Download as ppt, pdf, or txt

You might also like

- ENG Westernpips Private-User GuideDocument45 pagesENG Westernpips Private-User GuideThiago HenriqueNo ratings yet

- CAPM and APT With SolutionsDocument6 pagesCAPM and APT With SolutionsChinmayee ChoudhuryNo ratings yet

- Income GeneratorDocument18 pagesIncome GeneratoramareswarNo ratings yet

- Indian Financial SystemDocument52 pagesIndian Financial SystemtperuNo ratings yet

- Indian Financial SystemDocument52 pagesIndian Financial SystemSuresh Kumar manoharan86% (7)

- Session 01 Basics of Technical AnalysisDocument8 pagesSession 01 Basics of Technical AnalysisZulfiqar AliNo ratings yet

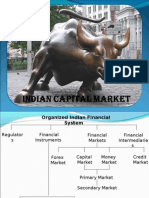

- Indian Capital MarketDocument19 pagesIndian Capital MarketdollieNo ratings yet

- Commodity PresentationDocument28 pagesCommodity PresentationROHIT_80No ratings yet

- Commodity Market ReportDocument38 pagesCommodity Market Reportpankajku2020100% (6)

- Diamond Derivatives: Lessons From Indian Markets: June 2007Document19 pagesDiamond Derivatives: Lessons From Indian Markets: June 2007Satendra KumarNo ratings yet

- On Interest Rate Futures: Reserve Bank of India August 2008Document52 pagesOn Interest Rate Futures: Reserve Bank of India August 2008Makarand LonkarNo ratings yet

- Original 1683521375 Equity SharesDocument40 pagesOriginal 1683521375 Equity SharesJaval ChoksiNo ratings yet

- A Summer Training ReportDocument14 pagesA Summer Training ReportSandeep_Sharma_5260No ratings yet

- 5.C - Regulatory Bodies in Different CountriesDocument5 pages5.C - Regulatory Bodies in Different CountriesCrest WolfNo ratings yet

- Securities Board of Nepal: Jawalakhel, Lalitpur, Nepal 9 October 2020Document132 pagesSecurities Board of Nepal: Jawalakhel, Lalitpur, Nepal 9 October 2020Max MysterioNo ratings yet

- Financial Market Final Collegeforprtg1Document105 pagesFinancial Market Final Collegeforprtg1vishgupta1987No ratings yet

- Capital Markets Secondary MarketsDocument32 pagesCapital Markets Secondary Marketsmedha_mehtaNo ratings yet

- Capital Markets & Money MarketsDocument52 pagesCapital Markets & Money Marketsynkamat100% (6)

- Impact of Reforms in Capital Market On Indian Capital MarketDocument30 pagesImpact of Reforms in Capital Market On Indian Capital MarketNiketu Shah0% (1)

- Indian Fin. SystemDocument66 pagesIndian Fin. SystemshahankeetNo ratings yet

- Report of The Rbi-Sebi Standing Technical Committee ON Exchange Traded Currency FuturesDocument21 pagesReport of The Rbi-Sebi Standing Technical Committee ON Exchange Traded Currency FuturesAnnie NishankNo ratings yet

- Capital MarketDocument19 pagesCapital MarketFast TrackNo ratings yet

- Commodity Guide PDFDocument108 pagesCommodity Guide PDFgaurav dixitNo ratings yet

- Indian Derivative Markets Future Prospects: CAPAM 2003 August 7, 2003Document27 pagesIndian Derivative Markets Future Prospects: CAPAM 2003 August 7, 2003api-19739167No ratings yet

- 5 Stocks For Accelerated Profit Apr2021Document28 pages5 Stocks For Accelerated Profit Apr2021Amrit KocharNo ratings yet

- MSEIDocument28 pagesMSEIadi08642No ratings yet

- NSE Annual Report 2021Document444 pagesNSE Annual Report 2021manas choudhuryNo ratings yet

- The Sasub IDocument24 pagesThe Sasub IHarsh KaushikNo ratings yet

- Capital Market Ecosystem LLM 12122022Document55 pagesCapital Market Ecosystem LLM 12122022KavyaNo ratings yet

- Markettimingreport PDFDocument46 pagesMarkettimingreport PDFJayanth RamNo ratings yet

- Introduction To Financial Institutions and Markets: Dr. Pradiptarathi Panda Assistant Professor, NismDocument26 pagesIntroduction To Financial Institutions and Markets: Dr. Pradiptarathi Panda Assistant Professor, NismMaunil OzaNo ratings yet

- Upsc - Cse: Union Public Service Commission General StudiesDocument26 pagesUpsc - Cse: Union Public Service Commission General Studiesmalik mohsinNo ratings yet

- G.S. Paper - 3 Volume - 1 EconomyDocument26 pagesG.S. Paper - 3 Volume - 1 EconomyAkash Kumar SinghNo ratings yet

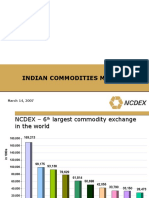

- Indian Commodities Market: March 14, 2007Document40 pagesIndian Commodities Market: March 14, 2007parishkaaNo ratings yet

- Commodity Basics: Himanshu AroraDocument32 pagesCommodity Basics: Himanshu AroraVaibhav GuptaNo ratings yet

- Capital Market: Presented byDocument134 pagesCapital Market: Presented byprathamesh09No ratings yet

- Lecture1-Basics of BFDocument30 pagesLecture1-Basics of BFAreeba QureshiNo ratings yet

- Group Members Kishan Gupta (72) Aditi Gupta (71) Harshit Gupta (70) Dhiraj DubeyDocument16 pagesGroup Members Kishan Gupta (72) Aditi Gupta (71) Harshit Gupta (70) Dhiraj Dubeyaditig22No ratings yet

- Basic 2 Financial Markets and Instruments v2Document26 pagesBasic 2 Financial Markets and Instruments v2ShailjaNo ratings yet

- National Stock Exchange: Research ReportDocument21 pagesNational Stock Exchange: Research ReportPramod KamathNo ratings yet

- Level 2 - Pragati - Basics of Capital Markets - 0Document25 pagesLevel 2 - Pragati - Basics of Capital Markets - 0Pulipaka NimeshikaNo ratings yet

- Capital MarketDocument12 pagesCapital MarketIBRAHIM FOYEZ Fall 20No ratings yet

- Equity Derivatives FAQ Document 1Document117 pagesEquity Derivatives FAQ Document 1Shruti TiwariNo ratings yet

- Role of Regulators in Indian Market: Presented By:mohd HuzaifaDocument31 pagesRole of Regulators in Indian Market: Presented By:mohd HuzaifaMuhammed HuzaifaNo ratings yet

- Commodity Futures MarketDocument12 pagesCommodity Futures Marketvaibhavrs22.pumbaNo ratings yet

- Financial Awareness Capsule For IBPS PO Mains 2022 PDF by Ambitious BabaDocument98 pagesFinancial Awareness Capsule For IBPS PO Mains 2022 PDF by Ambitious BabaAshutosh LandeNo ratings yet

- Short Name of Stock MarketDocument7 pagesShort Name of Stock MarketSARKAR TRADERSNo ratings yet

- 1146-Article Text-3219-1-10-20200101 PDFDocument7 pages1146-Article Text-3219-1-10-20200101 PDFjyoti parabNo ratings yet

- PPT-10 REITs - InvITs PresentaionDocument24 pagesPPT-10 REITs - InvITs PresentaionVikas MaheshwariNo ratings yet

- Part 1 - Introduction To Islamic Capital MarketDocument31 pagesPart 1 - Introduction To Islamic Capital MarketIzNew0212No ratings yet

- Feb Co1Document5 pagesFeb Co1saritasinha0207No ratings yet

- Comm Futures in India NseDocument9 pagesComm Futures in India Nseapi-3833893No ratings yet

- Financial Awareness Capsule For RRB Scale 2 2022 PDF by Ambitious BabaDocument119 pagesFinancial Awareness Capsule For RRB Scale 2 2022 PDF by Ambitious Bababhaskar kNo ratings yet

- 18th Nepal PDFDocument22 pages18th Nepal PDFparvez ansari100% (1)

- Sebibulletinjuly2018new PDocument123 pagesSebibulletinjuly2018new PRajat MittalNo ratings yet

- Capital Market - Secondary: Learning OutcomesDocument26 pagesCapital Market - Secondary: Learning OutcomesGiri SachinNo ratings yet

- Final ProjectDocument90 pagesFinal Projectaryanabhi123No ratings yet

- Chapter 7Document10 pagesChapter 7Sasikumar ThangaveluNo ratings yet

- Securities Operations: A Guide to Trade and Position ManagementFrom EverandSecurities Operations: A Guide to Trade and Position ManagementRating: 4 out of 5 stars4/5 (3)

- Hedge Fund Investment StrategiesDocument386 pagesHedge Fund Investment Strategiesjk kumar100% (1)

- Perspectives in Modelling of PricingDocument52 pagesPerspectives in Modelling of Pricingnil_parkarNo ratings yet

- Module 1 - Behavioural Finance IntroducedDocument94 pagesModule 1 - Behavioural Finance IntroducedShilpaNo ratings yet

- FINECO 04 State Preference TheoryDocument22 pagesFINECO 04 State Preference TheoryHiếu Nhi TrịnhNo ratings yet

- Global FinanceDocument49 pagesGlobal FinanceAnisha JhawarNo ratings yet

- The International Bond MarketDocument23 pagesThe International Bond Market2005raviNo ratings yet

- Stock Index FuturesDocument4 pagesStock Index FutureswannaflynowNo ratings yet

- Internatioanl FinanceDocument34 pagesInternatioanl FinanceABDUL SAMAD SUBHANINo ratings yet

- Tata Balanced Advantage Fund Nfo Scheme BrochureDocument4 pagesTata Balanced Advantage Fund Nfo Scheme BrochureNaveen VaryaniNo ratings yet

- Algorithmic Trading and Quantitative StrategiesDocument7 pagesAlgorithmic Trading and Quantitative StrategiesSelly YunitaNo ratings yet

- FIE400E 2016 Spring SolutionsDocument4 pagesFIE400E 2016 Spring SolutionsSander Von Porat BaugeNo ratings yet

- BFM Murugan McqsDocument34 pagesBFM Murugan McqsHanumantha Rao Turlapati100% (1)

- JPMorgan Global LNG Feb 2012Document248 pagesJPMorgan Global LNG Feb 2012rasjlpNo ratings yet

- Nism 8 - Equity Derivatives - Practice Test 2Document19 pagesNism 8 - Equity Derivatives - Practice Test 2complaints.tradeNo ratings yet

- International Economics II-1Document32 pagesInternational Economics II-1Dhugo abduNo ratings yet

- CFA一级基础段衍生 Tom 标准版Document113 pagesCFA一级基础段衍生 Tom 标准版Evelyn YangNo ratings yet

- Illustrations For Practice Q&ADocument5 pagesIllustrations For Practice Q&ADhruvi AgarwalNo ratings yet

- ECN FinalDocument8 pagesECN FinalRocel B. LigayaNo ratings yet

- ArbitrageDocument16 pagesArbitrageRishabYdvNo ratings yet

- CFA Level 2 Fixed Income 2017Document52 pagesCFA Level 2 Fixed Income 2017EdmundSiauNo ratings yet

- Commodity AssignmentDocument7 pagesCommodity Assignment05550No ratings yet

- FN2191 Commentary 2019Document22 pagesFN2191 Commentary 2019slimshadyNo ratings yet

- Ebook Fundamentals of Financial Instruments 2Nd Edition Sunil K Parameswaran Online PDF All ChapterDocument69 pagesEbook Fundamentals of Financial Instruments 2Nd Edition Sunil K Parameswaran Online PDF All Chaptercharles.powell359100% (5)

- Derivatives 1 MFIN IntroductionDocument49 pagesDerivatives 1 MFIN IntroductionYIN HanNo ratings yet

- ECMC49Y Market Efficiency Hypothesis Practice Questions Date: Aug 2, 2006Document6 pagesECMC49Y Market Efficiency Hypothesis Practice Questions Date: Aug 2, 2006Damalai YansanehNo ratings yet

- Dictionary of BankingDocument113 pagesDictionary of Bankingمحمود الحروب100% (1)

- Case Study: Collapse of Long-Term Capital ManagementDocument20 pagesCase Study: Collapse of Long-Term Capital ManagementVaibhav KharadeNo ratings yet

- Valuation of Option ModelDocument12 pagesValuation of Option ModelSagar GajjarNo ratings yet