Download as pptx, pdf, or txt

You might also like

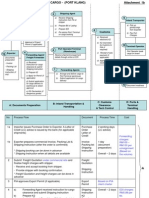

- Export + Import Process Flow - Break Bulk Cargo 27072010Document11 pagesExport + Import Process Flow - Break Bulk Cargo 27072010Ahmad Fauzi Mehat100% (1)

- Federal Register / Vol. 77, No. 76 / Thursday, April 19, 2012 / Rules and RegulationsDocument5 pagesFederal Register / Vol. 77, No. 76 / Thursday, April 19, 2012 / Rules and Regulationsshurst2No ratings yet

- International Tax Law Exchange of Information Cross-Border CollaborationDocument65 pagesInternational Tax Law Exchange of Information Cross-Border CollaborationKyriakos IosifellisNo ratings yet

- US Internal Revenue Service: td8845Document29 pagesUS Internal Revenue Service: td8845IRSNo ratings yet

- US Internal Revenue Service: 11943601Document7 pagesUS Internal Revenue Service: 11943601IRSNo ratings yet

- SaudiVATlaw-bilingual (Logo) 01Document22 pagesSaudiVATlaw-bilingual (Logo) 01mohamedNo ratings yet

- US Internal Revenue Service: 15623203Document13 pagesUS Internal Revenue Service: 15623203IRSNo ratings yet

- Guidance On Tax Audit Procedure: National Tax Service Instructions No. 1661Document8 pagesGuidance On Tax Audit Procedure: National Tax Service Instructions No. 1661Arya FlyingboyNo ratings yet

- CRP11 Introduction 2011.PDF Double TaxationDocument18 pagesCRP11 Introduction 2011.PDF Double TaxationLakshjit KapurNo ratings yet

- TIEA Agreement Between Ecuador and PeruDocument6 pagesTIEA Agreement Between Ecuador and PeruOECD: Organisation for Economic Co-operation and DevelopmentNo ratings yet

- The Interpretation and Meaning of "Beneficial Owner" in New ZealandDocument31 pagesThe Interpretation and Meaning of "Beneficial Owner" in New Zealandryu255No ratings yet

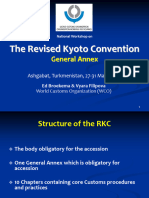

- Session 4 The Revised Kyoto Convention-General AnnexDocument22 pagesSession 4 The Revised Kyoto Convention-General AnnexHabtamu GabisaNo ratings yet

- Taxation 1 Digested CasesDocument39 pagesTaxation 1 Digested CasesfinserglenNo ratings yet

- FATCA Lawsuit: The Federal Government's Statement of DefenceDocument18 pagesFATCA Lawsuit: The Federal Government's Statement of DefencepatrickcainNo ratings yet

- Tax Remedies Under The NircDocument119 pagesTax Remedies Under The NircCaliNo ratings yet

- US Internal Revenue Service: 12237902Document24 pagesUS Internal Revenue Service: 12237902IRSNo ratings yet

- PWC FATCA Newsbrief Overview 02.27.12Document20 pagesPWC FATCA Newsbrief Overview 02.27.12Vitalii LiakhNo ratings yet

- Country by Country FaqDocument6 pagesCountry by Country FaqJayant JoshiNo ratings yet

- US Internal Revenue Service: 10274002Document7 pagesUS Internal Revenue Service: 10274002IRSNo ratings yet

- US Internal Revenue Service: A-06-22Document51 pagesUS Internal Revenue Service: A-06-22IRSNo ratings yet

- US Internal Revenue Service: 10951205Document8 pagesUS Internal Revenue Service: 10951205IRSNo ratings yet

- Handbook 5.12 Federal Tax Liens HandbookDocument41 pagesHandbook 5.12 Federal Tax Liens HandbookPaulStaplesNo ratings yet

- Regulatory Compliance - CDE Test - Milinda SenguptaDocument13 pagesRegulatory Compliance - CDE Test - Milinda SenguptaMilinda SenguptaNo ratings yet

- TIEA Agreement Between Mexico and CuraçaoDocument19 pagesTIEA Agreement Between Mexico and CuraçaoOECD: Organisation for Economic Co-operation and DevelopmentNo ratings yet

- Michael BoppDocument4 pagesMichael BoppMarketsWikiNo ratings yet

- Government Response Limited PartnershipsDocument18 pagesGovernment Response Limited PartnershipsOlegNo ratings yet

- Washington: New York 1101 New York Avenue, NW 8th Floor Washington, DC 20005-4269 P: 202.962.7300 F: 202.962.7305Document10 pagesWashington: New York 1101 New York Avenue, NW 8th Floor Washington, DC 20005-4269 P: 202.962.7300 F: 202.962.7305ABC DEFNo ratings yet

- TIEA Agreement Between Aruba and SpainDocument24 pagesTIEA Agreement Between Aruba and SpainOECD: Organisation for Economic Co-operation and DevelopmentNo ratings yet

- US Internal Revenue Service: Irb02-18Document50 pagesUS Internal Revenue Service: Irb02-18IRSNo ratings yet

- 2010 Protocol Amending The ConventionDocument11 pages2010 Protocol Amending The ConventionMahfoudh El MezziNo ratings yet

- Private Clarifications - EN - 31 05 2023Document18 pagesPrivate Clarifications - EN - 31 05 2023fatemazt29No ratings yet

- US Internal Revenue Service: 15924303Document18 pagesUS Internal Revenue Service: 15924303IRSNo ratings yet

- 1706-2342281 - International Reporting Challenges and Common Errors - 8!24!17 - ACM ReviewDocument48 pages1706-2342281 - International Reporting Challenges and Common Errors - 8!24!17 - ACM ReviewJamesMinionNo ratings yet

- Local Content Requirements in The Oil and Gas Sector - A. de Lima Campos Keynote Day 1Document25 pagesLocal Content Requirements in The Oil and Gas Sector - A. de Lima Campos Keynote Day 1nami_00No ratings yet

- BUSL320 - Mid Semester Exam StudyDocument4 pagesBUSL320 - Mid Semester Exam StudyAfaan Shakeeb0% (1)

- ACCC-ASIC Debt Collection GuidelineDocument67 pagesACCC-ASIC Debt Collection Guidelinetomecruzz100% (1)

- Unit 1 ExceDocument22 pagesUnit 1 ExceMaham KhanNo ratings yet

- Tax Remedies Under The Nirc (Repaired)Document119 pagesTax Remedies Under The Nirc (Repaired)RSOG PRO6No ratings yet

- US Internal Revenue Service: td8735Document10 pagesUS Internal Revenue Service: td8735IRSNo ratings yet

- Backgrounder On Proposals For Amendment of The ICSID RulesDocument4 pagesBackgrounder On Proposals For Amendment of The ICSID RulesFrancisco José GrobNo ratings yet

- CIR V SC Johnson and Son and CADocument4 pagesCIR V SC Johnson and Son and CAkenken320No ratings yet

- Investigating The Property Pre-Exchange SearchesDocument40 pagesInvestigating The Property Pre-Exchange SearchesFh FhNo ratings yet

- US Internal Revenue Service: A98-99Document15 pagesUS Internal Revenue Service: A98-99IRSNo ratings yet

- Federal Register / Vol. 77, No. 9 / Friday, January 13, 2012 / Rules and RegulationsDocument89 pagesFederal Register / Vol. 77, No. 9 / Friday, January 13, 2012 / Rules and RegulationsMarketsWikiNo ratings yet

- The Financial (Minimum Income) Requirement For Partner VisasDocument18 pagesThe Financial (Minimum Income) Requirement For Partner VisassjplepNo ratings yet

- 11 RR 10-2010 PDFDocument4 pages11 RR 10-2010 PDFJoyceNo ratings yet

- National Lead Company v. Commissioner of Internal Revenue, 336 F.2d 134, 2d Cir. (1964)Document11 pagesNational Lead Company v. Commissioner of Internal Revenue, 336 F.2d 134, 2d Cir. (1964)Scribd Government DocsNo ratings yet

- Ebook Byrd and Chens Canadian Tax Principles 2012 2013 Edition Canadian 1St Edition Byrd Solutions Manual Full Chapter PDFDocument68 pagesEbook Byrd and Chens Canadian Tax Principles 2012 2013 Edition Canadian 1St Edition Byrd Solutions Manual Full Chapter PDFShannonRussellapcx100% (15)

- US Internal Revenue Service: 064602fDocument6 pagesUS Internal Revenue Service: 064602fIRSNo ratings yet

- Taxation Notes 2024 s1Document7 pagesTaxation Notes 2024 s1xoloveyoona530No ratings yet

- US Internal Revenue Service: Irb04-43Document27 pagesUS Internal Revenue Service: Irb04-43IRSNo ratings yet

- US Internal Revenue Service: Irb06-42Document76 pagesUS Internal Revenue Service: Irb06-42IRSNo ratings yet

- Mesa Power Group Bifurcation ResponseDocument9 pagesMesa Power Group Bifurcation ResponseAanjaneya SinghNo ratings yet

- The Formation of Contract OnlineDocument12 pagesThe Formation of Contract OnlineinventionjournalsNo ratings yet

- Assignment - IiDocument12 pagesAssignment - IiMohitNo ratings yet

- Constitution Legislative SourcesDocument29 pagesConstitution Legislative SourcesAndrew NeuberNo ratings yet

- US Internal Revenue Service: 12256402Document6 pagesUS Internal Revenue Service: 12256402IRSNo ratings yet

- Unit 2, Section 2: Residential Block & Estate Management © ARLA, ARHM, ARMA, ASSET SKILLS, CIH, NAEA, RICSDocument11 pagesUnit 2, Section 2: Residential Block & Estate Management © ARLA, ARHM, ARMA, ASSET SKILLS, CIH, NAEA, RICSFranciska HeystekNo ratings yet

- 55 Water Street NEW YORK, NY 10041-0099 TEL: 212-855-3240Document5 pages55 Water Street NEW YORK, NY 10041-0099 TEL: 212-855-3240MarketsWikiNo ratings yet

- US Internal Revenue Service: 10534401Document9 pagesUS Internal Revenue Service: 10534401IRSNo ratings yet

- Europe: Rs o F Er Ak Le SDocument2 pagesEurope: Rs o F Er Ak Le SCo'nank Anfield100% (1)

- Handbook of Classical MythologyDocument2 pagesHandbook of Classical MythologyCo'nank AnfieldNo ratings yet

- Handbook of Classical Mythology 12: SatyricaDocument2 pagesHandbook of Classical Mythology 12: SatyricaCo'nank AnfieldNo ratings yet

- Untitled 11Document2 pagesUntitled 11Co'nank AnfieldNo ratings yet

- Basic Concepts: Handbook of Classical Mythology 2Document2 pagesBasic Concepts: Handbook of Classical Mythology 2Co'nank AnfieldNo ratings yet

- How Classical Mythology Came Into BeingDocument2 pagesHow Classical Mythology Came Into BeingCo'nank AnfieldNo ratings yet

- Untitled 3Document2 pagesUntitled 3Co'nank AnfieldNo ratings yet

- DsadsdsDocument2 pagesDsadsdsCo'nank AnfieldNo ratings yet

- And and andDocument2 pagesAnd and andCo'nank AnfieldNo ratings yet

- Wire Request FormDocument3 pagesWire Request Formkhushbu25No ratings yet

- Philippine Health Insurance CorporationDocument2 pagesPhilippine Health Insurance CorporationJaikonnenNo ratings yet

- Bulk DealDocument2 pagesBulk DealRavi UdeshiNo ratings yet

- Starting A BusinessDocument2 pagesStarting A BusinessYeasy AgustinaNo ratings yet

- Micro Credit in CanadaDocument16 pagesMicro Credit in CanadatextbooksneedthemNo ratings yet

- FASTag Application FormDocument4 pagesFASTag Application FormAtul Kumar DixitNo ratings yet

- Complaint Clout of Ttitle Breach of ContractDocument23 pagesComplaint Clout of Ttitle Breach of ContractChicagoCitizens EmpowermentGroupNo ratings yet

- Productivity 1236Document165 pagesProductivity 1236Sameer GuptaNo ratings yet

- Credit Card StatementDocument4 pagesCredit Card Statementanshuman kumarNo ratings yet

- Logistics Project ReportDocument7 pagesLogistics Project ReportTanmay MiddhaNo ratings yet

- Axis BAnk Case AnalysisDocument47 pagesAxis BAnk Case Analysissakyasingha4u100% (1)

- RACETRAC PETROLEUM, INC V ACE AMERICAN INSURANCE COMPANY Exhibits Policies2Document52 pagesRACETRAC PETROLEUM, INC V ACE AMERICAN INSURANCE COMPANY Exhibits Policies2ACELitigationWatchNo ratings yet

- Assignment - Explain Income From Other SourcesDocument9 pagesAssignment - Explain Income From Other SourcesPraveen SNo ratings yet

- Indwdhi 20183107 PDFDocument1 pageIndwdhi 20183107 PDFtuyiNo ratings yet

- CB - Annual Report 2010Document390 pagesCB - Annual Report 2010vindesel3984No ratings yet

- Wire Transfer Receipts 2Document1 pageWire Transfer Receipts 2namdrikaleleNo ratings yet

- Eduction SbiDocument119 pagesEduction SbiRoshan JadhavNo ratings yet

- Bihar Gramin Bank Bihar Gramin Bank: Challan Form-01 (Cash Voucher) Challan Form - 01 (Cash Voucher)Document1 pageBihar Gramin Bank Bihar Gramin Bank: Challan Form-01 (Cash Voucher) Challan Form - 01 (Cash Voucher)anand singhNo ratings yet

- Sajid Patel ResumeDocument2 pagesSajid Patel ResumeSajidpatel78603No ratings yet

- Internship PapanDocument59 pagesInternship PapanPapan Das SabujNo ratings yet

- CSOAStatement 103769173Document4 pagesCSOAStatement 103769173Hasan AliNo ratings yet

- 23 Office AccountsDocument9 pages23 Office AccountsNguyenNo ratings yet

- CrfguidancenotesDocument9 pagesCrfguidancenotesapi-100643385No ratings yet

- Bank of Baroda - Wikipedia, The Free EncyclopediaDocument8 pagesBank of Baroda - Wikipedia, The Free EncyclopediaSai RamNo ratings yet

- ConversionDocument62 pagesConversionMara Reyes50% (2)

- 2016 - G.R. No. 183486, (2016-02-24)Document23 pages2016 - G.R. No. 183486, (2016-02-24)ArahbellsNo ratings yet

- Case Study 1Document20 pagesCase Study 1Dirajen PMNo ratings yet

- Residual Method: A Development AppraisalDocument10 pagesResidual Method: A Development AppraisalYeowkoon ChinNo ratings yet

- Guide To Mystery ShoppingDocument53 pagesGuide To Mystery Shoppingriver33No ratings yet