PEM Audit

PEM Audit

You might also like

- Rye, C. (2001) Change Management The 5 Step ToolkitDocument59 pagesRye, C. (2001) Change Management The 5 Step ToolkitIleana SendreaNo ratings yet

- 5 - Ratio Regression and Difference Estimation - RevisedDocument39 pages5 - Ratio Regression and Difference Estimation - RevisedFiqry ZolkofiliNo ratings yet

- 6 Accountability and Auditing in The Public Sector (Nota)Document63 pages6 Accountability and Auditing in The Public Sector (Nota)cik bungaNo ratings yet

- Prelim Ch5Document14 pagesPrelim Ch5Cathleen Drew TuazonNo ratings yet

- Innovations in Public Sector Internal Audit: Case of IndonesiaDocument21 pagesInnovations in Public Sector Internal Audit: Case of IndonesiaMarlon StafinNo ratings yet

- Field BalancingsDocument51 pagesField BalancingsTaraknath MukherjeeNo ratings yet

- Research-Ch-4 - Sampling DesignDocument42 pagesResearch-Ch-4 - Sampling Designaddisyawkal18No ratings yet

- Basics of Company Act.Document10 pagesBasics of Company Act.neha kailleyNo ratings yet

- Introduction To Difference-In-Differences DesignDocument18 pagesIntroduction To Difference-In-Differences DesignDadan KosasihNo ratings yet

- Report Balancing 255 FDocument1 pageReport Balancing 255 Feka septianaNo ratings yet

- AEB14 SM CH15 v2Document24 pagesAEB14 SM CH15 v2RonLiu35No ratings yet

- ch09 - PPT - Rankin - 2e RevDocument37 pagesch09 - PPT - Rankin - 2e Revmichele hazelNo ratings yet

- Time Series Analysis and ForecastingDocument69 pagesTime Series Analysis and ForecastingSumendra RaghavNo ratings yet

- Environmental AccountingDocument27 pagesEnvironmental AccountingFaresh Haroon100% (1)

- AEB14 SM CH17 v2Document31 pagesAEB14 SM CH17 v2RonLiu350% (1)

- Assurance Engagements and Internal Audit and Sections On Public Sector and Charity Audits - pp15Document41 pagesAssurance Engagements and Internal Audit and Sections On Public Sector and Charity Audits - pp15dhea100% (1)

- Maximizing The Value of A Risk-Based Audit Plan.Document4 pagesMaximizing The Value of A Risk-Based Audit Plan.Arco Priyo DirgantoroNo ratings yet

- 2.3 Section Properties of Built-Up Steel SectionsDocument5 pages2.3 Section Properties of Built-Up Steel SectionsKen SmithNo ratings yet

- Course Title: Data Pre-Processing and VisualizationDocument11 pagesCourse Title: Data Pre-Processing and VisualizationIntekhab Aslam100% (2)

- Karanja Evanson Mwangi Cit Masters Report Libre PDFDocument136 pagesKaranja Evanson Mwangi Cit Masters Report Libre PDFTohko AmanoNo ratings yet

- An Integrated Fuzzy AHP and TOPSIS Appro PDFDocument25 pagesAn Integrated Fuzzy AHP and TOPSIS Appro PDFMarco Antônio SabaráNo ratings yet

- RM Module 1Document58 pagesRM Module 1Bhavani B S PoojaNo ratings yet

- Probability Ans StatisticsDocument40 pagesProbability Ans StatisticsSANTOSH K RACHARLA100% (1)

- Big Data AnalyticsDocument5 pagesBig Data AnalyticsPraveen KumarNo ratings yet

- Data Science Batch 9Document19 pagesData Science Batch 9Ardelia ParamestiNo ratings yet

- 02 Basic Prohibitions and EthicsDocument39 pages02 Basic Prohibitions and EthicsAmirah ShukriNo ratings yet

- Intelligent Decision Support in Auditing: Big Data and Machine Learning ApproachDocument7 pagesIntelligent Decision Support in Auditing: Big Data and Machine Learning ApproachClaudiu BrandasNo ratings yet

- 2017 - Sarstedt Et Al. - Handbook of Market Research PDFDocument41 pages2017 - Sarstedt Et Al. - Handbook of Market Research PDFF Cristina QueirozNo ratings yet

- Sas AnalyticsDocument35 pagesSas AnalyticsprakashnethaNo ratings yet

- Substantive Testing, Computer-Assisted Audit Techniques and Audit ProgrammesDocument23 pagesSubstantive Testing, Computer-Assisted Audit Techniques and Audit ProgrammesAnnaNo ratings yet

- Data Science With Python (Foundation) - Assignments - Case Studies PDFDocument3 pagesData Science With Python (Foundation) - Assignments - Case Studies PDFData Analyst100% (1)

- Financial Modeling Case Study (Enercon)Document2 pagesFinancial Modeling Case Study (Enercon)Wee Kiat LeeNo ratings yet

- Business Analytics-UNIt 1 ReDocument18 pagesBusiness Analytics-UNIt 1 Remayank.rockstarmayank.singh100% (1)

- Halaman 1 Dari 8Document8 pagesHalaman 1 Dari 8rizkiNo ratings yet

- Logistics Decision Analysis Methods: Analytic Hierarchy ProcessDocument62 pagesLogistics Decision Analysis Methods: Analytic Hierarchy ProcessKhalis MahmudahNo ratings yet

- CSR Funds in Banking Sector As An Effective Means For Financial Inclusion Initiatives in India 756999930Document4 pagesCSR Funds in Banking Sector As An Effective Means For Financial Inclusion Initiatives in India 756999930SaurabhNo ratings yet

- Statistik DeskriptifDocument33 pagesStatistik Deskriptifnurul shabrinaNo ratings yet

- Islamic Finance - Ethics, Concepts, Practice PDFDocument130 pagesIslamic Finance - Ethics, Concepts, Practice PDFMuhammad TalhaNo ratings yet

- Workshop: Intermediate 3 Data Science: Image Processing On R and PythonDocument3 pagesWorkshop: Intermediate 3 Data Science: Image Processing On R and PythonHeru Wiryanto100% (1)

- Bumper BookDocument90 pagesBumper BookPaulo Henrique NascimentoNo ratings yet

- Zoro Financial Modelling Case FMCGDocument10 pagesZoro Financial Modelling Case FMCGDhruvil GosaliaNo ratings yet

- Turban Bi2e PP Ch02Document48 pagesTurban Bi2e PP Ch02julianNo ratings yet

- Stats Chap03 BlumanDocument86 pagesStats Chap03 BlumanAnonymous IlzpPFINo ratings yet

- TM 01 Beams Aa13e PPT 16 EditedDocument43 pagesTM 01 Beams Aa13e PPT 16 EditedNigella SativaNo ratings yet

- Forecasting of Stock Prices Using Multi Layer PerceptronDocument6 pagesForecasting of Stock Prices Using Multi Layer Perceptronijbui iir100% (1)

- Bifurcation Analysis of The Modified Lotka-Volterra Prey-Predator ModelDocument44 pagesBifurcation Analysis of The Modified Lotka-Volterra Prey-Predator ModelMiliyon TilahunNo ratings yet

- Cooper&Schindler Chap7Document23 pagesCooper&Schindler Chap729_ramesh170100% (1)

- Data Science: Chapter 1: Introduction To Big DataDocument77 pagesData Science: Chapter 1: Introduction To Big DataHrishikesh Dabeer100% (2)

- New Time Series AnalysisDocument16 pagesNew Time Series AnalysisrakinsadaftabNo ratings yet

- Week 8a - Interval EstimationDocument43 pagesWeek 8a - Interval Estimation_vanitykNo ratings yet

- Statistics For Data Science - 1Document38 pagesStatistics For Data Science - 1Akash Srivastava100% (1)

- Unit-Ii: Data Analysis: Editing, Coding, Transformation of DataDocument9 pagesUnit-Ii: Data Analysis: Editing, Coding, Transformation of DataDurga Prasad NallaNo ratings yet

- CH - 14 - Advanced Panel Data MethodsDocument12 pagesCH - 14 - Advanced Panel Data MethodsHiếu DươngNo ratings yet

- MRP L&LLDocument15 pagesMRP L&LLmery dollNo ratings yet

- Audit Program Ppi (Mariani, SKM, Mha)Document23 pagesAudit Program Ppi (Mariani, SKM, Mha)Dedy HartantyoNo ratings yet

- IPPTChap 011Document28 pagesIPPTChap 011Tia Chrisna MurtiNo ratings yet

- Processing and Analyzing Data: Construction Management ChairDocument29 pagesProcessing and Analyzing Data: Construction Management ChairhayelomNo ratings yet

- Operational Risk ManagementDocument43 pagesOperational Risk ManagementJames Abueg Escaño100% (2)

- Module 2 - Introduction To FS AuditDocument5 pagesModule 2 - Introduction To FS AuditLysss EpssssNo ratings yet

- Chapter 7 AuditingDocument25 pagesChapter 7 AuditingMisshtaCNo ratings yet

- CS601 - Data Communication Updated HandoutsDocument805 pagesCS601 - Data Communication Updated HandoutsSUFYANNo ratings yet

- Sanchar: License Free Walkie - Talkie ETA-SD-20200201124Document2 pagesSanchar: License Free Walkie - Talkie ETA-SD-20200201124iamdenny2024No ratings yet

- 11 Fabm1 Q3 - M2Document11 pages11 Fabm1 Q3 - M2Syrwin SedaNo ratings yet

- Islamic Finace TutorialDocument6 pagesIslamic Finace Tutorialgom3awy2003No ratings yet

- Health System Director Administrator in Columbus OH Resume Cheryl GuymanDocument2 pagesHealth System Director Administrator in Columbus OH Resume Cheryl GuymanCherylGuymanNo ratings yet

- Total Amount: 1251.00 Adjust Coupon Amount: 0.00 Payable Amount: 1251.00Document2 pagesTotal Amount: 1251.00 Adjust Coupon Amount: 0.00 Payable Amount: 1251.00harikrushnaNo ratings yet

- DLCPM25314400000017730 2023Document2 pagesDLCPM25314400000017730 2023Shri MedhiniNo ratings yet

- Howard University Hospital Media Policy FAQsDocument2 pagesHoward University Hospital Media Policy FAQsshervon pascallNo ratings yet

- Clarification Regarding Special Offer - FAQDocument3 pagesClarification Regarding Special Offer - FAQShekhar PrasadNo ratings yet

- FinDestination ProfileDocument6 pagesFinDestination ProfileReetam halderNo ratings yet

- Malpractice Proposal-Aijaz-NewDocument2 pagesMalpractice Proposal-Aijaz-NewGalaleldin AliNo ratings yet

- MULTIPLE CHOICE: Select The Best Answer From The Choices and Write The Letter That Corresponds To Your Answer On The Answer SheetDocument2 pagesMULTIPLE CHOICE: Select The Best Answer From The Choices and Write The Letter That Corresponds To Your Answer On The Answer SheetSuper MelonNo ratings yet

- Agriculture 6 Weekly Test #6Document3 pagesAgriculture 6 Weekly Test #6lhe.magaoayNo ratings yet

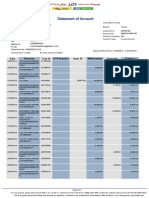

- Statement of Account: Date Tran Id Remarks UTR Number Instr. ID Withdrawals Deposits BalanceDocument8 pagesStatement of Account: Date Tran Id Remarks UTR Number Instr. ID Withdrawals Deposits Balancedinesh namdeoNo ratings yet

- CCMF Fund - Financial Statements - 2019Document8 pagesCCMF Fund - Financial Statements - 2019Cindy BartolayNo ratings yet

- What Is Microsoft TeamsDocument3 pagesWhat Is Microsoft TeamsNoreen GounderNo ratings yet

- Equity and Debt Pending NotesDocument18 pagesEquity and Debt Pending NotesAbbas BengaliwalaNo ratings yet

- StatementDocument5 pagesStatementgabrielsg3No ratings yet

- MicroservicesDocument9 pagesMicroservicesJimmy KumarNo ratings yet

- Core KPI Formulas Agreed 20211004Document3 pagesCore KPI Formulas Agreed 20211004nathaniel07No ratings yet

- CDM-FDM TDMDocument23 pagesCDM-FDM TDMjwmvandeven8045100% (1)

- UNYS Amazon PPC ReportDocument1 pageUNYS Amazon PPC ReportPanfletinho 2No ratings yet

- Resume Template 2Document4 pagesResume Template 2anwar0sadat-3No ratings yet

- Irm Module 1Document38 pagesIrm Module 1Durga Prasad DashNo ratings yet

- Nobles Acctg10 PPT 01Document61 pagesNobles Acctg10 PPT 01Tayar ElieNo ratings yet

- Bafin Chap 1Document2 pagesBafin Chap 1Philip DizonNo ratings yet

- Project Report ON "Customer Satisfaction Regarding HDFC Bank"Document63 pagesProject Report ON "Customer Satisfaction Regarding HDFC Bank"BHARATNo ratings yet

- Black Book Anuj ShahDocument37 pagesBlack Book Anuj Shahmanan141090No ratings yet

- Marketing Strategies of ViDocument10 pagesMarketing Strategies of ViAshmil AliarNo ratings yet

- Visa Public Key Infrastructure Certificate PolicyDocument80 pagesVisa Public Key Infrastructure Certificate PolicyDen Maz PoerNo ratings yet

Download as pptx, pdf, or txt

You might also like

- Rye, C. (2001) Change Management The 5 Step ToolkitDocument59 pagesRye, C. (2001) Change Management The 5 Step ToolkitIleana SendreaNo ratings yet

- 5 - Ratio Regression and Difference Estimation - RevisedDocument39 pages5 - Ratio Regression and Difference Estimation - RevisedFiqry ZolkofiliNo ratings yet

- 6 Accountability and Auditing in The Public Sector (Nota)Document63 pages6 Accountability and Auditing in The Public Sector (Nota)cik bungaNo ratings yet

- Prelim Ch5Document14 pagesPrelim Ch5Cathleen Drew TuazonNo ratings yet

- Innovations in Public Sector Internal Audit: Case of IndonesiaDocument21 pagesInnovations in Public Sector Internal Audit: Case of IndonesiaMarlon StafinNo ratings yet

- Field BalancingsDocument51 pagesField BalancingsTaraknath MukherjeeNo ratings yet

- Research-Ch-4 - Sampling DesignDocument42 pagesResearch-Ch-4 - Sampling Designaddisyawkal18No ratings yet

- Basics of Company Act.Document10 pagesBasics of Company Act.neha kailleyNo ratings yet

- Introduction To Difference-In-Differences DesignDocument18 pagesIntroduction To Difference-In-Differences DesignDadan KosasihNo ratings yet

- Report Balancing 255 FDocument1 pageReport Balancing 255 Feka septianaNo ratings yet

- AEB14 SM CH15 v2Document24 pagesAEB14 SM CH15 v2RonLiu35No ratings yet

- ch09 - PPT - Rankin - 2e RevDocument37 pagesch09 - PPT - Rankin - 2e Revmichele hazelNo ratings yet

- Time Series Analysis and ForecastingDocument69 pagesTime Series Analysis and ForecastingSumendra RaghavNo ratings yet

- Environmental AccountingDocument27 pagesEnvironmental AccountingFaresh Haroon100% (1)

- AEB14 SM CH17 v2Document31 pagesAEB14 SM CH17 v2RonLiu350% (1)

- Assurance Engagements and Internal Audit and Sections On Public Sector and Charity Audits - pp15Document41 pagesAssurance Engagements and Internal Audit and Sections On Public Sector and Charity Audits - pp15dhea100% (1)

- Maximizing The Value of A Risk-Based Audit Plan.Document4 pagesMaximizing The Value of A Risk-Based Audit Plan.Arco Priyo DirgantoroNo ratings yet

- 2.3 Section Properties of Built-Up Steel SectionsDocument5 pages2.3 Section Properties of Built-Up Steel SectionsKen SmithNo ratings yet

- Course Title: Data Pre-Processing and VisualizationDocument11 pagesCourse Title: Data Pre-Processing and VisualizationIntekhab Aslam100% (2)

- Karanja Evanson Mwangi Cit Masters Report Libre PDFDocument136 pagesKaranja Evanson Mwangi Cit Masters Report Libre PDFTohko AmanoNo ratings yet

- An Integrated Fuzzy AHP and TOPSIS Appro PDFDocument25 pagesAn Integrated Fuzzy AHP and TOPSIS Appro PDFMarco Antônio SabaráNo ratings yet

- RM Module 1Document58 pagesRM Module 1Bhavani B S PoojaNo ratings yet

- Probability Ans StatisticsDocument40 pagesProbability Ans StatisticsSANTOSH K RACHARLA100% (1)

- Big Data AnalyticsDocument5 pagesBig Data AnalyticsPraveen KumarNo ratings yet

- Data Science Batch 9Document19 pagesData Science Batch 9Ardelia ParamestiNo ratings yet

- 02 Basic Prohibitions and EthicsDocument39 pages02 Basic Prohibitions and EthicsAmirah ShukriNo ratings yet

- Intelligent Decision Support in Auditing: Big Data and Machine Learning ApproachDocument7 pagesIntelligent Decision Support in Auditing: Big Data and Machine Learning ApproachClaudiu BrandasNo ratings yet

- 2017 - Sarstedt Et Al. - Handbook of Market Research PDFDocument41 pages2017 - Sarstedt Et Al. - Handbook of Market Research PDFF Cristina QueirozNo ratings yet

- Sas AnalyticsDocument35 pagesSas AnalyticsprakashnethaNo ratings yet

- Substantive Testing, Computer-Assisted Audit Techniques and Audit ProgrammesDocument23 pagesSubstantive Testing, Computer-Assisted Audit Techniques and Audit ProgrammesAnnaNo ratings yet

- Data Science With Python (Foundation) - Assignments - Case Studies PDFDocument3 pagesData Science With Python (Foundation) - Assignments - Case Studies PDFData Analyst100% (1)

- Financial Modeling Case Study (Enercon)Document2 pagesFinancial Modeling Case Study (Enercon)Wee Kiat LeeNo ratings yet

- Business Analytics-UNIt 1 ReDocument18 pagesBusiness Analytics-UNIt 1 Remayank.rockstarmayank.singh100% (1)

- Halaman 1 Dari 8Document8 pagesHalaman 1 Dari 8rizkiNo ratings yet

- Logistics Decision Analysis Methods: Analytic Hierarchy ProcessDocument62 pagesLogistics Decision Analysis Methods: Analytic Hierarchy ProcessKhalis MahmudahNo ratings yet

- CSR Funds in Banking Sector As An Effective Means For Financial Inclusion Initiatives in India 756999930Document4 pagesCSR Funds in Banking Sector As An Effective Means For Financial Inclusion Initiatives in India 756999930SaurabhNo ratings yet

- Statistik DeskriptifDocument33 pagesStatistik Deskriptifnurul shabrinaNo ratings yet

- Islamic Finance - Ethics, Concepts, Practice PDFDocument130 pagesIslamic Finance - Ethics, Concepts, Practice PDFMuhammad TalhaNo ratings yet

- Workshop: Intermediate 3 Data Science: Image Processing On R and PythonDocument3 pagesWorkshop: Intermediate 3 Data Science: Image Processing On R and PythonHeru Wiryanto100% (1)

- Bumper BookDocument90 pagesBumper BookPaulo Henrique NascimentoNo ratings yet

- Zoro Financial Modelling Case FMCGDocument10 pagesZoro Financial Modelling Case FMCGDhruvil GosaliaNo ratings yet

- Turban Bi2e PP Ch02Document48 pagesTurban Bi2e PP Ch02julianNo ratings yet

- Stats Chap03 BlumanDocument86 pagesStats Chap03 BlumanAnonymous IlzpPFINo ratings yet

- TM 01 Beams Aa13e PPT 16 EditedDocument43 pagesTM 01 Beams Aa13e PPT 16 EditedNigella SativaNo ratings yet

- Forecasting of Stock Prices Using Multi Layer PerceptronDocument6 pagesForecasting of Stock Prices Using Multi Layer Perceptronijbui iir100% (1)

- Bifurcation Analysis of The Modified Lotka-Volterra Prey-Predator ModelDocument44 pagesBifurcation Analysis of The Modified Lotka-Volterra Prey-Predator ModelMiliyon TilahunNo ratings yet

- Cooper&Schindler Chap7Document23 pagesCooper&Schindler Chap729_ramesh170100% (1)

- Data Science: Chapter 1: Introduction To Big DataDocument77 pagesData Science: Chapter 1: Introduction To Big DataHrishikesh Dabeer100% (2)

- New Time Series AnalysisDocument16 pagesNew Time Series AnalysisrakinsadaftabNo ratings yet

- Week 8a - Interval EstimationDocument43 pagesWeek 8a - Interval Estimation_vanitykNo ratings yet

- Statistics For Data Science - 1Document38 pagesStatistics For Data Science - 1Akash Srivastava100% (1)

- Unit-Ii: Data Analysis: Editing, Coding, Transformation of DataDocument9 pagesUnit-Ii: Data Analysis: Editing, Coding, Transformation of DataDurga Prasad NallaNo ratings yet

- CH - 14 - Advanced Panel Data MethodsDocument12 pagesCH - 14 - Advanced Panel Data MethodsHiếu DươngNo ratings yet

- MRP L&LLDocument15 pagesMRP L&LLmery dollNo ratings yet

- Audit Program Ppi (Mariani, SKM, Mha)Document23 pagesAudit Program Ppi (Mariani, SKM, Mha)Dedy HartantyoNo ratings yet

- IPPTChap 011Document28 pagesIPPTChap 011Tia Chrisna MurtiNo ratings yet

- Processing and Analyzing Data: Construction Management ChairDocument29 pagesProcessing and Analyzing Data: Construction Management ChairhayelomNo ratings yet

- Operational Risk ManagementDocument43 pagesOperational Risk ManagementJames Abueg Escaño100% (2)

- Module 2 - Introduction To FS AuditDocument5 pagesModule 2 - Introduction To FS AuditLysss EpssssNo ratings yet

- Chapter 7 AuditingDocument25 pagesChapter 7 AuditingMisshtaCNo ratings yet

- CS601 - Data Communication Updated HandoutsDocument805 pagesCS601 - Data Communication Updated HandoutsSUFYANNo ratings yet

- Sanchar: License Free Walkie - Talkie ETA-SD-20200201124Document2 pagesSanchar: License Free Walkie - Talkie ETA-SD-20200201124iamdenny2024No ratings yet

- 11 Fabm1 Q3 - M2Document11 pages11 Fabm1 Q3 - M2Syrwin SedaNo ratings yet

- Islamic Finace TutorialDocument6 pagesIslamic Finace Tutorialgom3awy2003No ratings yet

- Health System Director Administrator in Columbus OH Resume Cheryl GuymanDocument2 pagesHealth System Director Administrator in Columbus OH Resume Cheryl GuymanCherylGuymanNo ratings yet

- Total Amount: 1251.00 Adjust Coupon Amount: 0.00 Payable Amount: 1251.00Document2 pagesTotal Amount: 1251.00 Adjust Coupon Amount: 0.00 Payable Amount: 1251.00harikrushnaNo ratings yet

- DLCPM25314400000017730 2023Document2 pagesDLCPM25314400000017730 2023Shri MedhiniNo ratings yet

- Howard University Hospital Media Policy FAQsDocument2 pagesHoward University Hospital Media Policy FAQsshervon pascallNo ratings yet

- Clarification Regarding Special Offer - FAQDocument3 pagesClarification Regarding Special Offer - FAQShekhar PrasadNo ratings yet

- FinDestination ProfileDocument6 pagesFinDestination ProfileReetam halderNo ratings yet

- Malpractice Proposal-Aijaz-NewDocument2 pagesMalpractice Proposal-Aijaz-NewGalaleldin AliNo ratings yet

- MULTIPLE CHOICE: Select The Best Answer From The Choices and Write The Letter That Corresponds To Your Answer On The Answer SheetDocument2 pagesMULTIPLE CHOICE: Select The Best Answer From The Choices and Write The Letter That Corresponds To Your Answer On The Answer SheetSuper MelonNo ratings yet

- Agriculture 6 Weekly Test #6Document3 pagesAgriculture 6 Weekly Test #6lhe.magaoayNo ratings yet

- Statement of Account: Date Tran Id Remarks UTR Number Instr. ID Withdrawals Deposits BalanceDocument8 pagesStatement of Account: Date Tran Id Remarks UTR Number Instr. ID Withdrawals Deposits Balancedinesh namdeoNo ratings yet

- CCMF Fund - Financial Statements - 2019Document8 pagesCCMF Fund - Financial Statements - 2019Cindy BartolayNo ratings yet

- What Is Microsoft TeamsDocument3 pagesWhat Is Microsoft TeamsNoreen GounderNo ratings yet

- Equity and Debt Pending NotesDocument18 pagesEquity and Debt Pending NotesAbbas BengaliwalaNo ratings yet

- StatementDocument5 pagesStatementgabrielsg3No ratings yet

- MicroservicesDocument9 pagesMicroservicesJimmy KumarNo ratings yet

- Core KPI Formulas Agreed 20211004Document3 pagesCore KPI Formulas Agreed 20211004nathaniel07No ratings yet

- CDM-FDM TDMDocument23 pagesCDM-FDM TDMjwmvandeven8045100% (1)

- UNYS Amazon PPC ReportDocument1 pageUNYS Amazon PPC ReportPanfletinho 2No ratings yet

- Resume Template 2Document4 pagesResume Template 2anwar0sadat-3No ratings yet

- Irm Module 1Document38 pagesIrm Module 1Durga Prasad DashNo ratings yet

- Nobles Acctg10 PPT 01Document61 pagesNobles Acctg10 PPT 01Tayar ElieNo ratings yet

- Bafin Chap 1Document2 pagesBafin Chap 1Philip DizonNo ratings yet

- Project Report ON "Customer Satisfaction Regarding HDFC Bank"Document63 pagesProject Report ON "Customer Satisfaction Regarding HDFC Bank"BHARATNo ratings yet

- Black Book Anuj ShahDocument37 pagesBlack Book Anuj Shahmanan141090No ratings yet

- Marketing Strategies of ViDocument10 pagesMarketing Strategies of ViAshmil AliarNo ratings yet

- Visa Public Key Infrastructure Certificate PolicyDocument80 pagesVisa Public Key Infrastructure Certificate PolicyDen Maz PoerNo ratings yet