Singapore Tax System

Singapore Tax System

You might also like

- Ross. Westerfield. Jaffe. Jordan Chapter 22 Test PDFDocument26 pagesRoss. Westerfield. Jaffe. Jordan Chapter 22 Test PDFSitti NajwaNo ratings yet

- Ross. Westerfield. Jaffe. Jordan Chapter 22 Test PDFDocument26 pagesRoss. Westerfield. Jaffe. Jordan Chapter 22 Test PDFSitti NajwaNo ratings yet

- SGV and Co Presentation On TRAIN LawDocument48 pagesSGV and Co Presentation On TRAIN LawPortCalls100% (8)

- Everything You Need To Know About Tax in Singapore (By PWC)Document64 pagesEverything You Need To Know About Tax in Singapore (By PWC)sathappan100% (1)

- SAP VAT For GCC CountryDocument16 pagesSAP VAT For GCC CountryEdith Yit50% (2)

- Solutions OptionsDocument215 pagesSolutions OptionsManton Yeung50% (2)

- Partner Program OverviewDocument19 pagesPartner Program OverviewfataiusNo ratings yet

- Business PlanDocument14 pagesBusiness PlanghadaNo ratings yet

- GST PPT June19Document65 pagesGST PPT June19yash bhushanNo ratings yet

- TAX For The Profession NIQSDocument52 pagesTAX For The Profession NIQSJoseph EzekielNo ratings yet

- Minarva Tripathi: Made byDocument52 pagesMinarva Tripathi: Made byCandy CrushNo ratings yet

- Strategic Tax Management (Final Period Assignment Quiz)Document4 pagesStrategic Tax Management (Final Period Assignment Quiz)Nelia AbellanoNo ratings yet

- Topic 6 - IndividualDocument81 pagesTopic 6 - Individualmichael krueseiNo ratings yet

- Pvt. Ltd. RegistrationDocument7 pagesPvt. Ltd. RegistrationPrakash VenkataramaniNo ratings yet

- Direct Tax BookletDocument24 pagesDirect Tax Bookletmbhartia999No ratings yet

- Angel Tax - Google SearchDocument1 pageAngel Tax - Google SearchSwayam ShubhamNo ratings yet

- GST Basic For WebsiteDocument17 pagesGST Basic For WebsiteUdit JalanNo ratings yet

- Ghanshyam 1813 PPT Public FinanceDocument64 pagesGhanshyam 1813 PPT Public FinanceShivansh JhaNo ratings yet

- GST GuideDocument48 pagesGST Guidelusifer kpNo ratings yet

- Overview of GST Model GST Law Meaning Scope of SupplyDocument47 pagesOverview of GST Model GST Law Meaning Scope of SupplyShubham More CenationNo ratings yet

- Singapore Tax System and Tax RatesDocument10 pagesSingapore Tax System and Tax RatesshafirasrjNo ratings yet

- Chapter 1Document30 pagesChapter 1Christine ChuaNo ratings yet

- GST Ebook sk-1Document89 pagesGST Ebook sk-1KunalKumarNo ratings yet

- Excise Taxes On Alcohol ProductsDocument18 pagesExcise Taxes On Alcohol ProductsChristine ChuaNo ratings yet

- Calender of EventsDocument89 pagesCalender of EventsShankar ReddyNo ratings yet

- PHD Research Bureau PHD Chamber of Commerce and IndustryDocument33 pagesPHD Research Bureau PHD Chamber of Commerce and IndustrySUNIL PUJARINo ratings yet

- Chapter 1: Introduction To Corporate Tax PlanningDocument5 pagesChapter 1: Introduction To Corporate Tax PlanningMd Manajer RoshidNo ratings yet

- Singapore Tax GuideDocument20 pagesSingapore Tax GuideTaccad ReydennNo ratings yet

- Tax Structure and Basic ConceptsDocument64 pagesTax Structure and Basic Conceptstushar_shetti100% (1)

- Fasd 2012 2016 Firs ReportDocument9 pagesFasd 2012 2016 Firs Reporthabibaamin951No ratings yet

- TAX Holidays & MAT For IT: Presentation BriefDocument12 pagesTAX Holidays & MAT For IT: Presentation BriefmuruganandammNo ratings yet

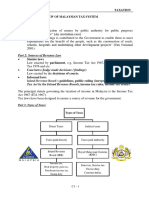

- Chapter 1 Overview of Malaysian Tax SystemDocument11 pagesChapter 1 Overview of Malaysian Tax SystemLOO YU HUANGNo ratings yet

- Topic 1 - Income Taxation-Part 1Document98 pagesTopic 1 - Income Taxation-Part 1Jaymee Andomang Os-agNo ratings yet

- Startups in India at A Glance Booklet 04-01-2023Document4 pagesStartups in India at A Glance Booklet 04-01-2023guruNo ratings yet

- Taxation-Reforms PRESENTATIONDocument17 pagesTaxation-Reforms PRESENTATIONRaman KumarNo ratings yet

- Notes For Diploma SLSP HighlightedDocument75 pagesNotes For Diploma SLSP HighlightedsameehaashrafaliNo ratings yet

- Republic Act No. 11976 (EOPT) - Infographics - SGVDocument3 pagesRepublic Act No. 11976 (EOPT) - Infographics - SGVAlbert SantiagoNo ratings yet

- Arrears of Salary - Taxability & Relief Under Section 89Document4 pagesArrears of Salary - Taxability & Relief Under Section 89SONANo ratings yet

- Tax and IPRDocument12 pagesTax and IPRMimiNo ratings yet

- Income Tax Calculator FY 2015-16 (AY 2016-17) : Particulars Details TypeDocument4 pagesIncome Tax Calculator FY 2015-16 (AY 2016-17) : Particulars Details TypeKamlesh ChauhanNo ratings yet

- GST Concept Note V1.01Document23 pagesGST Concept Note V1.01callit007No ratings yet

- FRA - 10-Income TaxesDocument35 pagesFRA - 10-Income Taxeskmayank0723No ratings yet

- 8.special Tax Rates of Companies & MATDocument22 pages8.special Tax Rates of Companies & MATMuthu nayagamNo ratings yet

- LAW Related-GST PresentationDocument137 pagesLAW Related-GST PresentationshreyasNo ratings yet

- Latar Belakang GST Di MalaysiaDocument49 pagesLatar Belakang GST Di MalaysiaBenny WeeNo ratings yet

- Goods and Services Tax (GST) : Simplified byDocument14 pagesGoods and Services Tax (GST) : Simplified bypushpendra singh sodhaNo ratings yet

- Goods and Service TaxDocument35 pagesGoods and Service Taxaditya2110No ratings yet

- Presentation On : Kiet Group of InstitutionsDocument27 pagesPresentation On : Kiet Group of InstitutionsVaishali SharmaNo ratings yet

- Presentation On : Kiet Group of InstitutionsDocument27 pagesPresentation On : Kiet Group of InstitutionsVaishali SharmaNo ratings yet

- VAT Presentation - Staff.Document36 pagesVAT Presentation - Staff.zubairNo ratings yet

- Taxation ReportDocument13 pagesTaxation ReportShivansh BhattNo ratings yet

- SAP GST - Smajo Rapid Start RoadMap V1.0Document25 pagesSAP GST - Smajo Rapid Start RoadMap V1.0satwikaNo ratings yet

- Suraj Sir 1Document8 pagesSuraj Sir 1Avinash YadavNo ratings yet

- 28-05-2017 Nagpur GST Conclave3Document203 pages28-05-2017 Nagpur GST Conclave3guptatarun2012septNo ratings yet

- GST (Good and Service TaxDocument3 pagesGST (Good and Service TaxvkNo ratings yet

- SSTPGV 1Document5 pagesSSTPGV 1api-474744842No ratings yet

- Should I Include Employer's Contribution To NPS IDocument2 pagesShould I Include Employer's Contribution To NPS IruchitssNo ratings yet

- Tax Structure in India: Income Tax Corporate Tax Central Tax State TaxDocument73 pagesTax Structure in India: Income Tax Corporate Tax Central Tax State TaxVarun VardhanNo ratings yet

- Gst-Act: Goods and Services Tax. One Nation-One TaxDocument63 pagesGst-Act: Goods and Services Tax. One Nation-One TaxKunal ChawlaNo ratings yet

- GST Audit Assessment - SNM - 15.11.19Document53 pagesGST Audit Assessment - SNM - 15.11.19GAMING WITH MADHURNo ratings yet

- Presentation ON: Goods and Service Tax: Applicability, Itc and ReturnsDocument31 pagesPresentation ON: Goods and Service Tax: Applicability, Itc and ReturnsSonal AggarwalNo ratings yet

- US Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesFrom EverandUS Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesNo ratings yet

- Topic 2 SupplementaryDocument26 pagesTopic 2 SupplementaryManton YeungNo ratings yet

- HSMC ADM (HSM50) - Items Which Were Not RenewedDocument2 pagesHSMC ADM (HSM50) - Items Which Were Not RenewedManton YeungNo ratings yet

- Put Call ExplanationDocument1 pagePut Call ExplanationManton YeungNo ratings yet

- Supplementary Exercise 1Document1 pageSupplementary Exercise 1Manton YeungNo ratings yet

- 2006 Lcci Level 3 Series 2answer 120418031555 Phpapp02Document18 pages2006 Lcci Level 3 Series 2answer 120418031555 Phpapp02Micheal ChuaNo ratings yet

- Supplementary Exercise 1Document1 pageSupplementary Exercise 1Manton YeungNo ratings yet

- Excel Practice 1Document1 pageExcel Practice 1Manton YeungNo ratings yet

- University of Sheffield PHD Thesis TemplateDocument5 pagesUniversity of Sheffield PHD Thesis Templatemonicaturnercolumbia100% (2)

- ITA Investoren PresentationDocument13 pagesITA Investoren PresentationDimitrios LiakosNo ratings yet

- Pratibimb Introductory PagesDocument7 pagesPratibimb Introductory PagesSaurabh TrivediNo ratings yet

- Application Form For Introduction of AFD-I Category ItemsDocument7 pagesApplication Form For Introduction of AFD-I Category ItemssukritgoelNo ratings yet

- Definition Essay HeroDocument4 pagesDefinition Essay Heroafibaubdfmaebo100% (2)

- 2018 Profile of International Residential Real Estate in Florida 10-25-2018Document30 pages2018 Profile of International Residential Real Estate in Florida 10-25-2018National Association of REALTORS®100% (1)

- Dynamics 365Document146 pagesDynamics 365Vishwas Yeeshwar100% (4)

- Vietnam Mobile VAS Market ReviewDocument30 pagesVietnam Mobile VAS Market ReviewNguyen Minh QuangNo ratings yet

- E. Sharath Babu, Founder & CEO, Food King: Entrepreneurs Non-Tech EntrepreneursDocument3 pagesE. Sharath Babu, Founder & CEO, Food King: Entrepreneurs Non-Tech Entrepreneurssundar666No ratings yet

- RPS ARS 201 Hospital LeadershipDocument9 pagesRPS ARS 201 Hospital LeadershiprajabNo ratings yet

- Jignesh Jethva - 124703803Document4 pagesJignesh Jethva - 124703803asdasdNo ratings yet

- Problem Set 1Document5 pagesProblem Set 1sxmmmNo ratings yet

- Development And Application Of Mobile Banking Concept: ТEME, г. XLI, бр. 2, априлDocument3 pagesDevelopment And Application Of Mobile Banking Concept: ТEME, г. XLI, бр. 2, априлKimberly ManradgeNo ratings yet

- Free PEST Market Analysis Template and Method, Free Pest Market Analysis ExamplesDocument7 pagesFree PEST Market Analysis Template and Method, Free Pest Market Analysis ExamplesWerner SchrammelNo ratings yet

- Mott MacDonald Case Study AnalysisDocument18 pagesMott MacDonald Case Study AnalysisIrah Dania MontesclarosNo ratings yet

- EBP 03-Activity-1Document2 pagesEBP 03-Activity-1Levi AckermanNo ratings yet

- Maintenance Planning Standard - Book - PT Freeport McMoran 2009 - Final v.1.6Document431 pagesMaintenance Planning Standard - Book - PT Freeport McMoran 2009 - Final v.1.6Bayu SudarsonoNo ratings yet

- UBL CSR ReportDocument38 pagesUBL CSR ReportTalha E100% (1)

- Functions of Entrepreneur: Assumption of Risk Business Decision Making Managerial Functions Function of InnovationDocument32 pagesFunctions of Entrepreneur: Assumption of Risk Business Decision Making Managerial Functions Function of Innovationarchana_sree13No ratings yet

- Ponzi SchemeDocument4 pagesPonzi SchemeLaudArchNo ratings yet

- Distribution ChannelDocument38 pagesDistribution ChannelSomalKantNo ratings yet

- NirmaDocument87 pagesNirmaJamila KhokharNo ratings yet

- Bibliography FINALDocument5 pagesBibliography FINALMina Klee ChapmanNo ratings yet

- Positioning and Targeting of Ichiban ShiboriDocument5 pagesPositioning and Targeting of Ichiban ShiboriRonil JainNo ratings yet

- All Kinds of SoilDocument7 pagesAll Kinds of SoilPujari Appala NaiduNo ratings yet

- Marketing Management Question Bank For MidDocument5 pagesMarketing Management Question Bank For Middynamo vjNo ratings yet

- Texmaco HiTech Presentation-AlstomDocument18 pagesTexmaco HiTech Presentation-AlstomANIRBANNo ratings yet

- AssignmentDocument8 pagesAssignmentNatalie Andria Weeramanthri100% (1)

- The Most Frequently Used Transaction Codes Are As FollowsDocument15 pagesThe Most Frequently Used Transaction Codes Are As FollowsJitender DalalNo ratings yet

Download as pptx, pdf, or txt

You might also like

- Ross. Westerfield. Jaffe. Jordan Chapter 22 Test PDFDocument26 pagesRoss. Westerfield. Jaffe. Jordan Chapter 22 Test PDFSitti NajwaNo ratings yet

- Ross. Westerfield. Jaffe. Jordan Chapter 22 Test PDFDocument26 pagesRoss. Westerfield. Jaffe. Jordan Chapter 22 Test PDFSitti NajwaNo ratings yet

- SGV and Co Presentation On TRAIN LawDocument48 pagesSGV and Co Presentation On TRAIN LawPortCalls100% (8)

- Everything You Need To Know About Tax in Singapore (By PWC)Document64 pagesEverything You Need To Know About Tax in Singapore (By PWC)sathappan100% (1)

- SAP VAT For GCC CountryDocument16 pagesSAP VAT For GCC CountryEdith Yit50% (2)

- Solutions OptionsDocument215 pagesSolutions OptionsManton Yeung50% (2)

- Partner Program OverviewDocument19 pagesPartner Program OverviewfataiusNo ratings yet

- Business PlanDocument14 pagesBusiness PlanghadaNo ratings yet

- GST PPT June19Document65 pagesGST PPT June19yash bhushanNo ratings yet

- TAX For The Profession NIQSDocument52 pagesTAX For The Profession NIQSJoseph EzekielNo ratings yet

- Minarva Tripathi: Made byDocument52 pagesMinarva Tripathi: Made byCandy CrushNo ratings yet

- Strategic Tax Management (Final Period Assignment Quiz)Document4 pagesStrategic Tax Management (Final Period Assignment Quiz)Nelia AbellanoNo ratings yet

- Topic 6 - IndividualDocument81 pagesTopic 6 - Individualmichael krueseiNo ratings yet

- Pvt. Ltd. RegistrationDocument7 pagesPvt. Ltd. RegistrationPrakash VenkataramaniNo ratings yet

- Direct Tax BookletDocument24 pagesDirect Tax Bookletmbhartia999No ratings yet

- Angel Tax - Google SearchDocument1 pageAngel Tax - Google SearchSwayam ShubhamNo ratings yet

- GST Basic For WebsiteDocument17 pagesGST Basic For WebsiteUdit JalanNo ratings yet

- Ghanshyam 1813 PPT Public FinanceDocument64 pagesGhanshyam 1813 PPT Public FinanceShivansh JhaNo ratings yet

- GST GuideDocument48 pagesGST Guidelusifer kpNo ratings yet

- Overview of GST Model GST Law Meaning Scope of SupplyDocument47 pagesOverview of GST Model GST Law Meaning Scope of SupplyShubham More CenationNo ratings yet

- Singapore Tax System and Tax RatesDocument10 pagesSingapore Tax System and Tax RatesshafirasrjNo ratings yet

- Chapter 1Document30 pagesChapter 1Christine ChuaNo ratings yet

- GST Ebook sk-1Document89 pagesGST Ebook sk-1KunalKumarNo ratings yet

- Excise Taxes On Alcohol ProductsDocument18 pagesExcise Taxes On Alcohol ProductsChristine ChuaNo ratings yet

- Calender of EventsDocument89 pagesCalender of EventsShankar ReddyNo ratings yet

- PHD Research Bureau PHD Chamber of Commerce and IndustryDocument33 pagesPHD Research Bureau PHD Chamber of Commerce and IndustrySUNIL PUJARINo ratings yet

- Chapter 1: Introduction To Corporate Tax PlanningDocument5 pagesChapter 1: Introduction To Corporate Tax PlanningMd Manajer RoshidNo ratings yet

- Singapore Tax GuideDocument20 pagesSingapore Tax GuideTaccad ReydennNo ratings yet

- Tax Structure and Basic ConceptsDocument64 pagesTax Structure and Basic Conceptstushar_shetti100% (1)

- Fasd 2012 2016 Firs ReportDocument9 pagesFasd 2012 2016 Firs Reporthabibaamin951No ratings yet

- TAX Holidays & MAT For IT: Presentation BriefDocument12 pagesTAX Holidays & MAT For IT: Presentation BriefmuruganandammNo ratings yet

- Chapter 1 Overview of Malaysian Tax SystemDocument11 pagesChapter 1 Overview of Malaysian Tax SystemLOO YU HUANGNo ratings yet

- Topic 1 - Income Taxation-Part 1Document98 pagesTopic 1 - Income Taxation-Part 1Jaymee Andomang Os-agNo ratings yet

- Startups in India at A Glance Booklet 04-01-2023Document4 pagesStartups in India at A Glance Booklet 04-01-2023guruNo ratings yet

- Taxation-Reforms PRESENTATIONDocument17 pagesTaxation-Reforms PRESENTATIONRaman KumarNo ratings yet

- Notes For Diploma SLSP HighlightedDocument75 pagesNotes For Diploma SLSP HighlightedsameehaashrafaliNo ratings yet

- Republic Act No. 11976 (EOPT) - Infographics - SGVDocument3 pagesRepublic Act No. 11976 (EOPT) - Infographics - SGVAlbert SantiagoNo ratings yet

- Arrears of Salary - Taxability & Relief Under Section 89Document4 pagesArrears of Salary - Taxability & Relief Under Section 89SONANo ratings yet

- Tax and IPRDocument12 pagesTax and IPRMimiNo ratings yet

- Income Tax Calculator FY 2015-16 (AY 2016-17) : Particulars Details TypeDocument4 pagesIncome Tax Calculator FY 2015-16 (AY 2016-17) : Particulars Details TypeKamlesh ChauhanNo ratings yet

- GST Concept Note V1.01Document23 pagesGST Concept Note V1.01callit007No ratings yet

- FRA - 10-Income TaxesDocument35 pagesFRA - 10-Income Taxeskmayank0723No ratings yet

- 8.special Tax Rates of Companies & MATDocument22 pages8.special Tax Rates of Companies & MATMuthu nayagamNo ratings yet

- LAW Related-GST PresentationDocument137 pagesLAW Related-GST PresentationshreyasNo ratings yet

- Latar Belakang GST Di MalaysiaDocument49 pagesLatar Belakang GST Di MalaysiaBenny WeeNo ratings yet

- Goods and Services Tax (GST) : Simplified byDocument14 pagesGoods and Services Tax (GST) : Simplified bypushpendra singh sodhaNo ratings yet

- Goods and Service TaxDocument35 pagesGoods and Service Taxaditya2110No ratings yet

- Presentation On : Kiet Group of InstitutionsDocument27 pagesPresentation On : Kiet Group of InstitutionsVaishali SharmaNo ratings yet

- Presentation On : Kiet Group of InstitutionsDocument27 pagesPresentation On : Kiet Group of InstitutionsVaishali SharmaNo ratings yet

- VAT Presentation - Staff.Document36 pagesVAT Presentation - Staff.zubairNo ratings yet

- Taxation ReportDocument13 pagesTaxation ReportShivansh BhattNo ratings yet

- SAP GST - Smajo Rapid Start RoadMap V1.0Document25 pagesSAP GST - Smajo Rapid Start RoadMap V1.0satwikaNo ratings yet

- Suraj Sir 1Document8 pagesSuraj Sir 1Avinash YadavNo ratings yet

- 28-05-2017 Nagpur GST Conclave3Document203 pages28-05-2017 Nagpur GST Conclave3guptatarun2012septNo ratings yet

- GST (Good and Service TaxDocument3 pagesGST (Good and Service TaxvkNo ratings yet

- SSTPGV 1Document5 pagesSSTPGV 1api-474744842No ratings yet

- Should I Include Employer's Contribution To NPS IDocument2 pagesShould I Include Employer's Contribution To NPS IruchitssNo ratings yet

- Tax Structure in India: Income Tax Corporate Tax Central Tax State TaxDocument73 pagesTax Structure in India: Income Tax Corporate Tax Central Tax State TaxVarun VardhanNo ratings yet

- Gst-Act: Goods and Services Tax. One Nation-One TaxDocument63 pagesGst-Act: Goods and Services Tax. One Nation-One TaxKunal ChawlaNo ratings yet

- GST Audit Assessment - SNM - 15.11.19Document53 pagesGST Audit Assessment - SNM - 15.11.19GAMING WITH MADHURNo ratings yet

- Presentation ON: Goods and Service Tax: Applicability, Itc and ReturnsDocument31 pagesPresentation ON: Goods and Service Tax: Applicability, Itc and ReturnsSonal AggarwalNo ratings yet

- US Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesFrom EverandUS Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesNo ratings yet

- Topic 2 SupplementaryDocument26 pagesTopic 2 SupplementaryManton YeungNo ratings yet

- HSMC ADM (HSM50) - Items Which Were Not RenewedDocument2 pagesHSMC ADM (HSM50) - Items Which Were Not RenewedManton YeungNo ratings yet

- Put Call ExplanationDocument1 pagePut Call ExplanationManton YeungNo ratings yet

- Supplementary Exercise 1Document1 pageSupplementary Exercise 1Manton YeungNo ratings yet

- 2006 Lcci Level 3 Series 2answer 120418031555 Phpapp02Document18 pages2006 Lcci Level 3 Series 2answer 120418031555 Phpapp02Micheal ChuaNo ratings yet

- Supplementary Exercise 1Document1 pageSupplementary Exercise 1Manton YeungNo ratings yet

- Excel Practice 1Document1 pageExcel Practice 1Manton YeungNo ratings yet

- University of Sheffield PHD Thesis TemplateDocument5 pagesUniversity of Sheffield PHD Thesis Templatemonicaturnercolumbia100% (2)

- ITA Investoren PresentationDocument13 pagesITA Investoren PresentationDimitrios LiakosNo ratings yet

- Pratibimb Introductory PagesDocument7 pagesPratibimb Introductory PagesSaurabh TrivediNo ratings yet

- Application Form For Introduction of AFD-I Category ItemsDocument7 pagesApplication Form For Introduction of AFD-I Category ItemssukritgoelNo ratings yet

- Definition Essay HeroDocument4 pagesDefinition Essay Heroafibaubdfmaebo100% (2)

- 2018 Profile of International Residential Real Estate in Florida 10-25-2018Document30 pages2018 Profile of International Residential Real Estate in Florida 10-25-2018National Association of REALTORS®100% (1)

- Dynamics 365Document146 pagesDynamics 365Vishwas Yeeshwar100% (4)

- Vietnam Mobile VAS Market ReviewDocument30 pagesVietnam Mobile VAS Market ReviewNguyen Minh QuangNo ratings yet

- E. Sharath Babu, Founder & CEO, Food King: Entrepreneurs Non-Tech EntrepreneursDocument3 pagesE. Sharath Babu, Founder & CEO, Food King: Entrepreneurs Non-Tech Entrepreneurssundar666No ratings yet

- RPS ARS 201 Hospital LeadershipDocument9 pagesRPS ARS 201 Hospital LeadershiprajabNo ratings yet

- Jignesh Jethva - 124703803Document4 pagesJignesh Jethva - 124703803asdasdNo ratings yet

- Problem Set 1Document5 pagesProblem Set 1sxmmmNo ratings yet

- Development And Application Of Mobile Banking Concept: ТEME, г. XLI, бр. 2, априлDocument3 pagesDevelopment And Application Of Mobile Banking Concept: ТEME, г. XLI, бр. 2, априлKimberly ManradgeNo ratings yet

- Free PEST Market Analysis Template and Method, Free Pest Market Analysis ExamplesDocument7 pagesFree PEST Market Analysis Template and Method, Free Pest Market Analysis ExamplesWerner SchrammelNo ratings yet

- Mott MacDonald Case Study AnalysisDocument18 pagesMott MacDonald Case Study AnalysisIrah Dania MontesclarosNo ratings yet

- EBP 03-Activity-1Document2 pagesEBP 03-Activity-1Levi AckermanNo ratings yet

- Maintenance Planning Standard - Book - PT Freeport McMoran 2009 - Final v.1.6Document431 pagesMaintenance Planning Standard - Book - PT Freeport McMoran 2009 - Final v.1.6Bayu SudarsonoNo ratings yet

- UBL CSR ReportDocument38 pagesUBL CSR ReportTalha E100% (1)

- Functions of Entrepreneur: Assumption of Risk Business Decision Making Managerial Functions Function of InnovationDocument32 pagesFunctions of Entrepreneur: Assumption of Risk Business Decision Making Managerial Functions Function of Innovationarchana_sree13No ratings yet

- Ponzi SchemeDocument4 pagesPonzi SchemeLaudArchNo ratings yet

- Distribution ChannelDocument38 pagesDistribution ChannelSomalKantNo ratings yet

- NirmaDocument87 pagesNirmaJamila KhokharNo ratings yet

- Bibliography FINALDocument5 pagesBibliography FINALMina Klee ChapmanNo ratings yet

- Positioning and Targeting of Ichiban ShiboriDocument5 pagesPositioning and Targeting of Ichiban ShiboriRonil JainNo ratings yet

- All Kinds of SoilDocument7 pagesAll Kinds of SoilPujari Appala NaiduNo ratings yet

- Marketing Management Question Bank For MidDocument5 pagesMarketing Management Question Bank For Middynamo vjNo ratings yet

- Texmaco HiTech Presentation-AlstomDocument18 pagesTexmaco HiTech Presentation-AlstomANIRBANNo ratings yet

- AssignmentDocument8 pagesAssignmentNatalie Andria Weeramanthri100% (1)

- The Most Frequently Used Transaction Codes Are As FollowsDocument15 pagesThe Most Frequently Used Transaction Codes Are As FollowsJitender DalalNo ratings yet