Download as pptx, pdf, or txt

ITTI `S

EGG WHOLESALER AND RETAILER

STORE

BREAK - EVEN POINT

ANALYSIS:

LINEAR fUNCTIONS

BREAK EVEN POINT

(BEP)

the simplest quantitative model

used by decision makers which

concerned the interrelationship of

cost, volume and profit

common point between the total

revenue and total cost

total revenue equals the total cost

the company has no profit but has

no loss also

also referred to as Cost

Volume Analysis

is the determination of the

number of units that must be

produced and add to equate sale

with total cost

the point at which your product

stops costing you money to

produce and sell, and starts to

generate a profit for your

company.

BREAK-EVEN ANALYSIS DEPENDS

ON THE FOLLOWING VARIABLES:

Selling price per Unit

Total Fixed Cost

Variable Unit Cost

Forecasted Net Profit

SELLING PRICE PER UNIT

The amount of money charged to the customer

for each unit of a product or service.

TOTAL FIXED COST

constant expenditures without regards to the

number of units produced like: rent expense,

depreciation expense, factory supervisory

salary. The sum of all costs required to

produce the first unit of a product. This amount

does not vary as production increases or

decreases, until new capital expenditures are

needed

VARIABLE COST

Variable Unit Cost

Costs that vary directly with the production of

one additional unit. Examples of this are

utilities, wages, raw materials, and packaging.

Total Variable Cost

The product of expected unit sales and variable

unit cost, i.e., expected unit sales times the

variable unit cost.

COMBINATION COST

costs that are a combination of fixed and variable: a

certain minimum level will be incurred regardless of

your sales levels, but the costs rise as your volume

increases. (ex. phone bill)

Strictly speaking, these costs should be separated

into their fixed and variable components, but that

may be more trouble than it's worth for a small

business. To simplify things, just decide which type

of cost (fixed or variable) is the most important for

the particular item, and then classify the whole item

according to the more important characteristic. For

example, in a telemarketing business, if your phone

call volume charges are normally greater than your

line access charges, you'd classify the entire bill as

variable.

FORECASTED NET PROFIT

Total revenue minus total cost

Total Revenue (TR)

the product of the selling price per unit and

number of units sold

Total Cost (TC)

sum of fixed cost (FC) and variable cost (VC)

COMPONENT OF BREAK EVEN ANALYSIS

1. Volume

level of production by a company, which is

expressed as the number of units (quantity)

produced and sold

2. Profit

the difference between total Sales and total cost

or the income generated by the sale of product

3. Costs

usual expenditures that must be taken into

account in order to determine profit

FORMULA

TR = Price per unit x units sold

TC = FC + VC

Profit = TR TC

TR = TC OR TR TC = 0 ,

* Profit = 0 at break even point

BEP GRAPH

MARKET EQUILIBRIUM GRAPH

EXERCISES

1. Consider a firm that buys units for Php 10.00 and sells

them for Php 15.00. There are no other variable cost.

Fixed costs are at Php 6000, Use the break-even formula

to determine the following:

a) TR, TC and profit functions

b) Sales volume when profit is Php 8000

c) Profit when sales are 500 units

d) The break-even quantity and revenue

e) The amount by which the variable cost per unit has to be

decreased in order to break even at 500 units. (selling

price and FC remains)

f) The new fixed cost in order to break even at 800 units.

Selling price cost remains constant.

g) The new selling price per unit, to break even at 500 units,

if VC and TC are constant.

Given:

Variable Cost = 10 per unit

Selling price = 15 per unit

Fixed Cost = 6000

a. TR = 15x

TC = 10x + 6000

Profit = 15x (10x +

6000)

= 15x 10x

6000

Profit = 5x 6000

b. Profit = 8000

Profit = 5x 6000

8000 = 5x 6000

-5x = -6000 8000

-5x/-5 = -14000/-5

x = 2800 units

c.

x = 500

Profit = 5 (500) 6000

= 2500 6000

= Php 3500 loss

d. TR = TC

15x = 10x + 6000

15x-10x = 6000

5x/5 = 6000/5

x = 1200 units (BEP

Quantity)

TR = 15x

= 15 (1200)

TR = Php 18000 BEP

revenue

e. Let y = new variable

cost

VC = 500y

Original TC = 10x +

6000

New TC = 500y + 6000

TR = TC

15 (500) = 500y + 6000

7500 = 500y + 6000

-500y = 6000 7500

-500y/-500 = -1500/-500

y = 3 new variable cost

per unit

*Since the old VC is 10

per unit and the new

VC is 3 so it

decreases 7 per unit

f. Given:

BEP quantity = 800

let z = fixed cost

TR = TC

15 (800) = 10 (800) + z

-z/-1 = (8000-12000)/-1

z = 4000 fixed cost

or

TC = TR

10 (800) + z = 15 (800)

8000 + z = 12000

z = 12000 8000

z = 4000

g. Given:

BEP quantity = 500 unit

Let p = selling price

TR = TC

500p = 10 (500) + 6000

500p/500 = 11000/500

p = Php 22.00 selling price per unit

EXERCISES

2. A business firm produces and sells a particular product.

Variable cost is Php 30.00 per unit. Selling price is Php

40.00 per unit. Fixed cost is Php 60000. Determine the

following:

a) Profit when sales are 10000 units.

b) The break-even point quantity and revenue.

c) Sales when profits are at Php 9000.

d) The amount by which fixed cost will have to be decreased

or increased, to allow the firm to break even at sales

volume of 500 units. VC and selling price per unit remain

constant.

e) The volume of sales to cover the fixed cost.

f) Suppose that the firm wants to break even at a lower

number of units, assuming that FC and VC remain

constant, how is the selling price affected?

g) Find the TC when sales are 500 units.

Given:

VC = Php 30.00 per unit

SP = Php 40.00 per unit

TC = Php 60000

a. x = 10000 units

Profit = 10x 60000

= 10 (10000) 60000

Profit = 40000

Functions:

TC = 30x + 60000

TR = 40x

Profit = 40x (30x + 60000)

= 40x 30x 60000

Profit = 10x 60000

b.

TR = TC

40x = 30x +

60000

10x/10 = 60000/10

x = 6000

(BEP

quantity )

TR = 40 (6000)

TR = Php 240000

BEP revenue

c.

Given:

Profit = 9000

Profit = 10x 60000

9000 = 10x 60000

-10x = -60000 9000

-10x/-10 = -69000/-10

x = 6900 units sold

TR = 40 (6900)

TR = 276000 for

6900 units sold

d. Given: BEP quantity = 500 units

Let y= fixed cost

Solution: TC=TR

30(500) + y = 40(500)

15000 + y = 20000

y = 20000 - 15000

y = 5000 new fixed cost.

*Since the old FC is 60000,and the new FC is 5000

so there is a decrease of 55000.

e. TR=FC

40x = 60000

40x/40 = 60000/40

x = 1500 units of

sale to cover the

fixed cost

f. If the firm wants

to break even at a

lower number of

units, but the FC

and VC remain

constant. The

selling price

should be

increased.

TR = TC

SP x X = FC + VC

3. A factory sells a particular product at Php 0.80 per

unit. The variable cost is Php 0.60 per unit. The

total fixed cost is Php 12000. Determine the

following:

a) The break-even point in units of sales.

b) Profit when sales are 10000 units.

c) TC when sales are 5000 units.

d) The amount by which the selling price will have to

increase or decrease for the firm to break even at

4000 units. Assume all costs remain the constant.

e) The amount by which the fixed cost will have to

decrease in order for the firm to break even at a

sales volume of 4000 units. Assume selling price

and variable cost remain the same.

Given:

SP = Php .80 per unit

VC = Php .60 per unit

FC = Php 12000

A. BEP

TR = TC

.80x = .60x + 12000

.80x - .60x = 12000

.20x/.20 = 12000/.20

x = 60000 BEP

quantity

TR = .80x

= .80 (60000)

TR = 48000 BEP

revenue

b.

Given: Unit sold

10000

Profit = .20x - 12000

= .20 (10000) -

12000

= 10000 loss

c.

Given: Unit sold 5000

TC = .60x + 12000

= .60(5000) + 12000

TC = 15000

d.

Given: BEP quantity = 4000

let S = selling price

TR = TC

4000S = .60(4000) + 12000

4000S = 2400 + 12000

4000S/4000 = 14400/4000

S = 3.60 new selling price to break even of 4000

e.

Given: BEP quantity = 4000 units

let z = fixed cost

TC = TR

.60x + z = .80x

.60(4000) + z = .80(4000)

2400 + z = 3200

z = 3200 - 2400

z = 800 new fixed cost to break

even of 4000 units

* Since the old FC is

12000,therefore there

should be a decrease

of 11200 to have a

break even quantity of

4000.

4. A manufacturer sells his product at Php 10.00

per unit.

a) Find the total revenue if the volume sales is

1800.

b) If fixed cost is Php 3000, represent the total cost

when the variable cost per unit is Php 5.00

c) Supposed that the variable cost per unit is 70%

of the selling price. Represent the total cost

when fixed cost is Php 5000.

d) If variable cost is 20% of the selling price and

the fixed cost is Php 1000, find the break-even

point.

Given: SP = Php 10

per unit

Solution:

a. Given: Unit Sold =

1800

Solution:

TR = 10x

= 10 (1800)

= 18000

b. Given: FC = 3000

VC = 5 per

unit

Solution:

TC = 5x + 3000

c.

Given: FC = 5000

VC = 70% of SP

= 70% (10)

= 7

Solution:

TC = 7x + 5000

d. Given: VC = 20% of SP

= 20% (10)

= 2 per unit

FC = 1000

Solution:

TR = TC

10x = 2x + 1000

10x - 2x = 1000

8x/8 = 1000/8

x = 125

TR = 10x

= 10 (125)

= 1250 BEP revenue

if BEP quantity of 125

where VC is 20% of

SP and FC is

equal to 1000

You might also like

- Tenancy Agreement (Kamal Carwash)Document3 pagesTenancy Agreement (Kamal Carwash)Syed Isamil75% (8)

- Budgeting ExercisesDocument3 pagesBudgeting ExercisesMaan Caboles100% (1)

- CVP Practice Exercises 3MA3 Part 2Document14 pagesCVP Practice Exercises 3MA3 Part 2Jyrus Cimatu100% (1)

- Do Not Send Anything To Austin TX 73301-0215 - This Is A Sorting OfficeDocument11 pagesDo Not Send Anything To Austin TX 73301-0215 - This Is A Sorting Officenaturalvibes94% (17)

- Cost Acc G4 2Document6 pagesCost Acc G4 2Asdfghjkl LkjhgfdsaNo ratings yet

- Exercises - Job Order CostingDocument7 pagesExercises - Job Order CostingJericho DupayaNo ratings yet

- Mas Second PB 03-11Document12 pagesMas Second PB 03-11Kim Cristian MaañoNo ratings yet

- Chapter 6 Man SciDocument8 pagesChapter 6 Man SciRits MonteNo ratings yet

- Cost-Volume Profit AnalysisDocument26 pagesCost-Volume Profit AnalysisClarizza20% (5)

- Case NO 3 - Mismatch Comp.Document5 pagesCase NO 3 - Mismatch Comp.abegail soquinaNo ratings yet

- Break-Even QuizDocument8 pagesBreak-Even QuizEricka Guisando0% (2)

- Differential Cost Analysis Part 1Document11 pagesDifferential Cost Analysis Part 1ABStract001No ratings yet

- Qmethods Notes1Document13 pagesQmethods Notes1Ermily Frances Derecho0% (1)

- 148-M-S-M-C (34) 5847Document2 pages148-M-S-M-C (34) 5847Ahmed AwaisNo ratings yet

- Handout ManAcc2 PDFDocument16 pagesHandout ManAcc2 PDFmobylay0% (1)

- Notes in CostDocument2 pagesNotes in CostKristine PerezNo ratings yet

- Week 2 Assignment SolutionDocument2 pagesWeek 2 Assignment Solutiontucker jacobsNo ratings yet

- 222Document3 pages222Carlo ParasNo ratings yet

- Republic of The Philippines Court of Tax Appeals Quezon: DecisionDocument10 pagesRepublic of The Philippines Court of Tax Appeals Quezon: DecisionPGIN Legal OfficeNo ratings yet

- Maranan, A2A - Break Even Point AnalysisDocument6 pagesMaranan, A2A - Break Even Point AnalysisJere Mae Maranan100% (1)

- Break Even AnalysisDocument9 pagesBreak Even AnalysisRoselle Manlapaz LorenzoNo ratings yet

- Lesson 3 Cost Volume Profit AnalysisDocument7 pagesLesson 3 Cost Volume Profit AnalysisklipordNo ratings yet

- Module 7 - AE4 - Break Even AnalysisDocument30 pagesModule 7 - AE4 - Break Even AnalysisJan Luis Ramiro100% (1)

- INTRODUCTION TOnLINEAR PROGRAMMINGDocument9 pagesINTRODUCTION TOnLINEAR PROGRAMMINGPrincess Amber0% (2)

- CHAPTER 4: Differential Cost Analysis (Relevant Costing) KaebDocument6 pagesCHAPTER 4: Differential Cost Analysis (Relevant Costing) KaebMark Gelo WinchesterNo ratings yet

- Bsa 2 - Finman - Group 8 - Lesson 4Document6 pagesBsa 2 - Finman - Group 8 - Lesson 4Allyson Charissa AnsayNo ratings yet

- G Quantitative-Techniques Final-Presentation PDFDocument62 pagesG Quantitative-Techniques Final-Presentation PDFSteffanie GranadaNo ratings yet

- Chapter 7 - Accounting For Joint and by ProductsDocument8 pagesChapter 7 - Accounting For Joint and by ProductsJoey LazarteNo ratings yet

- Cost Volume Profit AnalysisDocument18 pagesCost Volume Profit AnalysisLea GaacNo ratings yet

- Linear Programming - ProblemsDocument2 pagesLinear Programming - ProblemsZeus Olympus50% (2)

- Quantitative TechniquesDocument4 pagesQuantitative Techniquesshamel marohom100% (2)

- Final Examination Problem Solving (Ae 106)Document4 pagesFinal Examination Problem Solving (Ae 106)Robin Chris KapaliNo ratings yet

- Joint, Standard, ABCDocument10 pagesJoint, Standard, ABCXairah Kriselle de Ocampo50% (2)

- CA4 Just in Time and Backlush AccountingDocument9 pagesCA4 Just in Time and Backlush AccountinghellokittysaranghaeNo ratings yet

- Baggayao WACC PDFDocument7 pagesBaggayao WACC PDFMark John Ortile BrusasNo ratings yet

- Working Capital CashDocument6 pagesWorking Capital CashNiña Rhocel YangcoNo ratings yet

- Quiz On Relevant CostingDocument6 pagesQuiz On Relevant CostingRodolfo ManalacNo ratings yet

- Break-Even Analysis and ForecastingDocument50 pagesBreak-Even Analysis and ForecastingBabyNicoleArellano50% (2)

- SpoilageDocument17 pagesSpoilageBhawin DondaNo ratings yet

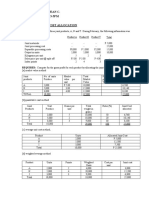

- Alvaro, Fernel Jean C. AE212-1741 TTHS 3-5PM Exercise 8-2. Joint Cost AllocationDocument4 pagesAlvaro, Fernel Jean C. AE212-1741 TTHS 3-5PM Exercise 8-2. Joint Cost AllocationNhel AlvaroNo ratings yet

- Acctg 13 - Midterm ExamDocument8 pagesAcctg 13 - Midterm ExamMary Grace Castillo AlmonedaNo ratings yet

- Cost-Volume-Profit Analysis Problems: CalculateDocument3 pagesCost-Volume-Profit Analysis Problems: CalculateAsma Hatam100% (6)

- MAS1Document46 pagesMAS1Frances Bernadette BaylosisNo ratings yet

- Multi-Product Break-Even Point Formula: Margin and Weighted Average Contribution Margin Ratio Are UsedDocument2 pagesMulti-Product Break-Even Point Formula: Margin and Weighted Average Contribution Margin Ratio Are UsedSayadi AdiihNo ratings yet

- AE 114 MidtermDocument7 pagesAE 114 MidtermMa Angelica BalatucanNo ratings yet

- Cost Accounting - QuizDocument5 pagesCost Accounting - QuizAnna Mae SanchezNo ratings yet

- Cost Accounting Quizzer No. 1: Basic ConceptsDocument11 pagesCost Accounting Quizzer No. 1: Basic ConceptsLuming100% (1)

- Fifo Costing Problems - Even and UnevenDocument3 pagesFifo Costing Problems - Even and UnevenDarra MatienzoNo ratings yet

- TB Addatu - Standard Costs and Variable AnalysisDocument15 pagesTB Addatu - Standard Costs and Variable AnalysisJean Fajardo Badillo0% (3)

- CORRECTION OF ERRORS Theories PDFDocument7 pagesCORRECTION OF ERRORS Theories PDFJoy Miraflor AlinoodNo ratings yet

- Chapter 16 Managing Productivity and Marketing EffectivenessDocument30 pagesChapter 16 Managing Productivity and Marketing EffectivenessHerrah Joyce Salinas100% (1)

- Assignment 4 - CVPDocument12 pagesAssignment 4 - CVPAlyssa BasilioNo ratings yet

- Ch04 Cost Volume Profit AnalysisDocument21 pagesCh04 Cost Volume Profit AnalysisYee Sook Ying0% (1)

- Cost Accounting and ManagementDocument7 pagesCost Accounting and ManagementCris Tarrazona CasipleNo ratings yet

- Absorption and Variable Costing Reviewer EphDocument4 pagesAbsorption and Variable Costing Reviewer Ephephraim100% (1)

- Lesson 1-Relevant Cost Analysis-Strategic Cost Management-Sisc-Ay 2020-2021-Second Sem-Jason I. Trinidad, CpaDocument13 pagesLesson 1-Relevant Cost Analysis-Strategic Cost Management-Sisc-Ay 2020-2021-Second Sem-Jason I. Trinidad, CpaAira Jaimee Gonzales100% (1)

- AP DLSA 05 PPE For DistributionDocument10 pagesAP DLSA 05 PPE For DistributionStela Marie CarandangNo ratings yet

- CH 5 - 1Document25 pagesCH 5 - 1api-251535767No ratings yet

- Biological AssetsDocument15 pagesBiological AssetsEliseNo ratings yet

- Cost Accounting & Cost Management Preliminary ExaminationDocument4 pagesCost Accounting & Cost Management Preliminary ExaminationClaire BarbaNo ratings yet

- 8 Economic GoalsDocument2 pages8 Economic GoalsNikki Banga100% (4)

- Module 4 Math in The Modern WorldDocument11 pagesModule 4 Math in The Modern WorldJerusa May CabinganNo ratings yet

- Management Science Module 8 - Break - Even Point AnalysisDocument7 pagesManagement Science Module 8 - Break - Even Point AnalysisMaria G. BernardinoNo ratings yet

- Food Menu: The Way To Good Body DietDocument12 pagesFood Menu: The Way To Good Body DietKelly NgNo ratings yet

- MannitolDocument1 pageMannitolKelly NgNo ratings yet

- ERF RequirementsDocument1 pageERF RequirementsKelly NgNo ratings yet

- Accounting For Income TaxDocument26 pagesAccounting For Income TaxKelly Ng67% (6)

- What Is Governance PDFDocument3 pagesWhat Is Governance PDFamirq4No ratings yet

- Lesson 15, Week 15: Auditing Payroll: TopicsDocument5 pagesLesson 15, Week 15: Auditing Payroll: TopicsChrista LenzNo ratings yet

- PSAK 10 Pengaruh Perubahan Kurs Valuta AsingDocument1 pagePSAK 10 Pengaruh Perubahan Kurs Valuta AsingWahyuniiNo ratings yet

- SSPCNADVDocument1 pageSSPCNADVearlcorrNo ratings yet

- Fundamentals of Accounting 1Document241 pagesFundamentals of Accounting 1kedge100% (2)

- Deductions On Gross EstateDocument5 pagesDeductions On Gross EstatefcnrrsNo ratings yet

- Finance Submission 02Document58 pagesFinance Submission 02prathamgharat019No ratings yet

- Intermediate Accounting Reporting and Analysis 1st Edition Wahlen Solutions Manual 1Document131 pagesIntermediate Accounting Reporting and Analysis 1st Edition Wahlen Solutions Manual 1willie100% (45)

- According To Section 44AA and Rule 6F of The Income Tax ActDocument2 pagesAccording To Section 44AA and Rule 6F of The Income Tax ActAmruta SharmaNo ratings yet

- Financial Analysiss IiDocument40 pagesFinancial Analysiss IiChe Omar100% (3)

- 4 Ratio, Proportion, and VariationDocument34 pages4 Ratio, Proportion, and VariationBoom Box100% (2)

- Nature and Types of Capital BudgetingDocument5 pagesNature and Types of Capital Budgetingnagendra6391No ratings yet

- BST Science and Technology Trust Factsheet Us09258g1040 Us en IndividualDocument3 pagesBST Science and Technology Trust Factsheet Us09258g1040 Us en IndividualJustin YeoNo ratings yet

- Income Tax Act 1961Document55 pagesIncome Tax Act 1961geeta100% (1)

- Costacc Testbank - WDocument44 pagesCostacc Testbank - WKristian Paolo De LunaNo ratings yet

- Manatad - Accounting 14NDocument5 pagesManatad - Accounting 14NJullie Carmelle ChattoNo ratings yet

- Product Life Cycle of KelvinatorDocument21 pagesProduct Life Cycle of Kelvinatorankit talujaNo ratings yet

- Organization Study At: AMC PVT LTDDocument15 pagesOrganization Study At: AMC PVT LTDRAGHU M SNo ratings yet

- Networth - Certificate For IDBIDocument4 pagesNetworth - Certificate For IDBISandip DasNo ratings yet

- Business and Transfer Taxation: TO Consumption TaxesDocument40 pagesBusiness and Transfer Taxation: TO Consumption TaxesKC GutierrezNo ratings yet

- Financial Accounting - WikipediaDocument21 pagesFinancial Accounting - Wikipediagurubks15No ratings yet

- Financial Management Model Question PaperDocument2 pagesFinancial Management Model Question PaperdvraoNo ratings yet

- M14 Gitman50803X 14 MF AC14Document70 pagesM14 Gitman50803X 14 MF AC14Joan Marie100% (2)

- Tally-Erp .9: S.No Topics 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29Document6 pagesTally-Erp .9: S.No Topics 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29ATS PROJECT DEPARTMENTNo ratings yet

- ANSWERS TO EXERCISES 4 TH Edition Cost B PDFDocument81 pagesANSWERS TO EXERCISES 4 TH Edition Cost B PDFAnnNo ratings yet

- 1 Modigliani MillerDocument3 pages1 Modigliani MillerVincenzo CassoneNo ratings yet

- Ch09-Advance Accounting-Mutual HoldingDocument50 pagesCh09-Advance Accounting-Mutual Holdingmichel00yesNo ratings yet

- Financial Management - NotesDocument39 pagesFinancial Management - NotesdollyguptaNo ratings yet