Download as pptx, pdf, or txt

You might also like

- As 1755-2000 Conveyors - Safety RequirementsDocument8 pagesAs 1755-2000 Conveyors - Safety RequirementsSAI Global - APACNo ratings yet

- Fact Finding On Peoples Resistance To The Utkal Alumina International Limited (UAIL), Kashipur, Rayagada, Southern Orissa (2005)Document11 pagesFact Finding On Peoples Resistance To The Utkal Alumina International Limited (UAIL), Kashipur, Rayagada, Southern Orissa (2005)willyindia100% (1)

- Airtel Project ReportDocument23 pagesAirtel Project ReportKanchan Sanyal100% (2)

- "Master of Business Administration: Project ReportDocument127 pages"Master of Business Administration: Project ReportSaab JiNo ratings yet

- Review of LiteratureDocument12 pagesReview of LiteratureeswariNo ratings yet

- Analysing The Case of BPLDocument3 pagesAnalysing The Case of BPLLOKESH DUTTANo ratings yet

- Porter's Five Force ModelDocument19 pagesPorter's Five Force ModelKrishna Chaitanya100% (1)

- Jio PortersDocument4 pagesJio PortersAnkita Asthana50% (2)

- Comparative Analysis of Customer Satisfaction For Dish TV and Different DTH Player inDocument62 pagesComparative Analysis of Customer Satisfaction For Dish TV and Different DTH Player inAniruddha Bisen100% (3)

- Jio Giga FiberDocument16 pagesJio Giga Fiberapi-458222767No ratings yet

- Jio Case Study PDFDocument4 pagesJio Case Study PDFmanindersingh949100% (1)

- Customer's Perception Towards Reliance CommunicationDocument78 pagesCustomer's Perception Towards Reliance CommunicationMallikarjun Reddy ChagamreddyNo ratings yet

- Summer Training Project Report ON: "Manchitra"Document57 pagesSummer Training Project Report ON: "Manchitra"Himani GugnaniNo ratings yet

- Mobile IndustryDocument3 pagesMobile IndustryPrathamesh ButeNo ratings yet

- Tata Power Case AnalysisDocument7 pagesTata Power Case AnalysisAvinashSinghNo ratings yet

- Introdution: Bharat Sanchar Nigam Limited BSNLDocument28 pagesIntrodution: Bharat Sanchar Nigam Limited BSNLHemaNo ratings yet

- Report On Telecom Sector in IndiaDocument8 pagesReport On Telecom Sector in IndiaSaurabh Paharia100% (2)

- JioDocument16 pagesJioTHOTAKURI SHIVANo ratings yet

- Bajaj Electrical 1Document21 pagesBajaj Electrical 1kunal hajareNo ratings yet

- Ritesh Airtel ReportDocument94 pagesRitesh Airtel Reportsoumen rooj75% (4)

- Reliance Jio Project ReportDocument7 pagesReliance Jio Project ReportMukesh ChauhanNo ratings yet

- Project Report: The Training & Development Practices LG Electronics India Pvt. LTDDocument101 pagesProject Report: The Training & Development Practices LG Electronics India Pvt. LTDvishalsorout23No ratings yet

- JioDocument88 pagesJioGokul Krishnan100% (1)

- Print Project Report On Brand Preference of Mobile Phone Among College StudentsDocument42 pagesPrint Project Report On Brand Preference of Mobile Phone Among College StudentsRiya Mcoy100% (1)

- A Study On Satisfaction Level of Customers Towards Reliance Jio FiberDocument9 pagesA Study On Satisfaction Level of Customers Towards Reliance Jio Fibervinay sainiNo ratings yet

- Customer Satisfaction Samsung ProjDocument64 pagesCustomer Satisfaction Samsung ProjSAKSHI KHAITANNo ratings yet

- Airtel ProjectDocument60 pagesAirtel Projectnaveennpr4556No ratings yet

- Project Report On Sony DdepakDocument69 pagesProject Report On Sony Ddepaktechcaresystem33% (3)

- FMCG Industry in IndiaDocument10 pagesFMCG Industry in IndiaCharuta Jagtap TekawadeNo ratings yet

- A Project Report On AIRTELDocument91 pagesA Project Report On AIRTELHari Krishan100% (1)

- Indian Telecom Industry AnalysisDocument53 pagesIndian Telecom Industry Analysisratabgull67% (3)

- A Study On Drivers of Brand Switching Behaviour of Consumers From Jio To AirtelDocument41 pagesA Study On Drivers of Brand Switching Behaviour of Consumers From Jio To AirtelNagarjuna ReddyNo ratings yet

- Customer Satisfaction of BSNLDocument12 pagesCustomer Satisfaction of BSNLpurwa3895No ratings yet

- Main Project Appolo TyreDocument96 pagesMain Project Appolo TyregoswamiphotostatNo ratings yet

- Models of Service MarketingDocument34 pagesModels of Service MarketingPrasang Mangal100% (1)

- A Comprehensive Study On BSNL Revival CADocument16 pagesA Comprehensive Study On BSNL Revival CARAVI KUMARNo ratings yet

- Telenor UnderdogDocument14 pagesTelenor UnderdogSandeep MishraNo ratings yet

- Orient Electric: Company ProfileDocument11 pagesOrient Electric: Company ProfilePrince JoshiNo ratings yet

- Marketing Mix of Reliance Jio PartsDocument47 pagesMarketing Mix of Reliance Jio PartsZo MaNo ratings yet

- 2020 Project On LG Graduation ReportDocument63 pages2020 Project On LG Graduation ReportAmirNo ratings yet

- Palani ProjectDocument75 pagesPalani ProjectVinitha PriyaNo ratings yet

- Role and Significance of InsuranceDocument10 pagesRole and Significance of InsuranceRohit PadalkarNo ratings yet

- Jio Vs Airtel Project FinalDocument70 pagesJio Vs Airtel Project FinalMANTEL TELECOMNo ratings yet

- Study of Consumer Attitude Toward Mobile PhonesDocument25 pagesStudy of Consumer Attitude Toward Mobile PhonesMd. Mesbah Uddin63% (8)

- Airtel and Vodafone Marketing AnalysisDocument49 pagesAirtel and Vodafone Marketing AnalysisGurmeet SinghNo ratings yet

- AIRTELDocument94 pagesAIRTELDeepanshu DuaNo ratings yet

- Project ReportDocument8 pagesProject Reporttashi_kuhu100% (3)

- About Snapdeal DocumentDocument5 pagesAbout Snapdeal Documentruchi ratan100% (1)

- Financial Analysis of HDFC LifeDocument77 pagesFinancial Analysis of HDFC LifeSankalp SamantNo ratings yet

- Case Study InfosysDocument40 pagesCase Study InfosysfarhanbilliNo ratings yet

- BSNLDocument6 pagesBSNLHarsh ParekhNo ratings yet

- Impact of GST FMCG and Retail SectorDocument11 pagesImpact of GST FMCG and Retail SectorSunoop BalaramanNo ratings yet

- Research Report On Consumer Perception of Promotion Tools Used by Vodafone by Social Population of VodafoneDocument64 pagesResearch Report On Consumer Perception of Promotion Tools Used by Vodafone by Social Population of VodafoneBheeshm SinghNo ratings yet

- Micro Analysis of CERA SenetaryDocument98 pagesMicro Analysis of CERA SenetaryDhimant0% (1)

- Investing in Natural Capital for a Sustainable Future in the Greater Mekong SubregionFrom EverandInvesting in Natural Capital for a Sustainable Future in the Greater Mekong SubregionNo ratings yet

- Tele 2Document52 pagesTele 2Naved AhmadNo ratings yet

- Marketing of Services Telecom Industries: By:-Rizwana Khan Parul Tanwar Sonia Choudhary Anil SaraswatDocument19 pagesMarketing of Services Telecom Industries: By:-Rizwana Khan Parul Tanwar Sonia Choudhary Anil Saraswatrizwana_khan_1No ratings yet

- The Indian Telecom StoryDocument17 pagesThe Indian Telecom Storypriyankkothari123No ratings yet

- Telecom Management India TelecomDocument34 pagesTelecom Management India TelecomaneesssNo ratings yet

- Project ReportDocument12 pagesProject ReportRohit SharmaNo ratings yet

- Fundamental AnalysisDocument20 pagesFundamental AnalysisRitu Walia100% (1)

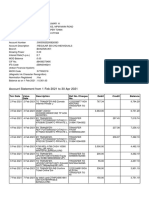

- Account Statement From 1 Feb 2021 To 30 Apr 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument11 pagesAccount Statement From 1 Feb 2021 To 30 Apr 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceUday AbhiNo ratings yet

- 2029 - School of Pharmacy, Swami Ramanand Teerth, Marathwada University, NandedDocument4 pages2029 - School of Pharmacy, Swami Ramanand Teerth, Marathwada University, NandedPharmacy Admission ExpertNo ratings yet

- Tuesday March 26 20241 53 48 Pmvacancy Notice For Various Posts On A Contract BasisDocument6 pagesTuesday March 26 20241 53 48 Pmvacancy Notice For Various Posts On A Contract BasisSonam PandeyNo ratings yet

- University Foundation - Financial DisclosureDocument7 pagesUniversity Foundation - Financial DisclosureSpotUsNo ratings yet

- It 41Document2 pagesIt 41रवींद्र वैद्यNo ratings yet

- The Commencement Date Is The Start of TheDocument4 pagesThe Commencement Date Is The Start of TheArvin BhurtunNo ratings yet

- MGMT 375 Trial ExamDocument2 pagesMGMT 375 Trial ExamPrince-SimonJohnMwanzaNo ratings yet

- Receiving Inspection ProcedureDocument2 pagesReceiving Inspection ProcedureErwin SantosoNo ratings yet

- 02 & 12 - Anup & Hitesh - Jubilant FoodWorks LTDDocument10 pages02 & 12 - Anup & Hitesh - Jubilant FoodWorks LTDasitbhatiaNo ratings yet

- 11.1valuation of Intellectual Property Assets PDFDocument31 pages11.1valuation of Intellectual Property Assets PDFShivam Anand100% (1)

- ITIL ConceptDocument57 pagesITIL Conceptsumanpk133100% (1)

- General ElectricDocument8 pagesGeneral ElectricAnjali Daisy100% (1)

- BUSI1633 L5 - Value ChainDocument23 pagesBUSI1633 L5 - Value ChainBùi Thu Hươngg100% (1)

- Project Assignment: Scope Purpose Covered inDocument6 pagesProject Assignment: Scope Purpose Covered inapplefieldNo ratings yet

- Annexure To The Joining Letter - C InitiateDocument5 pagesAnnexure To The Joining Letter - C Initiatekanna1808No ratings yet

- Iom 581 TTH Syllabus: Sosic@Marshall - Usc.EduDocument11 pagesIom 581 TTH Syllabus: Sosic@Marshall - Usc.Edusocalsurfy0% (1)

- Executive Recruitment in The Me Africa Amp RussiaDocument101 pagesExecutive Recruitment in The Me Africa Amp RussiaAvik SarkarNo ratings yet

- Mefa Ece 2-1Document8 pagesMefa Ece 2-1vamsibu50% (2)

- Archibald 11 08 PDFDocument13 pagesArchibald 11 08 PDFkvijayasokNo ratings yet

- Part 2Document179 pagesPart 2api-253241169No ratings yet

- Flexible Sheets For Waterproofing Bitumen Sheets For Roof Waterproofing Determination of Shear Resistance of JointsDocument1 pageFlexible Sheets For Waterproofing Bitumen Sheets For Roof Waterproofing Determination of Shear Resistance of Jointsmohammed wajidNo ratings yet

- Opm Problem Assignment 2Document10 pagesOpm Problem Assignment 2Aimes AliNo ratings yet

- PPP in Water Sector: Case Study From PRCDocument21 pagesPPP in Water Sector: Case Study From PRCkkawazu1450No ratings yet

- Revenue IAS 18Document7 pagesRevenue IAS 18Chota H MpukuNo ratings yet

- Advances in Banking Technology and Management Impacts of ICT and CRM Premier Reference SourceDocument381 pagesAdvances in Banking Technology and Management Impacts of ICT and CRM Premier Reference SourceShilpakumari Sudhamani100% (1)

- Report Accompanying The EstimateDocument3 pagesReport Accompanying The EstimateparameswarikumarNo ratings yet

- Feasibility Study Plan: LabadabangoDocument38 pagesFeasibility Study Plan: LabadabangoCocoy Llamas HernandezNo ratings yet

- SAP125 SAP Navigation 2005: SAP SCM-Procurement (MM) Academy ECC 6.0Document9 pagesSAP125 SAP Navigation 2005: SAP SCM-Procurement (MM) Academy ECC 6.0kngane8878No ratings yet

- CHS CBLM - Apply Quality Standards - FINALDocument51 pagesCHS CBLM - Apply Quality Standards - FINALYvonne Janet Cosico-Dela Fuente100% (1)