Download as pptx, pdf, or txt

You might also like

- Direct Deposit InfoDocument1 pageDirect Deposit InfoJose AlmonteNo ratings yet

- Wiley - Practice Exam 1 With SolutionsDocument10 pagesWiley - Practice Exam 1 With SolutionsIvan Bliminse80% (5)

- Frankwood Question Bank DSEDocument19 pagesFrankwood Question Bank DSEAu Tsz Man50% (4)

- Chapters 5-6: Use The Following For The Next Two QuestionsDocument9 pagesChapters 5-6: Use The Following For The Next Two QuestionsJane Ruby Jenniefer67% (3)

- CH 10Document9 pagesCH 10Tien Thanh DangNo ratings yet

- Withdrawal SlipDocument2 pagesWithdrawal SlipJerwin Samson100% (1)

- Credit Card FraudDocument13 pagesCredit Card Fraudharshita patni100% (1)

- KasdanPiutang 4B Kelompok1Document11 pagesKasdanPiutang 4B Kelompok1Estin TasyaNo ratings yet

- Ch. 7 NumericalsDocument20 pagesCh. 7 NumericalsSevera Zahoor100% (1)

- Chapter 14Document5 pagesChapter 14RahimahBawaiNo ratings yet

- Final - Adv Accounting2 - July 19 - 2021Document3 pagesFinal - Adv Accounting2 - July 19 - 2021Eleonora VinessaNo ratings yet

- Quiz Audit of LiabilitiesDocument3 pagesQuiz Audit of LiabilitiesCattleyaNo ratings yet

- 'ACT1204 Audit of Cash and Cash Equivalents Quiz No. 4Document4 pages'ACT1204 Audit of Cash and Cash Equivalents Quiz No. 4markNo ratings yet

- Chapter 14 Exercises - Set BDocument6 pagesChapter 14 Exercises - Set BHeather PaulsenNo ratings yet

- Cash and Cash Equivalents & Bank ReconciliationDocument20 pagesCash and Cash Equivalents & Bank ReconciliationHesil Jane DAGONDON100% (1)

- Bank Reconciliation Statement - Principles of AccountingDocument8 pagesBank Reconciliation Statement - Principles of AccountingAbdulla MaseehNo ratings yet

- Tugas Latihan 4 PDFDocument2 pagesTugas Latihan 4 PDFRadit Ramdan NopriantoNo ratings yet

- Audit Liability 12 Chapter 7Document1 pageAudit Liability 12 Chapter 7Ma Teresa B. CerezoNo ratings yet

- Tugas Latihan 4Document2 pagesTugas Latihan 4Radit Ramdan NopriantoNo ratings yet

- ACCT 2062 Homework #2Document22 pagesACCT 2062 Homework #2downinpuertorico100% (1)

- Poa May 2002 Paper 2Document12 pagesPoa May 2002 Paper 2Jerilee SoCute Watts50% (4)

- ACC 140 1 Period - Quiz 2Document7 pagesACC 140 1 Period - Quiz 2Rica Mille MartinNo ratings yet

- Bank Reconciliation PDFDocument12 pagesBank Reconciliation PDFKetan Thakkar100% (1)

- Workshop 9 Bank Reconciliation Statement - SsDocument2 pagesWorkshop 9 Bank Reconciliation Statement - Ssxu xuanNo ratings yet

- Acc 201 CH 10Document16 pagesAcc 201 CH 10Trickster TwelveNo ratings yet

- Week 4Document5 pagesWeek 4Erryn M. ParamythaNo ratings yet

- Notes Payable Test Bank PDFDocument5 pagesNotes Payable Test Bank PDFAB CloydNo ratings yet

- Cash and Accounts ReceivableDocument11 pagesCash and Accounts ReceivablePat ClosaNo ratings yet

- FA1 Chapter 1 EngDocument21 pagesFA1 Chapter 1 EngYong ChanNo ratings yet

- BU8101 Sem3 - Group 11Document63 pagesBU8101 Sem3 - Group 11Shweta SridharNo ratings yet

- CH 07Document5 pagesCH 07Ngọc NgốNo ratings yet

- CH 13Document6 pagesCH 13Zahid AkhtarNo ratings yet

- Quiz 2 Chpts 3 4Document14 pagesQuiz 2 Chpts 3 4Jayden Galing100% (1)

- 16772BRSDocument47 pages16772BRSSketch KathayatNo ratings yet

- Problem On Loan ImpairmentDocument26 pagesProblem On Loan ImpairmentYukiNo ratings yet

- Instructions:: Introduction To Financial Accounting B.Sc. 2 HrsDocument4 pagesInstructions:: Introduction To Financial Accounting B.Sc. 2 HrsPearl LawrenceNo ratings yet

- Fabm Module 3Document9 pagesFabm Module 3Cxharlyn AbayNo ratings yet

- Working 5Document6 pagesWorking 5Hà Lê DuyNo ratings yet

- Soal Asis Ak2 Pertemuan 1Document2 pagesSoal Asis Ak2 Pertemuan 1Aisya Fadhilla ShamaraNo ratings yet

- Acct 550 Final ExamDocument4 pagesAcct 550 Final ExamAlexis AhiagbeNo ratings yet

- FA & FFA Mock Exam Questions Set 5Document18 pagesFA & FFA Mock Exam Questions Set 5miss ainaNo ratings yet

- Nations: Practical Accounting 2Document2 pagesNations: Practical Accounting 2Lady Nhel Gutierrez PeradillaNo ratings yet

- La Consolacion College-Manila: School of Business and AccountancyDocument20 pagesLa Consolacion College-Manila: School of Business and AccountancyKasey PastorNo ratings yet

- Diploma in Cambodia Tax Pilot ExamDocument7 pagesDiploma in Cambodia Tax Pilot ExamVannak2015No ratings yet

- Lab-Current LiabilitiesDocument5 pagesLab-Current LiabilitiesPatrick HarponNo ratings yet

- Booklet 1 CORRECTION OF ERRORS CASHDocument17 pagesBooklet 1 CORRECTION OF ERRORS CASHnaddieNo ratings yet

- Test 3 of 2015Document7 pagesTest 3 of 2015muyan zouNo ratings yet

- Midterm Test - Code 37 - FA - Sem 2 - 21.22Document5 pagesMidterm Test - Code 37 - FA - Sem 2 - 21.22Đoàn Tài ĐứcNo ratings yet

- Ac550 FinalDocument4 pagesAc550 FinalGil SuarezNo ratings yet

- Seminar 3S212 - 13 PDFDocument4 pagesSeminar 3S212 - 13 PDFShweta SridharNo ratings yet

- Work SheetDocument2 pagesWork SheetFantayNo ratings yet

- Systems and Test of Controls Part 2 - Question and Solution Pack 2022Document33 pagesSystems and Test of Controls Part 2 - Question and Solution Pack 2022Rienhardt Van EedenNo ratings yet

- BANK RECONCILIATION NotesDocument9 pagesBANK RECONCILIATION NotesNicole DomingoNo ratings yet

- 123Document18 pages123Andrin LlemosNo ratings yet

- Quiz 3-Audit CashDocument8 pagesQuiz 3-Audit CashCindy CrausNo ratings yet

- Accrued Income: College of Business Studies BS Accountancy Midterm ExaminationDocument4 pagesAccrued Income: College of Business Studies BS Accountancy Midterm ExaminationPineda, King Moises PangilinanNo ratings yet

- QB IiiDocument33 pagesQB IiisaketramaNo ratings yet

- CH 07Document8 pagesCH 07Holly MotleyNo ratings yet

- One Year of Living with COVID-19: An Assessment of How ADB Members Fought the Pandemic in 2020From EverandOne Year of Living with COVID-19: An Assessment of How ADB Members Fought the Pandemic in 2020No ratings yet

- Financial Soundness Indicators for Financial Sector Stability in BangladeshFrom EverandFinancial Soundness Indicators for Financial Sector Stability in BangladeshNo ratings yet

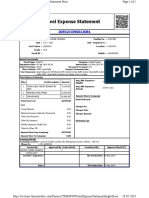

- Travel Expense Statement: 20E02CONS013081Document1 pageTravel Expense Statement: 20E02CONS013081DipNo ratings yet

- Dokumen - Tips Hsbcnet Mt940 Id Rev2Document6 pagesDokumen - Tips Hsbcnet Mt940 Id Rev2Emmanuel AristyaNo ratings yet

- 05 Jun 2020 - (Free) ..Chcltf1zaws - Bg0fagocegb - Ewx-Bav3egdyd2yldqyjahfycmxxawkicneja3edcqh0cwegcaekdhvycgDocument5 pages05 Jun 2020 - (Free) ..Chcltf1zaws - Bg0fagocegb - Ewx-Bav3egdyd2yldqyjahfycmxxawkicneja3edcqh0cwegcaekdhvycgDanny WilsonNo ratings yet

- Bank Account GuideDocument47 pagesBank Account Guidemayoo1986No ratings yet

- GTB - Obc MergerDocument5 pagesGTB - Obc MergermeetwithsanjayNo ratings yet

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument15 pagesStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceHunterNo ratings yet

- Benefits of BancassuranceDocument9 pagesBenefits of BancassuranceAllen ChiwauraNo ratings yet

- Balanced FundsDocument1 pageBalanced FundsYannah HidalgoNo ratings yet

- RES 3200 Chapter 2 Real Estate FinancingDocument12 pagesRES 3200 Chapter 2 Real Estate FinancingbaorunchenNo ratings yet

- Rek Koran Mandiri Juli 20Document10 pagesRek Koran Mandiri Juli 20sdwg0% (1)

- Consolidated Formcpdf 1288755 075734 SignedDocument4 pagesConsolidated Formcpdf 1288755 075734 SignedSRIKANTA ROUTNo ratings yet

- Difference Between Loans and Advances (With Comparison Chart) - Key DifferencesDocument11 pagesDifference Between Loans and Advances (With Comparison Chart) - Key DifferencesAnonymous sMqylHNo ratings yet

- Taylor Opposition To DemurrerDocument10 pagesTaylor Opposition To DemurrerGreg WilderNo ratings yet

- Brief History of Banking in IndiaDocument9 pagesBrief History of Banking in IndiaAakriti BhattNo ratings yet

- Bank Secrecy LawDocument17 pagesBank Secrecy LawSuzette VillalinoNo ratings yet

- 50 Bank Book IndexDocument2 pages50 Bank Book IndexAshutosh KumarNo ratings yet

- China, The United States, and Central Bank Digital Currencies How Important Is It To Be FirstDocument22 pagesChina, The United States, and Central Bank Digital Currencies How Important Is It To Be FirstJan BerkaNo ratings yet

- Tanzania Mortgage Market Update 31.12.2020Document7 pagesTanzania Mortgage Market Update 31.12.2020Arden Muhumuza KitomariNo ratings yet

- Forex ManagementDocument42 pagesForex ManagementRavinder YadavNo ratings yet

- Statement JUL2023 523565579 UnlockedDocument9 pagesStatement JUL2023 523565579 UnlockedúméshNo ratings yet

- My Bank StatementDocument1 pageMy Bank StatementDEMO HảiNo ratings yet

- March 2022Document5 pagesMarch 2022Сергей РатиновNo ratings yet

- Aishwarya Precision Works GECLSDocument7 pagesAishwarya Precision Works GECLSchandan bhatiNo ratings yet

- Reg6 MTCC Sagaycity 1stquarter2022Document129 pagesReg6 MTCC Sagaycity 1stquarter2022Aldous Pax ArcangelNo ratings yet

- Finance of Loan and Emi ProblemDocument6 pagesFinance of Loan and Emi ProblemPuducheri Yashwanth KumarNo ratings yet

- PG1234512451976Document1 pagePG1234512451976Nilay KumarNo ratings yet

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument4 pagesStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceHARSHIT CHAUHANNo ratings yet