Download as pptx, pdf, or txt

You might also like

- Process Costing NotesDocument3 pagesProcess Costing NotesOlin Pitters100% (1)

- Best Presentation On Cost SheetDocument34 pagesBest Presentation On Cost Sheetdhruvesh999100% (4)

- Chapter 5Document19 pagesChapter 5mbalenhle jezaNo ratings yet

- Process 08Document31 pagesProcess 08Aditya MishraNo ratings yet

- Costing PresentationDocument16 pagesCosting PresentationSarah Jane Ste MarieNo ratings yet

- Process Cost Accounting Additional Procedures: Accounting For Joint Products and By-ProductsDocument23 pagesProcess Cost Accounting Additional Procedures: Accounting For Joint Products and By-ProductsMudassar HassanNo ratings yet

- 10 - Accounting For Product CostDocument26 pages10 - Accounting For Product CostThanh LamNo ratings yet

- Chapter 1 ACCOUNTING FOR MANUFACTURING OPERATIONDocument36 pagesChapter 1 ACCOUNTING FOR MANUFACTURING OPERATIONMaimoona AsadNo ratings yet

- Process CostingDocument26 pagesProcess CostingsamiNo ratings yet

- Financial Tools Week 5 Block BDocument9 pagesFinancial Tools Week 5 Block BBelen González BouzaNo ratings yet

- Process CostingDocument16 pagesProcess CostingPiyush Gupta100% (2)

- 28 Process CostingDocument9 pages28 Process CostingJAY PRAKASH HINDOCHA-BBANo ratings yet

- Mowen2e PP Ch05Document43 pagesMowen2e PP Ch05DaveNo ratings yet

- 11 Production Cost Short-RunDocument42 pages11 Production Cost Short-RunHemachandra M mm21b029No ratings yet

- Cost AccountingDocument41 pagesCost AccountingNitin RajotiaNo ratings yet

- Features of Process CostingDocument9 pagesFeatures of Process CostingFred MutesasiraNo ratings yet

- CHAPTER 4 - Introduction To Economics by Ahmed A.Document24 pagesCHAPTER 4 - Introduction To Economics by Ahmed A.ahmedNo ratings yet

- Production Cost Short-RunDocument42 pagesProduction Cost Short-RunRichi KothariNo ratings yet

- Process CostingDocument83 pagesProcess CostingMohammad MoosaNo ratings yet

- Process CostingDocument13 pagesProcess CostingRajendran KajananthanNo ratings yet

- Cost Sheet (N)Document43 pagesCost Sheet (N)Shiv Deep Sharma 20mmb087No ratings yet

- Process CostingDocument3 pagesProcess CostingRahul SinghNo ratings yet

- Methods of CostingDocument21 pagesMethods of CostingsweetashusNo ratings yet

- Process Costing and Hybrid Product-Costing Systems: Mcgraw-Hill/IrwinDocument39 pagesProcess Costing and Hybrid Product-Costing Systems: Mcgraw-Hill/IrwinkasebNo ratings yet

- Producer TheoryDocument62 pagesProducer TheoryVriddhi ParekhNo ratings yet

- Output CostingDocument39 pagesOutput CostingTarpan MannanNo ratings yet

- Spoilage AccountingDocument26 pagesSpoilage AccountingParth BarotNo ratings yet

- Cost ClassificationDocument17 pagesCost Classificationsyed mohdNo ratings yet

- ACCT403 Product Costing Methods - Process CostingDocument39 pagesACCT403 Product Costing Methods - Process CostingMary AmoNo ratings yet

- Ebd IvDocument49 pagesEbd IvSharath NateshNo ratings yet

- Lecture On Output and Cost Israt Hossain, Lecturer Ba, DiuDocument18 pagesLecture On Output and Cost Israt Hossain, Lecturer Ba, DiuFoyez IslamNo ratings yet

- Process CostingDocument29 pagesProcess Costingrikesh radhe100% (1)

- Cost Chapter-4Document41 pagesCost Chapter-4yonaseyoum20No ratings yet

- AC222 2023 2 Process-CostingDocument22 pagesAC222 2023 2 Process-CostingLloyd MasiNo ratings yet

- Producer and Optimal Production ChoiceDocument20 pagesProducer and Optimal Production ChoiceSangram sahooNo ratings yet

- Process Costing TutorialDocument45 pagesProcess Costing Tutorialvenu gopal100% (1)

- Process CostingDocument48 pagesProcess CostingIrfanNo ratings yet

- Econdev Cost Concepts Classification and AnalysisDocument4 pagesEcondev Cost Concepts Classification and AnalysisKen Ivan HervasNo ratings yet

- Lec#5 Week#5 ECODocument33 pagesLec#5 Week#5 ECOZoha MughalNo ratings yet

- Ag Econ ReviewerDocument8 pagesAg Econ ReviewerNezuko CutieeeNo ratings yet

- Process Costing 01Document28 pagesProcess Costing 01Bharat GhoghariNo ratings yet

- Job, Batch and Process CostingDocument9 pagesJob, Batch and Process CostingLetlotlo LebeteNo ratings yet

- ACCT3203 Contemporary Managerial Accounting: Process Costing II Accounting For SpoilageDocument11 pagesACCT3203 Contemporary Managerial Accounting: Process Costing II Accounting For SpoilageJingwen YangNo ratings yet

- Costing Project PDFDocument25 pagesCosting Project PDFSuraj SingolkarNo ratings yet

- Understanding To Process CostingDocument43 pagesUnderstanding To Process CostingSarim Saleheen LariNo ratings yet

- Exercise Process CostingDocument5 pagesExercise Process Costingshahadat hossainNo ratings yet

- Management AccountingDocument246 pagesManagement AccountingsaraNo ratings yet

- Process CostingDocument14 pagesProcess CostingfitsumNo ratings yet

- Acc20007 Week 7Document31 pagesAcc20007 Week 7dannielNo ratings yet

- Chapter 6 Process CostingDocument28 pagesChapter 6 Process CostingAtif Saeed100% (1)

- Cost Units, Cost Classification, and Profit ReportingDocument43 pagesCost Units, Cost Classification, and Profit ReportingkundiarshdeepNo ratings yet

- Chapter3Process Cost Systems - AMSerrano.MPADocument57 pagesChapter3Process Cost Systems - AMSerrano.MPAAPPLE SERRANONo ratings yet

- The IIS University: Cost Accounting Project "Process Costing"Document15 pagesThe IIS University: Cost Accounting Project "Process Costing"Anjali GurejaniNo ratings yet

- Cost Analysis of Any Product or ServiceDocument27 pagesCost Analysis of Any Product or ServiceAayushiNo ratings yet

- Ch06 Process CostingDocument19 pagesCh06 Process CostingZaira PangesfanNo ratings yet

- Manufacturing Cost: Jono - Suhartono@itenas - Ac.idDocument29 pagesManufacturing Cost: Jono - Suhartono@itenas - Ac.idFrans ArapentaNo ratings yet

- Mcom Ac Paper IIDocument282 pagesMcom Ac Paper IIAmar Kant Pandey100% (1)

- Creating a One-Piece Flow and Production Cell: Just-in-time Production with Toyota’s Single Piece FlowFrom EverandCreating a One-Piece Flow and Production Cell: Just-in-time Production with Toyota’s Single Piece FlowRating: 4 out of 5 stars4/5 (1)

- Manufacturing Wastes Stream: Toyota Production System Lean Principles and ValuesFrom EverandManufacturing Wastes Stream: Toyota Production System Lean Principles and ValuesRating: 4.5 out of 5 stars4.5/5 (3)

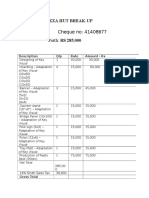

- Cheque No: 41408677 Worth: RS 285,000: Pizza Hut Break-UpDocument2 pagesCheque No: 41408677 Worth: RS 285,000: Pizza Hut Break-UpiishahbazNo ratings yet

- The22ImmutableLawsOfBranding BIZDocument16 pagesThe22ImmutableLawsOfBranding BIZRaja Sufyan MinhasNo ratings yet

- Divisional Performance ManagementDocument31 pagesDivisional Performance ManagementiishahbazNo ratings yet

- Time Sheet For Teaching AssistantDocument1 pageTime Sheet For Teaching AssistantiishahbazNo ratings yet

- Principles of Accounting I Assignment # 4: (Type Text)Document2 pagesPrinciples of Accounting I Assignment # 4: (Type Text)iishahbazNo ratings yet

- PLEST Analysis of Global Automotive IndustryDocument2 pagesPLEST Analysis of Global Automotive IndustryiishahbazNo ratings yet

- Financial Analysis of MitchellsDocument17 pagesFinancial Analysis of MitchellsiishahbazNo ratings yet

- SOAP Notes: HistoryDocument5 pagesSOAP Notes: HistoryRajveerNo ratings yet

- TechTalk Updated IEST-RP-CC012 A Must ReadDocument4 pagesTechTalk Updated IEST-RP-CC012 A Must ReadShivkumar Sharma100% (1)

- LPP - orDocument12 pagesLPP - orbharat_v79No ratings yet

- EXD2010 EX200: Compact Ex D Electro-Hydraulic Positioning and Monitoring SystemDocument8 pagesEXD2010 EX200: Compact Ex D Electro-Hydraulic Positioning and Monitoring SystemKelvin Anthony OssaiNo ratings yet

- Graphic Organizer 2Document4 pagesGraphic Organizer 2Amexis2No ratings yet

- OP AMPS HughesDocument8 pagesOP AMPS Hughesmarkos_mylonas4152No ratings yet

- Modal Adverb Lesson PlanDocument4 pagesModal Adverb Lesson Planapi-587326479100% (1)

- Oct 1st Week Details (Eng) by ACDocument26 pagesOct 1st Week Details (Eng) by ACHema Sundar ReddyNo ratings yet

- Illinois State Board of Education: General InformationDocument40 pagesIllinois State Board of Education: General InformationLeslie AtkinsonNo ratings yet

- CHP 7 InventoryDocument48 pagesCHP 7 InventoryStacy MitchellNo ratings yet

- Case Study Overhead Costs AnalysisDocument13 pagesCase Study Overhead Costs AnalysisTon SyNo ratings yet

- Anatomy of The Lymphatic SystemDocument76 pagesAnatomy of The Lymphatic SystemManisha RaoNo ratings yet

- Diaphragm and Lung Ultrasound To Predict Weaning Outcome: Systematic Review and Meta-AnalysisDocument11 pagesDiaphragm and Lung Ultrasound To Predict Weaning Outcome: Systematic Review and Meta-AnalysisPablo IgnacioNo ratings yet

- The Problem of Increasing Human Energy - Nikola Tesla PDFDocument27 pagesThe Problem of Increasing Human Energy - Nikola Tesla PDFKarhys100% (2)

- SPM (SEN 410) Lecturer HandoutsDocument51 pagesSPM (SEN 410) Lecturer HandoutsinzovarNo ratings yet

- Chapter 1Document43 pagesChapter 1Nour Aira NaoNo ratings yet

- Machine (Mechanical) - Wikipedia, The Free EncyclopediaDocument10 pagesMachine (Mechanical) - Wikipedia, The Free EncyclopediabmxengineeringNo ratings yet

- Champions 12 3 - Master PPT Slides - Oct2017Document14 pagesChampions 12 3 - Master PPT Slides - Oct2017Pieter Baobab BoomNo ratings yet

- Tamil Inscriptions in ChinaDocument38 pagesTamil Inscriptions in Chinasubiksha100% (1)

- Basic Concepts in Nursing (Report)Document101 pagesBasic Concepts in Nursing (Report)NDJNo ratings yet

- 1A New Five Level T Type Converter With SPWM For Medium Voltage ApplicationsDocument6 pages1A New Five Level T Type Converter With SPWM For Medium Voltage Applicationsyasin bayatNo ratings yet

- Assignment Name: Identifying Characteristics of Some Family With 5 ExamplesDocument4 pagesAssignment Name: Identifying Characteristics of Some Family With 5 ExamplesAbdullah Al MamunNo ratings yet

- Apache Kafka Quick Start GuideDocument180 pagesApache Kafka Quick Start GuidesleepercodeNo ratings yet

- Principles of Learning and Motivation Part 2Document3 pagesPrinciples of Learning and Motivation Part 2Tobs AnchetaNo ratings yet

- Time Value of Money: Compound InterestDocument28 pagesTime Value of Money: Compound InterestkateNo ratings yet

- Sarah Tchoukaleff ResumeDocument1 pageSarah Tchoukaleff Resumeapi-261081956No ratings yet

- De So 2 de Kiem Tra Hoc Ky 2 Tieng Anh 8 Moi 1681274649Document4 pagesDe So 2 de Kiem Tra Hoc Ky 2 Tieng Anh 8 Moi 1681274649Mai ChiNo ratings yet

- Chapter 5 - Object-Oriented Database ModelDocument9 pagesChapter 5 - Object-Oriented Database Modelyoseffisseha12No ratings yet

- Peripheral Testosterone MetabolismDocument8 pagesPeripheral Testosterone MetabolismAgung SentosaNo ratings yet

- LTL-X Software Manual - UKDocument19 pagesLTL-X Software Manual - UKHanif Yusfaula ZNo ratings yet