Tax 103 Aug3 2013

Tax 103 Aug3 2013

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5825)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (903)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (823)

- Storytelling Script For Primary SchoolDocument1 pageStorytelling Script For Primary Schoolelfida8087% (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Conflict of Interpretations Essays in - Paul RicoeurDocument521 pagesThe Conflict of Interpretations Essays in - Paul RicoeurSam CrowNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Beauty StandardsDocument10 pagesBeauty StandardsBet TeixeiraNo ratings yet

- ChemysteryDocument37 pagesChemysteryMonique del RosarioNo ratings yet

- DTI and DOLE InterimGuidelinesonWorkplacePreventionandControlofCOVID19 3Document8 pagesDTI and DOLE InterimGuidelinesonWorkplacePreventionandControlofCOVID19 3Monique del RosarioNo ratings yet

- BB Phone OrderDocument1 pageBB Phone OrderMonique del RosarioNo ratings yet

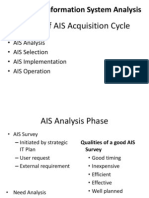

- Phases of AIS Acquisition Cycle: Accounting Information System AnalysisDocument6 pagesPhases of AIS Acquisition Cycle: Accounting Information System AnalysisMonique del RosarioNo ratings yet

- Canon Selphy ES30 GuideDocument102 pagesCanon Selphy ES30 GuideMonique del RosarioNo ratings yet

- NGAS Vol 2 CH 1Document7 pagesNGAS Vol 2 CH 1Monique del RosarioNo ratings yet

- Users of Information: Fundamentals of Information Systems and Systems Development Lecture 2Document11 pagesUsers of Information: Fundamentals of Information Systems and Systems Development Lecture 2Monique del RosarioNo ratings yet

- CIS Lec2Document11 pagesCIS Lec2Monique del RosarioNo ratings yet

- State Audit Code of The Philippines (P.D. 1445)Document37 pagesState Audit Code of The Philippines (P.D. 1445)Monique del Rosario100% (3)

- AIS Lec2Document48 pagesAIS Lec2Monique del RosarioNo ratings yet

- AIS Lec1Document32 pagesAIS Lec1Monique del RosarioNo ratings yet

- 10th 2nd Lang Eng 1Document31 pages10th 2nd Lang Eng 1Pubg KeliyeNo ratings yet

- Round Shapes and Square Shapes Representation of ShapesDocument8 pagesRound Shapes and Square Shapes Representation of ShapeselmoNo ratings yet

- Mains Filter 250V 25A Article Number B3058365K BarcoDocument3 pagesMains Filter 250V 25A Article Number B3058365K Barcojay leeNo ratings yet

- Otable Ews: Mennonite Children's ChoirDocument14 pagesOtable Ews: Mennonite Children's ChoirMaria BowmanNo ratings yet

- Lithium Orotate Helps PTSD - TestimonialsDocument74 pagesLithium Orotate Helps PTSD - TestimonialsjofortruthNo ratings yet

- United States Court of Appeals, Second CircuitDocument22 pagesUnited States Court of Appeals, Second CircuitScribd Government DocsNo ratings yet

- Assigment Problem 2Document5 pagesAssigment Problem 2William Y. OspinaNo ratings yet

- Literary DevicesDocument22 pagesLiterary DevicesHammadJavaid ConceptNo ratings yet

- Broken Toy Obooko Rom0311Document69 pagesBroken Toy Obooko Rom0311Themba Mhlanga MposekieNo ratings yet

- Principles 1Document13 pagesPrinciples 1RicaNo ratings yet

- Admiralty LawDocument576 pagesAdmiralty LawRihardsNo ratings yet

- Yoruba and Benin Kingdom - Ile Ife The Final Resting Place of HistoryDocument5 pagesYoruba and Benin Kingdom - Ile Ife The Final Resting Place of HistoryugwakaluNo ratings yet

- Cito Proefschrift Maarten Marsman PDFDocument114 pagesCito Proefschrift Maarten Marsman PDFtimobechgerNo ratings yet

- Full Download PDF of Fundamentals of Anatomy & Physiology Martini Nath 9th Edition Test Bank All ChapterDocument43 pagesFull Download PDF of Fundamentals of Anatomy & Physiology Martini Nath 9th Edition Test Bank All Chapterterzovleiser100% (4)

- Resume-Amy FowlerDocument2 pagesResume-Amy Fowlerapi-417811233No ratings yet

- La Civilta Cattolica 15 July 2020Document128 pagesLa Civilta Cattolica 15 July 2020Tetiana BogoslavetsNo ratings yet

- A Study On Nonlinear Behaviour of Subgrades Under Cyclic LoadingDocument364 pagesA Study On Nonlinear Behaviour of Subgrades Under Cyclic LoadingSamanta Pandey100% (1)

- Journal of Electrical EngineeringDocument16 pagesJournal of Electrical EngineeringkodandaramNo ratings yet

- Falling Worlds by Z0RUASDocument19 pagesFalling Worlds by Z0RUASGleneeveeNo ratings yet

- Rodriguez, A. G. & Mckay, S. (2010) - Professional Development For Experienced Teachers Working WithDocument4 pagesRodriguez, A. G. & Mckay, S. (2010) - Professional Development For Experienced Teachers Working WithAaron Jay MondayaNo ratings yet

- Fs 8Document12 pagesFs 8May Cruzel TorresNo ratings yet

- Fashion - PortfolioDocument99 pagesFashion - PortfolioPalak ShrivastavaNo ratings yet

- The Brantley EnterpriseDocument10 pagesThe Brantley EnterprisesegacomNo ratings yet

- Simple PastDocument25 pagesSimple PastAilyn Corpuz SamsonNo ratings yet

- Autism Spectrum Disorder Diagnostic Assessment Report: Greg ExampleDocument42 pagesAutism Spectrum Disorder Diagnostic Assessment Report: Greg ExampleADI-RRNo ratings yet

- Study of Fully Homomorphic Encryption Over IntegersDocument4 pagesStudy of Fully Homomorphic Encryption Over IntegersAnonymous lPvvgiQjRNo ratings yet

- Recovery of Immovable PropertyDocument3 pagesRecovery of Immovable PropertyAzad SamiNo ratings yet

Download as pptx, pdf, or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5825)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (903)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (823)

- Storytelling Script For Primary SchoolDocument1 pageStorytelling Script For Primary Schoolelfida8087% (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Conflict of Interpretations Essays in - Paul RicoeurDocument521 pagesThe Conflict of Interpretations Essays in - Paul RicoeurSam CrowNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Beauty StandardsDocument10 pagesBeauty StandardsBet TeixeiraNo ratings yet

- ChemysteryDocument37 pagesChemysteryMonique del RosarioNo ratings yet

- DTI and DOLE InterimGuidelinesonWorkplacePreventionandControlofCOVID19 3Document8 pagesDTI and DOLE InterimGuidelinesonWorkplacePreventionandControlofCOVID19 3Monique del RosarioNo ratings yet

- BB Phone OrderDocument1 pageBB Phone OrderMonique del RosarioNo ratings yet

- Phases of AIS Acquisition Cycle: Accounting Information System AnalysisDocument6 pagesPhases of AIS Acquisition Cycle: Accounting Information System AnalysisMonique del RosarioNo ratings yet

- Canon Selphy ES30 GuideDocument102 pagesCanon Selphy ES30 GuideMonique del RosarioNo ratings yet

- NGAS Vol 2 CH 1Document7 pagesNGAS Vol 2 CH 1Monique del RosarioNo ratings yet

- Users of Information: Fundamentals of Information Systems and Systems Development Lecture 2Document11 pagesUsers of Information: Fundamentals of Information Systems and Systems Development Lecture 2Monique del RosarioNo ratings yet

- CIS Lec2Document11 pagesCIS Lec2Monique del RosarioNo ratings yet

- State Audit Code of The Philippines (P.D. 1445)Document37 pagesState Audit Code of The Philippines (P.D. 1445)Monique del Rosario100% (3)

- AIS Lec2Document48 pagesAIS Lec2Monique del RosarioNo ratings yet

- AIS Lec1Document32 pagesAIS Lec1Monique del RosarioNo ratings yet

- 10th 2nd Lang Eng 1Document31 pages10th 2nd Lang Eng 1Pubg KeliyeNo ratings yet

- Round Shapes and Square Shapes Representation of ShapesDocument8 pagesRound Shapes and Square Shapes Representation of ShapeselmoNo ratings yet

- Mains Filter 250V 25A Article Number B3058365K BarcoDocument3 pagesMains Filter 250V 25A Article Number B3058365K Barcojay leeNo ratings yet

- Otable Ews: Mennonite Children's ChoirDocument14 pagesOtable Ews: Mennonite Children's ChoirMaria BowmanNo ratings yet

- Lithium Orotate Helps PTSD - TestimonialsDocument74 pagesLithium Orotate Helps PTSD - TestimonialsjofortruthNo ratings yet

- United States Court of Appeals, Second CircuitDocument22 pagesUnited States Court of Appeals, Second CircuitScribd Government DocsNo ratings yet

- Assigment Problem 2Document5 pagesAssigment Problem 2William Y. OspinaNo ratings yet

- Literary DevicesDocument22 pagesLiterary DevicesHammadJavaid ConceptNo ratings yet

- Broken Toy Obooko Rom0311Document69 pagesBroken Toy Obooko Rom0311Themba Mhlanga MposekieNo ratings yet

- Principles 1Document13 pagesPrinciples 1RicaNo ratings yet

- Admiralty LawDocument576 pagesAdmiralty LawRihardsNo ratings yet

- Yoruba and Benin Kingdom - Ile Ife The Final Resting Place of HistoryDocument5 pagesYoruba and Benin Kingdom - Ile Ife The Final Resting Place of HistoryugwakaluNo ratings yet

- Cito Proefschrift Maarten Marsman PDFDocument114 pagesCito Proefschrift Maarten Marsman PDFtimobechgerNo ratings yet

- Full Download PDF of Fundamentals of Anatomy & Physiology Martini Nath 9th Edition Test Bank All ChapterDocument43 pagesFull Download PDF of Fundamentals of Anatomy & Physiology Martini Nath 9th Edition Test Bank All Chapterterzovleiser100% (4)

- Resume-Amy FowlerDocument2 pagesResume-Amy Fowlerapi-417811233No ratings yet

- La Civilta Cattolica 15 July 2020Document128 pagesLa Civilta Cattolica 15 July 2020Tetiana BogoslavetsNo ratings yet

- A Study On Nonlinear Behaviour of Subgrades Under Cyclic LoadingDocument364 pagesA Study On Nonlinear Behaviour of Subgrades Under Cyclic LoadingSamanta Pandey100% (1)

- Journal of Electrical EngineeringDocument16 pagesJournal of Electrical EngineeringkodandaramNo ratings yet

- Falling Worlds by Z0RUASDocument19 pagesFalling Worlds by Z0RUASGleneeveeNo ratings yet

- Rodriguez, A. G. & Mckay, S. (2010) - Professional Development For Experienced Teachers Working WithDocument4 pagesRodriguez, A. G. & Mckay, S. (2010) - Professional Development For Experienced Teachers Working WithAaron Jay MondayaNo ratings yet

- Fs 8Document12 pagesFs 8May Cruzel TorresNo ratings yet

- Fashion - PortfolioDocument99 pagesFashion - PortfolioPalak ShrivastavaNo ratings yet

- The Brantley EnterpriseDocument10 pagesThe Brantley EnterprisesegacomNo ratings yet

- Simple PastDocument25 pagesSimple PastAilyn Corpuz SamsonNo ratings yet

- Autism Spectrum Disorder Diagnostic Assessment Report: Greg ExampleDocument42 pagesAutism Spectrum Disorder Diagnostic Assessment Report: Greg ExampleADI-RRNo ratings yet

- Study of Fully Homomorphic Encryption Over IntegersDocument4 pagesStudy of Fully Homomorphic Encryption Over IntegersAnonymous lPvvgiQjRNo ratings yet

- Recovery of Immovable PropertyDocument3 pagesRecovery of Immovable PropertyAzad SamiNo ratings yet