Download as ppt, pdf, or txt

You might also like

- Investor Database MumbaiDocument9 pagesInvestor Database MumbaiVishal JwellNo ratings yet

- Apeal 4Document2 pagesApeal 4Sultan AfzalNo ratings yet

- Yacht and Small Craft Surveying: Diploma inDocument46 pagesYacht and Small Craft Surveying: Diploma inAdele Murray100% (1)

- Finance Bill 2009 - Direct Tax Proposals: Presentation By: CA. Kapil Goel, ACA, LLB Chartered Accountant New DelhiDocument43 pagesFinance Bill 2009 - Direct Tax Proposals: Presentation By: CA. Kapil Goel, ACA, LLB Chartered Accountant New DelhiPrasad KadamNo ratings yet

- Finance Bill 2010Document51 pagesFinance Bill 2010riddhivakhariaNo ratings yet

- Income Tax Amendments & Transition Notes For CA Inter May 24 byDocument63 pagesIncome Tax Amendments & Transition Notes For CA Inter May 24 byRutika ShindeNo ratings yet

- Union Budget 2012-Income TaxDocument21 pagesUnion Budget 2012-Income TaxFinquity IndiaNo ratings yet

- Budget 2020 HighlightsDocument12 pagesBudget 2020 HighlightsPriyankaNo ratings yet

- RSM India Newsflash - Employees Guidance On New Vs Old Tax Regime Individuals April 2020Document17 pagesRSM India Newsflash - Employees Guidance On New Vs Old Tax Regime Individuals April 2020Rohan JainNo ratings yet

- CA CS CMA Final Statutory Updates For Nov Dec 2020Document43 pagesCA CS CMA Final Statutory Updates For Nov Dec 2020Anu GraphicsNo ratings yet

- OL 4 - BLT Study Text Suppliment 2021 - On New Tax AmmendmentsDocument28 pagesOL 4 - BLT Study Text Suppliment 2021 - On New Tax Ammendmentshte19031No ratings yet

- FAQ On Budget FY 2020-21Document9 pagesFAQ On Budget FY 2020-21GUNANo ratings yet

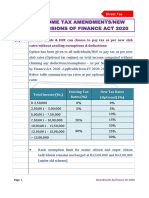

- Income Tax Amendments/New Provisions of Finance Act 2020Document46 pagesIncome Tax Amendments/New Provisions of Finance Act 2020shubhamworkNo ratings yet

- 80TTB - Provides Deduction Benefit On Interest Income For Senior CitizensDocument1 page80TTB - Provides Deduction Benefit On Interest Income For Senior CitizensArjun VermaNo ratings yet

- AmendDocument25 pagesAmendanshulagarwal62No ratings yet

- GST Update124Document6 pagesGST Update124suhani singhNo ratings yet

- Amendments in Service TaxDocument15 pagesAmendments in Service TaxShankar NarayananNo ratings yet

- YYC July NewsletterDocument11 pagesYYC July NewsletterCatherine ChuaNo ratings yet

- Category Current (RS) Proposed (RS) Savings P.A. (RS) : Direct TaxDocument16 pagesCategory Current (RS) Proposed (RS) Savings P.A. (RS) : Direct TaxshwetakuppanNo ratings yet

- @dtaxmcq Income Tax Amendment SheetDocument50 pages@dtaxmcq Income Tax Amendment Sheetmshivam617No ratings yet

- Tax Updates For June 2012 ExamsDocument37 pagesTax Updates For June 2012 ExamsShanky MalhotraNo ratings yet

- CAclubindia News - The SUPER Budget - AnalysisDocument15 pagesCAclubindia News - The SUPER Budget - AnalysisMahaveer DhelariyaNo ratings yet

- Statutory Updates For Nov-21 ExamsDocument50 pagesStatutory Updates For Nov-21 ExamsShodasakshari VidyaNo ratings yet

- Tax Icsi 2012Document84 pagesTax Icsi 2012Janani ParameswaranNo ratings yet

- Elective Ourse in Commerce ECO-11 Elements of Income TaxDocument12 pagesElective Ourse in Commerce ECO-11 Elements of Income TaxJai GorakhNo ratings yet

- Paper-18 Supplementary 180221Document109 pagesPaper-18 Supplementary 180221Srihari SrinivasNo ratings yet

- Presentation TaxDocument25 pagesPresentation Taxsrihimanshu1988No ratings yet

- Composition SchemeDocument4 pagesComposition Schemecloudstorage567No ratings yet

- 2017 Amendments To The Tax Code by The TRAIN LawDocument28 pages2017 Amendments To The Tax Code by The TRAIN LawScarlette CooperaNo ratings yet

- 56212rtpfinaloldnov19 p7Document52 pages56212rtpfinaloldnov19 p7naveen kumarNo ratings yet

- BDO Budget Snapshot - 2012-13Document9 pagesBDO Budget Snapshot - 2012-13Pulluri Ravikumar YugandarNo ratings yet

- Special Provisions Relating To Taxation of IncomeDocument27 pagesSpecial Provisions Relating To Taxation of IncomeABC 123No ratings yet

- Decoding Indian Union Budget Finance Bil PDFDocument7 pagesDecoding Indian Union Budget Finance Bil PDFkumarNo ratings yet

- Income Which Do Not Form Part of Total Income: HapterDocument33 pagesIncome Which Do Not Form Part of Total Income: HapterAleti NithishNo ratings yet

- When Will The New Scheme Be Applicable?: Faqs On Budget Fy 2020-21Document6 pagesWhen Will The New Scheme Be Applicable?: Faqs On Budget Fy 2020-21Biswabandhu PalNo ratings yet

- Deductions From Gross Total IncomeDocument8 pagesDeductions From Gross Total IncomeDevil GamerNo ratings yet

- Chapter 8 Composition Scheme Under GSTDocument12 pagesChapter 8 Composition Scheme Under GSTDR. PREETI JINDALNo ratings yet

- Latest Circulars, Notifications and Press Releases: 2. This Notification Shall Come Into Force From The 1Document0 pagesLatest Circulars, Notifications and Press Releases: 2. This Notification Shall Come Into Force From The 1Ketan ThakkarNo ratings yet

- Budget 2013 - 2014Document11 pagesBudget 2013 - 2014sdfdhgtj894No ratings yet

- Chapter 5 Composition Scheme Nov 2020Document41 pagesChapter 5 Composition Scheme Nov 2020Alka GuptaNo ratings yet

- Amendment Final N2020 BGSirDocument30 pagesAmendment Final N2020 BGSirAfnan KhanNo ratings yet

- The Budget 2011 - A Glimpse: Shetty Prabhu & AshokDocument15 pagesThe Budget 2011 - A Glimpse: Shetty Prabhu & AshokMadhusudan MagajiNo ratings yet

- Income Tax ActDocument4 pagesIncome Tax ActgoborgonesNo ratings yet

- Income Tax AmendmentsNew Provisions of Finance Act 2020Document26 pagesIncome Tax AmendmentsNew Provisions of Finance Act 2020Piyush HarlalkaNo ratings yet

- Understanding On: Tax Audit U/s 44AB of I.T. ActDocument29 pagesUnderstanding On: Tax Audit U/s 44AB of I.T. Actspchheda4996No ratings yet

- Income Tax - Major Highlights of Union Budget - 2011-12: Prasad V Sawant Roll No:96 Tax AssignmentDocument5 pagesIncome Tax - Major Highlights of Union Budget - 2011-12: Prasad V Sawant Roll No:96 Tax AssignmentJohn DoinNo ratings yet

- Mat and Amt: Objective of Levying MATDocument17 pagesMat and Amt: Objective of Levying MATSamuel AnthrayoseNo ratings yet

- Comparative Analysis of Financial Bills: C C C CCDocument5 pagesComparative Analysis of Financial Bills: C C C CCpdabriwalNo ratings yet

- AFF's Tax Memorandum - Changes in Finance Bill, 2023 (Pakistan)Document14 pagesAFF's Tax Memorandum - Changes in Finance Bill, 2023 (Pakistan)salahuddin ahmedNo ratings yet

- Draft File (Shafin)Document11 pagesDraft File (Shafin)MD Shafin AhmedNo ratings yet

- Delloite CIT (A) PDFDocument7 pagesDelloite CIT (A) PDFshashi vermaNo ratings yet

- TNF Korea Tax Reform Aug10 2023Document7 pagesTNF Korea Tax Reform Aug10 2023crazymoneyNo ratings yet

- Pre Budget1 MemorandumDocument29 pagesPre Budget1 Memorandumnikhilsawant93No ratings yet

- Pawan 115ja JCDocument35 pagesPawan 115ja JCKapasi TejasNo ratings yet

- Indirect Tax - Budget 2019Document43 pagesIndirect Tax - Budget 2019Brijesh PitrodaNo ratings yet

- Mat - PPT FinalDocument18 pagesMat - PPT FinalAkash PatelNo ratings yet

- Minimum Alternate Tax MAT PDFDocument6 pagesMinimum Alternate Tax MAT PDFmuskan khatriNo ratings yet

- Mat and Amt: Objective of Levying MATDocument17 pagesMat and Amt: Objective of Levying MATNitin ChoudharyNo ratings yet

- Overview of The Amendments-Train LawDocument23 pagesOverview of The Amendments-Train LawCha GalangNo ratings yet

- Critical Analysis of Income Tax Ordinance 2010Document16 pagesCritical Analysis of Income Tax Ordinance 2010Dilnawaz KhanNo ratings yet

- Uganda Tax Amendment Bills For 2018Document10 pagesUganda Tax Amendment Bills For 2018jadwongscribdNo ratings yet

- Section 80CCD (1B) Deduction - About NPS Scheme & Tax BenefitsDocument7 pagesSection 80CCD (1B) Deduction - About NPS Scheme & Tax BenefitsP B ChaudharyNo ratings yet

- 2013 GUIDELINES On Marginal Fields UpdateDocument29 pages2013 GUIDELINES On Marginal Fields UpdateHampus DynebrinkNo ratings yet

- MBA 2020 - MBA508-MBA2020 - 2020 - 3 - Final - OutlineDocument12 pagesMBA 2020 - MBA508-MBA2020 - 2020 - 3 - Final - OutlineamaanrizaNo ratings yet

- Turban Dss9e Im Ch02Document15 pagesTurban Dss9e Im Ch02jennytan8970330% (1)

- Sample Contents of A Completed Feasibility StudyDocument4 pagesSample Contents of A Completed Feasibility StudyMatthew DasigNo ratings yet

- Internal Table Operations - Internal Tables and Work Areas - SapnutsDocument4 pagesInternal Table Operations - Internal Tables and Work Areas - SapnutsDeepakNo ratings yet

- The New Industrial PolicyDocument4 pagesThe New Industrial PolicyPratima KambleNo ratings yet

- Bonus Shares, Right Shares PDFDocument30 pagesBonus Shares, Right Shares PDFNaga ChandraNo ratings yet

- RiseSmart Career Transition Services - For Responsability PDFDocument14 pagesRiseSmart Career Transition Services - For Responsability PDFAlaksamNo ratings yet

- Training and Development @godrejDocument23 pagesTraining and Development @godrejrohitbhargoNo ratings yet

- Explain Diversifiable Risk and Non-Diversifiable Risk in Financial Markets?Document2 pagesExplain Diversifiable Risk and Non-Diversifiable Risk in Financial Markets?fnajwa55No ratings yet

- CH 02 AnswersDocument25 pagesCH 02 AnswerscheekbutterNo ratings yet

- 21-1361558 City of Warren - Forensic Accounting REPORTDocument16 pages21-1361558 City of Warren - Forensic Accounting REPORTdaneNo ratings yet

- Clearsight Monitor - Professional Services Industry UpdateDocument9 pagesClearsight Monitor - Professional Services Industry UpdateClearsight AdvisorsNo ratings yet

- Solution Manual For Fundamentals of Taxation 2019 Edition 12th by CruzDocument31 pagesSolution Manual For Fundamentals of Taxation 2019 Edition 12th by CruzSherryBakerdawz100% (40)

- Financial Accounting and Reporting - Week 1 Topic 1 - Overview of AccountingDocument9 pagesFinancial Accounting and Reporting - Week 1 Topic 1 - Overview of AccountingLuisitoNo ratings yet

- Ee Assignment Lu 6Document6 pagesEe Assignment Lu 6NethiyaaRajendranNo ratings yet

- Century Textile ReportDocument4 pagesCentury Textile ReportAishwarya WakkarNo ratings yet

- GST CertificateDocument3 pagesGST CertificateRajakumar RajendranNo ratings yet

- Aud 4 - BPO Industry 2022Document32 pagesAud 4 - BPO Industry 20229nh9xfrkqyNo ratings yet

- Final ReportSTUDY OF EMPLOYER BRANDING IT SECTOR (TCS & WIPRO) THROUGH THE EYES OF POTENTIAL EMPLOYEESDocument50 pagesFinal ReportSTUDY OF EMPLOYER BRANDING IT SECTOR (TCS & WIPRO) THROUGH THE EYES OF POTENTIAL EMPLOYEESShouvik Oblivious Bhattacharya0% (1)

- IAS 16 NotesDocument2 pagesIAS 16 Notesshoaib jamshedNo ratings yet

- Walmat Case Study-M IsasmendiDocument10 pagesWalmat Case Study-M IsasmendiCairis CairisNo ratings yet

- Topic 8 Currency Derivatives FutureDocument26 pagesTopic 8 Currency Derivatives Futurecyrax 3000No ratings yet

- Ambit PDFDocument70 pagesAmbit PDFshahavNo ratings yet

- NAME XXXXXXX: Personal StatementDocument3 pagesNAME XXXXXXX: Personal Statement끄저긔No ratings yet

- Submitted To: Submitted By:: Marketing PlanDocument8 pagesSubmitted To: Submitted By:: Marketing PlanZeeshan AhmadNo ratings yet

- 6043 Coursework Handbook Sample Projects (For Examination From 2020)Document95 pages6043 Coursework Handbook Sample Projects (For Examination From 2020)VivekNo ratings yet