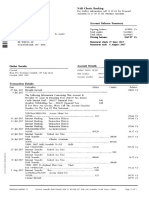

MNG Accounting Week 1

MNG Accounting Week 1

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5822)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (898)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Market Analysis Template 02Document5 pagesMarket Analysis Template 02YAP JOON YEE NICHOLASNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- State Vs MarketDocument22 pagesState Vs MarketSnigdha BansalNo ratings yet

- TFIN20Document2 pagesTFIN20anil-mbaNo ratings yet

- Internal Control Management 122: Michael WilliamsDocument7 pagesInternal Control Management 122: Michael WilliamsSeung Hyun BaeNo ratings yet

- MNG Accounting Week 8Document14 pagesMNG Accounting Week 8Seung Hyun BaeNo ratings yet

- MNG Accounting Week 4Document16 pagesMNG Accounting Week 4Seung Hyun BaeNo ratings yet

- Decision Making Management 122: Michael WilliamsDocument10 pagesDecision Making Management 122: Michael WilliamsSeung Hyun BaeNo ratings yet

- Cost Accounting Management 122: Michael WilliamsDocument13 pagesCost Accounting Management 122: Michael WilliamsSeung Hyun BaeNo ratings yet

- 9980 20170804 StatementDocument2 pages9980 20170804 StatementLyon Paing PhyoNo ratings yet

- Closing and Post-Closing EntriesDocument13 pagesClosing and Post-Closing EntriesBrian Reyes GangcaNo ratings yet

- Total Assets P2,888,000: Debit To ExpensesDocument25 pagesTotal Assets P2,888,000: Debit To ExpensesLove FreddyNo ratings yet

- Entep Not Yet Done Super Duper Not Yet DoneDocument21 pagesEntep Not Yet Done Super Duper Not Yet DoneMickaela CaldonaNo ratings yet

- Chapter 17 Oligopolies Look For The Answers To These QuestionsDocument24 pagesChapter 17 Oligopolies Look For The Answers To These QuestionsshamsaNo ratings yet

- Snapdeal and E Bay ProjectDocument15 pagesSnapdeal and E Bay ProjectAlyka MachadoNo ratings yet

- Ch-1 PPT Principles of MKTDocument22 pagesCh-1 PPT Principles of MKTBamlak WenduNo ratings yet

- Zafe Builders A Proposed Business Plan: A Proposed Business PlanDocument31 pagesZafe Builders A Proposed Business Plan: A Proposed Business PlanpicefeatiNo ratings yet

- Audit of InventoryDocument9 pagesAudit of InventoryEliyah JhonsonNo ratings yet

- Strategic Management ToyotaDocument27 pagesStrategic Management Toyotaglittering_star900280% (5)

- Managerial Economics Economic Tools For Todays Decision Makers 6E 6Th Edition Paul G Keat Download PDF ChapterDocument51 pagesManagerial Economics Economic Tools For Todays Decision Makers 6E 6Th Edition Paul G Keat Download PDF Chapterlouise.dietrick782100% (18)

- DaburDocument43 pagesDaburdeepak boraNo ratings yet

- Chapter 16 - Pricing StrategyDocument36 pagesChapter 16 - Pricing StrategyAnuj ChandaNo ratings yet

- Seperation of Mixed CostsDocument2 pagesSeperation of Mixed CostsTanvir Ahmed ChowdhuryNo ratings yet

- Imperfect Market in IndonesiaDocument2 pagesImperfect Market in IndonesiaTri Nugraha Ramadhani100% (1)

- Digital Marketing Plan For Private Unive PDFDocument63 pagesDigital Marketing Plan For Private Unive PDFkbd alokNo ratings yet

- Marketing ResearchDocument19 pagesMarketing ResearchmklrlclNo ratings yet

- KM30 Old National Highway, San Pedro, Laguna, PhilippinesDocument2 pagesKM30 Old National Highway, San Pedro, Laguna, Philippineschristina abucayNo ratings yet

- Module 4-Operating, Financial, and Total LeverageDocument45 pagesModule 4-Operating, Financial, and Total LeverageAna ValenovaNo ratings yet

- ENT 600 - Commercialization of RNDDocument3 pagesENT 600 - Commercialization of RNDsyamilmazlanNo ratings yet

- Jetblue Airways: Deicing at Logan AirportDocument5 pagesJetblue Airways: Deicing at Logan AirportNarinderNo ratings yet

- Work Attitude in VietnamDocument1 pageWork Attitude in VietnamThanh ThủyNo ratings yet

- BCG MatrixDocument18 pagesBCG Matrixsamm78992% (12)

- Netrika Due DiligenceDocument3 pagesNetrika Due DiligenceHimanshu BishtNo ratings yet

- Ratio VoltasDocument22 pagesRatio VoltasMandeep BatraNo ratings yet

- P5 - Auditing - May 2024 - AnsDocument10 pagesP5 - Auditing - May 2024 - Ansrathiharsh.indiaNo ratings yet

- Audit II CH 4 Nov 2020Document10 pagesAudit II CH 4 Nov 2020padmNo ratings yet

Download as pptx, pdf, or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5822)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (898)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Market Analysis Template 02Document5 pagesMarket Analysis Template 02YAP JOON YEE NICHOLASNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- State Vs MarketDocument22 pagesState Vs MarketSnigdha BansalNo ratings yet

- TFIN20Document2 pagesTFIN20anil-mbaNo ratings yet

- Internal Control Management 122: Michael WilliamsDocument7 pagesInternal Control Management 122: Michael WilliamsSeung Hyun BaeNo ratings yet

- MNG Accounting Week 8Document14 pagesMNG Accounting Week 8Seung Hyun BaeNo ratings yet

- MNG Accounting Week 4Document16 pagesMNG Accounting Week 4Seung Hyun BaeNo ratings yet

- Decision Making Management 122: Michael WilliamsDocument10 pagesDecision Making Management 122: Michael WilliamsSeung Hyun BaeNo ratings yet

- Cost Accounting Management 122: Michael WilliamsDocument13 pagesCost Accounting Management 122: Michael WilliamsSeung Hyun BaeNo ratings yet

- 9980 20170804 StatementDocument2 pages9980 20170804 StatementLyon Paing PhyoNo ratings yet

- Closing and Post-Closing EntriesDocument13 pagesClosing and Post-Closing EntriesBrian Reyes GangcaNo ratings yet

- Total Assets P2,888,000: Debit To ExpensesDocument25 pagesTotal Assets P2,888,000: Debit To ExpensesLove FreddyNo ratings yet

- Entep Not Yet Done Super Duper Not Yet DoneDocument21 pagesEntep Not Yet Done Super Duper Not Yet DoneMickaela CaldonaNo ratings yet

- Chapter 17 Oligopolies Look For The Answers To These QuestionsDocument24 pagesChapter 17 Oligopolies Look For The Answers To These QuestionsshamsaNo ratings yet

- Snapdeal and E Bay ProjectDocument15 pagesSnapdeal and E Bay ProjectAlyka MachadoNo ratings yet

- Ch-1 PPT Principles of MKTDocument22 pagesCh-1 PPT Principles of MKTBamlak WenduNo ratings yet

- Zafe Builders A Proposed Business Plan: A Proposed Business PlanDocument31 pagesZafe Builders A Proposed Business Plan: A Proposed Business PlanpicefeatiNo ratings yet

- Audit of InventoryDocument9 pagesAudit of InventoryEliyah JhonsonNo ratings yet

- Strategic Management ToyotaDocument27 pagesStrategic Management Toyotaglittering_star900280% (5)

- Managerial Economics Economic Tools For Todays Decision Makers 6E 6Th Edition Paul G Keat Download PDF ChapterDocument51 pagesManagerial Economics Economic Tools For Todays Decision Makers 6E 6Th Edition Paul G Keat Download PDF Chapterlouise.dietrick782100% (18)

- DaburDocument43 pagesDaburdeepak boraNo ratings yet

- Chapter 16 - Pricing StrategyDocument36 pagesChapter 16 - Pricing StrategyAnuj ChandaNo ratings yet

- Seperation of Mixed CostsDocument2 pagesSeperation of Mixed CostsTanvir Ahmed ChowdhuryNo ratings yet

- Imperfect Market in IndonesiaDocument2 pagesImperfect Market in IndonesiaTri Nugraha Ramadhani100% (1)

- Digital Marketing Plan For Private Unive PDFDocument63 pagesDigital Marketing Plan For Private Unive PDFkbd alokNo ratings yet

- Marketing ResearchDocument19 pagesMarketing ResearchmklrlclNo ratings yet

- KM30 Old National Highway, San Pedro, Laguna, PhilippinesDocument2 pagesKM30 Old National Highway, San Pedro, Laguna, Philippineschristina abucayNo ratings yet

- Module 4-Operating, Financial, and Total LeverageDocument45 pagesModule 4-Operating, Financial, and Total LeverageAna ValenovaNo ratings yet

- ENT 600 - Commercialization of RNDDocument3 pagesENT 600 - Commercialization of RNDsyamilmazlanNo ratings yet

- Jetblue Airways: Deicing at Logan AirportDocument5 pagesJetblue Airways: Deicing at Logan AirportNarinderNo ratings yet

- Work Attitude in VietnamDocument1 pageWork Attitude in VietnamThanh ThủyNo ratings yet

- BCG MatrixDocument18 pagesBCG Matrixsamm78992% (12)

- Netrika Due DiligenceDocument3 pagesNetrika Due DiligenceHimanshu BishtNo ratings yet

- Ratio VoltasDocument22 pagesRatio VoltasMandeep BatraNo ratings yet

- P5 - Auditing - May 2024 - AnsDocument10 pagesP5 - Auditing - May 2024 - Ansrathiharsh.indiaNo ratings yet

- Audit II CH 4 Nov 2020Document10 pagesAudit II CH 4 Nov 2020padmNo ratings yet