Download as ppt, pdf, or txt

You might also like

- Original PDF Financial Management Core Concepts 4th Edition by Raymond Brooks PDFDocument42 pagesOriginal PDF Financial Management Core Concepts 4th Edition by Raymond Brooks PDFmathew.robertson818100% (40)

- Burton SensorsDocument7 pagesBurton SensorsMOHIT SINGHNo ratings yet

- ch04 PDFDocument4 pagesch04 PDFMosharraf HussainNo ratings yet

- Earn Hart Corporation Has Outstanding 3 000 000 Shares of Common PDFDocument1 pageEarn Hart Corporation Has Outstanding 3 000 000 Shares of Common PDFAnbu jaromiaNo ratings yet

- Investments Levy and Post PDFDocument82 pagesInvestments Levy and Post PDFDivyanshi SatsangiNo ratings yet

- Soal Kuis Asistensi AK1 Setelah UTSDocument6 pagesSoal Kuis Asistensi AK1 Setelah UTSManggala Patria WicaksonoNo ratings yet

- Question and Answer - 8Document30 pagesQuestion and Answer - 8acc-expertNo ratings yet

- Chap 011Document44 pagesChap 011Jessica Cola50% (2)

- Week 09 - Tutorial-Mishal Manzoor (Fins3616) - T3 2020Document106 pagesWeek 09 - Tutorial-Mishal Manzoor (Fins3616) - T3 2020Kelvin ChenNo ratings yet

- Ifrs 9Document80 pagesIfrs 9Veer Pratab SinghNo ratings yet

- Chapter 2 (Tan&Lee)Document47 pagesChapter 2 (Tan&Lee)desy nataNo ratings yet

- Gitman IM Ch09Document24 pagesGitman IM Ch09Imran FarmanNo ratings yet

- Tutor Revenue RecognitionDocument20 pagesTutor Revenue RecognitionAngel Valentine TirayoNo ratings yet

- Module 9-DIRECT FINANCING LEASE - LESSORDocument10 pagesModule 9-DIRECT FINANCING LEASE - LESSORJeanivyle CarmonaNo ratings yet

- Kieso 6Document54 pagesKieso 6noortiaNo ratings yet

- Chapter 12 Solution ManualDocument68 pagesChapter 12 Solution ManualRiskaNo ratings yet

- Kieso 14e PowerPoint Ch24Document59 pagesKieso 14e PowerPoint Ch24James LeeNo ratings yet

- Z003800101201740141305080572 448187Document51 pagesZ003800101201740141305080572 448187Dian AnitaNo ratings yet

- Hybrid Financing Final 2011-2012Document33 pagesHybrid Financing Final 2011-2012Kim Aaron T. RuizNo ratings yet

- Beams10e Ch04 Consolidation Techniques and ProceduresDocument48 pagesBeams10e Ch04 Consolidation Techniques and ProceduresLeini TanNo ratings yet

- Chapter 01 - Business CombinationsDocument17 pagesChapter 01 - Business CombinationsTina LundstromNo ratings yet

- CH 01Document53 pagesCH 01Triệu Nguyễn MinhNo ratings yet

- CH 21Document11 pagesCH 21Hanif MusyaffaNo ratings yet

- Beams10e Ch07 Intercompany Profit Transactions BondsDocument25 pagesBeams10e Ch07 Intercompany Profit Transactions BondsIrma RismayantiNo ratings yet

- Summary of The Case 24Document11 pagesSummary of The Case 24farisa.oeNo ratings yet

- CH 21Document144 pagesCH 21fiorensaNo ratings yet

- Chapter 13Document38 pagesChapter 13Kimmy ShawwyNo ratings yet

- Audit Sampling For Tests of Details of BalancesDocument43 pagesAudit Sampling For Tests of Details of BalancesEndah Hamidah AiniNo ratings yet

- Euro Disney and The First Five Steps of Accounting AnalysisDocument8 pagesEuro Disney and The First Five Steps of Accounting AnalysisblackraidenNo ratings yet

- Beams Aa13e PPT 14Document43 pagesBeams Aa13e PPT 14Abeer Al OlaimatNo ratings yet

- 109Document34 pages109danara1991No ratings yet

- Chapter 23Document56 pagesChapter 23Jennifer BrattainNo ratings yet

- Beams10e Ch06 Intercompany Profit Transactions Plant AssetsDocument30 pagesBeams10e Ch06 Intercompany Profit Transactions Plant AssetsLeini TanNo ratings yet

- Share Based PaymentDocument13 pagesShare Based PaymentPHI NGUYEN HOANGNo ratings yet

- Partnership FormationDocument28 pagesPartnership FormationDe Gala ShailynNo ratings yet

- Learning Packet FINMAN2-03 Working Capital Management and FinancingDocument10 pagesLearning Packet FINMAN2-03 Working Capital Management and FinancingDanica Christele AlfaroNo ratings yet

- Audit Risk Model Application ProblemsDocument2 pagesAudit Risk Model Application ProblemsZoe MoranNo ratings yet

- Financial Accounting - TheoriesDocument5 pagesFinancial Accounting - TheoriesKim Cristian MaañoNo ratings yet

- P 6 DepresiasiDocument101 pagesP 6 DepresiasiRaehan RaesaNo ratings yet

- Chap 11 - Equity Analysis and ValuationDocument26 pagesChap 11 - Equity Analysis and ValuationWindyee TanNo ratings yet

- Audit Module 2 - Payroll Tax and Superannuation WorkpaperDocument2 pagesAudit Module 2 - Payroll Tax and Superannuation WorkpaperSiddhant AggarwalNo ratings yet

- ch11 Beams10e TBDocument28 pagesch11 Beams10e TBK. CustodioNo ratings yet

- Rais12 SM CH17Document23 pagesRais12 SM CH17Anton VitaliNo ratings yet

- Romney Ais14 CH 16 General Ledger and Reporting SystemDocument11 pagesRomney Ais14 CH 16 General Ledger and Reporting SystemHabteweld EdluNo ratings yet

- Early in The Year Bill Barnes and Several Friends OrganizedDocument1 pageEarly in The Year Bill Barnes and Several Friends OrganizedM Bilal Saleem0% (1)

- Boynton SM CH 14Document52 pagesBoynton SM CH 14jeankopler50% (2)

- ch18, IFRS 15Document107 pagesch18, IFRS 15Bayan KttbNo ratings yet

- The Basics of Capital Budgeting: Should We Build This Plant?Document42 pagesThe Basics of Capital Budgeting: Should We Build This Plant?Harry Satria PutraNo ratings yet

- The Basics of Capital Budgeting: Apakah Akan Membangun Pabrik?Document43 pagesThe Basics of Capital Budgeting: Apakah Akan Membangun Pabrik?Ibrahim SanyNo ratings yet

- Capital BudgetingDocument52 pagesCapital Budgetinganuz7611No ratings yet

- The Basics of Capital Budgeting: Should We Build This Plant?Document51 pagesThe Basics of Capital Budgeting: Should We Build This Plant?Montasir Islam ZeesunNo ratings yet

- Apital Budgeting: Decision Criteria: Should We Build This Plant?Document59 pagesApital Budgeting: Decision Criteria: Should We Build This Plant?hendraNo ratings yet

- The Basics of Capital Budgeting: Evaluating Cash Flows: Should We Build This Plant?Document22 pagesThe Basics of Capital Budgeting: Evaluating Cash Flows: Should We Build This Plant?Anonymous 9YDoWXXNo ratings yet

- What Is Capital Budgeting? Steps: ImportantDocument21 pagesWhat Is Capital Budgeting? Steps: ImportantÖzge UzerNo ratings yet

- The Basics of Capital Budgeting: Evaluating Cash Flows: Should We Build This Plant?Document59 pagesThe Basics of Capital Budgeting: Evaluating Cash Flows: Should We Build This Plant?sidhanthaNo ratings yet

- ffm911 CBDocument42 pagesffm911 CBnisyaa callistaNo ratings yet

- Capital BudgetingDocument41 pagesCapital Budgetingcatharina arnitaNo ratings yet

- The Basics of Capital Budgeting: Should We Build This Plant?Document30 pagesThe Basics of Capital Budgeting: Should We Build This Plant?siddis316No ratings yet

- Capital Budgeting: Should We Build This Plant? Should We Build This Plant?Document24 pagesCapital Budgeting: Should We Build This Plant? Should We Build This Plant?Ankkit PandeyNo ratings yet

- Basics of Capital BudgetingDocument28 pagesBasics of Capital BudgetingEugene NavarroNo ratings yet

- The Basics of Capital Budgeting: Should We Build This Plant?Document28 pagesThe Basics of Capital Budgeting: Should We Build This Plant?Jessica Adharana KurniaNo ratings yet

- Basics of Capital Budgeting PDFDocument26 pagesBasics of Capital Budgeting PDFShikinNorehaNo ratings yet

- Editorial PDFDocument1 pageEditorial PDFChaitanya JagarlapudiNo ratings yet

- IDirect GSKConsumer ICDocument26 pagesIDirect GSKConsumer ICChaitanya JagarlapudiNo ratings yet

- Quarterly Update - June 2021Document5 pagesQuarterly Update - June 2021Chaitanya Jagarlapudi100% (1)

- Quarterly Report - September 2021Document6 pagesQuarterly Report - September 2021Chaitanya JagarlapudiNo ratings yet

- Intellect Technology Day Presentations June 2021Document176 pagesIntellect Technology Day Presentations June 2021Chaitanya JagarlapudiNo ratings yet

- DAWisdomGreatInvestors 1213Document14 pagesDAWisdomGreatInvestors 1213Chaitanya JagarlapudiNo ratings yet

- Bernstein Journal Summer08Document39 pagesBernstein Journal Summer08Chaitanya JagarlapudiNo ratings yet

- 1-TMG Student Mannual-Introduction To The CompetitionDocument78 pages1-TMG Student Mannual-Introduction To The CompetitionChaitanya JagarlapudiNo ratings yet

- 05aug2014 India DailyDocument73 pages05aug2014 India DailyChaitanya JagarlapudiNo ratings yet

- Shree Rama Multi-Tech Ltd1 140114Document2 pagesShree Rama Multi-Tech Ltd1 140114Chaitanya JagarlapudiNo ratings yet

- (Kotak) ICICI Bank, January 31, 2013Document14 pages(Kotak) ICICI Bank, January 31, 2013Chaitanya JagarlapudiNo ratings yet

- Tod Nielsen VMworld 2012Document23 pagesTod Nielsen VMworld 2012Chaitanya JagarlapudiNo ratings yet

- Savita Oil Technologies LTD (SOTL) : Techno Fundamental Note CMP: Rs.400.60Document7 pagesSavita Oil Technologies LTD (SOTL) : Techno Fundamental Note CMP: Rs.400.60Chaitanya JagarlapudiNo ratings yet

- Shree AjitDocument8 pagesShree AjitChaitanya JagarlapudiNo ratings yet

- AcrysilDocument89 pagesAcrysilChaitanya JagarlapudiNo ratings yet

- FM Crash Course Material 111Document65 pagesFM Crash Course Material 111Safwan Abdul GafoorNo ratings yet

- LiuMeihan PC#4Document4 pagesLiuMeihan PC#4MeihanNo ratings yet

- PMP Rapid Review PDFDocument270 pagesPMP Rapid Review PDFbalakrishnaNo ratings yet

- Building The Business Case For Master Data ManagementDocument18 pagesBuilding The Business Case For Master Data ManagementGeethaChNo ratings yet

- Tai Lieu SCADocument154 pagesTai Lieu SCAsy_binh97No ratings yet

- Chapter4 SPM Project Integration ManagementDocument52 pagesChapter4 SPM Project Integration Managementirapurple03No ratings yet

- Capital Budgeting Techniques Practices in Eastern Bank and IFIC BankDocument44 pagesCapital Budgeting Techniques Practices in Eastern Bank and IFIC BankEdu WriterNo ratings yet

- Managerial ReportDocument31 pagesManagerial ReportQuỳnh QuỳnhNo ratings yet

- Corporate Finance IDocument3 pagesCorporate Finance IAmit PandeyNo ratings yet

- CH 23 Wiley Kimmel Quiz HomeworkDocument5 pagesCH 23 Wiley Kimmel Quiz Homeworkmki100% (3)

- Tutorial 6 SolutionsDocument3 pagesTutorial 6 SolutionsAlexander D'AmoreNo ratings yet

- Determination of Optimal Mining Cut-OffDocument51 pagesDetermination of Optimal Mining Cut-OffRough Bayram KoçNo ratings yet

- P4 Advanced Financial Management SummaryDocument7 pagesP4 Advanced Financial Management SummaryHubert AnipaNo ratings yet

- Theoretical Framework For Business Planning For C2R: How To Write A Business PlanDocument42 pagesTheoretical Framework For Business Planning For C2R: How To Write A Business PlanMuhammad FadhlullahNo ratings yet

- PPAM Final NotesDocument51 pagesPPAM Final NotesShimels ShitayeNo ratings yet

- HolaKola HW Model ProvideDocument4 pagesHolaKola HW Model ProvideslmedcalfeNo ratings yet

- Examinations: 18 April 2000 (Am)Document205 pagesExaminations: 18 April 2000 (Am)Georgess Murithi GitongaNo ratings yet

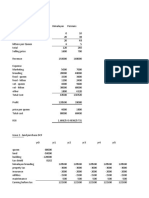

- Hitungan Kuis 6 Bethesda Mining CompanyDocument6 pagesHitungan Kuis 6 Bethesda Mining Companyrica100% (1)

- Chapter 4 Questions V4Document7 pagesChapter 4 Questions V4darrrriaNo ratings yet

- Mas QuestionsDocument10 pagesMas QuestionsHeinie Joy PauleNo ratings yet

- Financial Management - AssignmentDocument18 pagesFinancial Management - AssignmentCarina Ng Ka Ling50% (2)

- System Center Configuration Manager 2012 Business Value White PaperDocument15 pagesSystem Center Configuration Manager 2012 Business Value White PaperRai Kashif JahangirNo ratings yet

- NFJPIA - Mockboard 2011 - MAS PDFDocument7 pagesNFJPIA - Mockboard 2011 - MAS PDFAbigail Faye RoxasNo ratings yet

- Corporate Finance Tutorial 4 - SolutionsDocument22 pagesCorporate Finance Tutorial 4 - Solutionsandy033003No ratings yet

- HandoutDocument14 pagesHandoutJuzer ShabbirNo ratings yet

- FIN2001 Exam - 2021feb - FormoodleDocument7 pagesFIN2001 Exam - 2021feb - Formoodletanren010727No ratings yet

- Investment Decision: Wepix LTDDocument28 pagesInvestment Decision: Wepix LTDZubairia KhanNo ratings yet