-Sector Economy Y C+IDocument52 pagesEquilibrium Income and Output: Two-Sector Economy Y C+ISunu 3670100% (1)

- Angeles City Vs Angeles City Electric CorporationDocument1 pageAngeles City Vs Angeles City Electric CorporationJesse MoranteNo ratings yet

- R SwieratDocument2 pagesR SwieratDe Gen G.No ratings yet

- B6XK73831W5692124RDocument2 pagesB6XK73831W5692124RB02 - Alingayao, Mitchjohnlee C.No ratings yet

- Research Proposal GDocument12 pagesResearch Proposal Gአዲሱ ዞላNo ratings yet

- DR Rohit JainDocument1 pageDR Rohit JainlxshNo ratings yet

- Computation FY 21-22Document2 pagesComputation FY 21-22gondaliyaconsultancy0909No ratings yet

- Orlando Manufacturing Company Makes Camping Equipment Selected Account Balances ListedDocument1 pageOrlando Manufacturing Company Makes Camping Equipment Selected Account Balances ListedMiroslav GegoskiNo ratings yet

- Letter - RoU Permission To GSEG Water PipelineDocument3 pagesLetter - RoU Permission To GSEG Water Pipelinepriyanka babu prustyNo ratings yet

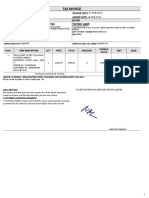

- Tax Invoice Ashutosh Kumar: Billing Period Invoice Date Amount Payable Due Date Amount After Due DateDocument2 pagesTax Invoice Ashutosh Kumar: Billing Period Invoice Date Amount Payable Due Date Amount After Due DateAshutosh KumarNo ratings yet

- Po 690000087Document1 pagePo 690000087Eka Dwi PutraNo ratings yet

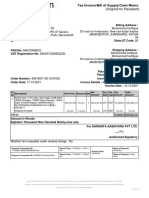

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Mohd UvaisNo ratings yet

- Subnational Taxation in Developing Countries: A Review of The LiteratureDocument24 pagesSubnational Taxation in Developing Countries: A Review of The LiteratureKelas MPA Fiskal Kelompok 2No ratings yet