Accounting Salam: Fachrullah (14312437) Hilman Lutfan Iqro Asmi Mohammad Jordy Krisnawan P

Accounting Salam: Fachrullah (14312437) Hilman Lutfan Iqro Asmi Mohammad Jordy Krisnawan P

You might also like

- Options Trading Crash Course: The #1 Beginner's Guide to Make Money with Trading Options in 7 Days or Less!From EverandOptions Trading Crash Course: The #1 Beginner's Guide to Make Money with Trading Options in 7 Days or Less!Rating: 4.5 out of 5 stars4.5/5 (7)

- Islamic Finance (Self Made Notes)Document8 pagesIslamic Finance (Self Made Notes)Muhammad Hamza AyoubNo ratings yet

- Bai Al UrbunDocument8 pagesBai Al UrbunSiti Hajar Ghazali100% (2)

- LAW ON SALES Art 1521 1641Document90 pagesLAW ON SALES Art 1521 1641Lyka Nicole DoradoNo ratings yet

- Chapter 8 Salam-16032020-034603amDocument10 pagesChapter 8 Salam-16032020-034603amTaimoorJavedNo ratings yet

- Bay' SALAMDocument21 pagesBay' SALAMHobi MonieNo ratings yet

- Islamic Finance: By: Abdul MoueedDocument30 pagesIslamic Finance: By: Abdul MoueedALI SHER HaidriNo ratings yet

- Bay Al-Salam (Forward Sale)Document30 pagesBay Al-Salam (Forward Sale)Nurul 'Aqilah HhrifinNo ratings yet

- Bai Salam and Bai IstisnaDocument11 pagesBai Salam and Bai Istisnaamnajamil0001No ratings yet

- SalamDocument5 pagesSalamdipanajnNo ratings yet

- Baisalamistisna 110103082540 Phpapp02Document29 pagesBaisalamistisna 110103082540 Phpapp02maria9002No ratings yet

- Islamic Modes of FinanceDocument23 pagesIslamic Modes of FinanceKassahun EssaNo ratings yet

- Bay Assalam (Rangka IBF)Document11 pagesBay Assalam (Rangka IBF)syarafanaNo ratings yet

- Commercial Law-DoneDocument17 pagesCommercial Law-Doneraina mattNo ratings yet

- Presentation (Sale of G.a2003) - in Of03Document25 pagesPresentation (Sale of G.a2003) - in Of03Tanvi AmberkarNo ratings yet

- 4.3-Salam & IstisnaDocument32 pages4.3-Salam & IstisnaAllauddinaghaNo ratings yet

- 14-Salam and IstisnaDocument5 pages14-Salam and Istisna✬ SHANZA MALIK ✬No ratings yet

- Contract of Sale of GoodsDocument2 pagesContract of Sale of GoodsAsad UllahNo ratings yet

- The Sale OF Goods ActDocument58 pagesThe Sale OF Goods ActANJUPOONIANo ratings yet

- Salam, Istisna, SarfDocument42 pagesSalam, Istisna, SarfSari ManiraNo ratings yet

- Ch-18 Sale of Goods Act, 1930 Unpaid Seller and His RightsDocument7 pagesCh-18 Sale of Goods Act, 1930 Unpaid Seller and His RightsShivang SrivastavaNo ratings yet

- Islamic Modes of FinanceDocument61 pagesIslamic Modes of Financegom3awy2003No ratings yet

- Talaboc Week3Document5 pagesTalaboc Week3Carolyn TalabocNo ratings yet

- Maxim Bay Al SalamDocument17 pagesMaxim Bay Al SalamNaim ARNo ratings yet

- Obligations of The VendeeDocument55 pagesObligations of The VendeerchllmclnNo ratings yet

- Business LawDocument41 pagesBusiness LawttirvNo ratings yet

- Islamic Banking & Finance: International Islamic University IslamabadDocument13 pagesIslamic Banking & Finance: International Islamic University IslamabadurjaveedNo ratings yet

- Islamic Modes of FinancingDocument38 pagesIslamic Modes of FinancingMuhammad Shahzeb KhanNo ratings yet

- Bai SalamDocument2 pagesBai Salamkanwal1234No ratings yet

- Islamic Banking-Ijarah & Murabaha ( )Document52 pagesIslamic Banking-Ijarah & Murabaha ( )Naveed Abdullah100% (1)

- Unpaid Seller Rights & RemediesDocument12 pagesUnpaid Seller Rights & RemediesPrabodh KuncheNo ratings yet

- Business Law 5Document41 pagesBusiness Law 5Life BloggerNo ratings yet

- Rights of Unpaid SellerDocument3 pagesRights of Unpaid Sellerravurirajkumar2005No ratings yet

- 2 Conditions WarrantyDocument21 pages2 Conditions WarrantyRohita PadimitiNo ratings yet

- UntitledDocument20 pagesUntitledDr. Arif RahmanNo ratings yet

- Chapter 6 Purchasing and Selling ProceduresDocument9 pagesChapter 6 Purchasing and Selling ProceduresellengaoneNo ratings yet

- UIB2612 1630 LECTURE 6 MurabahahDocument32 pagesUIB2612 1630 LECTURE 6 MurabahahSyahirah ArifNo ratings yet

- Bai SalamDocument24 pagesBai SalamM Azaan OwaisNo ratings yet

- Salam & IstisnaDocument30 pagesSalam & IstisnaMUHAMMAD TALATNo ratings yet

- Sale of GoodsDocument6 pagesSale of GoodsErum AnwerNo ratings yet

- Transfer Ownership of The Goods and Deliver The Goods: BAREBUSX - QuestionnaireDocument18 pagesTransfer Ownership of The Goods and Deliver The Goods: BAREBUSX - QuestionnaireKaye L. Dela CruzNo ratings yet

- A Sells Goods To B, at Rs. 15,000/-A Passes OnDocument7 pagesA Sells Goods To B, at Rs. 15,000/-A Passes OnAdv Sohail BhattiNo ratings yet

- Perfomance of The Contract of SaleDocument2 pagesPerfomance of The Contract of SaleMwika MusakuziNo ratings yet

- SPA AU BGC Dec 2022 BRC v1.3Document5 pagesSPA AU BGC Dec 2022 BRC v1.3Mond MondNo ratings yet

- SalamDocument12 pagesSalamqurathNo ratings yet

- LAB - Sale of Goods ActDocument33 pagesLAB - Sale of Goods Actaayush DanielNo ratings yet

- What Are The Rights of An Unpaid Seller - IpleadersDocument9 pagesWhat Are The Rights of An Unpaid Seller - IpleadersVivek TiwariNo ratings yet

- Rights of Unpaid Seller - Legal Study MaterialDocument8 pagesRights of Unpaid Seller - Legal Study MaterialSreepathi ShettyNo ratings yet

- Sale of Goods ActDocument10 pagesSale of Goods Actsowjanya kandukuriNo ratings yet

- Salam and Parallel SalamDocument5 pagesSalam and Parallel SalamTayyab AhmadNo ratings yet

- Rights of Unpaid Seller: BY SUNIL (9030) Aditya Kankani (9039) NARESH GADE (9055) Lakshman (90) ANUSHADocument17 pagesRights of Unpaid Seller: BY SUNIL (9030) Aditya Kankani (9039) NARESH GADE (9055) Lakshman (90) ANUSHAAditya KankaniNo ratings yet

- Chap 2 Part 2Document56 pagesChap 2 Part 2zakirah zalmieNo ratings yet

- Property Law Answer GuidesDocument46 pagesProperty Law Answer Guidesmattyt85No ratings yet

- Rights of Unpaid SellerDocument16 pagesRights of Unpaid SellerUtkarsh Sethi100% (1)

- Legal and TaxDocument35 pagesLegal and TaxSachin MethreeNo ratings yet

- Sale of GoodsDocument6 pagesSale of GoodsWANYAMA EMMANUELNo ratings yet

- Islamic Law of ContractDocument9 pagesIslamic Law of ContractMonju Grace100% (1)

- Cheer DanceDocument15 pagesCheer DanceElizabethNo ratings yet

- Certification 22000 Di Industri Kemasan Pangan: Analisis Pemenuhan Persyaratan Food Safety SystemDocument8 pagesCertification 22000 Di Industri Kemasan Pangan: Analisis Pemenuhan Persyaratan Food Safety SystemPeris tiantoNo ratings yet

- Naval Mines/Torpedoes Mines USA MK 67 SLMM Self-Propelled MineDocument2 pagesNaval Mines/Torpedoes Mines USA MK 67 SLMM Self-Propelled MinesmithNo ratings yet

- SAE Architecture PDFDocument54 pagesSAE Architecture PDFMirba mirbaNo ratings yet

- 3 MicroDocument4 pages3 MicroDumitraNo ratings yet

- ZeitgeistDocument1 pageZeitgeistNabiha NadeemNo ratings yet

- Ethics SyllabusDocument5 pagesEthics SyllabusprincessNo ratings yet

- Tom Swiss Weekly Mayoral PollDocument5 pagesTom Swiss Weekly Mayoral PollThe Daily LineNo ratings yet

- How To Test SMTP Services Manually in Windows ServerDocument14 pagesHow To Test SMTP Services Manually in Windows ServerHaftamu HailuNo ratings yet

- Dragon Capital 200906Document38 pagesDragon Capital 200906anraidNo ratings yet

- Section 14 HV Network DesignDocument11 pagesSection 14 HV Network DesignUsama AhmedNo ratings yet

- 2007 AmuDocument85 pages2007 AmuAnindyaMustikaNo ratings yet

- Opening RemarksDocument2 pagesOpening Remarksjennelyn malayno100% (1)

- Animation Thesis FilmDocument4 pagesAnimation Thesis Filmjuliemedinaphoenix100% (2)

- Information Before Stay BFDocument7 pagesInformation Before Stay BFBrat SiostraNo ratings yet

- Freeman v. Grain Processing Corp., No. 13-0723 (Iowa June 13, 2014)Document63 pagesFreeman v. Grain Processing Corp., No. 13-0723 (Iowa June 13, 2014)RHTNo ratings yet

- De Thi Giua Ki 2 Tieng Anh 8 Global Success de So 2Document21 pagesDe Thi Giua Ki 2 Tieng Anh 8 Global Success de So 2mit maiNo ratings yet

- Level 9Document9 pagesLevel 9direcciónc_1No ratings yet

- Case Study SIFFCO AGRO Chemicals Ltd.Document3 pagesCase Study SIFFCO AGRO Chemicals Ltd.AvinaNo ratings yet

- Stone Houses of Jefferson CountyDocument240 pagesStone Houses of Jefferson CountyAs PireNo ratings yet

- Bank of IndiaDocument63 pagesBank of IndiaArmaan ChhaprooNo ratings yet

- SV - ComplaintDocument72 pagesSV - ComplaintĐỗ Trà MyNo ratings yet

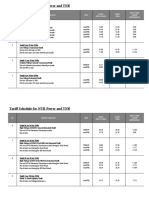

- TNB and NUR Tariff DifferencesDocument2 pagesTNB and NUR Tariff DifferencesAzree Mohd NoorNo ratings yet

- Documents in Credit TransactionsDocument6 pagesDocuments in Credit Transactionsgeofrey gepitulanNo ratings yet

- Holy Spirit in Christianity - WikipediaDocument21 pagesHoly Spirit in Christianity - WikipediaSunny BautistaNo ratings yet

- Attendance DenmarkDocument3 pagesAttendance Denmarkdennis berja laguraNo ratings yet

- Purposive Communication LectureDocument70 pagesPurposive Communication LectureJericho DadoNo ratings yet

- Spectra Precision FAST Survey User ManualDocument68 pagesSpectra Precision FAST Survey User ManualAlexis Olaf Montores CuNo ratings yet

- Customs Procedure CodesDocument23 pagesCustoms Procedure CodesJonathan D'limaNo ratings yet

- Solutions To Chapter 6 Valuing StocksDocument20 pagesSolutions To Chapter 6 Valuing StocksSam TnNo ratings yet

Download as pptx, pdf, or txt

You might also like

- Options Trading Crash Course: The #1 Beginner's Guide to Make Money with Trading Options in 7 Days or Less!From EverandOptions Trading Crash Course: The #1 Beginner's Guide to Make Money with Trading Options in 7 Days or Less!Rating: 4.5 out of 5 stars4.5/5 (7)

- Islamic Finance (Self Made Notes)Document8 pagesIslamic Finance (Self Made Notes)Muhammad Hamza AyoubNo ratings yet

- Bai Al UrbunDocument8 pagesBai Al UrbunSiti Hajar Ghazali100% (2)

- LAW ON SALES Art 1521 1641Document90 pagesLAW ON SALES Art 1521 1641Lyka Nicole DoradoNo ratings yet

- Chapter 8 Salam-16032020-034603amDocument10 pagesChapter 8 Salam-16032020-034603amTaimoorJavedNo ratings yet

- Bay' SALAMDocument21 pagesBay' SALAMHobi MonieNo ratings yet

- Islamic Finance: By: Abdul MoueedDocument30 pagesIslamic Finance: By: Abdul MoueedALI SHER HaidriNo ratings yet

- Bay Al-Salam (Forward Sale)Document30 pagesBay Al-Salam (Forward Sale)Nurul 'Aqilah HhrifinNo ratings yet

- Bai Salam and Bai IstisnaDocument11 pagesBai Salam and Bai Istisnaamnajamil0001No ratings yet

- SalamDocument5 pagesSalamdipanajnNo ratings yet

- Baisalamistisna 110103082540 Phpapp02Document29 pagesBaisalamistisna 110103082540 Phpapp02maria9002No ratings yet

- Islamic Modes of FinanceDocument23 pagesIslamic Modes of FinanceKassahun EssaNo ratings yet

- Bay Assalam (Rangka IBF)Document11 pagesBay Assalam (Rangka IBF)syarafanaNo ratings yet

- Commercial Law-DoneDocument17 pagesCommercial Law-Doneraina mattNo ratings yet

- Presentation (Sale of G.a2003) - in Of03Document25 pagesPresentation (Sale of G.a2003) - in Of03Tanvi AmberkarNo ratings yet

- 4.3-Salam & IstisnaDocument32 pages4.3-Salam & IstisnaAllauddinaghaNo ratings yet

- 14-Salam and IstisnaDocument5 pages14-Salam and Istisna✬ SHANZA MALIK ✬No ratings yet

- Contract of Sale of GoodsDocument2 pagesContract of Sale of GoodsAsad UllahNo ratings yet

- The Sale OF Goods ActDocument58 pagesThe Sale OF Goods ActANJUPOONIANo ratings yet

- Salam, Istisna, SarfDocument42 pagesSalam, Istisna, SarfSari ManiraNo ratings yet

- Ch-18 Sale of Goods Act, 1930 Unpaid Seller and His RightsDocument7 pagesCh-18 Sale of Goods Act, 1930 Unpaid Seller and His RightsShivang SrivastavaNo ratings yet

- Islamic Modes of FinanceDocument61 pagesIslamic Modes of Financegom3awy2003No ratings yet

- Talaboc Week3Document5 pagesTalaboc Week3Carolyn TalabocNo ratings yet

- Maxim Bay Al SalamDocument17 pagesMaxim Bay Al SalamNaim ARNo ratings yet

- Obligations of The VendeeDocument55 pagesObligations of The VendeerchllmclnNo ratings yet

- Business LawDocument41 pagesBusiness LawttirvNo ratings yet

- Islamic Banking & Finance: International Islamic University IslamabadDocument13 pagesIslamic Banking & Finance: International Islamic University IslamabadurjaveedNo ratings yet

- Islamic Modes of FinancingDocument38 pagesIslamic Modes of FinancingMuhammad Shahzeb KhanNo ratings yet

- Bai SalamDocument2 pagesBai Salamkanwal1234No ratings yet

- Islamic Banking-Ijarah & Murabaha ( )Document52 pagesIslamic Banking-Ijarah & Murabaha ( )Naveed Abdullah100% (1)

- Unpaid Seller Rights & RemediesDocument12 pagesUnpaid Seller Rights & RemediesPrabodh KuncheNo ratings yet

- Business Law 5Document41 pagesBusiness Law 5Life BloggerNo ratings yet

- Rights of Unpaid SellerDocument3 pagesRights of Unpaid Sellerravurirajkumar2005No ratings yet

- 2 Conditions WarrantyDocument21 pages2 Conditions WarrantyRohita PadimitiNo ratings yet

- UntitledDocument20 pagesUntitledDr. Arif RahmanNo ratings yet

- Chapter 6 Purchasing and Selling ProceduresDocument9 pagesChapter 6 Purchasing and Selling ProceduresellengaoneNo ratings yet

- UIB2612 1630 LECTURE 6 MurabahahDocument32 pagesUIB2612 1630 LECTURE 6 MurabahahSyahirah ArifNo ratings yet

- Bai SalamDocument24 pagesBai SalamM Azaan OwaisNo ratings yet

- Salam & IstisnaDocument30 pagesSalam & IstisnaMUHAMMAD TALATNo ratings yet

- Sale of GoodsDocument6 pagesSale of GoodsErum AnwerNo ratings yet

- Transfer Ownership of The Goods and Deliver The Goods: BAREBUSX - QuestionnaireDocument18 pagesTransfer Ownership of The Goods and Deliver The Goods: BAREBUSX - QuestionnaireKaye L. Dela CruzNo ratings yet

- A Sells Goods To B, at Rs. 15,000/-A Passes OnDocument7 pagesA Sells Goods To B, at Rs. 15,000/-A Passes OnAdv Sohail BhattiNo ratings yet

- Perfomance of The Contract of SaleDocument2 pagesPerfomance of The Contract of SaleMwika MusakuziNo ratings yet

- SPA AU BGC Dec 2022 BRC v1.3Document5 pagesSPA AU BGC Dec 2022 BRC v1.3Mond MondNo ratings yet

- SalamDocument12 pagesSalamqurathNo ratings yet

- LAB - Sale of Goods ActDocument33 pagesLAB - Sale of Goods Actaayush DanielNo ratings yet

- What Are The Rights of An Unpaid Seller - IpleadersDocument9 pagesWhat Are The Rights of An Unpaid Seller - IpleadersVivek TiwariNo ratings yet

- Rights of Unpaid Seller - Legal Study MaterialDocument8 pagesRights of Unpaid Seller - Legal Study MaterialSreepathi ShettyNo ratings yet

- Sale of Goods ActDocument10 pagesSale of Goods Actsowjanya kandukuriNo ratings yet

- Salam and Parallel SalamDocument5 pagesSalam and Parallel SalamTayyab AhmadNo ratings yet

- Rights of Unpaid Seller: BY SUNIL (9030) Aditya Kankani (9039) NARESH GADE (9055) Lakshman (90) ANUSHADocument17 pagesRights of Unpaid Seller: BY SUNIL (9030) Aditya Kankani (9039) NARESH GADE (9055) Lakshman (90) ANUSHAAditya KankaniNo ratings yet

- Chap 2 Part 2Document56 pagesChap 2 Part 2zakirah zalmieNo ratings yet

- Property Law Answer GuidesDocument46 pagesProperty Law Answer Guidesmattyt85No ratings yet

- Rights of Unpaid SellerDocument16 pagesRights of Unpaid SellerUtkarsh Sethi100% (1)

- Legal and TaxDocument35 pagesLegal and TaxSachin MethreeNo ratings yet

- Sale of GoodsDocument6 pagesSale of GoodsWANYAMA EMMANUELNo ratings yet

- Islamic Law of ContractDocument9 pagesIslamic Law of ContractMonju Grace100% (1)

- Cheer DanceDocument15 pagesCheer DanceElizabethNo ratings yet

- Certification 22000 Di Industri Kemasan Pangan: Analisis Pemenuhan Persyaratan Food Safety SystemDocument8 pagesCertification 22000 Di Industri Kemasan Pangan: Analisis Pemenuhan Persyaratan Food Safety SystemPeris tiantoNo ratings yet

- Naval Mines/Torpedoes Mines USA MK 67 SLMM Self-Propelled MineDocument2 pagesNaval Mines/Torpedoes Mines USA MK 67 SLMM Self-Propelled MinesmithNo ratings yet

- SAE Architecture PDFDocument54 pagesSAE Architecture PDFMirba mirbaNo ratings yet

- 3 MicroDocument4 pages3 MicroDumitraNo ratings yet

- ZeitgeistDocument1 pageZeitgeistNabiha NadeemNo ratings yet

- Ethics SyllabusDocument5 pagesEthics SyllabusprincessNo ratings yet

- Tom Swiss Weekly Mayoral PollDocument5 pagesTom Swiss Weekly Mayoral PollThe Daily LineNo ratings yet

- How To Test SMTP Services Manually in Windows ServerDocument14 pagesHow To Test SMTP Services Manually in Windows ServerHaftamu HailuNo ratings yet

- Dragon Capital 200906Document38 pagesDragon Capital 200906anraidNo ratings yet

- Section 14 HV Network DesignDocument11 pagesSection 14 HV Network DesignUsama AhmedNo ratings yet

- 2007 AmuDocument85 pages2007 AmuAnindyaMustikaNo ratings yet

- Opening RemarksDocument2 pagesOpening Remarksjennelyn malayno100% (1)

- Animation Thesis FilmDocument4 pagesAnimation Thesis Filmjuliemedinaphoenix100% (2)

- Information Before Stay BFDocument7 pagesInformation Before Stay BFBrat SiostraNo ratings yet

- Freeman v. Grain Processing Corp., No. 13-0723 (Iowa June 13, 2014)Document63 pagesFreeman v. Grain Processing Corp., No. 13-0723 (Iowa June 13, 2014)RHTNo ratings yet

- De Thi Giua Ki 2 Tieng Anh 8 Global Success de So 2Document21 pagesDe Thi Giua Ki 2 Tieng Anh 8 Global Success de So 2mit maiNo ratings yet

- Level 9Document9 pagesLevel 9direcciónc_1No ratings yet

- Case Study SIFFCO AGRO Chemicals Ltd.Document3 pagesCase Study SIFFCO AGRO Chemicals Ltd.AvinaNo ratings yet

- Stone Houses of Jefferson CountyDocument240 pagesStone Houses of Jefferson CountyAs PireNo ratings yet

- Bank of IndiaDocument63 pagesBank of IndiaArmaan ChhaprooNo ratings yet

- SV - ComplaintDocument72 pagesSV - ComplaintĐỗ Trà MyNo ratings yet

- TNB and NUR Tariff DifferencesDocument2 pagesTNB and NUR Tariff DifferencesAzree Mohd NoorNo ratings yet

- Documents in Credit TransactionsDocument6 pagesDocuments in Credit Transactionsgeofrey gepitulanNo ratings yet

- Holy Spirit in Christianity - WikipediaDocument21 pagesHoly Spirit in Christianity - WikipediaSunny BautistaNo ratings yet

- Attendance DenmarkDocument3 pagesAttendance Denmarkdennis berja laguraNo ratings yet

- Purposive Communication LectureDocument70 pagesPurposive Communication LectureJericho DadoNo ratings yet

- Spectra Precision FAST Survey User ManualDocument68 pagesSpectra Precision FAST Survey User ManualAlexis Olaf Montores CuNo ratings yet

- Customs Procedure CodesDocument23 pagesCustoms Procedure CodesJonathan D'limaNo ratings yet

- Solutions To Chapter 6 Valuing StocksDocument20 pagesSolutions To Chapter 6 Valuing StocksSam TnNo ratings yet