Download as pptx, pdf, or txt

You might also like

- FINA 385 Theory of Finance I Tutorials CAPMDocument17 pagesFINA 385 Theory of Finance I Tutorials CAPMgradesaverNo ratings yet

- Orange County Value at Risk CaseDocument16 pagesOrange County Value at Risk CaseSaad Bin MehmoodNo ratings yet

- The Golden PitchbookkDocument6 pagesThe Golden PitchbookkIftekharNo ratings yet

- Corporation Is: Separate Legal Entity Created by Law: Corporations and Stockholders EquityDocument25 pagesCorporation Is: Separate Legal Entity Created by Law: Corporations and Stockholders EquityCNo ratings yet

- Chapter 7 Stockholers Equity FinalDocument77 pagesChapter 7 Stockholers Equity FinalSampanna ShresthaNo ratings yet

- Chapter 13Document11 pagesChapter 13Maya HamdyNo ratings yet

- Chapter 13Document13 pagesChapter 13Mondy MondyNo ratings yet

- Corpo DefintionDocument3 pagesCorpo DefintionJhang Gheung Dee SaripNo ratings yet

- Chapter 17 Corporate FinanceDocument27 pagesChapter 17 Corporate Financecherryl marianoNo ratings yet

- BUSINESS FINANCE Week 2Document7 pagesBUSINESS FINANCE Week 2Ace San GabrielNo ratings yet

- Topic 5 - Sukokokopplemental Tasks and Exercises (Week 17)Document2 pagesTopic 5 - Sukokokopplemental Tasks and Exercises (Week 17)Taylor Kongitti PraditNo ratings yet

- FM10e ch17Document51 pagesFM10e ch17gurleen_2No ratings yet

- CH 10 Acc2010 NotesDocument10 pagesCH 10 Acc2010 Notesapi-248751950No ratings yet

- Introduction To Accounting 2 Organization and Capital Stock TransactionsDocument17 pagesIntroduction To Accounting 2 Organization and Capital Stock Transactionsalice horanNo ratings yet

- Accounting 2 - Book NotesDocument11 pagesAccounting 2 - Book NotesSimona PutnikNo ratings yet

- Company AccountingDocument7 pagesCompany AccountingMsuBrainBoxNo ratings yet

- Accounting For The Corporation Chapter 10Document51 pagesAccounting For The Corporation Chapter 10Rupesh PolNo ratings yet

- Fin Man Dividend PolicyDocument26 pagesFin Man Dividend PolicyMarriel Fate CullanoNo ratings yet

- Accounting Capital+Stock+TransactionsDocument17 pagesAccounting Capital+Stock+TransactionsOckouri BarnesNo ratings yet

- Valuation Methods: Common StocksDocument17 pagesValuation Methods: Common StocksJacinta Fatima ChingNo ratings yet

- Forms of DividendDocument24 pagesForms of Dividendsomanathbehera371No ratings yet

- Limited Liability CompanyDocument17 pagesLimited Liability CompanyAdrian RamsundarNo ratings yet

- All About StocksDocument21 pagesAll About Stockssimranjyotsuri7646No ratings yet

- Meeting 9 - Company Financial StatementsDocument42 pagesMeeting 9 - Company Financial StatementsHelen FebrianaNo ratings yet

- Shares and Their TermsDocument8 pagesShares and Their TermsVidya MastanammaNo ratings yet

- Chapter 11 Review 11th EdDocument15 pagesChapter 11 Review 11th EdTin RanocoNo ratings yet

- Solution Manual For Core Concepts of Accounting Raiborn 2nd EditionDocument18 pagesSolution Manual For Core Concepts of Accounting Raiborn 2nd EditionJacquelineFrancisfpgs100% (42)

- Chapter 13 SolutionsDocument45 pagesChapter 13 Solutionsaboodyuae2000No ratings yet

- CH 18: Dividend PolicyDocument55 pagesCH 18: Dividend PolicySaba MalikNo ratings yet

- Stockholders' Equity: in This Section We Will ReviewDocument25 pagesStockholders' Equity: in This Section We Will ReviewFitriyeni OktaviaNo ratings yet

- Long Term Sources of FinanceDocument21 pagesLong Term Sources of Financevivek patelNo ratings yet

- Share CapitalDocument6 pagesShare CapitalAashi DharwalNo ratings yet

- Corporations CH 12 Lecture 1Document18 pagesCorporations CH 12 Lecture 1Faisal SiddiquiNo ratings yet

- CAPE Recording Capital Stock & Reverses TransactionDocument49 pagesCAPE Recording Capital Stock & Reverses TransactionOckouri BarnesNo ratings yet

- Chapter 11 SummaryDocument3 pagesChapter 11 SummaryAreeba QureshiNo ratings yet

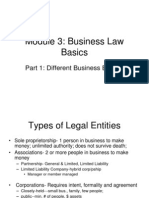

- Business Law - BasicDocument30 pagesBusiness Law - BasicGama Kristian AdikurniaNo ratings yet

- Corporations: Organization and Capital Stock Transactions: Weygandt - Kieso - KimmelDocument54 pagesCorporations: Organization and Capital Stock Transactions: Weygandt - Kieso - Kimmelkey aidanNo ratings yet

- sheet 5 E1 ازهرDocument9 pagessheet 5 E1 ازهرmagdy kamelNo ratings yet

- Dividend: Factors Affecting Dividend PolicyDocument11 pagesDividend: Factors Affecting Dividend PolicyNouman SheikhNo ratings yet

- Corporations: Organization, Capital Stock Transactions, and DividendsDocument37 pagesCorporations: Organization, Capital Stock Transactions, and DividendsTanhoster AgustinNo ratings yet

- A Money-Making Machine: Partnership Net AssetsDocument2 pagesA Money-Making Machine: Partnership Net AssetsRoberto TanakaNo ratings yet

- Finance Management 4Document26 pagesFinance Management 4charithNo ratings yet

- Fundamental AnalysisDocument48 pagesFundamental AnalysisBisma MasoodNo ratings yet

- Financial Accounting:: Tools For Business Decision Making, 4th EdDocument76 pagesFinancial Accounting:: Tools For Business Decision Making, 4th EdirquadriNo ratings yet

- Pptcorporation Module 5 Jan 2023Document56 pagesPptcorporation Module 5 Jan 2023Namor OnisaNo ratings yet

- Accounting Principles: Second Canadian EditionDocument35 pagesAccounting Principles: Second Canadian EditionEshetieNo ratings yet

- Principles of Accounting Chapter 11Document41 pagesPrinciples of Accounting Chapter 11myrentistoodamnhigh100% (1)

- Financial Reporting and Analysis: - Session 12-Professor Raluca Ratiu, PHDDocument45 pagesFinancial Reporting and Analysis: - Session 12-Professor Raluca Ratiu, PHDDaniel YebraNo ratings yet

- CFMP - Bloomberg Course: Your GuideDocument47 pagesCFMP - Bloomberg Course: Your GuideWilliam BoschNo ratings yet

- Common and Preferred StockDocument14 pagesCommon and Preferred StockMuhammad AyazNo ratings yet

- Tutorial 2Document6 pagesTutorial 2杰克 l孙No ratings yet

- EquityDocument34 pagesEquityVe DekNo ratings yet

- Chapter 12 - Shareholders' Equity: Capital Contributions, Distributions, and EarningsDocument47 pagesChapter 12 - Shareholders' Equity: Capital Contributions, Distributions, and EarningsDeepanshu PartiNo ratings yet

- Dividend Policy Dividend PolicyDocument42 pagesDividend Policy Dividend Policyshanzah amirNo ratings yet

- Equity of CorporationsDocument51 pagesEquity of Corporationskrys_elleNo ratings yet

- Free Cash Flow (Solution)Document11 pagesFree Cash Flow (Solution)alliahnahNo ratings yet

- Equity - The Accounting Equation For Every BusinessDocument5 pagesEquity - The Accounting Equation For Every BusinessSarah Del RosarioNo ratings yet

- Advanced AccountingDocument70 pagesAdvanced AccountingNasrudin Mohamed AhmedNo ratings yet

- Exchange-Traded Funds: Tax Advantages For ShareholdersDocument5 pagesExchange-Traded Funds: Tax Advantages For ShareholderscaashutoshsinghNo ratings yet

- Corporate Action Final DhirajDocument32 pagesCorporate Action Final Dhirajmishradhiraj533_gmaiNo ratings yet

- Chapter 11 - Reporting and Analyzing Stockholders' EquityDocument15 pagesChapter 11 - Reporting and Analyzing Stockholders' EquityElaiza RegaladoNo ratings yet

- A Beginners Guide to Stock Market: Investment, Types of Stocks, Growing Money & Securing Financial FutureFrom EverandA Beginners Guide to Stock Market: Investment, Types of Stocks, Growing Money & Securing Financial FutureNo ratings yet

- Intelligent Web Applications: (Part 1)Document36 pagesIntelligent Web Applications: (Part 1)Dhafra Sanchez'sNo ratings yet

- Slide Show:: Powerpoint For LearningDocument4 pagesSlide Show:: Powerpoint For LearningDhafra Sanchez'sNo ratings yet

- Course Overview and Intro To Ruby: INFO 2310: Topics in Web Design and ProgrammingDocument51 pagesCourse Overview and Intro To Ruby: INFO 2310: Topics in Web Design and ProgrammingDhafra Sanchez'sNo ratings yet

- Introduction To PHP and Postgresql: CSC 436 - Fall 2008Document18 pagesIntroduction To PHP and Postgresql: CSC 436 - Fall 2008Dhafra Sanchez'sNo ratings yet

- Introduction To Computers and ProgrammingDocument37 pagesIntroduction To Computers and ProgrammingDhafra Sanchez'sNo ratings yet

- 4 Internet ProgrammingDocument49 pages4 Internet ProgrammingDhafra Sanchez'sNo ratings yet

- Web Programming: Henning Schulzrinne Dept. of Computer Science Columbia UniversityDocument39 pagesWeb Programming: Henning Schulzrinne Dept. of Computer Science Columbia UniversityDhafra Sanchez'sNo ratings yet

- CS 380 Web Programming: Instructor: Xenia MountrouidouDocument44 pagesCS 380 Web Programming: Instructor: Xenia MountrouidouDhafra Sanchez'sNo ratings yet

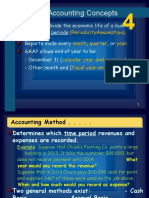

- Accrual Accounting Concepts: Accountants Divide The Economic Life of A Business Into Reporting PeriodsDocument36 pagesAccrual Accounting Concepts: Accountants Divide The Economic Life of A Business Into Reporting PeriodsDhafra Sanchez'sNo ratings yet

- Financial AnalysisDocument15 pagesFinancial AnalysisSitiNorhafizahDollah100% (1)

- PESTEL Analysis of Indian Capital MarketDocument4 pagesPESTEL Analysis of Indian Capital Marketdharmendra kumarNo ratings yet

- Project Template Comparing Tootsie Roll & HersheyDocument16 pagesProject Template Comparing Tootsie Roll & HersheymcmoneysNo ratings yet

- 57 2015Document4 pages57 2015Carlo100% (1)

- Bhanu PantDocument15 pagesBhanu PantMonojit RoyNo ratings yet

- Vertical Analysis SMDocument4 pagesVertical Analysis SMMac b IBANEZNo ratings yet

- A Study On The Financial Perfomance of Western India PlywoodsDocument105 pagesA Study On The Financial Perfomance of Western India PlywoodsMeena SivasubramanianNo ratings yet

- Merchant BankingDocument21 pagesMerchant BankinghksanthoshNo ratings yet

- Volume 1 12 The Dollar's Descent Orderly or Not October 30 2009Document12 pagesVolume 1 12 The Dollar's Descent Orderly or Not October 30 2009Denis OuelletNo ratings yet

- Impact of Behavioral Finance On Mergers and AcquisitionsDocument2 pagesImpact of Behavioral Finance On Mergers and AcquisitionsBharadwaj KA100% (1)

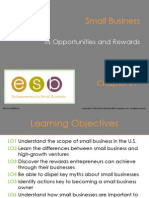

- Small Business: Its Opportunities and RewardsDocument22 pagesSmall Business: Its Opportunities and RewardsJose Antonio VegaNo ratings yet

- Test 092403Document10 pagesTest 092403Janice ChanNo ratings yet

- TransgendersDocument7 pagesTransgendersJastine Mae FajilanNo ratings yet

- Colliers KSA-Hotels-Review-Q1-2016-EN PDFDocument9 pagesColliers KSA-Hotels-Review-Q1-2016-EN PDFAbdellah EssonniNo ratings yet

- CH 18Document7 pagesCH 18Amit ChaturvediNo ratings yet

- SAP FI Certification Actual QuestionDocument4 pagesSAP FI Certification Actual QuestionkhalidmahmoodqumarNo ratings yet

- Pulse of Fintech 2018: Blockchain Investment Exceeds 2017 Annual TotalDocument2 pagesPulse of Fintech 2018: Blockchain Investment Exceeds 2017 Annual TotalSergio VinsennauNo ratings yet

- Major Project Key Decision PointsDocument7 pagesMajor Project Key Decision PointssiklebNo ratings yet

- RM 16076 ELK Petroleum AR16 Financials FinalwebDocument72 pagesRM 16076 ELK Petroleum AR16 Financials FinalwebAbdulSamadNo ratings yet

- Wework ReportDocument4 pagesWework Reporttran quoc vietNo ratings yet

- Property Types Diversification Strategy of Malaysian Real Estate Investment Trust (M-Reits)Document9 pagesProperty Types Diversification Strategy of Malaysian Real Estate Investment Trust (M-Reits)Hafis ShaharNo ratings yet

- Inventory ManagementDocument23 pagesInventory ManagementvmktptNo ratings yet

- Strategic ManagementDocument16 pagesStrategic Managementkhan moinNo ratings yet

- Jet - EtihadDocument21 pagesJet - EtihadPooja KhandwalaNo ratings yet

- 2016 Proposed Budget BookDocument761 pages2016 Proposed Budget BookJustin CarderNo ratings yet

- Sap Fi Transaction Codes List IDocument10 pagesSap Fi Transaction Codes List IJose Luis GonzalezNo ratings yet

- Maldives SME Development ProjectDocument109 pagesMaldives SME Development ProjectAdam KhaleelNo ratings yet