Download as ppt, pdf, or txt

You might also like

- LLQP StudyNotesDocument8 pagesLLQP StudyNotesikawoako100% (2)

- Organ Donation Act of 1991: Prepared By: Dayle Daniel Sorveto, RMTDocument10 pagesOrgan Donation Act of 1991: Prepared By: Dayle Daniel Sorveto, RMTRC SILVESTRENo ratings yet

- Unit 1 LifeDocument10 pagesUnit 1 LifeMohammed HussainNo ratings yet

- Unit 1 E TrustsDocument46 pagesUnit 1 E TrustsKhanyisile SitholeNo ratings yet

- ILIT Power Point October 2010Document8 pagesILIT Power Point October 2010Christopher GuestNo ratings yet

- Trust - Tax Planning - Estate Planning - Real Estate & ReitsDocument62 pagesTrust - Tax Planning - Estate Planning - Real Estate & ReitsAbhijeet PatilNo ratings yet

- Taxation of TrustDocument4 pagesTaxation of TrustRahul ARNo ratings yet

- Introduction To Life Insurance V 1.2 Jan 10Document21 pagesIntroduction To Life Insurance V 1.2 Jan 10vij_raajeev5534No ratings yet

- M11 Estate Planning and Family BreakdownDocument60 pagesM11 Estate Planning and Family BreakdownjoannamanngoNo ratings yet

- Irrevocable Trusts Explained How They Work, TypeDocument1 pageIrrevocable Trusts Explained How They Work, TypemikayNo ratings yet

- Trust 3Document15 pagesTrust 3Manthan_Joshi_6850No ratings yet

- 0853 Aig Guide To TrustsDocument8 pages0853 Aig Guide To Trustsmails4vipsNo ratings yet

- Benedicto, Kim Gabriel M. ECO101 Report/Quiz Palines, Estifano Sir. de Los ReyesDocument11 pagesBenedicto, Kim Gabriel M. ECO101 Report/Quiz Palines, Estifano Sir. de Los ReyesKim GabrielNo ratings yet

- Safe Guarding Your Future: Financial Literacy How a Trusts Can Shield Your Assets & Reduce TaxesFrom EverandSafe Guarding Your Future: Financial Literacy How a Trusts Can Shield Your Assets & Reduce TaxesNo ratings yet

- WMR Code of Ethics Nov 2021 Website VersionDocument27 pagesWMR Code of Ethics Nov 2021 Website VersionfrankNo ratings yet

- Trust and Estate ManagementDocument18 pagesTrust and Estate ManagementBhuvan100% (1)

- Trusts Act 2019 - InformationDocument10 pagesTrusts Act 2019 - InformationGibson SheatNo ratings yet

- Lecture 5 - Fundamental Legal Principles (FULL)Document19 pagesLecture 5 - Fundamental Legal Principles (FULL)Ziyi YinNo ratings yet

- Insurance IDocument30 pagesInsurance IpushkarNo ratings yet

- WM Assignment Group 2Document8 pagesWM Assignment Group 2Rikhabh DasNo ratings yet

- Family TrustsDocument2 pagesFamily Trustsvsimas11No ratings yet

- Claims AdjustingDocument49 pagesClaims AdjustingJaime DaliuagNo ratings yet

- User Guide - Understanding TrustsDocument12 pagesUser Guide - Understanding TrustswgrajNo ratings yet

- LiabilitiesDocument37 pagesLiabilitiesJamil RiveraNo ratings yet

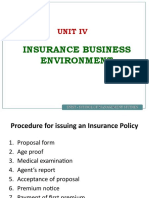

- Unit Iv: Insurance Business EnvironmentDocument20 pagesUnit Iv: Insurance Business Environmentmtechvlsitd labNo ratings yet

- TrustDocument4 pagesTrustkalinovskayaNo ratings yet

- Principles of Insurance - CHP 3Document25 pagesPrinciples of Insurance - CHP 3Hairul AziziNo ratings yet

- Bar Review Corp Law Part IiDocument78 pagesBar Review Corp Law Part IiJamie Rose AragonesNo ratings yet

- InsuranceDocument42 pagesInsurancePranavVohraNo ratings yet

- Trust Law 101 - Class NotesDocument2 pagesTrust Law 101 - Class NotesMichael JonesNo ratings yet

- Principles of LendingDocument32 pagesPrinciples of LendingsugirajamsrNo ratings yet

- Rev Trust 2016 Fall MeetingDocument10 pagesRev Trust 2016 Fall MeetingSheryllyne NacarioNo ratings yet

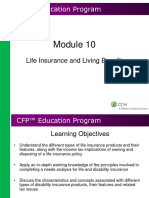

- Life Insurance and Living BenefitsDocument31 pagesLife Insurance and Living BenefitsblairkeaiNo ratings yet

- Trusts Oultine 2012Document34 pagesTrusts Oultine 2012David YergeeNo ratings yet

- Business Decision MakingDocument23 pagesBusiness Decision MakingKopal AgarwalNo ratings yet

- SecuritisationDocument26 pagesSecuritisationPuneet GargNo ratings yet

- Sources of Long-Term Financing: Chapter No. 4Document41 pagesSources of Long-Term Financing: Chapter No. 4Ruman MahmoodNo ratings yet

- Statuco Trust Guide 2016 DigitalDocument34 pagesStatuco Trust Guide 2016 DigitalDolly PuoengNo ratings yet

- Commercial Premium Financing: Exit StrategiesDocument3 pagesCommercial Premium Financing: Exit StrategiesKevin WheelerNo ratings yet

- Life Insurance MarketingDocument45 pagesLife Insurance MarketingKanishk GuptaNo ratings yet

- Session 3-4Document16 pagesSession 3-4SARA KOSHY RCBSNo ratings yet

- Unit II Kinds of SecuritiesDocument35 pagesUnit II Kinds of SecuritiesKanishka ReddyNo ratings yet

- A Securities-Based Line of Credit For Real Estate ProfessionalsDocument12 pagesA Securities-Based Line of Credit For Real Estate ProfessionalsJulesNo ratings yet

- Fund and Other InvestmentsDocument14 pagesFund and Other InvestmentsJay-L TanNo ratings yet

- Principle of LendingDocument32 pagesPrinciple of LendingashimathakurNo ratings yet

- Issue To The Applicant A Certifcte of RegistrationDocument8 pagesIssue To The Applicant A Certifcte of RegistrationGirish AroraNo ratings yet

- Accounting For InvestmentDocument29 pagesAccounting For InvestmentSyahrul AmirulNo ratings yet

- Bank LendingNEW11Document11 pagesBank LendingNEW11Loice MutetiNo ratings yet

- Difference Between Takaful and Conventional InsurencaaaaaaaaaaaDocument6 pagesDifference Between Takaful and Conventional InsurencaaaaaaaaaaaAyesha ShafiNo ratings yet

- Basics On TrustsDocument8 pagesBasics On TrustsMel Moxey50% (2)

- SecuritizationDocument22 pagesSecuritizationNishant_g90% (1)

- Trust ReceiptsDocument16 pagesTrust ReceiptsMonsterFish MNL (MonsterFishMNL)No ratings yet

- Captive Presentation Texas Department of Insurance: Presented byDocument74 pagesCaptive Presentation Texas Department of Insurance: Presented byTexasCaptivesNo ratings yet

- Banker As LenderDocument19 pagesBanker As Lendervanishachhabra5008No ratings yet

- 2nd UnitDocument29 pages2nd UnitkpericheNo ratings yet

- Jindal Global Law School: Concepts of Security-Creation, Perfection and Enforcement (With Special Emphasis On Mortgage)Document19 pagesJindal Global Law School: Concepts of Security-Creation, Perfection and Enforcement (With Special Emphasis On Mortgage)Giraj KumawatNo ratings yet

- Takaful Chapter 4 A201Document31 pagesTakaful Chapter 4 A201Cck CckweiNo ratings yet

- Topic 10 - Business TrustsDocument20 pagesTopic 10 - Business Trustsmissmokoena20No ratings yet

- Securitized Real Estate and 1031 ExchangesFrom EverandSecuritized Real Estate and 1031 ExchangesNo ratings yet

- Reverse Mortgage 2024: Unlock Your Home Equity for a Flourishing Retirement: The Essential Guidebook to Understanding Reverse Mortgages, Enhancing Retirement Planning, and Achieving Financial FreedomFrom EverandReverse Mortgage 2024: Unlock Your Home Equity for a Flourishing Retirement: The Essential Guidebook to Understanding Reverse Mortgages, Enhancing Retirement Planning, and Achieving Financial FreedomNo ratings yet

- Textbook of Urgent Care Management: Chapter 9, Insurance Requirements for the Urgent Care CenterFrom EverandTextbook of Urgent Care Management: Chapter 9, Insurance Requirements for the Urgent Care CenterNo ratings yet

- 5 in The Matter of Intestate Estate of RodriguezDocument4 pages5 in The Matter of Intestate Estate of RodriguezJeah N MelocotonesNo ratings yet

- Topic: Actions That Survive Doctrine: in Case of Unreasonable Delay in The Appointment of An Executor or Administrator of TheDocument57 pagesTopic: Actions That Survive Doctrine: in Case of Unreasonable Delay in The Appointment of An Executor or Administrator of TheJimi SolomonNo ratings yet

- JOAQUINO v. REYESDocument2 pagesJOAQUINO v. REYESKORINA NGALOY0% (1)

- Chapter - Ii Muslim Law of Testamentary SuccessionDocument51 pagesChapter - Ii Muslim Law of Testamentary Successiondeependra kumar100% (1)

- Settlement of Estate of Deceased Persons VenueDocument39 pagesSettlement of Estate of Deceased Persons VenueEunice Kalaw Vargas100% (1)

- Testacy of Maxima Santos Vda. de Blas. Rosalina Santos vs. Flora Blas de Buenaventura (Legatee), G.R. No. L-22797, September 22, 1966Document8 pagesTestacy of Maxima Santos Vda. de Blas. Rosalina Santos vs. Flora Blas de Buenaventura (Legatee), G.R. No. L-22797, September 22, 1966Sisinio BragatNo ratings yet

- Patricia Natcher vs. Court of Appeals Et. Al.Document3 pagesPatricia Natcher vs. Court of Appeals Et. Al.Susan FernandoNo ratings yet

- Daniel Studin - Uniform Probate Code, Last Updated 2008Document629 pagesDaniel Studin - Uniform Probate Code, Last Updated 2008Daniel StudinNo ratings yet

- Philippine Trust Co v. BohananDocument2 pagesPhilippine Trust Co v. BohananCourtney TirolNo ratings yet

- Pro SeDocument2 pagesPro SedaleNo ratings yet

- Wills & SuccessionDocument50 pagesWills & SuccessionJov May DimcoNo ratings yet

- Inheritance Tax Planning and Compliance RequirementsDocument4 pagesInheritance Tax Planning and Compliance RequirementsstflanagNo ratings yet

- Acific EporterDocument28 pagesAcific EporterScribd Government DocsNo ratings yet

- Succession Case DigestDocument24 pagesSuccession Case Digestmtabcao100% (1)

- Guerrero v. Director Land Management BureauDocument12 pagesGuerrero v. Director Land Management BureauJam NagamoraNo ratings yet

- Church Quiet TitleDocument119 pagesChurch Quiet Titlejerry mcleodNo ratings yet

- Conflicts of Law SUCCESSIONDocument15 pagesConflicts of Law SUCCESSIONlaursNo ratings yet

- in Re Estate of The Deceased Gregorio Tolentino - WillsDocument2 pagesin Re Estate of The Deceased Gregorio Tolentino - WillsAndrea TiuNo ratings yet

- Special ProceedingsDocument23 pagesSpecial ProceedingsJien LouNo ratings yet

- Spec Pro Nuguid V NuguidDocument9 pagesSpec Pro Nuguid V NuguidReah CrezzNo ratings yet

- Wills Rodriguez Vs RodriguezDocument1 pageWills Rodriguez Vs RodriguezMara Corteza San PedroNo ratings yet

- Section 10. Contestant To File Ground of Contest.: Rule 76 SECTIONS 10-13Document2 pagesSection 10. Contestant To File Ground of Contest.: Rule 76 SECTIONS 10-13Bfp Siniloan FS LagunaNo ratings yet

- Concepcion V ConcepcionDocument5 pagesConcepcion V ConcepcionRogie ToriagaNo ratings yet

- Lecture On Special Proceedings - JuristDocument364 pagesLecture On Special Proceedings - JuristNALDOGUIAJAYDENo ratings yet

- Suntay vs. Suntay FactsDocument2 pagesSuntay vs. Suntay FactsAQAANo ratings yet

- Nittscher Vs NittscherDocument5 pagesNittscher Vs NittscherJan Veah CaabayNo ratings yet

- PCIB V Escolin DigestDocument10 pagesPCIB V Escolin DigestGem LiNo ratings yet

- Labiano Succession DigestDocument2 pagesLabiano Succession DigestKrishianne LabianoNo ratings yet

- G.R. No. 127165 May 2, 2006 Salonga Hernandez & Allado, Olivia Sengco Pascual and The Honorable Court of APPEALS, RespondentsDocument34 pagesG.R. No. 127165 May 2, 2006 Salonga Hernandez & Allado, Olivia Sengco Pascual and The Honorable Court of APPEALS, Respondentscha chaNo ratings yet