Download as pptx, pdf, or txt

You might also like

- A Case Study in Soccer EthicsDocument4 pagesA Case Study in Soccer Ethicsapi-343966267No ratings yet

- Spencer Lawsuit ComplaintDocument15 pagesSpencer Lawsuit ComplaintLas Vegas Review-JournalNo ratings yet

- Corporate Tax Planning Unit-2 E-Text Module 5 & 6: Residential Status & Taxation of Companies Scope of Total Incidence of Tax (Section 5)Document10 pagesCorporate Tax Planning Unit-2 E-Text Module 5 & 6: Residential Status & Taxation of Companies Scope of Total Incidence of Tax (Section 5)imamNo ratings yet

- 01 Section 9Document54 pages01 Section 9ABHIJEETNo ratings yet

- ch-11 Taxation of NRIsDocument25 pagesch-11 Taxation of NRIsdean.socNo ratings yet

- Income Deemed To Arise in IndiaDocument7 pagesIncome Deemed To Arise in IndiaDebaNo ratings yet

- Introduction To ResidenceDocument4 pagesIntroduction To ResidenceNiya Maria NixonNo ratings yet

- Income Tax ActDocument12 pagesIncome Tax ActSomnath GuptaNo ratings yet

- Incidence of TaxDocument53 pagesIncidence of TaxAnurag SindhalNo ratings yet

- Permanent Esta ResearchDocument24 pagesPermanent Esta ResearchNeha PandeyNo ratings yet

- Principles of Taxation Law - (Week 6)Document56 pagesPrinciples of Taxation Law - (Week 6)ishikakeswani4No ratings yet

- Residential Status and Incidence of Tax - Study MaterialDocument6 pagesResidential Status and Incidence of Tax - Study MaterialEmeline SoroNo ratings yet

- Taxation Direct Tax Code Assignment 2: SUBMITTED TO: Mrs. Ranjani Matta SUBMITTED BY: Shalini MahawarDocument6 pagesTaxation Direct Tax Code Assignment 2: SUBMITTED TO: Mrs. Ranjani Matta SUBMITTED BY: Shalini MahawarShalini MahawarNo ratings yet

- Section 9 of Income Tax Act 1961Document55 pagesSection 9 of Income Tax Act 1961Bharath SimhaReddyNaiduNo ratings yet

- UNIT 1 - CT - Part 1Document39 pagesUNIT 1 - CT - Part 1Amogh AroraNo ratings yet

- Week 4-7Document9 pagesWeek 4-7Vijayant DalalNo ratings yet

- Direct Tax Summary NotesDocument88 pagesDirect Tax Summary NotesAlisha LukeNo ratings yet

- Income Deemed To Accrue or Arise in India-Sec 9Document16 pagesIncome Deemed To Accrue or Arise in India-Sec 9drive8124No ratings yet

- Basis of Charge and Scope of TotalDocument24 pagesBasis of Charge and Scope of TotalSujithNo ratings yet

- Sec 9Document39 pagesSec 9Akanksha BohraNo ratings yet

- 9Document4 pages9SPARSH KAPOORNo ratings yet

- e Book PDF PDFDocument91 pagese Book PDF PDFGiri SukumarNo ratings yet

- Sia - Itax-2018-19Document17 pagesSia - Itax-2018-19Abhay Pethani.No ratings yet

- 1518759148pdfjoiner PDFDocument40 pages1518759148pdfjoiner PDFAlkaNo ratings yet

- Semester V Direct Tax Residence & Scope of Total Income A/087/Divya KamaliyaDocument14 pagesSemester V Direct Tax Residence & Scope of Total Income A/087/Divya KamaliyaHarsh KamaliyaNo ratings yet

- Section 9Document7 pagesSection 9Achulendra Ji PushkarNo ratings yet

- Tax Planning For An NRI: Pratul JainDocument3 pagesTax Planning For An NRI: Pratul Jainjanardhan lalwaniNo ratings yet

- Income Deemed To Accrue or Arise in IndiaDocument2 pagesIncome Deemed To Accrue or Arise in IndiaDhirendra SinghNo ratings yet

- Unit 3Document20 pagesUnit 3Ram KrishnaNo ratings yet

- Subject: Taxation Law-I: Chanakya National Law University, PatnaDocument20 pagesSubject: Taxation Law-I: Chanakya National Law University, PatnaKritika SinghNo ratings yet

- Benefits Available To Non ResidentsDocument16 pagesBenefits Available To Non ResidentsArchita TiwariNo ratings yet

- Taxation: Residential Status (Part II)Document9 pagesTaxation: Residential Status (Part II)Vineet RajNo ratings yet

- Hand Out Vodafone International Holdings BDocument11 pagesHand Out Vodafone International Holdings Bprernachopra88No ratings yet

- Residential Status and Tax IncidenceDocument3 pagesResidential Status and Tax Incidenceambarishan mrNo ratings yet

- TDS On Commission To Non ResidentDocument6 pagesTDS On Commission To Non ResidentAdityaNo ratings yet

- Notes LLB Tax Nav 2Document12 pagesNotes LLB Tax Nav 2amit HCSNo ratings yet

- TaxationDocument15 pagesTaxationharshithaaba8No ratings yet

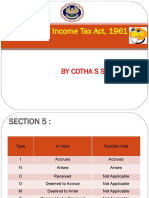

- Income Tax Act, 1961: Section - 5: Scope of Total IncomeDocument15 pagesIncome Tax Act, 1961: Section - 5: Scope of Total IncomeNisseem KrishnaNo ratings yet

- Residential Status and Taxation For Individuals - Taxguru - inDocument2 pagesResidential Status and Taxation For Individuals - Taxguru - inSubhamNo ratings yet

- Notes LLB Tax NavDocument33 pagesNotes LLB Tax Navamit HCSNo ratings yet

- Day4 Residential Status and Incidence of Tax (9 Oct)Document12 pagesDay4 Residential Status and Incidence of Tax (9 Oct)1986anuNo ratings yet

- Residential StatusDocument3 pagesResidential StatusMd DanishNo ratings yet

- Checklist For 15CBDocument4 pagesChecklist For 15CBKrishna S MohanNo ratings yet

- Taxation of Foreign Companies in Direct Taxes Code Bill PDFDocument6 pagesTaxation of Foreign Companies in Direct Taxes Code Bill PDFrajdeeppawarNo ratings yet

- Residential Status & Tax Incidence: DR Amit Kumar SinhaDocument14 pagesResidential Status & Tax Incidence: DR Amit Kumar SinhaasifanisNo ratings yet

- Income Tax Law & Practice: Unit 1Document30 pagesIncome Tax Law & Practice: Unit 1jaspreet kaurNo ratings yet

- PWC Regulatory Insights 13 August 2021 Overseas Investment Regulations Under Fema 1999 Draft Rules RegulationsDocument5 pagesPWC Regulatory Insights 13 August 2021 Overseas Investment Regulations Under Fema 1999 Draft Rules RegulationsStikcon PmcNo ratings yet

- Budget2017 18sudha 170215110415Document89 pagesBudget2017 18sudha 170215110415Taxpert mukeshNo ratings yet

- Non Resident TaxationDocument123 pagesNon Resident Taxationguru1barkiNo ratings yet

- Report Tax RevDocument10 pagesReport Tax RevMarga ErumNo ratings yet

- Income Tax Brief NotesDocument184 pagesIncome Tax Brief NotesCreanativeNo ratings yet

- Unit VI Income Tax ActDocument29 pagesUnit VI Income Tax ActNeha GeorgeNo ratings yet

- Unit VI5942Document29 pagesUnit VI5942Neha GeorgeNo ratings yet

- IncomeTax MaterialDocument91 pagesIncomeTax MaterialSandeep JaiswalNo ratings yet

- Scope of Total Income and Residential StatusDocument3 pagesScope of Total Income and Residential StatusSandeep SinghNo ratings yet

- College of Legal Studies Topic: Critical Analysis of Vodafone vs. Union of IndiaDocument33 pagesCollege of Legal Studies Topic: Critical Analysis of Vodafone vs. Union of IndiaNalini chandrakarNo ratings yet

- Form 15Cb: U. Mohanan & Co Chartered AccountantDocument4 pagesForm 15Cb: U. Mohanan & Co Chartered AccountantKrishna S MohanNo ratings yet

- Foreign Investment in IndiaDocument10 pagesForeign Investment in Indiaramashankar10No ratings yet

- Residential Status DC 2023-24Document11 pagesResidential Status DC 2023-24avinashhpv7785No ratings yet

- A Brief About Foreign Direct Investment in India A Brief About Foreign Direct Investment in IndiaDocument3 pagesA Brief About Foreign Direct Investment in India A Brief About Foreign Direct Investment in Indiaabc defNo ratings yet

- Taxation 2Document14 pagesTaxation 2iemhardikNo ratings yet

- Bar Exam 2016 Suggested Answers in Political Law by The UP Law ComplexDocument11 pagesBar Exam 2016 Suggested Answers in Political Law by The UP Law ComplexJha NizNo ratings yet

- Zoning Appeal - Martinez Briefs - Court of Common PleasDocument32 pagesZoning Appeal - Martinez Briefs - Court of Common PleasScrap The YardNo ratings yet

- Chapter 49:01 - Hides and Skins Export: Subsidiary Legislation Index To Subsidiary Legislation Hides and Skins RegulationsDocument11 pagesChapter 49:01 - Hides and Skins Export: Subsidiary Legislation Index To Subsidiary Legislation Hides and Skins RegulationsHenry MutungaNo ratings yet

- 06 Law On Public OfficersDocument39 pages06 Law On Public OfficersD Del SalNo ratings yet

- Notice, Agenda and MinutesDocument14 pagesNotice, Agenda and MinutesRaju KumarNo ratings yet

- Cases Evidence - Remedial Law2Document169 pagesCases Evidence - Remedial Law2play_pauseNo ratings yet

- Gitlow vs. New York, 268 US 652 (1925)Document23 pagesGitlow vs. New York, 268 US 652 (1925)Harold Q. GardonNo ratings yet

- Government Gazette - 26th AprilDocument96 pagesGovernment Gazette - 26th AprilistructeNo ratings yet

- SCR - Calculation of Accentric Fator by Various MethodsDocument9 pagesSCR - Calculation of Accentric Fator by Various MethodsscranderiNo ratings yet

- Law Test Series Question OnlyDocument2 pagesLaw Test Series Question OnlyNikhil BalanNo ratings yet

- Terrence Burns, M.D. John Zoll v. Imagine Films Entertainment, Inc. Universal City Studies, Inc. McA Inc., 108 F.3d 329, 2d Cir. (1997)Document6 pagesTerrence Burns, M.D. John Zoll v. Imagine Films Entertainment, Inc. Universal City Studies, Inc. McA Inc., 108 F.3d 329, 2d Cir. (1997)Scribd Government DocsNo ratings yet

- Booth Application For Independence FestivalDocument2 pagesBooth Application For Independence FestivalSCGC_ChamberNo ratings yet

- Us Court SystemDocument3 pagesUs Court SystemPhương Linh NguyễnNo ratings yet

- Book Review HomegoingDocument3 pagesBook Review HomegoingAbdirisack Ahmed AdenNo ratings yet

- De Gala Vs Gonzales Compared From Garcia Vs LacuestaDocument10 pagesDe Gala Vs Gonzales Compared From Garcia Vs LacuestaGerald GarcianoNo ratings yet

- Standalone Financial Results, Limited Review Report For December 31, 2016 (Result)Document4 pagesStandalone Financial Results, Limited Review Report For December 31, 2016 (Result)Shyam SunderNo ratings yet

- Cesarini v. USDocument3 pagesCesarini v. USDez BernaldezNo ratings yet

- DRAFT IRP For BarangaysDocument12 pagesDRAFT IRP For BarangaysMark Ajay Marino Grefaldio100% (1)

- Thai Visa FormDocument2 pagesThai Visa FormKalindaMadusankaDasanayakaNo ratings yet

- Tarlo's Estate: Supreme Court of PennsylvaniaDocument7 pagesTarlo's Estate: Supreme Court of Pennsylvaniaramos.jjmrNo ratings yet

- Integrated Bar of The Philippines IBP IBPDocument10 pagesIntegrated Bar of The Philippines IBP IBPyannie isananNo ratings yet

- 14 Vda de Herrera v. Bernardo (Lee)Document1 page14 Vda de Herrera v. Bernardo (Lee)Stefan Henry P. RodriguezNo ratings yet

- Goalkeeper HandbookDocument13 pagesGoalkeeper HandbookMiguel Martin JimeneszNo ratings yet

- Private Placement & Venture CapitalDocument18 pagesPrivate Placement & Venture Capitalshraddha mehtaNo ratings yet

- Department of Labor: 05 586Document6 pagesDepartment of Labor: 05 586USA_DepartmentOfLaborNo ratings yet

- Indian Law On LsDocument20 pagesIndian Law On LsShahrukh KhanNo ratings yet

- 18LLB080 A Case Study of Rudul Sah V State of BiharDocument21 pages18LLB080 A Case Study of Rudul Sah V State of BiharSanskar JainNo ratings yet

- AJ Jarrett-Damons Determined WolfDocument134 pagesAJ Jarrett-Damons Determined WolfAia Garcia0% (1)