Download as ppt, pdf, or txt

You might also like

- EpiPen Stakeholder AnalysisDocument11 pagesEpiPen Stakeholder Analysis吴茗No ratings yet

- Using Excel As A DSS: Don't Use Cell Reference Such As +E13-E19 Unless It Is NecessaryDocument3 pagesUsing Excel As A DSS: Don't Use Cell Reference Such As +E13-E19 Unless It Is NecessaryHà LêNo ratings yet

- Strengths in The SWOT Analysis of IndigoDocument2 pagesStrengths in The SWOT Analysis of IndigoJyoti joshiNo ratings yet

- Binomial TreesDocument25 pagesBinomial TreesJayash KaushalNo ratings yet

- Introduction To Binomial TreesDocument25 pagesIntroduction To Binomial Treesyty etytrfNo ratings yet

- Session 9Document29 pagesSession 9Ramesh PowarNo ratings yet

- Introduction To Binomial TreesDocument22 pagesIntroduction To Binomial Treesshashikant74No ratings yet

- Chapter 6 Option Pricing 2022 SDocument32 pagesChapter 6 Option Pricing 2022 SĐức Nam TrầnNo ratings yet

- Chapter 6 - Option Pricing - 2022 - SDocument32 pagesChapter 6 - Option Pricing - 2022 - SNgoc Anh LeNo ratings yet

- 7 Introduction To Binomial TreesDocument25 pages7 Introduction To Binomial TreesDragosCavescuNo ratings yet

- CH 12 Hull Fundamentals 8 The DDocument25 pagesCH 12 Hull Fundamentals 8 The DjlosamNo ratings yet

- BinomialDocument22 pagesBinomialSonam Gupta SarafNo ratings yet

- FM2 NumericalsDocument38 pagesFM2 NumericalsKamalakar ReddyNo ratings yet

- Binomial TreeDocument22 pagesBinomial TreeXavier Francis S. LutaloNo ratings yet

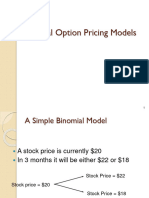

- A Simple Binomial Model: - A Stock Price Is Currently $20 - in Three Months It Will Be Either $22 or $18Document55 pagesA Simple Binomial Model: - A Stock Price Is Currently $20 - in Three Months It Will Be Either $22 or $18nasrullohNo ratings yet

- Black Scholes PDEDocument7 pagesBlack Scholes PDEmeleeisleNo ratings yet

- EC3314 Spring Lecture 9Document36 pagesEC3314 Spring Lecture 9christina0107No ratings yet

- Lecture 22Document40 pagesLecture 22Rita ChetwaniNo ratings yet

- RSM435 - Question 4Document16 pagesRSM435 - Question 4Oscar ChenNo ratings yet

- Option ValuationsDocument29 pagesOption ValuationsArham Kumar JainBD21064No ratings yet

- Put-Call Parity: - Put Option Value Can Be Computed Using Put-Call Parity Fiduciary Call Protective PutDocument30 pagesPut-Call Parity: - Put Option Value Can Be Computed Using Put-Call Parity Fiduciary Call Protective PutARYA SHETHNo ratings yet

- Binomial Option Pricing ModelDocument12 pagesBinomial Option Pricing Modelmiku hrshNo ratings yet

- Binomial Trees: Liuren WuDocument22 pagesBinomial Trees: Liuren WufpttmmNo ratings yet

- Black-Scholes Option Pricing AssigmentDocument3 pagesBlack-Scholes Option Pricing AssigmentInformation should be FREENo ratings yet

- InvestmentsHull2022 05Document21 pagesInvestmentsHull2022 05Barna OsztermayerNo ratings yet

- Modification of Black-Scholes Model: 7.1 DividendDocument9 pagesModification of Black-Scholes Model: 7.1 Dividendcharles luisNo ratings yet

- Pricingoptions by BlackscholesDocument98 pagesPricingoptions by BlackscholesNitish TanwarNo ratings yet

- Financial EngineeringDocument38 pagesFinancial EngineeringKubi lemmaNo ratings yet

- Chapter 13 - The Black-Scholes-Merton ModelDocument28 pagesChapter 13 - The Black-Scholes-Merton ModelJean Pierre NaamanNo ratings yet

- MathFin L2Document13 pagesMathFin L2fwm949fwxrNo ratings yet

- The Black-Scholes ModelDocument42 pagesThe Black-Scholes Modelnaviprasadthebond9532No ratings yet

- Final PPT IE612 - Financial EngineeringDocument16 pagesFinal PPT IE612 - Financial EngineeringHey BuddyNo ratings yet

- Option Valuation ModelsDocument97 pagesOption Valuation ModelsParitoshNo ratings yet

- FinMath Lecture 7 Black-ScholesDocument30 pagesFinMath Lecture 7 Black-ScholesavirgNo ratings yet

- Black Scholes ValuationDocument3 pagesBlack Scholes ValuationVivek SinghNo ratings yet

- BRIGHAM CH 19 SM 3ce - REVISEDDocument11 pagesBRIGHAM CH 19 SM 3ce - REVISEDVu Khanh LeNo ratings yet

- Risk and ReturnDocument166 pagesRisk and ReturnShailendra ShresthaNo ratings yet

- Ch07 ShowDocument57 pagesCh07 ShowBagus ZijlstraNo ratings yet

- Common Stock Valuation Some Features of Common and Preferred Stocks The Stock MarketsDocument16 pagesCommon Stock Valuation Some Features of Common and Preferred Stocks The Stock MarketsgelskNo ratings yet

- The Black-Scholes-Merton Model: Options, Futures, and Other Derivatives, 8th Edition, 1Document31 pagesThe Black-Scholes-Merton Model: Options, Futures, and Other Derivatives, 8th Edition, 1Manish Pushkar100% (1)

- BSM and BinominalDocument72 pagesBSM and BinominalANISH NARANGNo ratings yet

- DM9 CirculationDocument60 pagesDM9 CirculationNaman JainNo ratings yet

- MGMT 41150 - Chapter 13 - Binomial TreesDocument41 pagesMGMT 41150 - Chapter 13 - Binomial TreesLaxus DreyerNo ratings yet

- Real Options: Options, Futures, Derivatives / April 30, 2008 1Document27 pagesReal Options: Options, Futures, Derivatives / April 30, 2008 1Sarita SharmaNo ratings yet

- Complete Binomial Models - 張森林教授講稿Document111 pagesComplete Binomial Models - 張森林教授講稿abin465No ratings yet

- Problema 9 e 10Document8 pagesProblema 9 e 10pedrohminettoNo ratings yet

- Forward and Future Pricing 2 FinalDocument24 pagesForward and Future Pricing 2 FinalRahul Singh100% (1)

- Slides - Lecture9Document15 pagesSlides - Lecture9Mohanad DahlanNo ratings yet

- SOA MFE 76 Practice Ques SolsDocument70 pagesSOA MFE 76 Practice Ques SolsGracia DongNo ratings yet

- Binomial Option Pricing ModelDocument27 pagesBinomial Option Pricing ModelParthapratim Debnath50% (2)

- COMP 7570 - Computational Finance 12.7 Matching Volatility With U and DDocument8 pagesCOMP 7570 - Computational Finance 12.7 Matching Volatility With U and DAvardeep SinghNo ratings yet

- Final Assignment: 42106 Financial Risk ManagementDocument35 pagesFinal Assignment: 42106 Financial Risk ManagementJonatan BordingNo ratings yet

- 3962852Document60 pages3962852Ashley Ibe GuevarraNo ratings yet

- Stocks and Their Valuation: Taufikur@ugm - Ac.idDocument43 pagesStocks and Their Valuation: Taufikur@ugm - Ac.idNeneng Wulandari100% (1)

- Financial Derivatives: Section 5Document38 pagesFinancial Derivatives: Section 5palpakratwr9030No ratings yet

- Chapter 23 - Ç Æ¡Document14 pagesChapter 23 - Ç Æ¡張閔華No ratings yet

- Multi-Asset Options: 4.1 Pricing ModelDocument10 pagesMulti-Asset Options: 4.1 Pricing ModeldownloadfromscribdNo ratings yet

- Valuation of EquityDocument40 pagesValuation of EquityPRIYA KUMARINo ratings yet

- ECO4108Z Futures, Options, DerivativesDocument4 pagesECO4108Z Futures, Options, DerivativesnondweNo ratings yet

- CH 22Document68 pagesCH 22Aireen TanioNo ratings yet

- Valuation of Bond and StockDocument12 pagesValuation of Bond and StockShovan ChowdhuryNo ratings yet

- Probability Measures in Financial MathematicsDocument3 pagesProbability Measures in Financial MathematicsDudenNo ratings yet

- Module 9Document32 pagesModule 9Precious GiftsNo ratings yet

- Cost Audit ReportDocument20 pagesCost Audit ReportVishesh DwivediNo ratings yet

- Inbound 3494381804797819186Document17 pagesInbound 3494381804797819186Dương Huệ NhiNo ratings yet

- PWC Resolving Capital Project DisputesDocument24 pagesPWC Resolving Capital Project DisputesHein Zin HanNo ratings yet

- Passenger Details: Pdfiop Con RmedDocument3 pagesPassenger Details: Pdfiop Con RmedGray Japeth GelbolingoNo ratings yet

- Performance Evaluation For Decentralized OperationsDocument46 pagesPerformance Evaluation For Decentralized Operationswarsima100% (1)

- 4.1 - 4.5 Government Intervention HL RSDocument18 pages4.1 - 4.5 Government Intervention HL RSSyed HaroonNo ratings yet

- Complete Guide To Value InvestingDocument59 pagesComplete Guide To Value InvestingPaulo TrickNo ratings yet

- Management Acctg HospitalityDocument338 pagesManagement Acctg HospitalityGlenn Domingo80% (5)

- Corona Associates Capital Management, LLC - Q1 2019 Invesment Letter-4!29!19Document4 pagesCorona Associates Capital Management, LLC - Q1 2019 Invesment Letter-4!29!19Julian ScurciNo ratings yet

- Grams of Yogurt: U U U U UDocument3 pagesGrams of Yogurt: U U U U UPrateek BabbewalaNo ratings yet

- Examining &reporting On Tenders: Arithmetical Errors These May OccurDocument4 pagesExamining &reporting On Tenders: Arithmetical Errors These May Occursuman_civil100% (1)

- Industry Profile Management InventoryDocument113 pagesIndustry Profile Management InventoryBabu Battu100% (1)

- RWJLT FCF 2nd Ed CH 13Document46 pagesRWJLT FCF 2nd Ed CH 13Maria NatalinaNo ratings yet

- ACI PolicyBrief CreatingFertileGroundsforPrivateInvestmentinAirportsDocument48 pagesACI PolicyBrief CreatingFertileGroundsforPrivateInvestmentinAirportsIndranovsky IskandarNo ratings yet

- Head Quarter Level StrategyDocument11 pagesHead Quarter Level Strategyoureducation.inNo ratings yet

- DocxDocument33 pagesDocxGray Javier0% (1)

- ch03 PDFDocument9 pagesch03 PDFFaisal MumtazNo ratings yet

- Nec TSC High Pressure Cleaning ServicesDocument35 pagesNec TSC High Pressure Cleaning ServicesLiberty MunyatiNo ratings yet

- EMG152 - Assignment 1Document2 pagesEMG152 - Assignment 1Cedric RepradoNo ratings yet

- Mas MidtermsDocument4 pagesMas MidtermsClaudine DelacruzNo ratings yet

- Cpga Peg November 09Document9 pagesCpga Peg November 09Sheraz AhmedNo ratings yet

- Government Intervention in The MarketDocument12 pagesGovernment Intervention in The MarketAkshay LalwaniNo ratings yet

- Speed Limits Versus Slow SteamingDocument10 pagesSpeed Limits Versus Slow Steamingc rkNo ratings yet

- Tutorial - Chapter 1 - Introduction - Questions 1Document4 pagesTutorial - Chapter 1 - Introduction - Questions 1NandiieNo ratings yet

- Economics 1Document12 pagesEconomics 1jhozabethcarbonelNo ratings yet

- 002 Thakor 1991 Survey Game Theory and FinancesDocument14 pages002 Thakor 1991 Survey Game Theory and FinancesIdeas Guarani KaiowaNo ratings yet