Presentation On Airtel and Cell Phone Service Industry

Presentation On Airtel and Cell Phone Service Industry

You might also like

- Factors That Affect Reference Group InfluenceDocument3 pagesFactors That Affect Reference Group Influencegagan1509589571% (7)

- Chap 018Document27 pagesChap 018Xeniya Morozova Kurmayeva100% (3)

- Consulting Casebook 2019Document135 pagesConsulting Casebook 2019Hari Chandana100% (1)

- Airtel Service BlueprintDocument56 pagesAirtel Service BlueprintManish Gupta50% (2)

- Media Planning and Buying: Notes and PPT by Prof - Chahat HargunaniDocument35 pagesMedia Planning and Buying: Notes and PPT by Prof - Chahat HargunaniHarsha Bulani Chahat Hargunani100% (1)

- Betterment Demographics ReportDocument6 pagesBetterment Demographics ReportConnor LeeNo ratings yet

- R12.x Oracle Enterprise Asset Management FundamentalsDocument4 pagesR12.x Oracle Enterprise Asset Management FundamentalsSundar Kumar Vasantha GovindarajuluNo ratings yet

- PORTER 5 ForcesDocument4 pagesPORTER 5 ForcesMiley MartinNo ratings yet

- Telecom Sector Porter's 5 Force AnalysisDocument3 pagesTelecom Sector Porter's 5 Force AnalysisKARTIK ANAND100% (1)

- Airtel Strategic ManagementDocument29 pagesAirtel Strategic ManagementSandeep George80% (5)

- Report - Contemporary IssuesDocument5 pagesReport - Contemporary IssuesNiha SayyadNo ratings yet

- FinalyticsDocument3 pagesFinalyticschakshu chawlaNo ratings yet

- Strategic Audit of BSNLDocument42 pagesStrategic Audit of BSNLNishant Ahuja0% (1)

- Analysis of Vodafone Essar IndiaDocument34 pagesAnalysis of Vodafone Essar Indiachapal07No ratings yet

- Strategic Audit of BSNLDocument42 pagesStrategic Audit of BSNLNishant AhujaNo ratings yet

- Marketing Environment of AirtelDocument7 pagesMarketing Environment of AirtelTakauv-thiyagi Thiyagu0% (1)

- Porter's Five Forces Model: 1. Threat of New Entrants - LowDocument2 pagesPorter's Five Forces Model: 1. Threat of New Entrants - Low138PATEL KHYATIMMSBNo ratings yet

- Bharti Value Chain AnalysisDocument3 pagesBharti Value Chain AnalysisAnkit Bansal0% (1)

- 6 Meera Arora 1730 Review Article VSRDIJBMR April 2013 PDFDocument8 pages6 Meera Arora 1730 Review Article VSRDIJBMR April 2013 PDFAru BhartiNo ratings yet

- Group B AirtelDocument29 pagesGroup B AirtelPranitha_Shett_7109No ratings yet

- Kinny Jain Nikhil Saraf Dionysiamichalopoulou Rajinder Pal SinghDocument39 pagesKinny Jain Nikhil Saraf Dionysiamichalopoulou Rajinder Pal SinghKanchan VardhaniNo ratings yet

- SWOT Analysis On Jio: StrengthDocument3 pagesSWOT Analysis On Jio: StrengthAmal Raj SinghNo ratings yet

- SWOT JioDocument3 pagesSWOT JioAmal Raj SinghNo ratings yet

- AirtelDocument31 pagesAirtelRajiv KeshriNo ratings yet

- Advertising Effectiveness On Telecom Ind - ProjectDocument51 pagesAdvertising Effectiveness On Telecom Ind - Projecttina_18No ratings yet

- Report On Industry, Competitive, SPACE Matrix Analysis For Telecom Industry - TATA Tele Services, Bharti AirtelDocument18 pagesReport On Industry, Competitive, SPACE Matrix Analysis For Telecom Industry - TATA Tele Services, Bharti AirtelankitsuroliaNo ratings yet

- AirtelDocument19 pagesAirtelSabyasachi DebNo ratings yet

- Business Strategy Assignment - Final TelecomDocument10 pagesBusiness Strategy Assignment - Final TelecomAishwarya SankhlaNo ratings yet

- Airtel 1Document39 pagesAirtel 1Sameer AggarwalNo ratings yet

- What Is An IndustryDocument8 pagesWhat Is An IndustrypritamNo ratings yet

- Project AIRTELDocument58 pagesProject AIRTELSonal LuthraNo ratings yet

- Customer Satisfaction: Summer Project Report ONDocument75 pagesCustomer Satisfaction: Summer Project Report ONManjeet SinghNo ratings yet

- Comparison Between Two Brands Airtel Vs HutchDocument8 pagesComparison Between Two Brands Airtel Vs HutchAdithya Anuroop SridharanNo ratings yet

- Kinny Jain Nikhil Saraf Dionysiamichalopoulou Rajinder Pal SinghDocument39 pagesKinny Jain Nikhil Saraf Dionysiamichalopoulou Rajinder Pal SinghPrashant KumarNo ratings yet

- Final ReportDocument51 pagesFinal ReportNaveen Kumar VenigallaNo ratings yet

- Bharti Airtel PresentationDocument32 pagesBharti Airtel PresentationNaina ChetwaniNo ratings yet

- Idea Cellular StrategyDocument34 pagesIdea Cellular Strategysdrkmau50% (2)

- Swot Analysis of Bharti Airtel Mobile ServicesDocument6 pagesSwot Analysis of Bharti Airtel Mobile ServicesAnusree RavikumarNo ratings yet

- Airtel - Targeting High Paying Customers and Foreign Partners To Offset Declining Revenues and Market ShareDocument16 pagesAirtel - Targeting High Paying Customers and Foreign Partners To Offset Declining Revenues and Market ShareNikhil KumarNo ratings yet

- Company IdeaDocument8 pagesCompany IdeaishanNo ratings yet

- Indian Telecom Industry-Porter's 5 Force Model: by - Sukanya Roy Chowdhury & Abhirup Roy ChoudhuryDocument41 pagesIndian Telecom Industry-Porter's 5 Force Model: by - Sukanya Roy Chowdhury & Abhirup Roy Choudhurysuku1983No ratings yet

- Assingment On Stratergic Management: Submitted By: Sampada KarpateDocument15 pagesAssingment On Stratergic Management: Submitted By: Sampada Karpateashish chaturvediNo ratings yet

- StartgyDocument7 pagesStartgyshafeeqaliNo ratings yet

- SWOT ANALYSIS Chapter SixDocument8 pagesSWOT ANALYSIS Chapter SixSetu MehtaNo ratings yet

- Analysis of Vodafone Essar IndiaDocument34 pagesAnalysis of Vodafone Essar IndiaSantosh SamNo ratings yet

- Porter Five Forces WordDocument11 pagesPorter Five Forces WordvinodvahoraNo ratings yet

- BHARTI AIRTEL Suvendu & NitinDocument3 pagesBHARTI AIRTEL Suvendu & Nitinsuvendu08No ratings yet

- Study of Competitive Rivalry in Indian Telecom SectorDocument18 pagesStudy of Competitive Rivalry in Indian Telecom Sectorarnabnitw100% (1)

- Can The Telecom Industry Welcome The New Entrants? Ms. Ambika Rathi, Mr. Rajesh VermaDocument8 pagesCan The Telecom Industry Welcome The New Entrants? Ms. Ambika Rathi, Mr. Rajesh VermaPijush Kanti DolaiNo ratings yet

- Vodafone-Brand ManagementDocument63 pagesVodafone-Brand ManagementKuntal PanjaNo ratings yet

- Merger and AcquisitionDocument5 pagesMerger and AcquisitionShilpiNo ratings yet

- Objective of The Study: Literature ReviewDocument15 pagesObjective of The Study: Literature ReviewAanchal PatnahaNo ratings yet

- AIRTELDocument104 pagesAIRTELNazuk Batra100% (1)

- CFM - Bharti AirtelDocument12 pagesCFM - Bharti Airtel202022030 imtnagNo ratings yet

- Report On Airtel Market Analysis: AcknowledgementDocument13 pagesReport On Airtel Market Analysis: AcknowledgementGIRIJANo ratings yet

- Report On Brand Image of Nokia MobileDocument14 pagesReport On Brand Image of Nokia MobileMuhammed MusthafaNo ratings yet

- Security Analysis AssignmentDocument14 pagesSecurity Analysis AssignmentShivam V PunyaniNo ratings yet

- Alhad 504-AirtelDocument11 pagesAlhad 504-AirtelAlhad PosamNo ratings yet

- Cellular Technologies for Emerging Markets: 2G, 3G and BeyondFrom EverandCellular Technologies for Emerging Markets: 2G, 3G and BeyondNo ratings yet

- Papers on the field: Telecommunication Economic, Business, Regulation & PolicyFrom EverandPapers on the field: Telecommunication Economic, Business, Regulation & PolicyNo ratings yet

- An Introduction to SDN Intent Based NetworkingFrom EverandAn Introduction to SDN Intent Based NetworkingRating: 5 out of 5 stars5/5 (1)

- A Skill Based Pay SystemDocument12 pagesA Skill Based Pay Systemgagan15095895No ratings yet

- Carf Paper 2 - Hedging Currency Risk in International Investment and TradeDocument26 pagesCarf Paper 2 - Hedging Currency Risk in International Investment and Tradebalasurya4321No ratings yet

- Chap 019Document9 pagesChap 019gagan15095895No ratings yet

- Vision & Mission StatementDocument1 pageVision & Mission Statementgagan15095895No ratings yet

- Institutional Infrastructure For Export PromotionDocument68 pagesInstitutional Infrastructure For Export Promotiongagan1509589580% (5)

- New QuessinnaireDocument4 pagesNew Quessinnairegagan15095895No ratings yet

- Basic Facts About JammuDocument7 pagesBasic Facts About Jammugagan15095895No ratings yet

- Case Study of CresentDocument3 pagesCase Study of Cresentgagan15095895No ratings yet

- DGFTDocument35 pagesDGFTgagan15095895No ratings yet

- Kandla SezDocument5 pagesKandla Sezgagan15095895No ratings yet

- Competitor Brand Analysis of Nirma DetergentDocument31 pagesCompetitor Brand Analysis of Nirma Detergentgagan15095895100% (1)

- Classical Encryption Techniques: Symmetric Ciphers (Class-L4 & L5)Document13 pagesClassical Encryption Techniques: Symmetric Ciphers (Class-L4 & L5)gagan15095895No ratings yet

- Presentation of Subsidiary BooksDocument37 pagesPresentation of Subsidiary Booksgagan15095895100% (1)

- Account Statement From 1 Feb 2021 To 30 Apr 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument11 pagesAccount Statement From 1 Feb 2021 To 30 Apr 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceUday AbhiNo ratings yet

- 5s LearningDocument35 pages5s LearningAnkur100% (1)

- SAP125 SAP Navigation 2005: SAP SCM-Procurement (MM) Academy ECC 6.0Document9 pagesSAP125 SAP Navigation 2005: SAP SCM-Procurement (MM) Academy ECC 6.0kngane8878No ratings yet

- The Impact of Globalizationon International BusinessDocument12 pagesThe Impact of Globalizationon International Businessmoza50% (2)

- i-ROOMZ Nakshatra-LRDocument1 pagei-ROOMZ Nakshatra-LRsharadNo ratings yet

- Case1 1Document3 pagesCase1 1rgovindan123No ratings yet

- TIEP Application TemplatesDocument6 pagesTIEP Application TemplatesactivatedcarbonsolutionsNo ratings yet

- Stst3002 Op EdDocument3 pagesStst3002 Op EdEmma ChenNo ratings yet

- PCI Case Study Maf680Document23 pagesPCI Case Study Maf680Nur Ifa100% (26)

- Project Assignment: Scope Purpose Covered inDocument6 pagesProject Assignment: Scope Purpose Covered inapplefieldNo ratings yet

- De Los Santos V NLRCDocument2 pagesDe Los Santos V NLRCPBWGNo ratings yet

- Rainbow CatalougeDocument5 pagesRainbow Catalougeapi-257794235No ratings yet

- ClayCraft 09 2017Document84 pagesClayCraft 09 2017OksanaNo ratings yet

- KIA India Dealer Application FormDocument22 pagesKIA India Dealer Application FormAditya BhalotiaNo ratings yet

- Voucher & Other FormsDocument30 pagesVoucher & Other FormsLeonorBagnisonNo ratings yet

- Briefings - LiatDocument2 pagesBriefings - Liatapi-252471713No ratings yet

- Audit Non Conformance ReportDocument4 pagesAudit Non Conformance Reportbudi_alamsyah100% (2)

- Budget and Budgetary ControlDocument14 pagesBudget and Budgetary ControlPassmore DubeNo ratings yet

- Asia Pacific Shopping Center Definition Standard Proposal PDFDocument18 pagesAsia Pacific Shopping Center Definition Standard Proposal PDFwitanti nur utamiNo ratings yet

- TSPA Scheme RKSV PDFDocument2 pagesTSPA Scheme RKSV PDFKolla Srikanth100% (1)

- EX PARTE APPLICATION FEDERAL COURT NATIONSTAR MORTGAGE LLC (Billy Earley)Document25 pagesEX PARTE APPLICATION FEDERAL COURT NATIONSTAR MORTGAGE LLC (Billy Earley)Billy EarleyNo ratings yet

- Law On Business Organizations ReviewerDocument51 pagesLaw On Business Organizations ReviewerAriana Regio100% (2)

- BURGER KING Case Analysis Final PDFDocument26 pagesBURGER KING Case Analysis Final PDFdigantrayNo ratings yet

- 1 GTAG Assessing Cybersecurity RiskDocument31 pages1 GTAG Assessing Cybersecurity RiskWrafael Garcia100% (3)

- JIMS International Conference Paper Sequence Details - Top Management Institute in India Delhi NCR Management International Events Seminars ConferencesDocument11 pagesJIMS International Conference Paper Sequence Details - Top Management Institute in India Delhi NCR Management International Events Seminars ConferencesJagan Institute of Management StudiesNo ratings yet

- MERS Southeast Legal Seminar (11.10.04) FinalDocument26 pagesMERS Southeast Legal Seminar (11.10.04) FinalgregmanuelNo ratings yet

Download as pptx, pdf, or txt

You might also like

- Factors That Affect Reference Group InfluenceDocument3 pagesFactors That Affect Reference Group Influencegagan1509589571% (7)

- Chap 018Document27 pagesChap 018Xeniya Morozova Kurmayeva100% (3)

- Consulting Casebook 2019Document135 pagesConsulting Casebook 2019Hari Chandana100% (1)

- Airtel Service BlueprintDocument56 pagesAirtel Service BlueprintManish Gupta50% (2)

- Media Planning and Buying: Notes and PPT by Prof - Chahat HargunaniDocument35 pagesMedia Planning and Buying: Notes and PPT by Prof - Chahat HargunaniHarsha Bulani Chahat Hargunani100% (1)

- Betterment Demographics ReportDocument6 pagesBetterment Demographics ReportConnor LeeNo ratings yet

- R12.x Oracle Enterprise Asset Management FundamentalsDocument4 pagesR12.x Oracle Enterprise Asset Management FundamentalsSundar Kumar Vasantha GovindarajuluNo ratings yet

- PORTER 5 ForcesDocument4 pagesPORTER 5 ForcesMiley MartinNo ratings yet

- Telecom Sector Porter's 5 Force AnalysisDocument3 pagesTelecom Sector Porter's 5 Force AnalysisKARTIK ANAND100% (1)

- Airtel Strategic ManagementDocument29 pagesAirtel Strategic ManagementSandeep George80% (5)

- Report - Contemporary IssuesDocument5 pagesReport - Contemporary IssuesNiha SayyadNo ratings yet

- FinalyticsDocument3 pagesFinalyticschakshu chawlaNo ratings yet

- Strategic Audit of BSNLDocument42 pagesStrategic Audit of BSNLNishant Ahuja0% (1)

- Analysis of Vodafone Essar IndiaDocument34 pagesAnalysis of Vodafone Essar Indiachapal07No ratings yet

- Strategic Audit of BSNLDocument42 pagesStrategic Audit of BSNLNishant AhujaNo ratings yet

- Marketing Environment of AirtelDocument7 pagesMarketing Environment of AirtelTakauv-thiyagi Thiyagu0% (1)

- Porter's Five Forces Model: 1. Threat of New Entrants - LowDocument2 pagesPorter's Five Forces Model: 1. Threat of New Entrants - Low138PATEL KHYATIMMSBNo ratings yet

- Bharti Value Chain AnalysisDocument3 pagesBharti Value Chain AnalysisAnkit Bansal0% (1)

- 6 Meera Arora 1730 Review Article VSRDIJBMR April 2013 PDFDocument8 pages6 Meera Arora 1730 Review Article VSRDIJBMR April 2013 PDFAru BhartiNo ratings yet

- Group B AirtelDocument29 pagesGroup B AirtelPranitha_Shett_7109No ratings yet

- Kinny Jain Nikhil Saraf Dionysiamichalopoulou Rajinder Pal SinghDocument39 pagesKinny Jain Nikhil Saraf Dionysiamichalopoulou Rajinder Pal SinghKanchan VardhaniNo ratings yet

- SWOT Analysis On Jio: StrengthDocument3 pagesSWOT Analysis On Jio: StrengthAmal Raj SinghNo ratings yet

- SWOT JioDocument3 pagesSWOT JioAmal Raj SinghNo ratings yet

- AirtelDocument31 pagesAirtelRajiv KeshriNo ratings yet

- Advertising Effectiveness On Telecom Ind - ProjectDocument51 pagesAdvertising Effectiveness On Telecom Ind - Projecttina_18No ratings yet

- Report On Industry, Competitive, SPACE Matrix Analysis For Telecom Industry - TATA Tele Services, Bharti AirtelDocument18 pagesReport On Industry, Competitive, SPACE Matrix Analysis For Telecom Industry - TATA Tele Services, Bharti AirtelankitsuroliaNo ratings yet

- AirtelDocument19 pagesAirtelSabyasachi DebNo ratings yet

- Business Strategy Assignment - Final TelecomDocument10 pagesBusiness Strategy Assignment - Final TelecomAishwarya SankhlaNo ratings yet

- Airtel 1Document39 pagesAirtel 1Sameer AggarwalNo ratings yet

- What Is An IndustryDocument8 pagesWhat Is An IndustrypritamNo ratings yet

- Project AIRTELDocument58 pagesProject AIRTELSonal LuthraNo ratings yet

- Customer Satisfaction: Summer Project Report ONDocument75 pagesCustomer Satisfaction: Summer Project Report ONManjeet SinghNo ratings yet

- Comparison Between Two Brands Airtel Vs HutchDocument8 pagesComparison Between Two Brands Airtel Vs HutchAdithya Anuroop SridharanNo ratings yet

- Kinny Jain Nikhil Saraf Dionysiamichalopoulou Rajinder Pal SinghDocument39 pagesKinny Jain Nikhil Saraf Dionysiamichalopoulou Rajinder Pal SinghPrashant KumarNo ratings yet

- Final ReportDocument51 pagesFinal ReportNaveen Kumar VenigallaNo ratings yet

- Bharti Airtel PresentationDocument32 pagesBharti Airtel PresentationNaina ChetwaniNo ratings yet

- Idea Cellular StrategyDocument34 pagesIdea Cellular Strategysdrkmau50% (2)

- Swot Analysis of Bharti Airtel Mobile ServicesDocument6 pagesSwot Analysis of Bharti Airtel Mobile ServicesAnusree RavikumarNo ratings yet

- Airtel - Targeting High Paying Customers and Foreign Partners To Offset Declining Revenues and Market ShareDocument16 pagesAirtel - Targeting High Paying Customers and Foreign Partners To Offset Declining Revenues and Market ShareNikhil KumarNo ratings yet

- Company IdeaDocument8 pagesCompany IdeaishanNo ratings yet

- Indian Telecom Industry-Porter's 5 Force Model: by - Sukanya Roy Chowdhury & Abhirup Roy ChoudhuryDocument41 pagesIndian Telecom Industry-Porter's 5 Force Model: by - Sukanya Roy Chowdhury & Abhirup Roy Choudhurysuku1983No ratings yet

- Assingment On Stratergic Management: Submitted By: Sampada KarpateDocument15 pagesAssingment On Stratergic Management: Submitted By: Sampada Karpateashish chaturvediNo ratings yet

- StartgyDocument7 pagesStartgyshafeeqaliNo ratings yet

- SWOT ANALYSIS Chapter SixDocument8 pagesSWOT ANALYSIS Chapter SixSetu MehtaNo ratings yet

- Analysis of Vodafone Essar IndiaDocument34 pagesAnalysis of Vodafone Essar IndiaSantosh SamNo ratings yet

- Porter Five Forces WordDocument11 pagesPorter Five Forces WordvinodvahoraNo ratings yet

- BHARTI AIRTEL Suvendu & NitinDocument3 pagesBHARTI AIRTEL Suvendu & Nitinsuvendu08No ratings yet

- Study of Competitive Rivalry in Indian Telecom SectorDocument18 pagesStudy of Competitive Rivalry in Indian Telecom Sectorarnabnitw100% (1)

- Can The Telecom Industry Welcome The New Entrants? Ms. Ambika Rathi, Mr. Rajesh VermaDocument8 pagesCan The Telecom Industry Welcome The New Entrants? Ms. Ambika Rathi, Mr. Rajesh VermaPijush Kanti DolaiNo ratings yet

- Vodafone-Brand ManagementDocument63 pagesVodafone-Brand ManagementKuntal PanjaNo ratings yet

- Merger and AcquisitionDocument5 pagesMerger and AcquisitionShilpiNo ratings yet

- Objective of The Study: Literature ReviewDocument15 pagesObjective of The Study: Literature ReviewAanchal PatnahaNo ratings yet

- AIRTELDocument104 pagesAIRTELNazuk Batra100% (1)

- CFM - Bharti AirtelDocument12 pagesCFM - Bharti Airtel202022030 imtnagNo ratings yet

- Report On Airtel Market Analysis: AcknowledgementDocument13 pagesReport On Airtel Market Analysis: AcknowledgementGIRIJANo ratings yet

- Report On Brand Image of Nokia MobileDocument14 pagesReport On Brand Image of Nokia MobileMuhammed MusthafaNo ratings yet

- Security Analysis AssignmentDocument14 pagesSecurity Analysis AssignmentShivam V PunyaniNo ratings yet

- Alhad 504-AirtelDocument11 pagesAlhad 504-AirtelAlhad PosamNo ratings yet

- Cellular Technologies for Emerging Markets: 2G, 3G and BeyondFrom EverandCellular Technologies for Emerging Markets: 2G, 3G and BeyondNo ratings yet

- Papers on the field: Telecommunication Economic, Business, Regulation & PolicyFrom EverandPapers on the field: Telecommunication Economic, Business, Regulation & PolicyNo ratings yet

- An Introduction to SDN Intent Based NetworkingFrom EverandAn Introduction to SDN Intent Based NetworkingRating: 5 out of 5 stars5/5 (1)

- A Skill Based Pay SystemDocument12 pagesA Skill Based Pay Systemgagan15095895No ratings yet

- Carf Paper 2 - Hedging Currency Risk in International Investment and TradeDocument26 pagesCarf Paper 2 - Hedging Currency Risk in International Investment and Tradebalasurya4321No ratings yet

- Chap 019Document9 pagesChap 019gagan15095895No ratings yet

- Vision & Mission StatementDocument1 pageVision & Mission Statementgagan15095895No ratings yet

- Institutional Infrastructure For Export PromotionDocument68 pagesInstitutional Infrastructure For Export Promotiongagan1509589580% (5)

- New QuessinnaireDocument4 pagesNew Quessinnairegagan15095895No ratings yet

- Basic Facts About JammuDocument7 pagesBasic Facts About Jammugagan15095895No ratings yet

- Case Study of CresentDocument3 pagesCase Study of Cresentgagan15095895No ratings yet

- DGFTDocument35 pagesDGFTgagan15095895No ratings yet

- Kandla SezDocument5 pagesKandla Sezgagan15095895No ratings yet

- Competitor Brand Analysis of Nirma DetergentDocument31 pagesCompetitor Brand Analysis of Nirma Detergentgagan15095895100% (1)

- Classical Encryption Techniques: Symmetric Ciphers (Class-L4 & L5)Document13 pagesClassical Encryption Techniques: Symmetric Ciphers (Class-L4 & L5)gagan15095895No ratings yet

- Presentation of Subsidiary BooksDocument37 pagesPresentation of Subsidiary Booksgagan15095895100% (1)

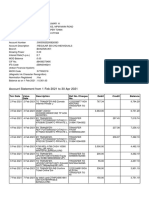

- Account Statement From 1 Feb 2021 To 30 Apr 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument11 pagesAccount Statement From 1 Feb 2021 To 30 Apr 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceUday AbhiNo ratings yet

- 5s LearningDocument35 pages5s LearningAnkur100% (1)

- SAP125 SAP Navigation 2005: SAP SCM-Procurement (MM) Academy ECC 6.0Document9 pagesSAP125 SAP Navigation 2005: SAP SCM-Procurement (MM) Academy ECC 6.0kngane8878No ratings yet

- The Impact of Globalizationon International BusinessDocument12 pagesThe Impact of Globalizationon International Businessmoza50% (2)

- i-ROOMZ Nakshatra-LRDocument1 pagei-ROOMZ Nakshatra-LRsharadNo ratings yet

- Case1 1Document3 pagesCase1 1rgovindan123No ratings yet

- TIEP Application TemplatesDocument6 pagesTIEP Application TemplatesactivatedcarbonsolutionsNo ratings yet

- Stst3002 Op EdDocument3 pagesStst3002 Op EdEmma ChenNo ratings yet

- PCI Case Study Maf680Document23 pagesPCI Case Study Maf680Nur Ifa100% (26)

- Project Assignment: Scope Purpose Covered inDocument6 pagesProject Assignment: Scope Purpose Covered inapplefieldNo ratings yet

- De Los Santos V NLRCDocument2 pagesDe Los Santos V NLRCPBWGNo ratings yet

- Rainbow CatalougeDocument5 pagesRainbow Catalougeapi-257794235No ratings yet

- ClayCraft 09 2017Document84 pagesClayCraft 09 2017OksanaNo ratings yet

- KIA India Dealer Application FormDocument22 pagesKIA India Dealer Application FormAditya BhalotiaNo ratings yet

- Voucher & Other FormsDocument30 pagesVoucher & Other FormsLeonorBagnisonNo ratings yet

- Briefings - LiatDocument2 pagesBriefings - Liatapi-252471713No ratings yet

- Audit Non Conformance ReportDocument4 pagesAudit Non Conformance Reportbudi_alamsyah100% (2)

- Budget and Budgetary ControlDocument14 pagesBudget and Budgetary ControlPassmore DubeNo ratings yet

- Asia Pacific Shopping Center Definition Standard Proposal PDFDocument18 pagesAsia Pacific Shopping Center Definition Standard Proposal PDFwitanti nur utamiNo ratings yet

- TSPA Scheme RKSV PDFDocument2 pagesTSPA Scheme RKSV PDFKolla Srikanth100% (1)

- EX PARTE APPLICATION FEDERAL COURT NATIONSTAR MORTGAGE LLC (Billy Earley)Document25 pagesEX PARTE APPLICATION FEDERAL COURT NATIONSTAR MORTGAGE LLC (Billy Earley)Billy EarleyNo ratings yet

- Law On Business Organizations ReviewerDocument51 pagesLaw On Business Organizations ReviewerAriana Regio100% (2)

- BURGER KING Case Analysis Final PDFDocument26 pagesBURGER KING Case Analysis Final PDFdigantrayNo ratings yet

- 1 GTAG Assessing Cybersecurity RiskDocument31 pages1 GTAG Assessing Cybersecurity RiskWrafael Garcia100% (3)

- JIMS International Conference Paper Sequence Details - Top Management Institute in India Delhi NCR Management International Events Seminars ConferencesDocument11 pagesJIMS International Conference Paper Sequence Details - Top Management Institute in India Delhi NCR Management International Events Seminars ConferencesJagan Institute of Management StudiesNo ratings yet

- MERS Southeast Legal Seminar (11.10.04) FinalDocument26 pagesMERS Southeast Legal Seminar (11.10.04) FinalgregmanuelNo ratings yet