Download as ppt, pdf, or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5835)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (903)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (350)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (824)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (405)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Business Valuation: by Ca. Aparna RammohanDocument46 pagesBusiness Valuation: by Ca. Aparna RammohanAvinash SharmaNo ratings yet

- Maneesh Capstone 2 FinalDocument45 pagesManeesh Capstone 2 FinalRakesh SinghNo ratings yet

- FM423 Practice Exam IIDocument7 pagesFM423 Practice Exam IIruonanNo ratings yet

- SAP Best Practice Design - S4HANA 1709 Transfer Prices.v1Document71 pagesSAP Best Practice Design - S4HANA 1709 Transfer Prices.v1DipomoySaha100% (1)

- Towards An Agreed Body of Knowledge, Understanding, Skills and Expertise For Managers: Managing in Turbulent TimesDocument10 pagesTowards An Agreed Body of Knowledge, Understanding, Skills and Expertise For Managers: Managing in Turbulent TimesAnonymous nD4KwhNo ratings yet

- Misplaced Modifiers: Usage - Modifier ProblemsDocument8 pagesMisplaced Modifiers: Usage - Modifier ProblemsAnonymous nD4KwhNo ratings yet

- CER ThailandDocument30 pagesCER ThailandAnonymous nD4KwhNo ratings yet

- Mouth Communications and Opinion Leadership Model Fit Epinions On The InternetDocument31 pagesMouth Communications and Opinion Leadership Model Fit Epinions On The InternetAnonymous nD4KwhNo ratings yet

- Chapter 2 Cultural PatternsDocument51 pagesChapter 2 Cultural PatternsAnonymous nD4KwhNo ratings yet

- Understanding Financial StatementsDocument60 pagesUnderstanding Financial StatementsAnonymous nD4Kwh100% (1)

- What Is Strategy and Why Is It Important?Document17 pagesWhat Is Strategy and Why Is It Important?Anonymous nD4KwhNo ratings yet

- Byproduct AccountingDocument13 pagesByproduct AccountingAbu NaserNo ratings yet

- ACCA F2 VariancesDocument12 pagesACCA F2 VariancesLiam Bourke50% (2)

- Handout Classification of TakafulDocument10 pagesHandout Classification of TakafulLail M PimadaNo ratings yet

- BAF India - Policy On Moratorium On EMI - COVID 19 Regulatory PackageDocument5 pagesBAF India - Policy On Moratorium On EMI - COVID 19 Regulatory PackageLax MishraNo ratings yet

- C B E M: WWW - Isap.edu - PH Adminoffice@isap - Edu.phDocument5 pagesC B E M: WWW - Isap.edu - PH Adminoffice@isap - Edu.phJohn Mark PalapuzNo ratings yet

- ACCY 2002 Fall 2013 Quiz # 5 - Chapter 7 DUE October 20thDocument4 pagesACCY 2002 Fall 2013 Quiz # 5 - Chapter 7 DUE October 20thRad WimpsNo ratings yet

- Engro's Annual Report 2008Document189 pagesEngro's Annual Report 2008shahidamin1100% (2)

- A EduAchieve JunDocument14 pagesA EduAchieve JunkimikononNo ratings yet

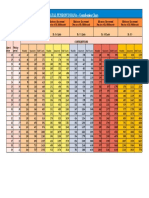

- Apy ChartDocument1 pageApy ChartMohit PathaniaNo ratings yet

- JPMorgan PaperDocument30 pagesJPMorgan PaperJan2050No ratings yet

- 3i Infotech-Developing A Hybrid StrategyDocument20 pages3i Infotech-Developing A Hybrid StrategyVinod JoshiNo ratings yet

- Green Shoe OptionDocument15 pagesGreen Shoe OptionNadeem Ahmad100% (1)

- CPJ Annual Report 2021Document98 pagesCPJ Annual Report 2021Samuel HamiltonNo ratings yet

- VDO-digitCare - 1899230702029742 - SCHEDULE 3Document2 pagesVDO-digitCare - 1899230702029742 - SCHEDULE 3Rahil ShekhNo ratings yet

- Sales Management Meeting - May 24-25 2016Document229 pagesSales Management Meeting - May 24-25 2016Emilian NeculaNo ratings yet

- Adobe Scan 14 Apr 2023Document1 pageAdobe Scan 14 Apr 2023srii21rohithNo ratings yet

- Chapter 4 Sources of Income PDFDocument5 pagesChapter 4 Sources of Income PDFkimberly tenebroNo ratings yet

- Introduction To Project AppraisalDocument3 pagesIntroduction To Project AppraisalGerald Maginga100% (2)

- Behavioral - Investment Banking InterviewsDocument12 pagesBehavioral - Investment Banking InterviewsIanNo ratings yet

- The Mauritius Route: The Indian Response: S L U S LDocument16 pagesThe Mauritius Route: The Indian Response: S L U S LAbhinav SwarajNo ratings yet

- HDMF Citizens CharterDocument24 pagesHDMF Citizens CharterEarl Russell S PaulicanNo ratings yet

- Personal Monthly BudgetDocument3 pagesPersonal Monthly BudgetCatherine MahuguNo ratings yet

- XBMA 2017 Annual ReviewDocument23 pagesXBMA 2017 Annual Reviewvfb74No ratings yet

- FWD: Nesl - Request To Authenticate: Nesliu@Nesl - Co.InDocument2 pagesFWD: Nesl - Request To Authenticate: Nesliu@Nesl - Co.InSagar GuptaNo ratings yet

- CB Sof SimplylifeDocument9 pagesCB Sof Simplylifekich unnyNo ratings yet

- U3A2 - Recording Transactions in A Journal - TemplateDocument3 pagesU3A2 - Recording Transactions in A Journal - TemplateJay PatelNo ratings yet