Download as ppt, pdf, or txt

You might also like

- Assignment 4 Capital Budgeting and COCDocument3 pagesAssignment 4 Capital Budgeting and COCQurat Saboor100% (1)

- Dynamics NAV IFRSDocument32 pagesDynamics NAV IFRSGeorge Baciu50% (2)

- Financial Accounting Theory Craig Deegan Chapter 2Document34 pagesFinancial Accounting Theory Craig Deegan Chapter 2Siti AdawiyahNo ratings yet

- The Afn FormulaDocument1 pageThe Afn Formulasplendidhcc100% (2)

- Analysis and Interpretation of FS-Part 1Document2 pagesAnalysis and Interpretation of FS-Part 1Rhea RamirezNo ratings yet

- BSBFIM601 Student AssessmentDocument15 pagesBSBFIM601 Student AssessmentSaru Koduru33% (6)

- Merger and AcquisitionDocument49 pagesMerger and AcquisitionVivek Singh0% (1)

- Master Budget and ResponisbiltiyDocument68 pagesMaster Budget and ResponisbiltiyTekaling Negash100% (1)

- Management Accounting & Business EnvironmentDocument26 pagesManagement Accounting & Business Environmentemon100% (1)

- Role of Financial Management in OrganizationDocument8 pagesRole of Financial Management in OrganizationTasbeha SalehjeeNo ratings yet

- CH 12Document63 pagesCH 12Grace VersoniNo ratings yet

- Financial Performance Measures - Ch10 - SDocument32 pagesFinancial Performance Measures - Ch10 - SLok Fung KanNo ratings yet

- Ch12 Planning For Capital InvestmentsDocument62 pagesCh12 Planning For Capital Investmentsعبدالله ماجد المطارنهNo ratings yet

- An Empirical Study of The Effectiveness of Internal Control and Influencing FactorsDocument7 pagesAn Empirical Study of The Effectiveness of Internal Control and Influencing FactorsDedi PramonoNo ratings yet

- InventoryDocument45 pagesInventoryjoyabyssNo ratings yet

- Budgeting As A Mechanism For Management Planning and ControlDocument50 pagesBudgeting As A Mechanism For Management Planning and ControlMatthewOdaliNo ratings yet

- The Balanced Scorecard: A Tool To Implement StrategyDocument39 pagesThe Balanced Scorecard: A Tool To Implement StrategyAilene QuintoNo ratings yet

- 06-Earnings-Per-Share Practice Problems Faisal & CODocument10 pages06-Earnings-Per-Share Practice Problems Faisal & COsyed asim shahNo ratings yet

- Forecasting Financial StatementsDocument58 pagesForecasting Financial StatementsEman KhalilNo ratings yet

- Chapter 5 Marginal CostingDocument36 pagesChapter 5 Marginal CostingSuku Thomas SamuelNo ratings yet

- Cost VarianceDocument20 pagesCost VarianceMukesh ManwaniNo ratings yet

- Chapter 10-Standard Costing: A Managerial Control Tool: True/FalseDocument66 pagesChapter 10-Standard Costing: A Managerial Control Tool: True/FalseClarisse AlimotNo ratings yet

- Hilton 11e Chap001 PPT-STU PDFDocument41 pagesHilton 11e Chap001 PPT-STU PDFKhánh Linh CaoNo ratings yet

- Flexible Budget and Performance AnalysisDocument22 pagesFlexible Budget and Performance AnalysisttzaxsanNo ratings yet

- Chapter 13 Financial Statement Analysis SolutionsDocument3 pagesChapter 13 Financial Statement Analysis Solutionsbhardwajvn100% (3)

- Acctg233 Investment Centers and Transfer PricingDocument5 pagesAcctg233 Investment Centers and Transfer PricingNino Joycelee TuboNo ratings yet

- Chapter 7 Asset Investment Decisions and Capital RationingDocument31 pagesChapter 7 Asset Investment Decisions and Capital RationingdperepolkinNo ratings yet

- Pepsi and Coke Financial ManagementDocument11 pagesPepsi and Coke Financial ManagementNazish Sohail100% (1)

- p23 Case 1-3 Baron CoburgDocument7 pagesp23 Case 1-3 Baron Coburgrajo_onglao100% (2)

- Chapter 13 Relevant Costs For Decision Making: True/False QuestionsDocument140 pagesChapter 13 Relevant Costs For Decision Making: True/False QuestionsexgayssNo ratings yet

- Chapter 15Document12 pagesChapter 15Zack ChongNo ratings yet

- Session 17 Inventory Management EOQ OM 2019 ProblemsDocument13 pagesSession 17 Inventory Management EOQ OM 2019 Problemsashish sunnyNo ratings yet

- 20180308012211are Farms Becomin Digital FirmsDocument4 pages20180308012211are Farms Becomin Digital Firmsnguyễn hoaNo ratings yet

- Cash Flow Statement InterpertationsDocument6 pagesCash Flow Statement InterpertationsMansoor FayyazNo ratings yet

- Decentralization and Segment ReportingDocument3 pagesDecentralization and Segment ReportingYousuf SoortyNo ratings yet

- Relevant Costs 4Document6 pagesRelevant Costs 4Franklin Evan PerezNo ratings yet

- Chapter 16 Budgeting Capital Expenditures Research and Development Expenditures and Cash Pert Cost The Flexible BudgetDocument17 pagesChapter 16 Budgeting Capital Expenditures Research and Development Expenditures and Cash Pert Cost The Flexible BudgetZunaira ButtNo ratings yet

- Gitman CH 14 15 QnsDocument3 pagesGitman CH 14 15 QnsFrancisCop100% (1)

- Corporate Reporting-1Document69 pagesCorporate Reporting-1Najmul IslamNo ratings yet

- Ten Axioms, Principles in FinanceDocument14 pagesTen Axioms, Principles in FinancePierreNo ratings yet

- Chap 11 - Equity Analysis and ValuationDocument26 pagesChap 11 - Equity Analysis and ValuationWindyee TanNo ratings yet

- Solution Manual12Document65 pagesSolution Manual12sandeep_41633% (3)

- Mployee Stakeholders and Workplace IssuesDocument25 pagesMployee Stakeholders and Workplace IssuesAlexander Agung HRDNo ratings yet

- Question Bank - Practical QuestionsDocument10 pagesQuestion Bank - Practical QuestionsNeel KapoorNo ratings yet

- Chapter 9 - Profit PlanningDocument28 pagesChapter 9 - Profit PlanningEnrique Miguel Gonzalez Collado0% (1)

- MBA 504 Ch11 SolutionsDocument31 pagesMBA 504 Ch11 Solutionschawlavishnu100% (1)

- Question and Answer - 60Document31 pagesQuestion and Answer - 60acc-expertNo ratings yet

- Straight ProblemsDocument1 pageStraight ProblemsMaybelle100% (1)

- Managerial Accounting 8th Edition: Chapter 11 SolutionsDocument25 pagesManagerial Accounting 8th Edition: Chapter 11 SolutionsMarielle Tamayo100% (1)

- Regulatory Framework of AuditingDocument18 pagesRegulatory Framework of AuditingSohaib BilalNo ratings yet

- Chapter 17 Financial Planning and ForecastingDocument39 pagesChapter 17 Financial Planning and ForecastingYu BabylanNo ratings yet

- Decentralization of Operation and Segment Reporting: Organizational StructureDocument7 pagesDecentralization of Operation and Segment Reporting: Organizational StructureMon RamNo ratings yet

- Preparation of Master BudgetDocument43 pagesPreparation of Master Budgetsaran_16100% (1)

- Dupont AnalysisDocument5 pagesDupont AnalysisNoraminah IsmailNo ratings yet

- Ch19 Guan Hansen MowenDocument38 pagesCh19 Guan Hansen MowenratuhsNo ratings yet

- Capital BudgetingDocument19 pagesCapital BudgetingJane Masigan50% (2)

- Basics of Capital BudgetingDocument26 pagesBasics of Capital BudgetingChaitanya JagarlapudiNo ratings yet

- 5 - Capital Budgeting - Risk & UncertaintyDocument22 pages5 - Capital Budgeting - Risk & UncertaintySymron KheraNo ratings yet

- Detecting Earning ManagementDocument34 pagesDetecting Earning ManagementAlmizan AbadiNo ratings yet

- I Practice of Horizontal & Verticle Analysis Activity IDocument3 pagesI Practice of Horizontal & Verticle Analysis Activity IZarish AzharNo ratings yet

- What Is Budget? Budget Is Quantitative Expression of Future PlanDocument4 pagesWhat Is Budget? Budget Is Quantitative Expression of Future PlanZubair ArshadNo ratings yet

- Corporate Financial Analysis with Microsoft ExcelFrom EverandCorporate Financial Analysis with Microsoft ExcelRating: 5 out of 5 stars5/5 (1)

- Budgetary Planning: Accounting Principles, Eighth EditionDocument52 pagesBudgetary Planning: Accounting Principles, Eighth EditionMaristella GatonNo ratings yet

- Gen Banking LawDocument11 pagesGen Banking LawDaniel John Cañares LegaspiNo ratings yet

- Chapter 5 Professional AudiDocument35 pagesChapter 5 Professional AudiDaniel John Cañares Legaspi100% (1)

- Bank Secrecy LawDocument2 pagesBank Secrecy LawDaniel John Cañares LegaspiNo ratings yet

- The Trans-Pacific Partnership (Trade of Goods)Document6 pagesThe Trans-Pacific Partnership (Trade of Goods)Daniel John Cañares LegaspiNo ratings yet

- Scatter Plot: 10000 F (X) 7.6826983136x 2 - 10550.0630855715x + 10546.0342910681 R 0.9999999728Document6 pagesScatter Plot: 10000 F (X) 7.6826983136x 2 - 10550.0630855715x + 10546.0342910681 R 0.9999999728Daniel John Cañares LegaspiNo ratings yet

- Certificate of Recognition: Charrevie M. TingsonDocument2 pagesCertificate of Recognition: Charrevie M. TingsonDaniel John Cañares LegaspiNo ratings yet

- Monday (November 24) : Men's& Women's Volleyball 12:30PM-5:00PM GYMDocument2 pagesMonday (November 24) : Men's& Women's Volleyball 12:30PM-5:00PM GYMDaniel John Cañares LegaspiNo ratings yet

- BEHASCIDocument2 pagesBEHASCIDaniel John Cañares LegaspiNo ratings yet

- Candidates For Internship Program For 1st Term AY 2015-2016Document1 pageCandidates For Internship Program For 1st Term AY 2015-2016Daniel John Cañares LegaspiNo ratings yet

- City University of PasayDocument2 pagesCity University of PasayDaniel John Cañares LegaspiNo ratings yet

- Chapter 3. Decision Analysis Section 3.1. Decision Trees With Conditional ProbabilitiesDocument12 pagesChapter 3. Decision Analysis Section 3.1. Decision Trees With Conditional ProbabilitiesDaniel John Cañares LegaspiNo ratings yet

- House Rules: 1. English Only PolicyDocument2 pagesHouse Rules: 1. English Only PolicyDaniel John Cañares LegaspiNo ratings yet

- SMCDocument12 pagesSMCDaniel John Cañares LegaspiNo ratings yet

- Del Mundo Q and ADocument2 pagesDel Mundo Q and ADaniel John Cañares LegaspiNo ratings yet

- 23 Marcon, Louise Margarette 24 Millar, AllyssaDocument2 pages23 Marcon, Louise Margarette 24 Millar, AllyssaDaniel John Cañares LegaspiNo ratings yet

- Partnership ReviewerDocument21 pagesPartnership ReviewerDaniel John Cañares Legaspi100% (1)

- PhotoshootDocument1 pagePhotoshootDaniel John Cañares LegaspiNo ratings yet

- Federatio N Year: Prof. Osler T AquinoDocument2 pagesFederatio N Year: Prof. Osler T AquinoDaniel John Cañares LegaspiNo ratings yet

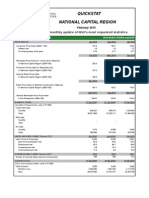

- Quickstat National Capital Region: A Monthly Update of NSO's Most Requested StatisticsDocument3 pagesQuickstat National Capital Region: A Monthly Update of NSO's Most Requested StatisticsDaniel John Cañares LegaspiNo ratings yet

- Federatio N Year: Prof. Osler T AquinoDocument1 pageFederatio N Year: Prof. Osler T AquinoDaniel John Cañares LegaspiNo ratings yet

- Cost of Production Report First Department: Quantity ScheduleDocument4 pagesCost of Production Report First Department: Quantity ScheduleDaniel John Cañares LegaspiNo ratings yet

- Grand Academic Congress 2015 (Responses) - v7Document14 pagesGrand Academic Congress 2015 (Responses) - v7Daniel John Cañares LegaspiNo ratings yet

- Sampoerna - Marketing Plan-Gc BonchonDocument13 pagesSampoerna - Marketing Plan-Gc BonchonDaniel John Cañares Legaspi50% (2)

- APS For Peer MentoringDocument2 pagesAPS For Peer MentoringDaniel John Cañares LegaspiNo ratings yet

- Activity 2 Fundamentals of AccountingDocument25 pagesActivity 2 Fundamentals of AccountingLaiza Cristella SarayNo ratings yet

- CA IPCC Branch AccountsDocument19 pagesCA IPCC Branch AccountsAkash Gupta75% (4)

- Budgeting - Seatwork MaDocument11 pagesBudgeting - Seatwork MaErica Caliuag100% (1)

- IAS-19 at Glance (BDO)Document4 pagesIAS-19 at Glance (BDO)FaraisNo ratings yet

- Financial Statement Analysis 1Document16 pagesFinancial Statement Analysis 1aehy lznuscrfbjNo ratings yet

- MODULE 15 Financial Reporting and ManagementDocument5 pagesMODULE 15 Financial Reporting and ManagementEuli Mae SomeraNo ratings yet

- Notes To The Consolidated Financial Statements: For The Year Ended December 31, 2008Document50 pagesNotes To The Consolidated Financial Statements: For The Year Ended December 31, 2008Rabail PkNo ratings yet

- Assessing A New Venture's Financial Strength and Viability: Bruce R. Barringer R. Duane IrelandDocument195 pagesAssessing A New Venture's Financial Strength and Viability: Bruce R. Barringer R. Duane IrelandLei OsNo ratings yet

- Com 5 CDocument2 pagesCom 5 CShamima AkterNo ratings yet

- Using The Altman Z-Score Model To Test Bankruptcy in The Oil IndustryDocument103 pagesUsing The Altman Z-Score Model To Test Bankruptcy in The Oil IndustrySumayya SiddiquaNo ratings yet

- Statement of Comprehensive IncomeDocument22 pagesStatement of Comprehensive IncomeAd BeeNo ratings yet

- Forum 1Document1 pageForum 1Nurul AryaniNo ratings yet

- Ias 1Document59 pagesIas 1gauravNo ratings yet

- Account GPDocument22 pagesAccount GPNurul SyuhadaNo ratings yet

- Sales & Receivables Journal-CITRADocument2 pagesSales & Receivables Journal-CITRAIqbal FisikaNo ratings yet

- M. Kabir Hassan, Rasem N. Kayed, and Umar A. Oseni: Introduction To Islamic Banking and Finance: Principles and PracticeDocument40 pagesM. Kabir Hassan, Rasem N. Kayed, and Umar A. Oseni: Introduction To Islamic Banking and Finance: Principles and PracticeAhmed MousaNo ratings yet

- The Elements of Financial StatementsDocument7 pagesThe Elements of Financial StatementsIan RanilopaNo ratings yet

- BFC 3227 Cost AccountingDocument85 pagesBFC 3227 Cost AccountingDaniel Ng'etichNo ratings yet

- Accounting Cycle: 4. Preparation of The Trial BalanceDocument8 pagesAccounting Cycle: 4. Preparation of The Trial BalanceAda Janelle Manzano0% (1)

- Dispensers of California, Inc.Document7 pagesDispensers of California, Inc.Prashuk SethiNo ratings yet

- 20 007 Tax Accounting Unravelling Mystery Income Taxes Second Revised Edition Final PrintDocument32 pages20 007 Tax Accounting Unravelling Mystery Income Taxes Second Revised Edition Final Printmolladagim19No ratings yet

- ACC100 Chapter 10Document61 pagesACC100 Chapter 10ConnieNo ratings yet

- BS Goyal Sons 180122Document66 pagesBS Goyal Sons 180122SANJIT CHAKMANo ratings yet

- Kunci Jawaban Semua BabDocument46 pagesKunci Jawaban Semua BabMuhammad RifqiNo ratings yet

- Toaz - Info Prelim Midterm PRDocument98 pagesToaz - Info Prelim Midterm PRClandestine SoulNo ratings yet

- Inter Accounts Revision - Part 1Document317 pagesInter Accounts Revision - Part 1311812922nishanthininkNo ratings yet

- Accounting Q&ADocument50 pagesAccounting Q&AKumaar Guhan50% (2)