Download as ppt, pdf, or txt

You might also like

- Mcdonalds Corporation Case StudyDocument19 pagesMcdonalds Corporation Case StudyAnas Mahmood100% (1)

- Barclays Shiller White PaperDocument36 pagesBarclays Shiller White PaperRyan LeggioNo ratings yet

- Topic 2 - Long Term FinDocument25 pagesTopic 2 - Long Term FinAina KhairunnisaNo ratings yet

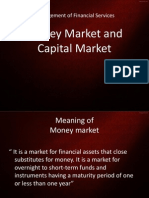

- Fm302 Management+of+Financial+ServicesDocument83 pagesFm302 Management+of+Financial+ServicesVinayrajNo ratings yet

- Constituents of The Financial System DD Intro NewDocument17 pagesConstituents of The Financial System DD Intro NewAnonymous bf1cFDuepPNo ratings yet

- Finance Specilization: Asst. Professors, MBA Department, Bhagawan Mahavir College of Management, SuratDocument85 pagesFinance Specilization: Asst. Professors, MBA Department, Bhagawan Mahavir College of Management, Suratsakshirelan87No ratings yet

- Unit III Capital MarketDocument27 pagesUnit III Capital MarketAbin VargheseNo ratings yet

- Finance Specilization: Asst. Professors, MBA Department, Bhagawan Mahavir College of Management, SuratDocument85 pagesFinance Specilization: Asst. Professors, MBA Department, Bhagawan Mahavir College of Management, Suratpravesh malikNo ratings yet

- International Capital Market Case Study - Part 1. Basic Knowledge of Capital MarketDocument27 pagesInternational Capital Market Case Study - Part 1. Basic Knowledge of Capital Marketmanojbhatia1220No ratings yet

- Abhishek Chaudhary Jatinder Dangwal Nupur Jain Ravinder Sharma Rishi Panwar Sakshi Chauhan Shashi Kumar Shankar Narayan BatabyalDocument41 pagesAbhishek Chaudhary Jatinder Dangwal Nupur Jain Ravinder Sharma Rishi Panwar Sakshi Chauhan Shashi Kumar Shankar Narayan BatabyalSakshi ChauhanNo ratings yet

- Chapter 5Document27 pagesChapter 5arnav.gopalNo ratings yet

- Capital Market 2Document25 pagesCapital Market 2manyasinghNo ratings yet

- FE Chapter 4Document43 pagesFE Chapter 4dehinnetagimasNo ratings yet

- Financial Institutions & Financial Markets Module - 1: by Sanjeev TamhaneDocument35 pagesFinancial Institutions & Financial Markets Module - 1: by Sanjeev TamhaneSwagatJagtapNo ratings yet

- Overview of Indian Financial MARKETSDocument46 pagesOverview of Indian Financial MARKETSGaurav Rathaur100% (2)

- Mutual FundDocument167 pagesMutual FundVinithaNo ratings yet

- Financial Market - Unit 1 (1) (Autosaved)Document71 pagesFinancial Market - Unit 1 (1) (Autosaved)learnerme129No ratings yet

- Financial MarketDocument17 pagesFinancial MarketsadikiNo ratings yet

- Chapter 10 Financial Market XII 1Document21 pagesChapter 10 Financial Market XII 1Keshvi AggarwalNo ratings yet

- Investment BankingDocument64 pagesInvestment BankingSandeep YadavNo ratings yet

- CH 1Document36 pagesCH 1youssef ibrahimNo ratings yet

- Module 3.1 Secondary MarketDocument54 pagesModule 3.1 Secondary MarketsateeshjorliNo ratings yet

- Unit 5Document97 pagesUnit 5Pankaj PrasadNo ratings yet

- Week No.1Document13 pagesWeek No.1Nasir KhattakNo ratings yet

- Secondary Markets in IndiaDocument49 pagesSecondary Markets in Indiayashi225100% (1)

- Management of Financial Services: Finance SpecilizationDocument83 pagesManagement of Financial Services: Finance SpecilizationaamirankNo ratings yet

- Tunis Stock ExchangeDocument54 pagesTunis Stock ExchangeAnonymous AoDxR5Rp4JNo ratings yet

- Capital Market OperationsDocument120 pagesCapital Market OperationsmanjapcNo ratings yet

- Financial MarketsDocument34 pagesFinancial Marketsmouli poliparthiNo ratings yet

- Unit II L2 Money Market InstrumentsDocument67 pagesUnit II L2 Money Market InstrumentsHari chandanaNo ratings yet

- Indian Financial System Chapter 1Document16 pagesIndian Financial System Chapter 1Rahul GhosaleNo ratings yet

- Part III Money Market (Revised For 2e)Document31 pagesPart III Money Market (Revised For 2e)Harun MusaNo ratings yet

- FMI Module I - PPT - An Introduction To Financial System and Its Constituents - StudentDocument65 pagesFMI Module I - PPT - An Introduction To Financial System and Its Constituents - StudentAnisha RohatgiNo ratings yet

- MFS IntroDocument35 pagesMFS IntroCharu ModiNo ratings yet

- International Business: Presented By: Group 8 Sonal Jain Mona Gogar Aastha AggarwalDocument35 pagesInternational Business: Presented By: Group 8 Sonal Jain Mona Gogar Aastha Aggarwalsonal jainNo ratings yet

- Overview of Indian Financial SystemDocument25 pagesOverview of Indian Financial SystemDr. Meghna DangiNo ratings yet

- INVESTMENTDocument41 pagesINVESTMENTbereket nigussieNo ratings yet

- Indian Financial & Secu. Markets & ProductsDocument93 pagesIndian Financial & Secu. Markets & ProductsLipika haldarNo ratings yet

- Mod 4 1Document29 pagesMod 4 1David JohnNo ratings yet

- Developing The Money Market in India: Dr. Muhammad ShafiDocument40 pagesDeveloping The Money Market in India: Dr. Muhammad ShafiPradeep KumarNo ratings yet

- Capital MarketDocument125 pagesCapital Marketrajni soni89% (9)

- Presented By:-Raj Kumar Lloyd Business School PGDM (2008-2010) PH: - 09711242389Document20 pagesPresented By:-Raj Kumar Lloyd Business School PGDM (2008-2010) PH: - 09711242389srajaloneNo ratings yet

- Chapter - I: Financial System - AnDocument33 pagesChapter - I: Financial System - AnSuresh VaddeNo ratings yet

- Capital MarketDocument125 pagesCapital MarketForam ChhedaNo ratings yet

- Mutual FundsDocument43 pagesMutual FundsAnkur PandeyNo ratings yet

- Introduction To Indian Financial SystemDocument31 pagesIntroduction To Indian Financial SystemthensureshNo ratings yet

- Ebi & Utual Unds: Ndian Inancial YstemDocument38 pagesEbi & Utual Unds: Ndian Inancial YstemKARISHMAATA2No ratings yet

- Chapter 1 Role of Financial Markets and InstitutionsDocument46 pagesChapter 1 Role of Financial Markets and InstitutionsJao FloresNo ratings yet

- Chapter - 2Document91 pagesChapter - 2Chetan BagriNo ratings yet

- Mutual Fund InvestmentDocument2 pagesMutual Fund Investmentsatya820No ratings yet

- C-PPT-Indian Financial SystemDocument27 pagesC-PPT-Indian Financial SystemAbhishek GuptaNo ratings yet

- 2.lecture 02-Role-of-Financial-Markets-InstitutionsDocument40 pages2.lecture 02-Role-of-Financial-Markets-InstitutionsTayyab SaleemNo ratings yet

- 1.3 Overview of Investments - Financial MarketDocument31 pages1.3 Overview of Investments - Financial MarketNatasha GhazaliNo ratings yet

- Ch.1 Money MarketDocument32 pagesCh.1 Money MarketjaludaxNo ratings yet

- Week 10Document7 pagesWeek 10zarmoona zarlalieNo ratings yet

- Chapter 1 Role of Financial Markets and InstitutionsDocument42 pagesChapter 1 Role of Financial Markets and Institutionschinuuchu100% (2)

- 6-Financial Environment System LDocument27 pages6-Financial Environment System LerolcanNo ratings yet

- Indian Financial SystemDocument18 pagesIndian Financial SystemSHASHANK TOMER 21211781No ratings yet

- Chapter No.1: The Financial System An IntroductionDocument19 pagesChapter No.1: The Financial System An IntroductionChavda BhaveshNo ratings yet

- Mastering the Market: A Comprehensive Guide to Successful Stock InvestingFrom EverandMastering the Market: A Comprehensive Guide to Successful Stock InvestingNo ratings yet

- NARS Nurses Assigned in Rural ServiceDocument2 pagesNARS Nurses Assigned in Rural ServiceTycoonVanrod Falculan PaasNo ratings yet

- Difference BTW Micro & Macro EconDocument5 pagesDifference BTW Micro & Macro EconshyasirNo ratings yet

- Jeppiaar Engineering College: Question BankDocument25 pagesJeppiaar Engineering College: Question Bankpasrinivasan_19973520% (1)

- Tax Invoice: Gstin Drug Licence NoDocument1 pageTax Invoice: Gstin Drug Licence NoRohit BansalNo ratings yet

- CPVDocument5 pagesCPVPrasetyo AdityaNo ratings yet

- Flexible Budget ExampleDocument2 pagesFlexible Budget Examplebrenica_2000No ratings yet

- SAARCDocument47 pagesSAARCVivek Tiwari100% (1)

- 3 SAMT Journal Winter 2013 PDFDocument40 pages3 SAMT Journal Winter 2013 PDFpatthai100% (1)

- Refrigerator BillDocument5 pagesRefrigerator BilldharmendraNo ratings yet

- A Federation in Peril Yugoslavia S EconomyDocument21 pagesA Federation in Peril Yugoslavia S EconomySlovenianStudyReferencesNo ratings yet

- Group 4 - Pse 11Document4 pagesGroup 4 - Pse 11Maulidah Nurul AiniNo ratings yet

- PC v00-SP3510 PDFDocument63 pagesPC v00-SP3510 PDFAlejandro López GómezNo ratings yet

- TEST BANK: Daft, Richard L. Management, 11th Ed. 2014 Chapter 15Document39 pagesTEST BANK: Daft, Richard L. Management, 11th Ed. 2014 Chapter 15polkadots93980% (5)

- Be Tutorial 3 - StuDocument18 pagesBe Tutorial 3 - StuGia LinhNo ratings yet

- B.O 2033 DGC Aee - II Data Sor 2014Document3 pagesB.O 2033 DGC Aee - II Data Sor 2014nisajamesNo ratings yet

- Operations and Production Management MGMT 405 Answer Set 1Document3 pagesOperations and Production Management MGMT 405 Answer Set 1Anissa Negra AkroutNo ratings yet

- Breed InauguralDocument3 pagesBreed InauguralJeff ElderNo ratings yet

- PRD Spec 2 5Document6 pagesPRD Spec 2 5Cesar Orlando Laura AlipazNo ratings yet

- Difference Between Merger & AcquisitionDocument16 pagesDifference Between Merger & AcquisitionAnand SalotNo ratings yet

- Facility Location - Operations ManagementDocument18 pagesFacility Location - Operations ManagementPrateek Vyas100% (2)

- Supply and Demand AnalysisDocument17 pagesSupply and Demand AnalysisMelody Zulueta ManicdoNo ratings yet

- Engro Food STG MNGT (1) ..Document36 pagesEngro Food STG MNGT (1) ..dreamy_geminiNo ratings yet

- AIP 2021 With Forms 1-7Document15 pagesAIP 2021 With Forms 1-7harlenemaybalacysaloNo ratings yet

- Acca Presentation 3Document23 pagesAcca Presentation 3Nearchos A. IoannouNo ratings yet

- Acid Hydrolysis of Bagasse For Ethanol ProductionDocument6 pagesAcid Hydrolysis of Bagasse For Ethanol ProductionRommelGalvanNo ratings yet

- Daft OT12e PPT Ch06Document23 pagesDaft OT12e PPT Ch06ravi prakashNo ratings yet

- Managing Competition in City Services: The Case of BarcelonaDocument15 pagesManaging Competition in City Services: The Case of BarcelonaN3N5YNo ratings yet

- Problem 8-35 Hansen Mowen Cornerstone of Managerial AccountingDocument4 pagesProblem 8-35 Hansen Mowen Cornerstone of Managerial Accountingwiwit_karyantiNo ratings yet