Download as pptx, pdf, or txt

You might also like

- ACT Invoice DecDocument2 pagesACT Invoice DecNikhil Gupta0% (1)

- Analyzing The Distribution Channel of GCPLDocument12 pagesAnalyzing The Distribution Channel of GCPLNikhil Gupta100% (3)

- 5th Module FMDocument16 pages5th Module FMAbhishek SarafNo ratings yet

- Underlying MarketsDocument30 pagesUnderlying MarketsDhairyaa BhardwajNo ratings yet

- Derivatives Market: By-Ambika GargDocument17 pagesDerivatives Market: By-Ambika GargRahul MauryaNo ratings yet

- Unit 1 Syllabus: Introduction To Derivatives: ForwardsDocument24 pagesUnit 1 Syllabus: Introduction To Derivatives: ForwardsSHANTAM KEDIANo ratings yet

- Presentation On Underlying Market: BY:-DHAIRYA (03) KANIKA (47) DARSHANDocument30 pagesPresentation On Underlying Market: BY:-DHAIRYA (03) KANIKA (47) DARSHANDhairyaa BhardwajNo ratings yet

- Chapter 8 - Markets For Foreign ExchangeDocument30 pagesChapter 8 - Markets For Foreign Exchangesiobhan margaretNo ratings yet

- Foreign Exchange Market & Structure - IntroductionDocument38 pagesForeign Exchange Market & Structure - IntroductionVaidyanathan RavichandranNo ratings yet

- Derivativesmarket 111dfsaf006143752 Phpapp02Document17 pagesDerivativesmarket 111dfsaf006143752 Phpapp02Aman TyagiNo ratings yet

- MMS Derivatives Lec 1Document85 pagesMMS Derivatives Lec 1AzharNo ratings yet

- Research On Uses of Derivative in Pakistan by SaifullahDocument35 pagesResearch On Uses of Derivative in Pakistan by SaifullahMian Saifullah50% (2)

- Structure of Forwards Future MarketsDocument23 pagesStructure of Forwards Future MarketsRahimullah QaziNo ratings yet

- BFN 427 Business Scenarios Using Swaps, Options and FuturesDocument68 pagesBFN 427 Business Scenarios Using Swaps, Options and FuturesgeorgeNo ratings yet

- Chapter-2_6Document42 pagesChapter-2_6Linh LêNo ratings yet

- Futures - Introduction: Ravi - IBADocument38 pagesFutures - Introduction: Ravi - IBAVaidyanathan RavichandranNo ratings yet

- Commodities ExchangeDocument59 pagesCommodities ExchangesherazhassannNo ratings yet

- Financial Derivatives and Risk ManagementDocument6 pagesFinancial Derivatives and Risk Managementstriker shakeNo ratings yet

- Angel Broking's Suite of Products & Services: 1. EquityDocument9 pagesAngel Broking's Suite of Products & Services: 1. Equityrk_sharktalb214322No ratings yet

- Icici Securities Project ReportDocument22 pagesIcici Securities Project ReportbruhNo ratings yet

- Over-The-Counter (Finance) : OTC-traded StocksDocument6 pagesOver-The-Counter (Finance) : OTC-traded StocksRohan ShettyNo ratings yet

- If 4Document79 pagesIf 4Aalfin MariyaNo ratings yet

- Introduction To DerivativesDocument23 pagesIntroduction To DerivativesVaidyanathan RavichandranNo ratings yet

- RSMDocument10 pagesRSMregan165No ratings yet

- Derivative 1Document39 pagesDerivative 1Heera JhaNo ratings yet

- Session -3 Forex MarketDocument122 pagesSession -3 Forex MarketHaritika ChhatwalNo ratings yet

- Short Explanation of The Important Topics in Bbs 4 Year Prepared by Sijan Raj JoshiDocument64 pagesShort Explanation of The Important Topics in Bbs 4 Year Prepared by Sijan Raj JoshiSijan Raj JoshiNo ratings yet

- How To Invest in CommoditiesDocument8 pagesHow To Invest in CommoditiesAikoDesuNo ratings yet

- Derivativesmarket 111006143752 Phpapp02Document21 pagesDerivativesmarket 111006143752 Phpapp02sejalahir30_40759023No ratings yet

- Options, Futures, and Othe R Derivatives: Chapter 1 IntroductionDocument32 pagesOptions, Futures, and Othe R Derivatives: Chapter 1 IntroductionBasappaSarkarNo ratings yet

- Session 1 RISK MANAGEMENT & DERIVATIVES MARKETSDocument43 pagesSession 1 RISK MANAGEMENT & DERIVATIVES MARKETSAkash MithauliaNo ratings yet

- Hamutyinei Harvey Pamburai RM 4.67 Leslie Social Science BuildingDocument30 pagesHamutyinei Harvey Pamburai RM 4.67 Leslie Social Science BuildingMbusoThabetheNo ratings yet

- What Is A Derivative?Document36 pagesWhat Is A Derivative?Mahesh ShahNo ratings yet

- DerivativesDocument41 pagesDerivativesmugdha.ghag3921No ratings yet

- Derivatives SYBBI - PPTX FinalDocument70 pagesDerivatives SYBBI - PPTX Finalsmit mestryNo ratings yet

- RMT Lecture NotesDocument13 pagesRMT Lecture NotesAbid100% (1)

- Chapter 1: Introduction To DerivativesDocument11 pagesChapter 1: Introduction To DerivativesDimithri De MeraalNo ratings yet

- CSC Summary IDocument38 pagesCSC Summary IWendy Shi0% (1)

- Currency Futures Market in India: at India Info Line LTD, HyderabadDocument19 pagesCurrency Futures Market in India: at India Info Line LTD, HyderabadSubodh KothariNo ratings yet

- FuturesDocument117 pagesFuturesLekha GuptaNo ratings yet

- S2 - Financial Markets-UnlockedDocument31 pagesS2 - Financial Markets-UnlockedAYUSHI NAGARNo ratings yet

- Derivatives MKTDocument65 pagesDerivatives MKTMahesh DupareNo ratings yet

- Managing Steel Price RiskDocument106 pagesManaging Steel Price RiskNoemi J Campa RoblesNo ratings yet

- Bonds and DerivativesDocument149 pagesBonds and DerivativesLinh LinhNo ratings yet

- Futures and OptionsDocument51 pagesFutures and OptionsRitik VermaniNo ratings yet

- Lecture 1 - Foreign Exchange MarketDocument64 pagesLecture 1 - Foreign Exchange MarkettcmathewwongNo ratings yet

- Intro FDRMDocument35 pagesIntro FDRMRupayan DuttaNo ratings yet

- DerivativesDocument10 pagesDerivativesSalman MSDNo ratings yet

- Derivatives V 2Document57 pagesDerivatives V 2Pooja BansalNo ratings yet

- Fundamental Series IDocument35 pagesFundamental Series ILal DhwojNo ratings yet

- What Is A "Derivative"?Document15 pagesWhat Is A "Derivative"?mohammad ahmadNo ratings yet

- What's An Index?Document23 pagesWhat's An Index?deepani_446621No ratings yet

- Stock Exchange MechanismDocument24 pagesStock Exchange MechanismSandeep Sandeep SinghNo ratings yet

- The Bond MarketDocument11 pagesThe Bond Marketborn2growNo ratings yet

- Energy TradeDocument48 pagesEnergy TradeNaina Singh AdarshNo ratings yet

- Infinox CorporateDocument17 pagesInfinox CorporateRonald FriasNo ratings yet

- Derivative+Market - Recent Trends ND Development, Future .Document25 pagesDerivative+Market - Recent Trends ND Development, Future .KARISHMAAT86% (7)

- Chapter 1 DerivativesDocument6 pagesChapter 1 DerivativesalanoudNo ratings yet

- Derivatives 1 2021Document71 pagesDerivatives 1 2021Gragnor Pride100% (1)

- CH 1Document32 pagesCH 1华邦盛No ratings yet

- đề cương Inter.I - 161022Document10 pagesđề cương Inter.I - 161022Huyền DuyênNo ratings yet

- Moving US White Collar Jobs OffshoreDocument8 pagesMoving US White Collar Jobs OffshoreNikhil GuptaNo ratings yet

- Brand Equity ArticleDocument5 pagesBrand Equity ArticleNikhil GuptaNo ratings yet

- Summary BRM PidiliteDocument2 pagesSummary BRM PidiliteNikhil GuptaNo ratings yet

- Measuring Brand EquityDocument33 pagesMeasuring Brand EquityNikhil GuptaNo ratings yet

- Industrial Chemical Inc. - Pigment DivisionDocument6 pagesIndustrial Chemical Inc. - Pigment DivisionNikhil GuptaNo ratings yet

- Industrial Chemical Inc. - Pigment DivisionDocument6 pagesIndustrial Chemical Inc. - Pigment DivisionNikhil GuptaNo ratings yet

- Mattel Toys India LTDDocument6 pagesMattel Toys India LTDNikhil GuptaNo ratings yet

- Titman CH 16 - Dividend PolicyDocument55 pagesTitman CH 16 - Dividend PolicyIKA RAHMAWATINo ratings yet

- Robotti Securities, LLC: Partnering With Buy-and-Hold InvestorsDocument6 pagesRobotti Securities, LLC: Partnering With Buy-and-Hold InvestorsMatt EbrahimiNo ratings yet

- NSDL NotesDocument14 pagesNSDL NotesAnmol RahangdaleNo ratings yet

- 6c656pms & Esop NewDocument24 pages6c656pms & Esop NewSasanka YalamanchiliNo ratings yet

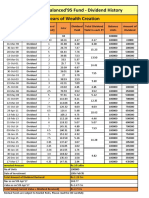

- Dividend HistoryDocument1 pageDividend HistoryJeetendra KumarNo ratings yet

- Stocks and Shares Case of StudyDocument4 pagesStocks and Shares Case of StudyBrayan Manuel Cabrera DuvergeNo ratings yet

- Chartering and OperationDocument35 pagesChartering and Operationmarines0587% (15)

- 12 Business Studies CH 10 Financial MarkeetsDocument10 pages12 Business Studies CH 10 Financial MarkeetsVikky GuptaNo ratings yet

- Chapter 2. Model For Financial Statements, Cash Flows, and TaxesDocument3 pagesChapter 2. Model For Financial Statements, Cash Flows, and TaxesNaser Fayyaz KhawajaNo ratings yet

- 6.lecture 6 - Basic Option StrategiesDocument33 pages6.lecture 6 - Basic Option StrategiesKasidit AsavakittikawinNo ratings yet

- Indigo Paints LimitedDocument402 pagesIndigo Paints LimitedSuresh Kumar DevanathanNo ratings yet

- B7110-001 Financial Statement Analysis and Valuation PDFDocument3 pagesB7110-001 Financial Statement Analysis and Valuation PDFLittleBlondie0% (2)

- Ascending Triangle: Trade SetupDocument1 pageAscending Triangle: Trade SetupamithrNo ratings yet

- Open InterestDocument9 pagesOpen InterestAmbikesh ChauhanNo ratings yet

- Eps Ias 33Document5 pagesEps Ias 33Yasir Iftikhar AbbasiNo ratings yet

- Trends in Stock MarketDocument28 pagesTrends in Stock MarketHarshraj ShahNo ratings yet

- Merchant Banker PerformanceDocument18 pagesMerchant Banker PerformanceMilin RaijadaNo ratings yet

- Mutual Funds Question Paper 2Document9 pagesMutual Funds Question Paper 2studysks2324No ratings yet

- The Wolf of Wall StreetDocument2 pagesThe Wolf of Wall StreetAbigail Cruz ParaanNo ratings yet

- Futures Trading GuideDocument16 pagesFutures Trading GuideTan Chung KenNo ratings yet

- Assignment On BaringsDocument10 pagesAssignment On Baringsimtehan_chowdhuryNo ratings yet

- Comparative Analysis of Investment AvenuesDocument68 pagesComparative Analysis of Investment Avenueskritika kapoor71% (17)

- GanncalculatorDocument2 pagesGanncalculatorhthinaNo ratings yet

- Implied Volatility Formula of European Power Option Pricing: ( ) RespectivelyDocument8 pagesImplied Volatility Formula of European Power Option Pricing: ( ) RespectivelyAdnan KamalNo ratings yet

- Unit-5 3 Put-Call Parity PrincipleDocument18 pagesUnit-5 3 Put-Call Parity PrincipleJack SparrowNo ratings yet

- Investor Presentation (Company Update)Document34 pagesInvestor Presentation (Company Update)Shyam SunderNo ratings yet

- Central Depository Services01Document11 pagesCentral Depository Services01Rajendra SwarnakarNo ratings yet

- Venture Hacks Twitter BibleDocument244 pagesVenture Hacks Twitter BibleniviNo ratings yet