Download as ppt, pdf, or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5823)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (898)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (823)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Chapter 1 BowersoxDocument38 pagesChapter 1 Bowersoxssregens82100% (1)

- Lussier 3 Ech 05Document50 pagesLussier 3 Ech 05ssregens82No ratings yet

- Orchestro State Inventory Management 2015Document8 pagesOrchestro State Inventory Management 2015ssregens82No ratings yet

- Building Multi-Tier Web Applications in Virtual EnvironmentsDocument30 pagesBuilding Multi-Tier Web Applications in Virtual Environmentsssregens82No ratings yet

- Risk and Rates of Return: Learning ObjectivesDocument36 pagesRisk and Rates of Return: Learning Objectivesssregens82No ratings yet

- Judicial Power of Supreme CourtDocument2 pagesJudicial Power of Supreme Courtssregens82No ratings yet

- Transportation and Logistics OptimizationDocument18 pagesTransportation and Logistics Optimizationssregens82No ratings yet

- CHP 3Document2 pagesCHP 3ssregens82No ratings yet

- Regular Flow Irregular Flow Irregular Flow DepreciationDocument1 pageRegular Flow Irregular Flow Irregular Flow Depreciationssregens82No ratings yet

- Static Picture Effects For Powerpoint Slides: Reproductio N Instructions Printing Instructions Removing InstructionsDocument17 pagesStatic Picture Effects For Powerpoint Slides: Reproductio N Instructions Printing Instructions Removing Instructionsssregens82No ratings yet

- Supplier General QualificationsDocument3 pagesSupplier General Qualificationsssregens82No ratings yet

- Week 8 AssignmentDocument5 pagesWeek 8 Assignmentssregens82100% (2)

- V Ac - SC V (Aa Ar) - (Sa SR) V (Aa Ar) - (Aa SR) + (Aa SR) - (Sa SR) V ( (Aa Ar) - (Aa SR) ) + ( (Aa SR) - (Sa SR) )Document1 pageV Ac - SC V (Aa Ar) - (Sa SR) V (Aa Ar) - (Aa SR) + (Aa SR) - (Sa SR) V ( (Aa Ar) - (Aa SR) ) + ( (Aa SR) - (Sa SR) )ssregens82No ratings yet

- Problems, Problem Spaces and Search: Dr. Suthikshn KumarDocument47 pagesProblems, Problem Spaces and Search: Dr. Suthikshn Kumarssregens82No ratings yet

- Vcost DemoDocument2 pagesVcost Demossregens82No ratings yet

- AMIS 525 Pop Quiz - Chapters 22 and 23Document5 pagesAMIS 525 Pop Quiz - Chapters 22 and 23ssregens82No ratings yet

- TPRICEDocument1 pageTPRICEssregens82No ratings yet

- Time Value PracticeDocument1 pageTime Value Practicessregens82No ratings yet

- Ri RoiDocument1 pageRi Roissregens82No ratings yet

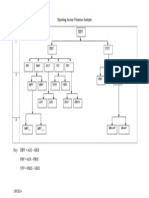

- Operating Income Variances DiagramDocument1 pageOperating Income Variances Diagramssregens82No ratings yet

- Signs For Income VarianceDocument1 pageSigns For Income Variancessregens82No ratings yet

- Percent DoneDocument1 pagePercent Donessregens82No ratings yet

- I (P Q) - (V Q) - F: The Fundamental EquationDocument1 pageI (P Q) - (V Q) - F: The Fundamental Equationssregens82No ratings yet

- Total For 5 Years Each YearDocument1 pageTotal For 5 Years Each Yearssregens82No ratings yet

- Process StepsDocument1 pageProcess Stepsssregens82No ratings yet

- MsmefinanceDocument55 pagesMsmefinanceGauri MittalNo ratings yet

- WCM - Review FinalDocument21 pagesWCM - Review FinalLawrence Scarlett100% (1)

- Working Capital Unit 1 To 4Document103 pagesWorking Capital Unit 1 To 4tarunNo ratings yet

- Borrowers and Lenders ActDocument23 pagesBorrowers and Lenders ActMagnifera IsaacsNo ratings yet

- Internshipprojectreportallahabadbank-170706183254 (1) MMN (6) NMNNJHDocument37 pagesInternshipprojectreportallahabadbank-170706183254 (1) MMN (6) NMNNJHmaheshgutam8756No ratings yet

- Harsh Mini ProjectDocument177 pagesHarsh Mini ProjectHarsh KumarNo ratings yet

- App Form ACEPLDocument18 pagesApp Form ACEPLjayminsuthar76No ratings yet

- Zass-MOA & AOADocument20 pagesZass-MOA & AOAAtiqur SobhanNo ratings yet

- 75766bos61307-P2 Important ThingsDocument26 pages75766bos61307-P2 Important ThingsVishal AgarwalNo ratings yet

- Corporate Finance - Chapter - 19 - Rasha Al-HabalDocument26 pagesCorporate Finance - Chapter - 19 - Rasha Al-Habalrasha mohammedNo ratings yet

- 21 Problems For CB NewDocument31 pages21 Problems For CB NewNguyễn Thảo MyNo ratings yet

- A Presentation On Action StandardDocument40 pagesA Presentation On Action StandardBikash MagarNo ratings yet

- EDE - 22032 - Solved Manual Practical (AICTE)Document61 pagesEDE - 22032 - Solved Manual Practical (AICTE)Snehal SolankeNo ratings yet

- Standby Letter of Credit FacilityDocument7 pagesStandby Letter of Credit FacilityKagimu Clapton ENo ratings yet

- Module 2-Receivables ManagementDocument36 pagesModule 2-Receivables Managementgaurav shettyNo ratings yet

- FIN204 AnswersDocument9 pagesFIN204 Answerssiddhant jainNo ratings yet

- Cibil ReportDocument75 pagesCibil Reportsrinivas rao kNo ratings yet

- Financing Trends in The Rooftop Solar Consumer and Industrial Segment in India September 2021Document34 pagesFinancing Trends in The Rooftop Solar Consumer and Industrial Segment in India September 2021luxymaheshNo ratings yet

- Intermediate Accounting 2 Week 2 Lecture AY 2020-2021 Chapter 2:notes PayableDocument5 pagesIntermediate Accounting 2 Week 2 Lecture AY 2020-2021 Chapter 2:notes PayabledeeznutsNo ratings yet

- VIETTELDocument20 pagesVIETTELSolgrynNo ratings yet

- Schmitz ComplaintDocument11 pagesSchmitz ComplaintChicago TribuneNo ratings yet

- By Phone: To Contact U.S. Bank: P.O. Box 1800 Saint Paul, Minnesota 55101-0800 849 IMG S X ST01Document4 pagesBy Phone: To Contact U.S. Bank: P.O. Box 1800 Saint Paul, Minnesota 55101-0800 849 IMG S X ST01cherry swartzNo ratings yet

- Secrets To Business Credit - Monica MainDocument75 pagesSecrets To Business Credit - Monica MainJawan Starling100% (7)

- CIBIl GDocument38 pagesCIBIl GAlok G ShindeNo ratings yet

- Unit ThreeDocument22 pagesUnit ThreeEYOB AHMEDNo ratings yet

- Mint Delhi 06-02-2023 PDFDocument20 pagesMint Delhi 06-02-2023 PDFubisoft playNo ratings yet

- DBB2104 Unit-14Document23 pagesDBB2104 Unit-14anamikarajendran441998No ratings yet

- Module 2Document20 pagesModule 2FRANZ ERVY D MALLARINo ratings yet

- Corporate FinanceDocument69 pagesCorporate FinancePriyanka RaipancholiaNo ratings yet

- IndiaSales Feb CC SlabsDocument2 pagesIndiaSales Feb CC Slabssocialmedia.manager.incNo ratings yet