Download as ppt, pdf, or txt

You might also like

- CH - 02 - Cost Terms, Concepts and Classifications With Mixed Cost AnalysisDocument84 pagesCH - 02 - Cost Terms, Concepts and Classifications With Mixed Cost AnalysisankonmahmudNo ratings yet

- Gann RRR Technical AnalysisDocument57 pagesGann RRR Technical AnalysisThiru Shankar100% (5)

- Philippe Van Parijs - What (If Anything) Is Intrinsically Wrong With Capitalism (1984)Document18 pagesPhilippe Van Parijs - What (If Anything) Is Intrinsically Wrong With Capitalism (1984)guilmoura100% (1)

- Bua108 Ch06 Higgins QuizDocument7 pagesBua108 Ch06 Higgins QuizAlberto Barocio0% (1)

- Cost Term, Concept and ClassificationsDocument28 pagesCost Term, Concept and ClassificationskumarNo ratings yet

- Chapter 02 - Cost Term and Concepts FinalDocument60 pagesChapter 02 - Cost Term and Concepts FinalAminaMatinNo ratings yet

- Act 202 Chapter 2Document52 pagesAct 202 Chapter 2Shaon KhanNo ratings yet

- Managerial Accounting and Cost Concepts: Chapter TwoDocument63 pagesManagerial Accounting and Cost Concepts: Chapter TwoMd Hasibul Karim 1811766630No ratings yet

- Cost Terms, Concepts, and ClassificationsDocument22 pagesCost Terms, Concepts, and ClassificationsKi xxiNo ratings yet

- Cost Terms, Concepts, and ClassificationDocument27 pagesCost Terms, Concepts, and ClassificationParadise VillageNo ratings yet

- Managerial Accounting and Cost ConceptsDocument50 pagesManagerial Accounting and Cost ConceptsGigo Kafare BinoNo ratings yet

- Chapter 01 BGN7eDocument62 pagesChapter 01 BGN7enhittm59.fbaeliteNo ratings yet

- Cost Accounting Concepts: Prof. Dr. Farid MoharamDocument90 pagesCost Accounting Concepts: Prof. Dr. Farid Moharammohamed el kadyNo ratings yet

- CH 02Document40 pagesCH 02lyonanh289No ratings yet

- Chapter 2 - Managerial Acc. & Cost ConceptsDocument23 pagesChapter 2 - Managerial Acc. & Cost ConceptsMuhammad Ali KazmiNo ratings yet

- Cost ConceptsDocument56 pagesCost ConceptsAngela De chavezNo ratings yet

- Managerial Accounting and Cost Concepts: Mcgraw-Hill/IrwinDocument55 pagesManagerial Accounting and Cost Concepts: Mcgraw-Hill/IrwinWaqas HussainNo ratings yet

- Session 2 - MAC - ConceptsDocument33 pagesSession 2 - MAC - ConceptsABHASH JHANo ratings yet

- Managerial Accounting and Cost ConceptsDocument48 pagesManagerial Accounting and Cost ConceptsKirei MinaNo ratings yet

- Basic Cost ConceptDocument43 pagesBasic Cost ConceptAaron WidofanNo ratings yet

- Management Accounting: Product CostingDocument22 pagesManagement Accounting: Product CostingDaksh AnejaNo ratings yet

- Chapter - 2 - Managerial Accounting and Cost ConceptDocument61 pagesChapter - 2 - Managerial Accounting and Cost ConceptSoka PokaNo ratings yet

- Garrison Lecture Chapter 2Document61 pagesGarrison Lecture Chapter 2Ahmad Tawfiq Darabseh100% (2)

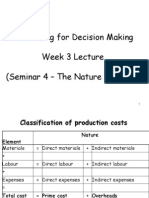

- Accounting For Decision Making Week 3 Lecture (Seminar 4 - The Nature of Costs)Document51 pagesAccounting For Decision Making Week 3 Lecture (Seminar 4 - The Nature of Costs)nwcbenny337No ratings yet

- 1a Cost Classification Form Manufacturing PT of View and Predicting Cost Behaviour - 19 - 12 - 2023Document12 pages1a Cost Classification Form Manufacturing PT of View and Predicting Cost Behaviour - 19 - 12 - 2023Md Rashadul IslamNo ratings yet

- Cost Concept and ClassificationDocument45 pagesCost Concept and ClassificationMountaha0% (1)

- Brewer 8e PPT Ch01 TDocument54 pagesBrewer 8e PPT Ch01 TJuan Camilo IdarragaNo ratings yet

- Cost Defined: Introduction To Cost Accounting, Cost Concepts, Cost Behavior Analysis and Cost Accounting CycleDocument4 pagesCost Defined: Introduction To Cost Accounting, Cost Concepts, Cost Behavior Analysis and Cost Accounting Cyclecriselyn agtingNo ratings yet

- Managerial Accounting and Cost ConceptsDocument18 pagesManagerial Accounting and Cost ConceptsrisaNo ratings yet

- Week 2-Basic Cost ManagementDocument21 pagesWeek 2-Basic Cost ManagementRichard Oliver CortezNo ratings yet

- Managerial Accounting and Cost ConceptsDocument61 pagesManagerial Accounting and Cost ConceptsAmer Wagdy GergesNo ratings yet

- Cost Accounting Foundations and Evolutions 8th Edition Kinney Solutions ManualDocument23 pagesCost Accounting Foundations and Evolutions 8th Edition Kinney Solutions Manualatwovarusbbn8d100% (25)

- Chapter 2 UpdatedDocument58 pagesChapter 2 Updatedbing bongNo ratings yet

- Managerial Accounting and Cost ConceptsDocument61 pagesManagerial Accounting and Cost ConceptsFederico SalernoNo ratings yet

- Managerial Accounting and Cost ConceptsDocument62 pagesManagerial Accounting and Cost ConceptsJuana BoresNo ratings yet

- SPPTChap 002Document16 pagesSPPTChap 002saharinshakib7505No ratings yet

- Managerial Accounting and Cost ConceptsDocument19 pagesManagerial Accounting and Cost ConceptsFarhan RabbehNo ratings yet

- 1b - Cost Concepts and Terminology - 14sept06Document31 pages1b - Cost Concepts and Terminology - 14sept06Zaid AnsariNo ratings yet

- Cost AccountingDocument39 pagesCost AccountingMian Abdullah MukhdoomNo ratings yet

- Cost Accounting Foundations and Evolutions 9th Edition Kinney Solutions ManualDocument36 pagesCost Accounting Foundations and Evolutions 9th Edition Kinney Solutions Manualatwovarusbbn8d100% (24)

- Dwnload Full Cost Accounting Foundations and Evolutions 9th Edition Kinney Solutions Manual PDFDocument36 pagesDwnload Full Cost Accounting Foundations and Evolutions 9th Edition Kinney Solutions Manual PDFleroyweavervpgnrf100% (17)

- 10632m Lecture 6 - Full Costing I (Full Version)Document53 pages10632m Lecture 6 - Full Costing I (Full Version)kammiefan215No ratings yet

- Lec 02 - Managerial Accounting (Concepts & Principles)Document35 pagesLec 02 - Managerial Accounting (Concepts & Principles)Mhuthasim Ahmed EmonNo ratings yet

- Chapter 3 - Virtual - Classroom-M.Document61 pagesChapter 3 - Virtual - Classroom-M.rebeccahf7No ratings yet

- Chapter 2 Managerial Accounting and Cost ConceptsDocument49 pagesChapter 2 Managerial Accounting and Cost ConceptsFarihaNo ratings yet

- Classification of CostsDocument2 pagesClassification of CostsBeatrize ValerioNo ratings yet

- Chapter 2 Cost Accounting ConceptsDocument22 pagesChapter 2 Cost Accounting ConceptsRosliana RazabNo ratings yet

- Cost Accounting Foundations and Evolutions 8th Edition Kinney Solutions ManualDocument26 pagesCost Accounting Foundations and Evolutions 8th Edition Kinney Solutions ManualToniSmithmozr100% (53)

- Latest Cost AccountingDocument128 pagesLatest Cost AccountingMian Abdullah MukhdoomNo ratings yet

- Acct Cost ConceptsDocument52 pagesAcct Cost ConceptsLauNo ratings yet

- Topic 2 IDocument16 pagesTopic 2 Iami zawaniNo ratings yet

- Classification of CostDocument33 pagesClassification of CostGeet SharmaNo ratings yet

- MS 2Document8 pagesMS 2gabprems11No ratings yet

- Managerial Accounting and Cost ConceptsDocument18 pagesManagerial Accounting and Cost ConceptsadamNo ratings yet

- Managerial Accounting and Cost ConceptsDocument44 pagesManagerial Accounting and Cost ConceptsQUANG NGUYỄN VINHNo ratings yet

- Introduction To Managerial Accounting Canadian 5th Edition Brewer Solutions ManualDocument25 pagesIntroduction To Managerial Accounting Canadian 5th Edition Brewer Solutions ManualMaryJohnsonsmni100% (60)

- Cost Concepts HandoutsDocument13 pagesCost Concepts HandoutsTushar DuaNo ratings yet

- Chapter 2-Cost ClassificationDocument66 pagesChapter 2-Cost Classification040404.anniNo ratings yet

- CH 2Document35 pagesCH 2nigoxiy168No ratings yet

- Cost - Pa2 - Ligawad, Melody-Bsa 2CDocument6 pagesCost - Pa2 - Ligawad, Melody-Bsa 2CLIGAWAD, MELODY P.No ratings yet

- Management Accounting Strategy Study Resource for CIMA Students: CIMA Study ResourcesFrom EverandManagement Accounting Strategy Study Resource for CIMA Students: CIMA Study ResourcesNo ratings yet

- Management Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageFrom EverandManagement Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageRating: 5 out of 5 stars5/5 (1)

- Cultural Intelligence:: A Key Competence For Managers in A Diverse and Global WorkplaceDocument29 pagesCultural Intelligence:: A Key Competence For Managers in A Diverse and Global WorkplaceLim Jie XiNo ratings yet

- Presentatie 5 Tcm258-111141Document29 pagesPresentatie 5 Tcm258-111141Lim Jie XiNo ratings yet

- 3208 Intro To MA On BBDocument24 pages3208 Intro To MA On BBLim Jie XiNo ratings yet

- Chapter 8 - Training and Developing EmployeesDocument8 pagesChapter 8 - Training and Developing EmployeesLim Jie XiNo ratings yet

- Assignment 4Document3 pagesAssignment 4Tahmina RemiNo ratings yet

- FINS3616 Week 10 TutorialDocument27 pagesFINS3616 Week 10 TutorialMartinNo ratings yet

- Tata Nano BCGDocument3 pagesTata Nano BCGpralabh88No ratings yet

- Griffin IB6e PPT 01BDocument28 pagesGriffin IB6e PPT 01Basad_91No ratings yet

- MG 2451 Engineering Economics & Cost Analysis: Production and Operations Management - R B Khanna © Prentice Hall IndiaDocument91 pagesMG 2451 Engineering Economics & Cost Analysis: Production and Operations Management - R B Khanna © Prentice Hall IndiararaNo ratings yet

- Sale ProclamationDocument2 pagesSale ProclamationGoutam KumarNo ratings yet

- Homework 2 Group A and CDocument1 pageHomework 2 Group A and CGabriel FernandesNo ratings yet

- Ga Draft ICPODocument2 pagesGa Draft ICPOAmiruddin IslamNo ratings yet

- Volatility Trading System Rules PDFDocument6 pagesVolatility Trading System Rules PDFprathapnomulaNo ratings yet

- Mortgages: Additional Concepts, Analysis, and Applications: Mcgraw-Hill/IrwinDocument32 pagesMortgages: Additional Concepts, Analysis, and Applications: Mcgraw-Hill/IrwinTam NguyenNo ratings yet

- Hull: Options, Futures, and Other Derivatives, Ninth Edition Chapter 2: Mechanics of Futures Markets Multiple Choice Test Bank: Question With AnswersDocument2 pagesHull: Options, Futures, and Other Derivatives, Ninth Edition Chapter 2: Mechanics of Futures Markets Multiple Choice Test Bank: Question With Answersnew england brickNo ratings yet

- The Free Rider Problem of Anarchism and National DefenseDocument17 pagesThe Free Rider Problem of Anarchism and National DefenseJohns EgoNo ratings yet

- Direct Compensation-Human Resource Management by Wayne MondyDocument11 pagesDirect Compensation-Human Resource Management by Wayne MondyMaqsood BrohiNo ratings yet

- A Descriptive Study About The Struggles of A Beginner in Online Home Based Bakery On Making Their Product Costing During Pandemic Year 2020-2021Document4 pagesA Descriptive Study About The Struggles of A Beginner in Online Home Based Bakery On Making Their Product Costing During Pandemic Year 2020-2021Dale CastroNo ratings yet

- Role of SEBI in Secondary MarketDocument14 pagesRole of SEBI in Secondary MarketMithlesh Singh57% (7)

- SCO-06 FeeSched Rev22Document1 pageSCO-06 FeeSched Rev22Micky PlumbNo ratings yet

- Bodie 11e Ch24 AccessibleDocument51 pagesBodie 11e Ch24 AccessibleNagatoOzomaki100% (1)

- APIRCode List For MLCDocument10 pagesAPIRCode List For MLCBrad AndersonNo ratings yet

- Chapter 19 Dividends and Other PayoutsDocument28 pagesChapter 19 Dividends and Other PayoutsHUONG NGUYEN VU QUYNHNo ratings yet

- Submitted By: Haritha K Roll No: 4912 (Mcom 3 Semester) : Topic: DumpingDocument6 pagesSubmitted By: Haritha K Roll No: 4912 (Mcom 3 Semester) : Topic: DumpingJohn HonnaiNo ratings yet

- Crocs Inc.: Team MembersDocument6 pagesCrocs Inc.: Team MembersKshitishNo ratings yet

- Micro & Macro EconomicsDocument8 pagesMicro & Macro Economicsadnantariq_2004100% (1)

- A New Era of Currency Derivatives Market in India: Dr. E.V.P.A.S.PallaviDocument5 pagesA New Era of Currency Derivatives Market in India: Dr. E.V.P.A.S.PallavirommelNo ratings yet

- DVB IIMA Case StudyDocument56 pagesDVB IIMA Case StudyMitesh KumarNo ratings yet

- Assignment 5 EconDocument3 pagesAssignment 5 EconSheen CatayongNo ratings yet

- 14 DEC 09 Mercedes-Benz Price ListDocument22 pages14 DEC 09 Mercedes-Benz Price ListhelosmdnNo ratings yet

- Chapter 7: Engineering EconomicsDocument1 pageChapter 7: Engineering EconomicsFrancisNo ratings yet