Download as ppt, pdf, or txt

You might also like

- Motion To Compel The Defendants To Complete Forms 1Document6 pagesMotion To Compel The Defendants To Complete Forms 1John Carroll100% (1)

- 1 2 PracticeDocument11 pages1 2 PracticecsolutionNo ratings yet

- Fundamentals of Financial Planning - Ronak - HindujaDocument70 pagesFundamentals of Financial Planning - Ronak - HindujaAmrin ChaudharyNo ratings yet

- Quality Database PAN INDIADocument15 pagesQuality Database PAN INDIAJoydeep Sengupta100% (1)

- Employee Benefits: Retirement PlansDocument28 pagesEmployee Benefits: Retirement PlansFaiza OmarNo ratings yet

- Employee Benefits: Retirement PlansDocument28 pagesEmployee Benefits: Retirement Plansbose3508No ratings yet

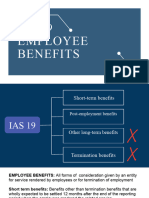

- Employee Benefits Ias19Document42 pagesEmployee Benefits Ias19krishnaguptaNo ratings yet

- Tax Exempt and Government Entities (TE/GE) Employee PlansDocument34 pagesTax Exempt and Government Entities (TE/GE) Employee PlansIRSNo ratings yet

- Compensation Strategies For in Fortune HotelDocument6 pagesCompensation Strategies For in Fortune Hotelgudia2020No ratings yet

- Payroll: Policy and ProceduresDocument5 pagesPayroll: Policy and ProceduresHer Huw100% (1)

- CH 13Document21 pagesCH 13AHMED MOHAMED YUSUFNo ratings yet

- Employer Employee PresentationDocument18 pagesEmployer Employee PresentationAshish MahajanNo ratings yet

- "Income From Salaries" Masters of Commerce (Accountancy)Document30 pages"Income From Salaries" Masters of Commerce (Accountancy)jidnyasaproject100% (1)

- Family SecureDocument8 pagesFamily SecureMärinël VëlmöntëNo ratings yet

- The Employee'S Provident Act1952: Name: Yogesh SinghDocument10 pagesThe Employee'S Provident Act1952: Name: Yogesh Singhyogesh singhNo ratings yet

- Monika Rehman Roll No 10Document19 pagesMonika Rehman Roll No 10Monika RehmanNo ratings yet

- Incentive To WorkDocument4 pagesIncentive To Workapi-249115191No ratings yet

- CHAPTER 11 ACTFADocument41 pagesCHAPTER 11 ACTFACriselda ClemensoNo ratings yet

- UlipDocument7 pagesUlipVinayak BhardwajNo ratings yet

- Pay-for-Performance and Financial Incentives: Lecture OutlineDocument10 pagesPay-for-Performance and Financial Incentives: Lecture Outlineraks_mechnadNo ratings yet

- Instructions of Fill in CashDocument4 pagesInstructions of Fill in CashHayat Ali ShawNo ratings yet

- LN07 Rejda99500X 12 Principles LN07Document28 pagesLN07 Rejda99500X 12 Principles LN07adenhalawehNo ratings yet

- Q2 WordDocument22 pagesQ2 WordNishita DagaNo ratings yet

- Chap 013Document75 pagesChap 013stramieNo ratings yet

- Sept Briefing National Institute For Retirement SecurityDocument37 pagesSept Briefing National Institute For Retirement Securitypcapineri8399No ratings yet

- Choosing: A Retirement SolutionDocument8 pagesChoosing: A Retirement Solutionapi-309082881No ratings yet

- Simplified Employee Pension Plan (SEP) - Internal Revenue ServiceDocument8 pagesSimplified Employee Pension Plan (SEP) - Internal Revenue Serviceabdullahkhanlala03No ratings yet

- Pederson CPA Review FAR Notes PensionDocument8 pagesPederson CPA Review FAR Notes Pensionboen jaymeNo ratings yet

- Edu 2013 10 Ret Plan Exam Case Kuk671xDocument20 pagesEdu 2013 10 Ret Plan Exam Case Kuk671xjusttestitNo ratings yet

- BIG Job ApplicationDocument4 pagesBIG Job ApplicationWilliam GoldingNo ratings yet

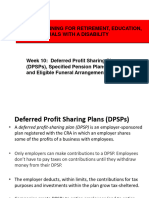

- Week 10 - DPSPs - SPPs - EFAsDocument41 pagesWeek 10 - DPSPs - SPPs - EFAsluxuriousclassic100No ratings yet

- Untitled DocumentDocument285 pagesUntitled DocumentKlancie FreebodyNo ratings yet

- About Your Retirement: Slide 1Document21 pagesAbout Your Retirement: Slide 1IRSNo ratings yet

- Master of Business Administration: Project Report Optimization of Portfolio Risk and ReturnDocument55 pagesMaster of Business Administration: Project Report Optimization of Portfolio Risk and ReturnpiusadrienNo ratings yet

- HRDocument51 pagesHRkaran12110% (1)

- Retirement Planning With Group SuperannuationDocument5 pagesRetirement Planning With Group SuperannuationRutul DaveNo ratings yet

- HR Manual GaganDocument15 pagesHR Manual GaganbaluchakpNo ratings yet

- Pension FundsDocument26 pagesPension Fundschhassan7No ratings yet

- Leave Policy For Different Sectors in IndiaDocument8 pagesLeave Policy For Different Sectors in IndiaRaja SekharNo ratings yet

- IHRM - Chapter 5Document7 pagesIHRM - Chapter 5TauhidZamanNo ratings yet

- Solutions Manual Chapter Eighteen: Answers To Chapter 18 QuestionsDocument5 pagesSolutions Manual Chapter Eighteen: Answers To Chapter 18 QuestionsBiloni KadakiaNo ratings yet

- Mployment Agreement For TeacherDocument7 pagesMployment Agreement For TeacherHazel Ih - BernardinoNo ratings yet

- Benefits and ServicesDocument26 pagesBenefits and ServicesSushmit ShettyNo ratings yet

- Pensions and Other Employee Future BenefitsDocument50 pagesPensions and Other Employee Future BenefitsBic NgoNo ratings yet

- How Is Payroll A HR FunctionsDocument8 pagesHow Is Payroll A HR FunctionsParamita SarkarNo ratings yet

- Employee Rights and Responsibilities Workbook For Apprentices in The Automotive IndustryDocument31 pagesEmployee Rights and Responsibilities Workbook For Apprentices in The Automotive IndustrymajaklipaNo ratings yet

- Employee Benefits PlansDocument9 pagesEmployee Benefits PlansshrikaapntNo ratings yet

- E.Types of Retirement Plans-1Document13 pagesE.Types of Retirement Plans-1Madhu dollyNo ratings yet

- Comp - MNGT .New PracticesDocument22 pagesComp - MNGT .New PracticesMadhura BhadsavleNo ratings yet

- IRS Publication 4333Document12 pagesIRS Publication 4333Francis Wolfgang UrbanNo ratings yet

- Collaboration Business Plan TemplateDocument18 pagesCollaboration Business Plan TemplateThu A. PhamNo ratings yet

- IncentivesDocument31 pagesIncentivessayaliNo ratings yet

- Pension AcgDocument12 pagesPension Acgswicher5No ratings yet

- SM Chapter 01Document36 pagesSM Chapter 01mfawzi010No ratings yet

- HR Resources Sheet Employ MenDocument5 pagesHR Resources Sheet Employ MenMaylene Baquiran CuencoNo ratings yet

- Employee Stock Ownership Plan (ESOP) :: The EmployerDocument1 pageEmployee Stock Ownership Plan (ESOP) :: The EmployerThanu SuthatharanNo ratings yet

- MWP & KeymanDocument11 pagesMWP & KeymanEnnsignn Advisory Services P LtdNo ratings yet

- CH 8 Housing Finance (M.Y.khan)Document22 pagesCH 8 Housing Finance (M.Y.khan)vigneshwarantNo ratings yet

- Uploads/Presentations/184/Mr. M S SureshDocument10 pagesUploads/Presentations/184/Mr. M S Sureshjitu031No ratings yet

- Do-It-Yourself Financial Plans: VeriPlan User Guide - 2023From EverandDo-It-Yourself Financial Plans: VeriPlan User Guide - 2023No ratings yet

- The 401(K) Owner’S Manual: Preparing Participants, Protecting FiduciariesFrom EverandThe 401(K) Owner’S Manual: Preparing Participants, Protecting FiduciariesNo ratings yet

- Education Sector in IndiaDocument3 pagesEducation Sector in IndiaVaibhav P ShahNo ratings yet

- The Ceramics Industry in India Came Into Existence About A Century Ago and HasDocument1 pageThe Ceramics Industry in India Came Into Existence About A Century Ago and HasVaibhav P ShahNo ratings yet

- Behavioral FinanceDocument88 pagesBehavioral FinanceVaibhav P Shah100% (3)

- Highlights of Ceramics IndustryDocument5 pagesHighlights of Ceramics IndustryVaibhav P ShahNo ratings yet

- 02 Uma Steel Rating FinalDocument29 pages02 Uma Steel Rating FinalVaibhav P ShahNo ratings yet

- Eighteen: Portfolio Performance EvaluationDocument31 pagesEighteen: Portfolio Performance EvaluationVaibhav P ShahNo ratings yet

- Return On Investment: Methods To MaximizeDocument22 pagesReturn On Investment: Methods To MaximizeVaibhav P ShahNo ratings yet

- MBA BooksDocument654 pagesMBA BooksBhavesh Jha50% (4)

- A Project On Brand Repositioning Strategy of Titan WatchesDocument62 pagesA Project On Brand Repositioning Strategy of Titan WatchesAnuranjanSinha50% (2)

- 00 FormalitiesDocument6 pages00 FormalitiesVaibhav P ShahNo ratings yet

- 1237 Marketings 4 Ps GuideDocument21 pages1237 Marketings 4 Ps GuideVaibhav P ShahNo ratings yet

- Department of Human Services Seniors and People With Disabilities Division Oregon Administrative Rules Division 34 Personal Care ServicesDocument20 pagesDepartment of Human Services Seniors and People With Disabilities Division Oregon Administrative Rules Division 34 Personal Care ServicesVaibhav P ShahNo ratings yet

- Ratio AnalysisDocument17 pagesRatio AnalysisPGNo ratings yet

- Com BankDocument25 pagesCom BankAnonymous y3E7iaNo ratings yet

- Optimal Capital StructureDocument13 pagesOptimal Capital StructureScarlet SalongaNo ratings yet

- Pdic Frequently Ask QuestionsDocument3 pagesPdic Frequently Ask QuestionsColleen Rose GuanteroNo ratings yet

- Tutorial 12 Forward & FuturesDocument2 pagesTutorial 12 Forward & FuturesHenry Ng Yong KangNo ratings yet

- Xi Annual NewDocument5 pagesXi Annual NewPragadeshwar KarthikeyanNo ratings yet

- Income StatementDocument7 pagesIncome StatementVALENCIA TORENTHANo ratings yet

- Fundamentals of Corporate Finance Canadian 6th Edition Brealey Solutions Manual 1Document36 pagesFundamentals of Corporate Finance Canadian 6th Edition Brealey Solutions Manual 1jillhernandezqortfpmndz100% (34)

- 1Document60 pages1alicewilliams83nNo ratings yet

- Viva On Project and CfsDocument7 pagesViva On Project and CfsCrazy GamerNo ratings yet

- Money: Unit of ExchangeDocument2 pagesMoney: Unit of ExchangeElla PlacidoNo ratings yet

- BPI Family Savings V AvenidoDocument10 pagesBPI Family Savings V AvenidoBrian TomasNo ratings yet

- Trial Essay Questions V3 DoneDocument5 pagesTrial Essay Questions V3 DoneNguyễn Huỳnh ĐứcNo ratings yet

- Central Azucarera de Don Pedro V CTADocument3 pagesCentral Azucarera de Don Pedro V CTAChino Sison100% (1)

- Revolutionary Perspectives 21Document55 pagesRevolutionary Perspectives 21HegelNo ratings yet

- Meeting 2 - Accounting PrincipleDocument3 pagesMeeting 2 - Accounting PrinciplenisaNo ratings yet

- Tax Planning Tips For Property Investors Financial Year EndDocument1 pageTax Planning Tips For Property Investors Financial Year EndAdrianNo ratings yet

- Fundamentals of Accountancy, Business and Management 1: Teddy B. GanDocument25 pagesFundamentals of Accountancy, Business and Management 1: Teddy B. GanWindelyn IliganNo ratings yet

- Guideline For A Business Plan For A Sawmilling Enterprise - Final - 0 - 0Document10 pagesGuideline For A Business Plan For A Sawmilling Enterprise - Final - 0 - 0scrivener white mulubwa jrNo ratings yet

- Auto Secure - Private Car Package Policy: Sincerely, For Tata AIG General Insurance Company LimitedDocument4 pagesAuto Secure - Private Car Package Policy: Sincerely, For Tata AIG General Insurance Company Limitedismail02984No ratings yet

- Portfoliopython: 1 Week 1 Section 1 - Fundamentals of Risk and ReturnsDocument23 pagesPortfoliopython: 1 Week 1 Section 1 - Fundamentals of Risk and ReturnsHoda El HALABINo ratings yet

- Project Report On Punjab National Bank AakashDocument68 pagesProject Report On Punjab National Bank Aakashaakash_saxena8235356681% (16)

- Seminar 1 - QsDocument2 pagesSeminar 1 - QsMaman AbdurrahmanNo ratings yet

- Q & A - Insurance Act, 1938 (Scanner)Document5 pagesQ & A - Insurance Act, 1938 (Scanner)Rohit GargNo ratings yet

- Theoretical Foundations For Quantitative Finance 9813202475 9789813202474 - CompressDocument222 pagesTheoretical Foundations For Quantitative Finance 9813202475 9789813202474 - CompressLynaNo ratings yet

- Powers & Authority of The Commissioner of Internal Revenue Under Sec. 4-7, Title 1 of The Tax CodeDocument24 pagesPowers & Authority of The Commissioner of Internal Revenue Under Sec. 4-7, Title 1 of The Tax CodeRovi PatinoNo ratings yet

- Form PDF 197504840210823Document9 pagesForm PDF 197504840210823jassramgarhia2812No ratings yet